Crypto derivatives trading has moved well beyond a small group of futures-heavy exchanges. This guide compares centralized and on-chain platforms for perpetuals, dated futures, and options, with a close focus on fees, liquidity, risk controls, and access.

Availability still depends on region, legal entity, and product line, so a platform that offers perps in one market may offer only spot or limited derivatives in another.

Centralized exchanges still lead on fiat access, deeper order books, and broader derivatives tooling. Decentralized platforms have pushed perps further on-chain, with wallet-based access, different custody trade-offs, and faster product iteration.

Start by cutting the list down to platforms you can actually use where you live. Then compare product fit — perps, futures, or options — before looking at real trading costs, funding behavior, liquidity depth, leverage controls, and the margin model you are comfortable using.

Top Crypto Exchanges for Derivatives

- US-listed public company (NASDAQ: COIN)

- ~98% of crypto held in cold storage

- US-regulated perpetual futures

- User-verifiable Merkle proof of reserves

- Among the lowest pro fees in the US

- No customer-fund hack since 2011

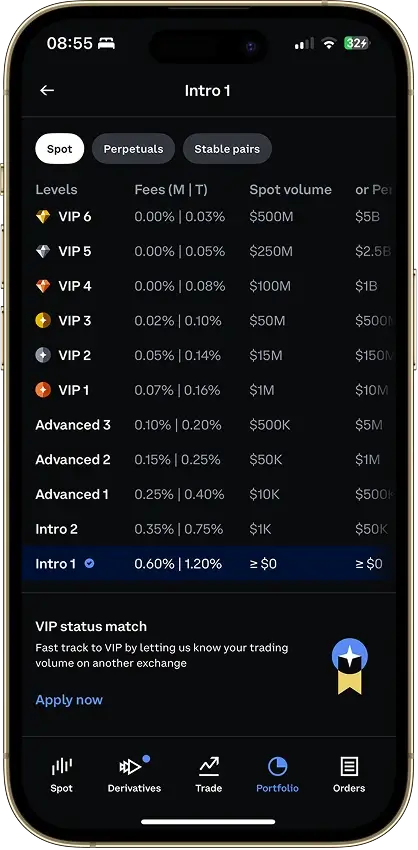

- Low, published spot and perps fees with VIP tiers

- Perpetuals and USDC options with advanced order controls

- Monthly proof of reserves with user‑verifiable Merkle checks

- Derivatives and copy trading are core products.

- Spot fees start at 0.1% maker/taker, or 0.08% with BGB fee deduction.

- USDT withdrawals support several low-cost networks.

- Licensed US relaunch with clear PoR

- Wallet and exchange under one login

- Deep global toolset for bots and copy trades

- Mature fiat bridge with exchange-first tooling

- Detailed public API, WebSocket & FIX docs

- Spot + perpetual markets, no bloated retail stack

- $750M+ cold-storage asset insurance

- ISO, SOC 2, and PCI DSS certified

- Visa card rewards via CRO staking

- 0% maker fee on all spot pairs, for every user

- FinCEN MSB and state money-transmitter licensed

- IRS 1099 tax reporting built in

This market breaks cleanly between account-based exchanges and wallet-based perpetual venues. Centralized platforms still do more on fiat access, support, and broader derivatives menus. Onchain platforms have become credible trading venues in their own right, but they suit a more self-directed trader.

Access narrows the field faster than any ranking does. After that, the shortlist comes down to liquidity on the pairs you actually trade, total cost once fees and funding are combined, margin design, and how clearly the platform handles risk controls.

Venue type matters more here than a clean split between two separate tables. Putting the main brands in one view makes it easier to compare product scope, leverage, collateral, and access without losing the centralized-versus-decentralized distinction.

