USDC is one of the few crypto assets that makes card spending practical day to day, but the gap between “supports USDC” and “works well with USDC” is wide once you look at how each card handles conversion, which deposit networks it accepts, and how easy it is to pull unused funds back out.

The five cards ranked here cover different regions and use cases. Some work better for U.S. users who already hold USDC on an exchange. Others suit international users who want a stablecoin-funded balance with bank payout or stablecoin withdrawal options. The right pick depends on where you are, which app you already use, and whether you want to stay in stablecoins or move to fiat at the point of spend.

Top Crypto Cards For USDC

- Virtual US bank numbers for ACH and wires

- Free instant transfers to other KAST users

- No card spending ceiling, USD spend at 0%

- Tap to switch Debit and Credit Mode

- Fund from stablecoins, fiat, or Savings crypto

- Spend borrowed funds, keep coins as collateral

- Switch your reward coin before each purchase

- No card balance to top up or strand

- 24/7 phone support with a dedicated card line

- Free on-chain and EUR/GBP funding rails

- No forced crypto sale at each purchase

- Hong Kong-licensed, FinCEN MSB registered

- Set your own crypto auto-sell priority

- Named EEA e-money card issuers

- Cashback paid in liquid BTC, USDC, or AVAX

KAST is the strongest active pick when USDC is the main funding asset and you also want stablecoin withdrawal or bank payout options. Coinbase is the easier path for U.S. users who already hold USDC on Coinbase. Nexo fits EEA and UK users who want Debit Mode, and RedotPay or Bybit make more sense when you already use those apps and can accept the extra conversion or regional friction.

For USDC users, the key question is what happens between deposit and payment. Some cards let you fund directly from USDC and spend with minimal friction, while others use USDC as a funding balance that converts before the transaction settles.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay | 100+ countries, varies by jurisdiction. |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card |

For a USDC user, the best card gives you a clear funding path, a predictable payment flow, and a usable way to withdraw unused funds. KAST, Coinbase, and Nexo handle those steps with fewer surprises. RedotPay and Bybit need closer attention to card fees, conversion costs, and regional limits.

These five cards all support USDC, but they handle it differently, and that difference shows up in daily use. A stablecoin-first card behaves differently from an exchange card that includes USDC as one of several funding options.

