Travel exposes card weaknesses fast. Foreign exchange fees, ATM limits, hotel deposit holds, fuel station pre-authorizations, and regional acceptance rules all show up within the first 24 hours of a trip. Most crypto cards handle local spending fine. Fewer hold up once you are outside your home country, dealing with a different currency, a cash-only market, or a rental desk that wants a deposit.

This ranking focuses on how each card performs on an actual trip. Country access, signup difficulty, funding clarity, foreign-spend cost, cash access, physical card usefulness, and what happens when a merchant ties up part of your balance all factor into the final score. The cards here are the ones that make the most sense for real travel, across a range of traveler types and funding preferences.

Top Crypto Cards for International Travel

- Virtual US bank numbers for ACH and wires

- Free instant transfers to other KAST users

- No card spending ceiling, USD spend at 0%

- Tap to switch Debit and Credit Mode

- Fund from stablecoins, fiat, or Savings crypto

- Spend borrowed funds, keep coins as collateral

- Free on-chain and EUR/GBP funding rails

- No forced crypto sale at each purchase

- Hong Kong-licensed, FinCEN MSB registered

- Named, FDIC-member US bank issuers

- Credit card triggers no per-purchase tax

- Visa Signature perks, Priority Pass tiers

- Cryptoback still live in UK, NZ, HK, TW

- Preload converts before the register, not at it

- Stablecoin loads convert close to 1:1

The strongest options here have lower foreign-spend costs, wider acceptance, or a more usable fallback when a payment fails. Region, funding method, and card format still change the answer.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay | 100+ countries, varies by jurisdiction. |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay, Samsung Pay | Available in many regions (e.g., US, EEA/UK, SG, CA, AU, BR) with residency-based eligibility and restricted markets per Crypto.com lists. |

| | Visa, Mastercard | Debit | Apple Pay, Google Pay | Available in UK and many countries (incl. parts of EEA, AU, NZ, HK, TW), while not available in USA, Canada, China, Japan, South Korea, Philippines, Russia (among others); EEA Mastercard eligibility requires EEA residency excluding Cyprus & Liechtenstein. |

The best all-round options combine wide country coverage, a live physical card, and foreign-spend pricing that stays easy to understand. Stablecoin-first cards can work well for card spend, but some lose appeal once you need cash, refunds, or large temporary holds.