Comparison Table

| Name | Total Assets | Products | Staking | Trading fees (low) | Trading fees (high) |

|---|---|---|---|---|---|

| | 270 | Spot, Futures or Perps, OTC, Simple-buy Broker | Yes | 0.00 | 0.60 |

| | 500 | Spot, Margin, Futures or Perps, OTC, Simple-buy Broker | Yes | 0.00 | 0.40 |

| | 350 | Spot, Margin, Futures or Perps, Options, OTC, Simple-buy Broker | Yes | 0.00 | 0.10 |

| | 600 | Spot, Margin, Futures or Perps, OTC, Simple-buy Broker | Yes | 0.00 | 0.10 |

| | 295 | Spot, Margin, Futures or Perps, Options, OTC, Simple-buy Broker | Yes | 0.02 | 0.35 |

| | 107 | Spot, Futures or Perps, OTC | Yes | 0.00 | 0.40 |

| | 438 | Spot, Margin, Futures or Perps, Options, OTC, Simple-buy Broker | Yes | 0.00 | 0.50 |

| | 190 | Spot | Yes | 0 | 0.02 |

Venue type changes the decision more than the brand count does. Centralized names are still stronger on onboarding, support, and broader product depth. Decentralized names are stronger on self-custody, direct wallet flows, and DeFi-native perpetual design. Traders who want a wider market view beyond derivatives can use broader exchange coverage.

Crypto Exchanges for Derivatives Reviews

Coinbase

Pros

- SEC filings show more than a Merkle-tree snapshot

- Native USDC with near-free withdrawals on Base

- Free ACH and instant RTP cash-out

- Among the largest US spot venues

- Clean tax exports and CoinTracker link

Cons

- Simple buy carries a heavy spread

- Support is slow without Coinbase One

- Account locks are a recurring complaint

- New-fund staking paused in 4 states

Kraken

Pros

- User-checkable Merkle proof of reserves

- Kraken Pro fees undercut most US rivals

- 14 years with no customer-fund hack

- 24/7 live chat for routine issues

- Wyoming bank charter for legal clarity

Cons

- Long holds on ACH and new addresses

- Pro interface is steep for beginners

- Account closures can lack a stated reason

- Staking limited to select US states

Bybit

Pros

- Low, transparent fee schedule on spot, perps, and options with VIP discounts

- Advanced suite: perps, USDC options, copy trading, bots, and OTC

- Fast crypto withdrawals with instant processing windows

- Ongoing proof of reserves with user‑side verification

- Broad P2P and card coverage for on‑ramping in many countries

Cons

- Unavailable in major markets (U.S., U.K., Canada, Singapore, and others)

- Fiat rails depend on third‑party providers and vary by country

- High leverage raises risk for new traders

- Card and some Earn products limited to specific regions

Bitget

Pros

- Futures, spot, margin, bots, and Earn are all in one account.

- Copy trading covers futures, spot, and bots, not just one market type.

- Bitget Onchain lets users access some onchain tokens without setting up a separate wallet.

- USDT withdrawals work across several affordable networks, including TRC20, BEP20, Polygon, Arbitrum, and Optimism.

- Monthly reserve reports let users verify their balance is included in the snapshot.

Cons

- Bitget blocks users in the U.S. and several other major markets.

- Simple buys and Convert trades can include a hidden spread cost.

- Using BGB for fee discounts means holding a token whose price can move against you.

- The reserve report is not a full audit of the company's finances.

- The app can feel cluttered for anyone who just wants to buy and hold.