Crypto Cards For USDC Reviews

Kast Card

Pros

- 1.5% USD cashback on the free tier

- Stablecoins load 1:1 with no spread

- Virtual card minutes after a two-minute KYC

- US-available, unlike most crypto cards

- Five stablecoins across major chains

Cons

- Volatile crypto is sold on deposit at 2%–5%

- Free-tier cashback stops at $2,000 a month

- ATM cash costs $3 + 2%, capped at $750 a day

- Top cashback rates cost $1,000–$10,000 a year

- Custodial USD balance, no self-custody

Nexo Card

Pros

- Credit Mode sells no crypto at purchase

- No monthly, annual, or inactivity fees

- 0.2% weekday FX in the EEA, UK, and CH

- Idle Debit Mode balance earns daily interest

- Issued by DiPocket UAB, a licensed EMI

Cons

- EEA and UK only, US persons excluded

- Physical ordering paused since Jan. 2025

- Cashback needs Credit Mode and a $5,000+ portfolio

- 2–2.5% FX outside the EEA, UK, and CH

- Base rates: 0.5% NEXO or 0.1% BTC

Coinbase Card

Pros

- $0 annual, monthly, and foreign transaction fees

- USD and USDC spend at par with no spread

- No credit check, staking, or lockup to earn

- Instant virtual card plus Apple Pay and Google Pay

Cons

- Crypto spend triggers spread plus taxable sale

- Reward rates are app-set, never published

- $2,500 daily spend cap binds on big purchases

- US-only rewards, and Hawaii is excluded

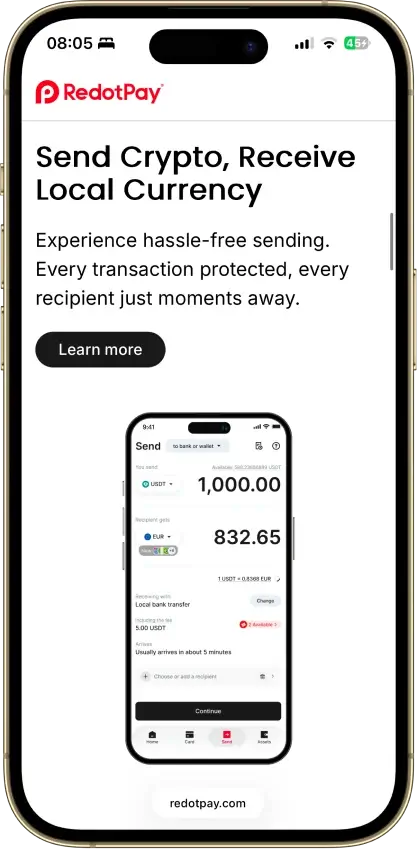

RedotPay

Pros

- No monthly or annual fee

- 1.2% FX fee beats most prepaid rivals

- Virtual card live minutes after KYC

- Fireblocks custody, segregated addresses

- Spends in 100+ countries

Cons

- No cashback or ongoing rewards

- Non-refundable 10/100 USDT issuance fees

- 2–3% ATM fees, physical card only

- $50 chargeback fee, 3–6 month waits

- Blocked in the US and 41 other markets

Bybit Card

Pros

- 1% uncapped base cashback with no annual fee

- Fiat-first funding can skip the 0.9% spread

- No monthly, inactivity, or issuance fees

- €5,000 daily spend and €2,000 daily ATM caps

- Instant virtual card, freeze and limit controls

Cons

- EEA EUR card closed on bybit.com Jan. 1, 2026

- 0.9% spread plus a taxable sale on crypto spend

- 0.5% FX fee on cross-currency purchases

- Custodial — funds sit on the exchange

- Base rate 1%; 2%+ needs VIP tier, capped monthly

Our Ranking Methodology

This ranking is built for USDC card users, not for general crypto card users. The highest scores go to cards that make the full USDC flow clear: how USDC gets into the account, what happens at checkout, which networks are supported, and how unused funds can leave again.

We scored each card across 10 criteria. Each criterion receives a score of 0, 0.5, or 1.0, then that score is multiplied by the criterion weight. The final score is out of 10.

| Criterion | Weight | What We Checked |

|---|---|---|

| Availability And Setup Friction | 1.00 | Eligible regions, application status, KYC, extra verification, and whether a new user can realistically get the card. |

| USDC Funding Rails And Conversion Path | 1.50 | Whether USDC can fund the card, which account or wallet receives it, when conversion happens, and whether the checkout flow is easy to understand. |

| USDC Network Support And Wrong-Chain Risk | 1.00 | Supported USDC networks, whether network support is public or app-only, and how easy it is to avoid sending USDC on the wrong chain. |

| Real-World Spend Reliability | 1.25 | Online spend, in-store spend, subscriptions, mobile wallets, merchant acceptance, pre-authorizations, and card-network behavior. |

| Fees And Hidden Cost Drag | 1.25 | Card issuance, annual fees, top-up fees, spread, crypto conversion, FX, ATM fees, withdrawal fees, and network costs. |

| Rewards Value After Conditions | 0.75 | Cashback asset, caps, tiers, token requirements, plan fees, volatility, and whether rewards are usable or speculative. |

| Exit Path And Cash-Out Convenience | 0.75 | Whether unused funds can exit as USDC, fiat bank payout, exchange withdrawal, or app transfer. |

| App Controls, Virtual Card, And Wallet Tooling | 0.75 | Virtual card access, physical card access, Apple Pay, Google Pay, freeze/unfreeze, spend controls, payment priority, and transaction history. |

| Custody, Security, And Freeze Risk | 1.00 | Custodial model, issuer dependence, compliance checks, account freezes, source-of-funds risk, and clarity of the trust model. |

| Tax And Reporting Readiness | 0.75 | Statements, CSV exports, transaction history, reward records, refund records, and clarity around USDC gains or losses. |

We gave more weight to funding, conversion, network support, spend reliability, and fees because those are the parts that most often break the USDC card experience. Rewards receive a lower weight because a speculative reward token or an “up to” cashback rate does not help much if the card is expensive, region-limited, or unclear about how USDC is converted.