Crypto Cards for International Travel Reviews

Kast Card

Pros

- 1.5% USD cashback on the free tier

- Stablecoins load 1:1 with no spread

- Virtual card minutes after a two-minute KYC

- US-available, unlike most crypto cards

- Five stablecoins across major chains

Cons

- Volatile crypto is sold on deposit at 2%–5%

- Free-tier cashback stops at $2,000 a month

- ATM cash costs $3 + 2%, capped at $750 a day

- Top cashback rates cost $1,000–$10,000 a year

- Custodial USD balance, no self-custody

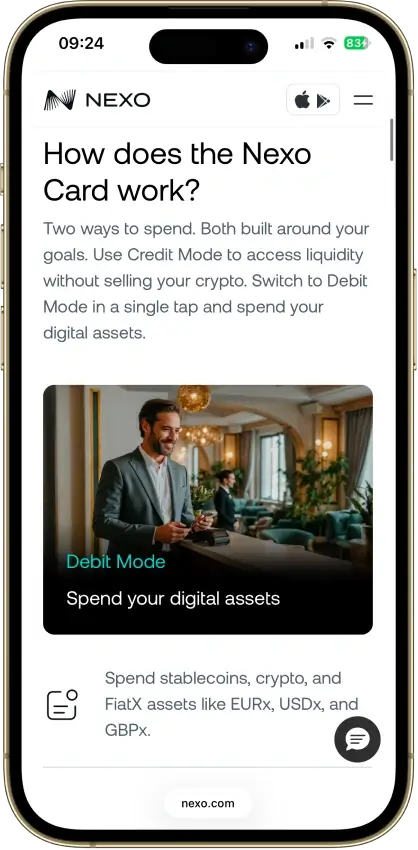

Nexo Card

Pros

- Credit Mode sells no crypto at purchase

- No monthly, annual, or inactivity fees

- 0.2% weekday FX in the EEA, UK, and CH

- Idle Debit Mode balance earns daily interest

- Issued by DiPocket UAB, a licensed EMI

Cons

- EEA and UK only, US persons excluded

- Physical ordering paused since Jan. 2025

- Cashback needs Credit Mode and a $5,000+ portfolio

- 2–2.5% FX outside the EEA, UK, and CH

- Base rates: 0.5% NEXO or 0.1% BTC

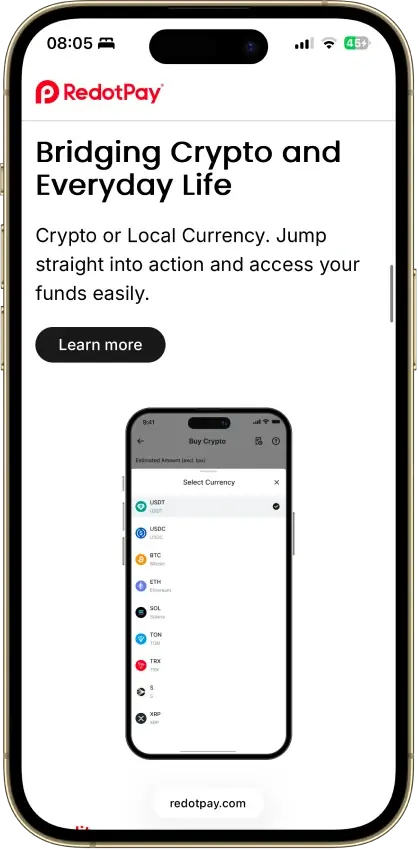

RedotPay

Pros

- No monthly or annual fee

- 1.2% FX fee beats most prepaid rivals

- Virtual card live minutes after KYC

- Fireblocks custody, segregated addresses

- Spends in 100+ countries

Cons

- No cashback or ongoing rewards

- Non-refundable 10/100 USDT issuance fees

- 2–3% ATM fees, physical card only

- $50 chargeback fee, 3–6 month waits

- Blocked in the US and 41 other markets

Crypto.com Card

Pros

- Free 1.5% base rate, no stake, no subscription

- Reward paid in BTC or CRO on the credit card

- $0 annual fee on both cards

- CRO card: tiered $300 welcome bonus, $5K/90 days

- Instant virtual card with one-tap freeze

Cons

- Prepaid free tier earns 0% cashback

- 3% FX fee on every accessible prepaid tier

- Top rates need $50k–$500k CRO stakes

- Prepaid rewards pay only in volatile CRO

- Crypto top-ups taxed as a sale at load

Wirex Card

Pros

- Principal member of both Visa and Mastercard

- 0% foreign-transaction fee on 30+ currencies

- Free issuance, PIN changes, and an ATM allowance

- Regulated, disclosed issuers in every region

Cons

- EEA and Australia Cryptoback ended Jun. 30, 2026

- Free tier pays 0.5%, in volatile WXT

- 8% needs Elite at €29.99/mo plus a WXT lockup

- Not available in the US or Canada

- 0% FX still carries a conversion spread

How We Ranked the Best Crypto Cards for International Travel

This ranking uses a travel-specific scoring model. The score is not a general crypto-card score. A card can be strong for everyday spending and still rank lower here if it is weak for foreign exchange, ATM access, hotel deposits, physical-card use, or emergency backup travel.

Final score = sum of each criterion score x weight. Each criterion is scored as 0, 0.5, or 1.0.