OKX

Pros

- US entity licensed in 48 states plus Puerto Rico

- Free ACH deposits, plus wire & debit-card funding

- Monthly zk-STARK proof of reserves you verify

- On-chain staking for US users: ETH, SOL, ADA+

Cons

- No derivatives, margin or futures; NY & TX out

- Too many surfaces for simple buy-and-hold

- Card and checkout fees vary and lack clarity

- Account reviews can freeze funds for days

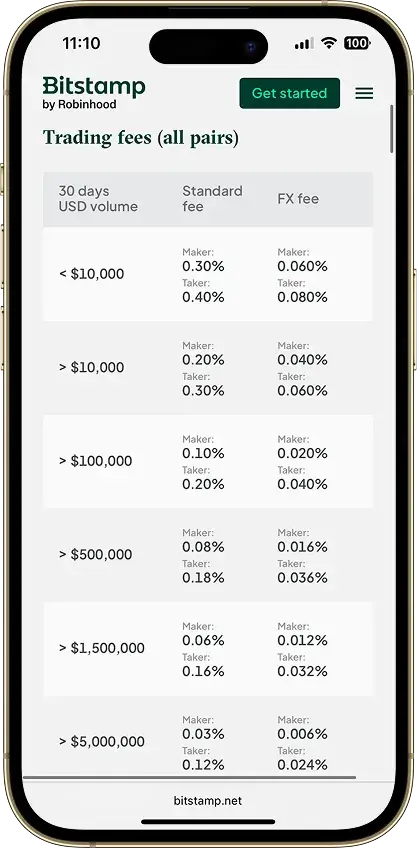

Bitstamp

Pros

- Free ACH withdrawals, flat €3 SEPA cash-outs

- Fees to 0.00%/0.03%, FastPass from 0.01%

- Per-asset networks shown before login

- ~95% cold storage; BitGo custody + insurance

Cons

- No public proof-of-reserves page confirmed

- Support reputation is a real drag

- Fewer extra products than larger global rivals

- Instant Purchase costs 4% vs order-book path

Crypto.com

Pros

- 2022 hack reimbursed in full, all 483 accounts

- Free ACH deposits and withdrawals for US users

- 0% maker fees reachable on the Exchange

- FDIC pass-through on USD cash at partner banks

- Proof of reserves you can check against balance

Cons

- Best fees and rewards require CRO

- Support is email and bot, no phone

- 24-hour hold on every new withdrawal address

- Not available in New York

- App spread hides behind "0% commission"

Binance.US

Pros

- Taker fees to 0.02%+ from trade one, no minimums

- Zero-fee ACH both ways since USD return Feb 2025

- Issues Form 1099-DA, so spot is pre-reported

- REST & WebSocket APIs follow Binance conventions

Cons

- No futures, options, or margin trading

- Not available in NY, TX, WA, OH, OR & more

- No user-verifiable proof of reserves

- High account-freeze complaint volume

Viewed side by side, centralized and decentralized derivatives venues solve different problems. Account-based exchanges usually do more for traders who want easier funding, broader product menus, and a formal support layer. Wallet-based venues appeal more to traders who care about custody, direct chain access, and DeFi-native execution.

That distinction matters because two platforms can both offer perpetuals while feeling nothing alike once funding, setup, and risk are taken into account. On Solana in particular, the wallet setup shapes the trading experience before Jupiter or Raydium even enters the shortlist.

What Is Crypto Derivatives Trading?

Crypto derivatives trading means trading a contract whose price is tied to an underlying asset such as Bitcoin or Ethereum, rather than buying and holding the coin itself. The contract gives traders price exposure without requiring them to own the asset on the spot market.

That changes how people use the market. Some traders use derivatives to speculate on short-term price moves. Others use them to hedge an existing spot position. A miner, treasury, or long-term holder can use derivatives to reduce downside exposure without selling the coins they already hold.

Leverage is a big part of that appeal. It lets traders control a larger position with a smaller amount of collateral. It also makes losses move faster. A small price swing can turn into a large percentage loss once leverage is added, which is why liquidation risk sits at the center of crypto derivative trading.

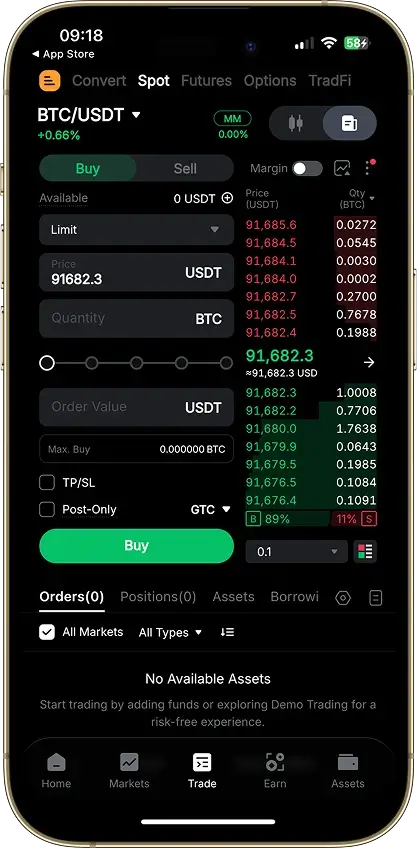

What Is Perpetual Trading In Crypto?

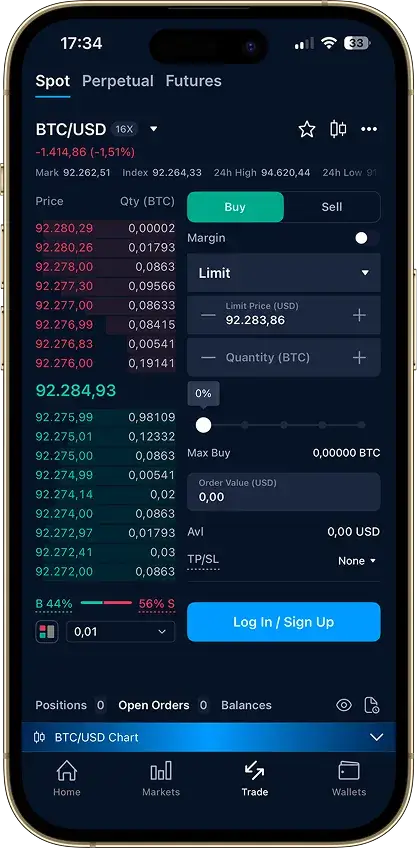

Perpetual trading in crypto usually refers to perpetual futures, often shortened to perps. These contracts do not expire, so traders can keep a position open as long as they maintain enough margin.

Because there is no expiry date, perpetual contracts use a funding mechanism to keep the contract price close to the spot market. When perp prices trade above spot, longs usually pay funding to shorts. When perp prices trade below spot, shorts usually pay longs. Funding does not replace trading fees, but it does change the real cost of holding a position over time.

Two numbers matter more than most beginners expect. The mark price is the reference price the platform uses for unrealized profit and loss and for liquidation checks. The liquidation price is the level where the platform will start closing the position because the posted margin is no longer enough.

Margin mode changes how much of your capital is at risk. Cross margin draws from the wider account balance, which can keep a position alive longer but can also expose more collateral to loss. Isolated margin limits risk to the margin assigned to that one trade, which makes it easier to cap downside on a single position.

Perps Vs Futures Vs Options

| Contract Type | Expiry | Funding | Typical Use Case | Complexity |

|---|---|---|---|---|

| Perpetuals | No expiry | Yes | Short-term trading, directional exposure, and active hedging | Medium |

| Dated Futures | Fixed expiry date | No recurring funding | Basis trading, calendar trades, and hedges tied to a known date | Medium |

| Options | Fixed expiry date | No recurring funding | Defined-risk trades, volatility strategies, and structured hedges | High |

Most people comparing crypto derivatives exchanges are really comparing perpetual futures access. Perps are the easiest derivatives product to find, they trade around the clock, and they do not force traders to manage expiry dates the way dated futures do. Options matter for more advanced strategies, but they sit further up the learning curve. Traders who only want expiry-based products may find this futures-only comparison more useful.

Best Platforms By Use Case

The best platform depends less on the headline brand and more on the kind of trader you are. A U.S.-based user working inside a narrower regulated market is solving a different problem from a beginner learning isolated margin, or a DeFi-native trader who wants wallet-based perpetuals without handing custody to an exchange.

A use-case table makes the trade-offs easier to scan. Once the category is clear, the shortlist gets much tighter.

| Category | Top Pick | Why It Fits | Main Catch |

|---|---|---|---|

| Best Crypto Derivatives Exchange For U.S. Traders | Coinbase | It offers the cleanest regulated path for many U.S.-based users, with stronger domestic funding options and a more familiar compliance setup than offshore rivals. | The derivatives range is narrower than what global platforms offer, and it is rarely the cheapest route for active traders. |

| Best Perpetual Futures Platform For Beginners | Bitstamp | It keeps the perpetuals experience simpler than most specialist derivatives venues, with less product clutter and a lower-intensity setup for users who want a calmer starting point. | The product menu is narrow, and it does not offer the same built-in practice flow that stronger demo platforms do. |

| Best Platforms For Paper Trading Crypto Perps | OKX | Built-in demo trading makes it easier to practice order entry, margin modes, stop-loss placement, and liquidation management without putting real capital at risk. | It is not a broad U.S. route, and the full platform can still feel dense once you move past the demo environment. |

| Best For Advanced Traders And API Users | Bybit | It combines deep perp coverage, options, bots, and automation tools in one of the strongest non-U.S. pro-trading stacks in the market. | Regional access is the limiting factor, and the feature set is more useful to active traders than to casual users. |

| Best Onchain Self-Custody Perps Platform | Hyperliquid | It offers the strongest wallet-native perpetuals experience on this page, with serious liquidity, low fees, and a trading interface that feels built for execution rather than for retail hand-holding. | It assumes more wallet fluency, gives up most fiat convenience, and asks the user to handle more of the setup and operational risk directly. |