- 1.0 = strong and clearly verified for a new eligible user

- 0.5 = usable, but with meaningful travel friction

- 0.0 = unavailable, unclear, unverified, or too weak for this travel use case

| Criterion | Weight | What We Scored |

|---|---|---|

| Country Coverage And New-User Access | 1.20 | Supported regions, eligibility, KYC, app access, and whether a new user can realistically get started before a trip |

| Pre-Trip Funding Rails And Conversion Path | 1.00 | Stablecoin deposits, fiat funding, crypto-to-card flow, supported assets, chain limits, and whether the spend path is easy to understand |

| FX Cost And Rate Predictability | 1.40 | Foreign transaction fees, weekend pricing, card-currency rules, conversion spreads, and whether the app shows costs clearly |

| In-Store, Online, And Mobile-Wallet Reliability | 1.20 | Card network, virtual card, Apple Pay / Google Pay, online use, tap-to-pay, and everyday merchant acceptance |

| Physical Card And ATM Cash Access | 1.10 | Physical-card availability, ATM support, free monthly allowance, withdrawal fees, and withdrawal caps |

| Hotel, Rental Car, And Fuel-Hold Fit | 1.10 | Whether the card can handle temporary holds, pre-authorizations, deposits, and hold-heavy merchants |

| Fees And Hidden Travel Cost Drag | 1.00 | Issuance, delivery, top-up fees, FX fees, ATM fees, small-transaction fees, inactivity, replacement, and tier costs |

| Operational Convenience And Limits | 0.80 | Issuance timing, physical delivery, spend limits, refund timing, card balance caps, and emergency usability |

| Security, Custody, Support, And Disputes | 0.80 | Freeze controls, custody model, compliance holds, support access, refund path, chargebacks, and escalation clarity |

| Rewards, Perks, And Reporting Readiness | 0.40 | Rewards after caps and tiers, travel perks, transaction history, statements, and tax-recording friction |

Rewards receive the lowest weight on this page because travel cards fail first on access, FX cost, ATM cash, physical-card availability, and temporary holds. A higher reward rate does not compensate for a card that is hard to fund, expensive to use abroad, or weak at hotel and rental counters.

Availability, Supported Countries and Setup Friction

Before you compare fees, you need to confirm that you can actually get the card. Country coverage, verification requirements, and physical delivery timelines decide whether the card is ready before your trip or not. If you want a card with minimal signup steps, it is also worth checking the no KYC cards page, though none of the five cards here qualify for that category.

Here is how each card compares on access and setup:

- Nexo:

- Region: EEA and UK only

- KYC: Full ID verification required; extra checks can apply

- Card format: Virtual only for new users; physical orders currently paused

- Time to first use: Virtual activates immediately after eligibility and verification

- Wirex:

- Region: 130+ countries, though card support is not universal across all of them

- KYC: Identity verification required; address and source-of-funds checks can be requested

- Card format: Both virtual and physical available in supported card markets

- Time to first use: Virtual available immediately in-app after ordering

- KAST:

- Region: Available in many countries; spend acceptance spans 170+ countries

- KYC: Required; extra documents can be requested for some activity

- Card format: Instant virtual card; physical available in supported markets

- Time to first use: Standard shipping 3 to 7 business days after processing; international shipping 7 to 21 business days

- RedotPay:

- Region: 158+ countries, excluding blocked jurisdictions such as the U.S.

- KYC: Full KYC required before use; ID and face scan required

- Card format: Both available, though physical shipping is restricted in some countries

- Time to first use: Virtual starts quickly after KYC; physical takes 10 to 15 days to produce plus 5 to 30 days delivery

- Crypto.com Prepaid Card:

- Region: Selected regional rollouts covering Europe, UK, U.S., Canada, APAC, Brazil and select LATAM, and Bahrain and select GCC

- KYC: Full app KYC required; some regions ask for additional card information

- Card format: Both available in supported markets

- Time to first use: Approval typically takes 3 to 4 days but can take up to 7 business days; virtual usable after approval

Example: Getting Set Up Before a Trip

Assume you book a trip three weeks out and want the physical card in hand before departure.

- Nexo: Virtual is ready within a day of passing verification. Physical card cannot be ordered right now, so this card is virtual-only for the trip.

- Wirex: Virtual is ready the same day in supported markets. Physical card ordering is available in supported markets, and standard delivery typically lands within the three-week window if ordered promptly.

- KAST: Virtual is instant. Standard physical shipping runs 3 to 7 business days after processing, which fits comfortably in three weeks. International shipping at 7 to 21 days is tighter and depends on the destination.

- RedotPay: Virtual starts quickly after KYC clears. Physical card takes 10 to 15 days to produce plus up to 30 days delivery. Three weeks may not be enough time depending on your country.