Each row points to a different kind of fit. Coinbase and Bitstamp make more sense when clarity, regulation, or a simpler learning curve matter more than raw product breadth. OKX and Bybit pull ahead once practice environments, deeper derivatives tooling, and pro features become the priority. Hyperliquid stands apart because it is built around self-custody and onchain execution rather than around mainstream exchange convenience.

Fees, Funding, Liquidity and Execution Quality

Derivatives trading costs rarely stop at the posted maker and taker rate. The real bill usually comes from five moving pieces working together — the trading fee, the funding rate, the spread, the slippage you take on size, and the way the venue handles liquidation and collateral movement.

That is why this section matters more than a headline “low fees” claim. A platform can look cheap on the fee page and still cost more once thin books, wide spreads, or repeated funding payments start working against the trade.

Trading Fees and Funding Rates

Base derivatives fees on major venues often sit close enough together that they look interchangeable at first glance. Kraken Derivatives starts at 0.0200% maker and 0.0500% taker. Bybit’s VIP 0 perpetual and futures schedule starts at 0.0200% maker and 0.0550% taker. Once volume tiers, market-maker programs, and token discounts enter the picture, the gap between platforms often shrinks even more.

The bigger difference comes from how you trade. Passive orders reduce cost. Aggressive orders lift the offer or hit the bid. On liquid BTC and ETH contracts that spread may stay manageable. On smaller contracts, the spread and the fill can matter more than the fee schedule itself.

Funding is the part many traders underweight. Perpetual contracts rely on funding payments to keep the contract price close to spot. On many centralized venues, funding lands every eight hours. Hyperliquid pays funding hourly. A position that looks cheap to open can become expensive to hold once several positive funding windows stack against it.

Liquidation design belongs in the same cost discussion. Some venues add explicit liquidation or close-out fees. Others absorb the cost through insurance funds, partial liquidation logic, or backstop mechanisms. Hyperliquid is unusual here because it routes most liquidations through the order book first and does not charge a separate clearance fee. Network fees sit further down the stack, but they still matter when you move collateral onchain, bridge stablecoins, or cycle funds between venues.

| Cost Layer | What Drives It | Why It Matters |

|---|---|---|

| Trading Fee | Maker or taker role, VIP tier, liquidity program | This is the visible cost, but not always the biggest one |

| Funding | Long or short imbalance in perpetual markets | Holding a crowded position can cost more than the entry fee |

| Spread And Slippage | Order-book depth, contract liquidity, position size | Thin books can turn a cheap venue into an expensive fill |

| Liquidation Cost | Leverage, margin mode, volatility, close-out rules | Forced exits can include explicit fees or deeper execution loss |

| Transfer / Network Cost | Onchain deposits, withdrawals, bridging, wallet setup | This matters more on self-custody and multivenue workflows |

Top Crypto Derivatives Exchanges By Volume and Open Interest

Market-share tables and editorial rankings are not the same thing. This block is here to show where activity is concentrated, not to replace the shortlist above.

As of April 2026, public rankings from CoinGecko and CoinMarketCap still place Binance at the top of the crypto-native derivatives market, with Bybit also sitting firmly in the top tier. CoinGlass data adds another layer: CME has become the dominant venue for BTC futures open interest on the institutional side, while Binance remains the clearest reference point for crypto-native exchange activity.

| Market View | Current Leaders | Why It Matters |

|---|---|---|

| Crypto-Native Derivatives Volume | Binance, Bybit, OKX | These are still the core venues for deep retail-facing derivatives flow on major crypto contracts |

| Crypto-Native Open Interest | Binance with Bybit and OKX close enough to matter | Open interest shows where leverage is already concentrated, not just where volume printed today |

| Institutional BTC Futures Open Interest | CME | This matters for total market structure, even though CME is not part of the crypto-exchange shortlist on this page |

| Onchain Perpetuals Presence | Hyperliquid is the clearest name to watch | Centralized venues still dominate absolute size, but Hyperliquid shows how much perpetual activity has shifted onchain |

On the crypto-native side, Binance is still the clearest answer on the major public rankings. That changes once the lens shifts to BTC futures open interest and includes institutional venues such as CME, which is why volume and open interest should not be treated as the same signal.