- Crypto.com: Approval can take up to 7 business days. Physical card delivery adds more time on top. If approval takes the full 7 days, physical delivery in the remaining two weeks is uncertain in many markets.

The quickest crypto cards to set up before a trip are the ones with instant virtual issuance and a cleaner verification flow. Wirex and KAST are strongest here. Nexo is quick for virtual use but weaker for trips that need a physical card. RedotPay needs more lead time if you want the plastic, and Crypto.com can work if approval clears early enough.

ATM Access, Withdrawal Fees and Limits Abroad

Cash still matters on many trips. Even if you mostly pay by card, you need to know whether emergency cash is realistic, how quickly fees stack, and whether the card becomes expensive after one or two withdrawals.

Here is how each card handles ATM access and withdrawal costs on the road:

- Nexo:

- Free monthly ATM allowance: €200 / £180 to €2,000 / £1,800 depending on loyalty tier

- Fee after limit: 2%, minimum €1.99 / £1.99

- Physical card required: Yes, and orders are currently paused for new users

- Main catch: Strong allowance on paper, but unavailable to new users until physical issuance resumes

- Wirex:

- Free monthly ATM allowance: Usually £200 / €200 / $200 monthly equivalent; A$400 in Australia

- Fee after limit: 2%

- Physical card required: Yes in most cases

- Main catch: Allowance is modest and region-specific

- KAST:

- Free monthly ATM allowance: None

- Fee per withdrawal: $3 flat + 2%, plus FX fees on non-USD cash

- Per-withdrawal cap: $250

- Physical card required: Yes

- Main catch: Expensive from the first withdrawal; not suited to regular cash use

- RedotPay:

- Free monthly ATM allowance: None

- Fee structure: 2% on HKD or USD card withdrawals up to $10,000 monthly; 3% above that on USD cards

- Additional fees: 1.2% non-card-currency fee and 1% crypto conversion fee may also apply

- Physical card required: Yes

- Main catch: Multiple fees stack on every withdrawal

- Crypto.com Prepaid Card:

- Free monthly ATM allowance: $200 / €200 to $1,000 depending on tier and region

- Fee after limit: 2%

- Physical card required: Yes

- Main catch: Base tiers are weak abroad and foreign-use fees may apply on top of ATM fees

Worked Example: One ATM Withdrawal of $200 Abroad

Assume you withdraw $200 equivalent in local currency. Here is what it costs per card:

- Nexo (inside free allowance, EEA): $0 withdrawal fee.

- Nexo (above free allowance): $200 x 2% = $4.00, minimum €1.99 / £1.99.

- Wirex (inside free allowance): $0 withdrawal fee.

- Wirex (above free allowance): $200 x 2% = $4.00.

- KAST: $3.00 flat + ($200 x 2%) = $7.00, plus FX if the currency is not USD.

- RedotPay: $200 x 2% ATM fee ($4.00) + 1.2% currency fee ($2.40) + 1% crypto conversion ($2.00) = approximately $8.40 if all fees apply.

- Crypto.com (inside free allowance, right tier): $0 withdrawal fee.

- Crypto.com (above free allowance): $200 x 2% = $4.00.

Nexo, Wirex, and Crypto.com are the better options for cash access, but only when the user is inside the right region and within the free monthly ATM allowance. KAST and RedotPay are better treated as debit cards for daily card spend first, with ATM use reserved for emergencies.

Virtual Cards, Physical Cards and Mobile Wallet Support

Some trips need fast virtual access. Others still depend on physical card acceptance, insert transactions, and reliable mobile-wallet support. The right mix depends on whether you need to start spending before the plastic arrives or whether the trip includes merchants that require a physical card. For a broader look at cards built specifically around contactless and app-based access, the virtual cards page covers options where the digital format is the primary use case. Separately, the Apple Pay and Google Pay page lists cards verified for mobile wallet support across different regions.