Crypto Exchanges With USDC Or USD Perpetual Futures

True USD-settled perpetuals are still less common than USDC- or USDT-margined contracts. For most traders, the more useful question is whether collateral, profit and loss, and settlement stay in a dollar-pegged asset rather than whether the contract name references BTC-USD or ETH-USD.

| Exchange | USDC-Margined Perps | USD-Settled Products | Notes |

|---|---|---|---|

| Coinbase International Exchange | Yes | No broad cash-USD perp focus | Coinbase’s perpetual futures specs describe linear perpetuals settled in USDC, with USDC, BTC, and ETH accepted as collateral on the international venue |

| Bybit | Yes | No broad cash-USD perp focus | Bybit’s USDC perpetuals are quoted, margined, and settled in USDC, which keeps profit and loss accounting in a dollar-pegged asset |

| Hyperliquid | Yes | No | Hyperliquid uses USDC margining for its main perpetual design even when contracts are quoted against USDT-based oracle prices |

| OKX | Yes, but lineup varies | Yes, in eligible jurisdictions | OKX still documents USDC-margined perpetual categories and also outlines USD-margined perpetual products in some jurisdictions, but contract availability has shifted over time |

USDC-margined perpetuals make the most sense for traders who want stable collateral, simpler profit-and-loss tracking, and less exposure to collateral swings while a position is open. True USD-settled perpetuals remain more specialized and tend to appear through jurisdiction-specific product lines rather than through the deepest global crypto books. For traders building around stable collateral, USDC wallet picks can matter almost as much as the venue itself.

Centralized Vs Decentralized Crypto Derivatives Exchanges

The split between centralized and decentralized crypto derivatives exchanges matters before a trade is even placed. The choice changes how funds are held, how access works, how quickly you can get started, and which risks sit closest to the position.

| Category | Centralized Exchanges | Decentralized Perpetual Platforms |

|---|---|---|

| Custody | The platform holds assets inside an exchange account and manages margin, liquidation, and transfers from that account layer. | The trader keeps custody through a wallet and signs transactions directly, even when the interface feels exchange-like. |

| KYC | Identity checks are common, especially for fiat rails, higher limits, and derivatives eligibility in regulated markets. | Wallet access is usually lighter at the protocol layer, but frontend restrictions and jurisdiction controls can still apply. |

| Fiat On-Ramps | Bank transfers, cards, and app-based funding are a core part of the product in many regions. | Fiat is usually a separate step handled before funds reach the wallet or the protocol. |

| Wallet Setup | No external wallet is required for basic use. Most users can fund the account and trade inside one platform. | A compatible wallet, chain-native assets, and gas-aware setup are part of the normal flow. |

| Order Types | Broader pro tooling is common, including conditional orders, complex triggers, options support, and deeper account controls. | The strongest DEX venues cover core perp trading well, but the feature set is usually tighter and more product-specific. |

| Liquidity Depth | Depth is usually stronger on major centralized venues, especially on BTC, ETH, and the most active altcoin contracts. | Liquidity can be strong on leading protocols, but it is still more concentrated and venue-specific. |

| Support Model | Live chat, tickets, help centers, and formal account support are part of the expected package. | Support is lighter, more community-led, or limited to docs, Discord, and protocol-level communication. |

| Main Risks | Counterparty risk, account restrictions, regional product carve-outs, and withdrawal or verification friction. | Smart-contract risk, oracle design, wallet mistakes, bridge friction, and thinner operational support. |

| Best For | Traders who want simpler onboarding, broader products, stronger support, and easier fiat movement. | Traders who want self-custody, wallet-native access, and a more direct path into onchain perpetuals. |

Centralized venues usually make more sense for users who value easier funding, broader product menus, and a support layer when something goes wrong. Decentralized venues fit users who already operate from wallets, are comfortable managing their own setup, and care more about self-custody and onchain access than about fiat convenience. A wider look at the broader DEX landscape helps once the decision starts leaning toward wallet-based trading, and self-custody wallet choices make that shift easier to plan.

The Pros and Cons of Crypto Derivatives Trading

Crypto derivatives can be useful tools. They can also magnify mistakes much faster than spot trading. The same features that make them attractive — leverage, short exposure, and round-the-clock access — are the same features that make risk build quickly when position sizing or timing goes wrong.

Why Traders Use Derivatives

| Advantage | Why It Appeals |

|---|---|

| Long And Short Exposure | Traders can position for rising or falling prices without having to borrow coins manually or exit a long-term spot holding. |

| Capital Efficiency | Leverage lets a trader control a larger position with less posted collateral, which can free up capital for other uses. |

| Hedging | Miners, funds, treasuries, and long-term holders can reduce downside risk without fully selling their spot exposure. |

| 24/7 Markets | Crypto derivatives trade around the clock, which gives traders more flexibility than markets tied to standard exchange hours. |

| Access To Onchain Alternatives | Wallet-based perpetual venues make it possible to trade without moving everything into a centralized account structure. |

These benefits explain why derivatives remain central to crypto market structure. They are not only speculation tools. They are also used for hedging, treasury management, and short-term execution across both centralized and onchain venues.

Where Derivatives Go Wrong

| Risk | Why It Matters |

|---|---|

| Liquidation Risk | Leverage reduces the distance between entry and forced exit. A modest market move can close the position before the trader has time to react. |

| Funding Drag | Perpetuals can become expensive to hold when funding repeatedly moves against the position, especially in crowded markets. |

| Slippage | Thin books and aggressive orders can make the actual fill much worse than the quoted price, especially on smaller contracts. |

| Leverage Misuse | High leverage can make small mistakes look manageable at entry and severe once volatility expands. |

| Regional Restrictions | Product access varies by country, legal entity, and sometimes by state, which limits what traders can actually use. |

| Smart-Contract And Oracle Risk | Onchain perpetuals add protocol-level risk that does not exist in the same form on centralized exchanges. |

The best use of derivatives starts with clear limits. Position size, margin mode, stop placement, and holding period matter as much as venue choice. Traders who treat leverage as a precision tool usually do better than traders who treat it as a shortcut.

Tax Reporting and Record-Keeping For Derivatives Traders

Tax treatment varies by jurisdiction, so this section is about documentation rather than tax advice. Derivatives traders should keep a clean export trail from the first deposit to the final close, especially when positions move across multiple exchanges, wallets, and collateral assets.

| Record Type | Why It Matters |

|---|---|

| Trade History | Entry and exit timestamps, size, price, contract type, and margin mode form the base record for any gain, loss, or income calculation. |

| Funding Payments | Perpetual funding can add or subtract material value over time and is easy to miss if only closed trades are exported. |

| Fees | Trading fees, liquidation charges, borrowing costs, and network fees can change the final profit-and-loss picture. |

| Transfers | Internal transfers between spot, margin, futures, and subaccounts help explain where collateral moved. |

| Wallet Activity | Onchain deposits, withdrawals, bridges, and swaps matter when collateral enters or leaves self-custody. |

| Realized PnL Exports | A venue’s realized profit-and-loss file is useful, but it should be treated as one record, not the only one. |

The safest habit is to export records regularly instead of waiting until year-end. Save CSVs, account statements, TXIDs, and screenshots of any unusual liquidation, adjustment, or clawback event. If you trade across centralized and decentralized venues, keep one master ledger that ties exchange activity to wallet movement so the reporting trail does not break when collateral moves.