Here is how each card covers digital and physical access before and during a trip:

- Nexo:

- Instant virtual card: Yes

- Physical card: Orders currently paused for new users

- Apple Pay / Google Pay: Both supported

- Best on-trip use: Fast wallet spend and online checkout where a virtual card is enough

- Wirex:

- Instant virtual card: Yes, in supported markets

- Physical card: Available in supported markets

- Apple Pay / Google Pay: Both supported in supported markets

- Best on-trip use: Quick setup and everyday travel spend

- KAST:

- Instant virtual card: Yes, instant

- Physical card: Available in supported markets

- Apple Pay / Google Pay: Both supported for active cards in supported countries

- Best on-trip use: Digital-first travel with physical fallback on longer trips

- RedotPay:

- Instant virtual card: Yes, starts quickly after KYC

- Physical card: Available, though shipping is restricted in some countries

- Apple Pay / Google Pay: Both supported, though some wallet links can take a few days to sync

- Best on-trip use: Online spend, wallet pay, and backup physical use

- Crypto.com Prepaid Card:

- Instant virtual card: Yes, in supported markets after approval

- Physical card: Available in supported markets

- Apple Pay / Google Pay: Region-dependent; strong in major issuing regions, mixed elsewhere

- Best on-trip use: Works well once local wallet support is live and the physical card has arrived

Nexo, Wirex, and KAST are the most digital-first options here. Physical cards still carry a lot of weight on real trips. KAST, RedotPay, and Crypto.com become considerably more useful once the physical card is in hand. Nexo stays limited for hotel holds or ATM use until physical card issuance returns.

Stablecoin Support and Travel Funding Options

Travel use also depends on how easy the card is to fund and which assets it can spend cleanly. Strong USDC or USDT support can make a real difference if that is how you already manage your travel balance.

Here is how each card handles stablecoin funding and other top-up options:

- Nexo:

- Stablecoin support: USDC and USDT

- Other funding rails: EURx, GBPx, USDx, bank transfer, card purchases, and other crypto

- Wirex:

- Stablecoin support: USDC and USDT

- Other funding rails: Bank transfer, debit or credit card, fiat balances, and other crypto

- KAST:

- Stablecoin support: USDC and USDT

- Other funding rails: Bank transfer by region, BTC, ETH, SOL, and other crypto deposits

- RedotPay:

- Stablecoin support: USDC and USDT

- Other funding rails: Crypto deposits, Binance Pay, and buy-crypto-by-card on Android

- Crypto.com Prepaid Card:

- Stablecoin support: USDC and USDT, though the top-up asset list varies by market

- Other funding rails: Fiat wallet, debit or credit card, PayPal in some markets, and crypto wallet top-up

KAST and RedotPay make the most sense for stablecoin-heavy users who want their travel balance to start in USDC or USDT. Nexo and Wirex feel more balanced if you move between fiat and crypto often. Crypto.com sits closer to a standard travel card with a crypto funding layer added on top, especially for users who fund it in the local fiat currency they plan to spend.

Best Crypto Cards By Traveler Type

The right card changes with the trip. A frequent flyer, a digital nomad, and someone who still expects to use cash regularly abroad will each get different value from the same product. If rewards matter after the travel use case is covered, the rewards cards page ranks cards specifically on cashback rate and earn structure.

| Traveler Type | Best Pick | Why It Fits |

|---|---|---|

| Frequent Flyer | Wirex | Broad country reach, no card-level FX fee, and quick virtual setup in supported markets |

| Digital Nomad | KAST | Stablecoin funding is clean, USD balance is easy to manage, and physical plus virtual support fits long trips |

| Cash-Heavy Traveler | Crypto.com Prepaid Card | Better than most rivals only if your tier and region give enough free monthly ATM allowance before the 2% post-limit fee |

| Stablecoin-First Traveler | KAST | USDC and USDT funding is simple, and the spending model is easy to understand on the road |

| Backup-Card Seeker | RedotPay | Quick virtual start, broad non-U.S. coverage, and useful physical backup once delivered |

Match the card to the way you actually travel. Rewards and headline perks tell you much less once you know whether you need cash access, stablecoin funding, fast virtual use, or a second card that can step in when the first one fails.

How To Choose The Right Crypto Card For International Travel

The best card is the one that still works when the trip gets unpredictable: a delayed refund, a fuel hold, an offline terminal, or a late ATM run. Most of these failure points are predictable. You just need to check for them before you fly.

Before comparing rewards, check country access, merchant acceptance, ATM fees, and your backup option. A good travel card is one you can verify in time, fund clearly, and rely on when a payment fails.

Main Card vs. Backup Card

Use a traditional credit card as the primary card for hotel deposits, car rental holds, and any merchant that requires a credit card at check-in. Those holds can be larger than the final bill. On prepaid or debit-style crypto cards, they can lock the balance you need for the rest of the trip.

Use the crypto card as the daily-spend tool once the deposit problem is covered. It handles meals, transit, shopping, online bookings, mobile-wallet payments, and stablecoin-funded spending well once the conversion path is clear. The safest setup is one credit card for holds, one crypto card for daily spend, and a small cash reserve for terminals or merchants that fail.

What To Check Before You Fly

A quick pre-trip check can save you from the most common card problems abroad. Run the card through the route, spend type, and backup plan before you rely on it.

Here is the pre-departure checklist that covers the most common failure points:

- Confirm your country, destination, and identity document are supported.

- Order the physical card early if the trip includes hotels, car rentals, ATMs, fuel kiosks, or offline terminals.

- Activate the virtual card and add it to Apple Pay or Google Pay before departure.

- Make one small test purchase in your home country before loading a larger travel balance.

- Check the FX rule for the exact currency you will spend in, including weekend pricing and non-USD fees.

- Check the ATM allowance, the post-limit fee, per-withdrawal limits, and whether the physical card is required.

- Keep enough available balance for temporary hotel, car rental, fuel, or restaurant holds.

- Decide which card will handle deposits and which card will handle daily purchases.

- Download or enable transaction statements so refunds, disputes, and tax records are easier to reconcile later.

- Carry a mainstream credit card and a small amount of local cash if the trip includes deposits, rentals, or multiple countries.

Common Ways Travelers Lose Money Abroad

Most travel-card mistakes look small in the moment, but they stack quickly. Paying in your home currency instead of the local one, assuming a virtual card will cover every travel payment, or relying on a single card all trip are all easy ways to make a trip more expensive than it needs to be.

The other common mistake is misreading the pricing. Post-limit ATM fees, low withdrawal caps, and weak conversion rates can cost more than the headline card fee, especially when a card advertises no FX fee but still gives a poor exchange rate on the conversion itself.

Worked Travel Scenario: Card Spend, One ATM Withdrawal and One Hotel Hold

Assume a traveler loads funds before departure, pays for daily purchases abroad, withdraws cash once, and checks into a hotel. The friction shows up in different places depending on whether the card is being used for spending, cash, or a temporary hold.

| Trip Moment | What The Traveler Does | Where Friction Appears |

|---|---|---|

| Foreign spend | Pays for meals, transport, and shopping in the local currency | FX cost depends on the card: Wirex has no card-level FX fee, KAST adds 0.5% to 1.75% on non-USD spend, RedotPay can stack crypto conversion and cross-currency fees, and Crypto.com depends on region and tier |

| One ATM withdrawal | Takes out local cash for cash-only merchants | Physical card is usually required. KAST costs $3 + 2% plus non-USD FX, RedotPay charges ATM and conversion layers, while Nexo, Wirex, or Crypto.com may be cheaper inside the free monthly allowance |

| Hotel hold | Presents a card at check-in for deposit or incidentals | The hold can be higher than the expected bill and can block the available crypto-card balance until the merchant or network releases it |

The practical setup is simple: put deposits and rental holds on a credit card, keep one crypto card funded for daily purchases, and treat ATM withdrawals as small backup events rather than the main way to get money abroad.

Tip That Can Save You Money

When a card terminal or ATM asks whether to charge you in your home currency or the local currency, choose local currency. The home-currency option is dynamic currency conversion: the merchant or ATM operator sets the conversion rate, and it can be worse even if your card advertises low or zero FX fees. Decline the terminal's conversion, let the card network or issuer handle the exchange, and check the final amount in the app afterward. This applies to all five cards here.