How to Choose a Crypto Derivatives Exchange

The shortlist usually gets smaller once you stop asking which exchange looks biggest and start asking which one actually fits the way you trade. The right venue depends on access, product type, funding route, and how much complexity you are willing to manage before and after the trade.

| What To Check | Why It Matters | What Good Looks Like |

|---|---|---|

| Regional Availability | A platform is useless if the product you want is not available in your country, state, or legal entity. | Clear access rules for your jurisdiction and no guesswork around whether perps, futures, or options are actually live for you. |

| Product Fit | Not every venue offers the same mix of perpetuals, expiry futures, options, or onchain markets. | The exchange supports the contract type you actually plan to trade instead of forcing you into a near substitute. |

| Liquidity On Your Pairs | Deep liquidity on BTC and ETH does not always translate to the altcoin contracts you care about. | Tight spreads, solid depth, and cleaner fills on the exact contracts and sizes you trade most often. |

| Fee And Funding Profile | Posted fees are only one part of cost. Funding and slippage can matter more over time. | Competitive maker and taker pricing, manageable funding, and no obvious mismatch between headline fees and real execution cost. |

| Collateral Model | Collateral affects risk, accounting, and how exposed you are to swings outside the trade itself. | A model you understand, whether that means USDC margin, cross collateral, isolated margin, or wallet-based collateral flows. |

| Risk Controls | Stop placement, margin mode, liquidation visibility, and order controls matter more than branding once volatility rises. | Clear liquidation price display, isolated and cross margin options, reduce-only controls, and reliable order handling. |

| Fiat Rails Or Wallet Friction | Some traders need fast bank rails. Others prefer self-custody and can work entirely from wallets. | A funding path that matches how you move capital, without adding unnecessary steps before every trade. |

| Support Or Protocol Maturity | When something goes wrong, the difference between a formal support stack and a docs-plus-Discord model becomes obvious. | A venue whose operational model matches your tolerance for self-service, community support, or formal account help. |

For most traders, the cleanest selection process is simple. Confirm access first. Match the platform to the product you actually want to trade. Then compare real execution cost, risk controls, and funding friction. If two venues still look close, choose the one whose custody model and support structure you are more likely to handle well under stress. If derivatives still feel too advanced, a simpler place to start is often the better next move.

How We Ranked The Best Crypto Derivatives Exchanges

This page uses CryptoSlate’s Pro / Derivatives lens rather than a general retail-exchange framework. That shifts more weight toward execution quality, pricing, API depth, and trading reliability because those factors matter more in derivatives than they do in a spot-first review.

We look first at market quality and reliability. That includes liquidity depth, spread behavior, slippage, and how stable the venue remains when markets move quickly. A platform can offer a broad contract list and still fall short if execution quality breaks down when volatility rises.

Fees and pricing sit close behind. We look at maker and taker costs, how clearly those costs are presented, and whether the venue stays competitive once real trading behavior is taken into account. That includes funding, spread pressure, and the practical cost of entering and exiting positions rather than fee-page marketing alone.

API and pro tooling matter more here than they would on a beginner spot guide. Conditional orders, test environments, automation support, and deeper account controls all shape how usable a venue is for active traders. Security and custody still matter heavily, especially when leverage is involved, because counterparty risk and collateral handling become more important once capital is tied to open positions.

Proof of reserves and transparency, regulatory posture, payments and rails, product breadth, and UX and support still play a role in the final editorial picture. They just do not outweigh market quality and real trading cost on a derivatives-first page.

| Pillar | What We Look For |

|---|---|

| Market Quality And Reliability | Liquidity depth, spreads, slippage, and trading stability under stress |

| Fees And Pricing | Maker and taker costs, real execution cost, and whether pricing stays competitive in practice |

| API And Pro Tooling | Testnet access, automation support, order controls, and advanced trading infrastructure |

| Security And Custody | Account security, collateral handling, custody setup, and platform-level safeguards |

| Proof Of Reserves And Transparency | Transparency around reserves, disclosures, and operational clarity |

| Regulatory Posture | Entity structure, jurisdiction fit, and how clearly the venue presents product availability |

| Payments And Rails | Fiat access, funding flexibility, and how easy it is to move capital in and out |

| Product Breadth | Coverage across perps, dated futures, options, and related trading tools |

| UX And Support | Platform usability, support structure, and how manageable the product is under real trading conditions |

Centralized exchanges are the closest fit for the CES framework and follow that logic directly. Decentralized perpetual platforms are handled through a separate editorial lens inside this page so they are not forced into a custody, fiat-rail, or support model that does not match how they actually work. Until CryptoSlate introduces a dedicated DEX derivatives scoring model, the onchain names here are compared through product, execution, custody, and risk structure rather than through a straight CEX scorecard.