You may check our top crypto rewards cards if rewards are an important decision factor here.

What To Look For In A USDC Crypto Card

A good USDC card needs to work at three points: funding, checkout, and cash-out. Start with the spend model. Some cards work with a USDC-funded balance more directly, while others convert earlier or settle in a way that adds cost.

The funding path and withdrawal path matter just as much as the spending experience. Check which networks the card accepts for USDC deposits, whether you can move money back out without friction, and how much KYC is required before the card becomes usable for everyday spending.

Then consider daily use. A reliable virtual crypto card, Apple Pay or Google Pay support, clear handling for refunds and failed payments, and usable statements or export options all matter more than a simple rewards headline.

USDC Network Support

USDC is issued on many chains, but a card app only accepts the routes it supports for that asset. The cheapest option is not always the safest unless the same network appears on both the sending wallet and the card app deposit screen.

| Card | Supported and Cheapest USDC Networks |

|---|---|

| KAST Card | Receive USDC on Ethereum, Solana, Polygon, Arbitrum, and Stellar. Send USDC on Ethereum, Solana, and Arbitrum. Arbitrum is typically the cheapest withdrawal route; deposit cost depends on the sending wallet. |

| Coinbase Visa Debit Card | Coinbase-supported USDC networks shown during send/receive; availability can vary by account, region, and state. Use the lowest-fee route shown by Coinbase before confirming. |

| Nexo Card | USDC is supported, but network options should be checked inside the Nexo app before transfer. Do not assume Solana, Base, or Arbitrum unless displayed. |

| RedotPay | USDC deposits accepted only on the specific networks shown on the RedotPay deposit page in the app. Unsupported networks can fail or require paid recovery. |

| Bybit Card | USDC deposit and withdrawal chains depend on the supported chain shown on the Bybit asset page for that account. Use the chain with the lowest fee inside Bybit; unsupported chains can require recovery or fail. |

Do not assume USDC is interchangeable across chains. If a card route only accepts ERC-20 and you hold USDC on Solana, sending anyway can fail, trigger a recovery review, waste time, add fees, or become unrecoverable.

Do not assume USDC is interchangeable across chains. If a card route only accepts ERC-20 and you hold USDC on Solana, sending anyway can fail, trigger a recovery review, waste time, add fees, or become unrecoverable.

How These Cards Usually Work

Most USDC cards follow the same basic payment flow, but balance handling is where they diverge. That difference determines whether the card works like a stablecoin spending tool, a fiat card funded from crypto, or an exchange card with USDC sitting in the funding balance.

The steps are the same for most cards, but what happens between step two and step three is where costs and friction appear:

- You fund the app or wallet with USDC.

- The platform either keeps that balance as spendable USDC, converts at checkout, or requires you to preload fiat first.

- The card network processes the merchant payment in fiat.

- The app settles the spend against your balance and displays the transaction history afterward.

The spend model matters more than the marketing label because it changes the real cost and the real workflow. A card that advertises USDC support can still convert early, add spread at payment, or make withdrawals and refunds harder than expected.

Custody, Freezes and Refunds with USDC Cards

USDC card apps usually require custody. After you deposit USDC, the exchange or card provider controls the balance until it is spent, withdrawn, or closed out. Compliance checks, wrong-chain deposits, Travel Rule reviews, suspicious-activity flags, or chargeback investigations can all block spending or withdrawals even when the on-chain transfer succeeded.

Refunds usually come back through card rails, not as instant USDC transfers. Keep the app statement, merchant receipt, and funding transaction together so support can trace a failed purchase, reversal, refund, or chargeback without needing you to reconstruct the flow from scratch.

Fees Associated with USDC Crypto Cards

Headline pricing rarely reflects what a crypto debit card will cost once you use it as a regular spending tool. The bigger costs tend to appear when the app converts your balance, when a foreign purchase settles, or when you try to pull unused funds back out. Here is how the fee picture breaks down for each card covered in this guide.

KAST Card

- Stablecoin top-up: 0%

- USD spend: 0%

- Non-USD FX: 0.5%–1.75%

- ATM: $3 flat plus 2%

KAST has no top-up fee and no fee on USD purchases, which keeps daily spending costs low for users who stay in dollar-denominated merchants. The cost shows up on ATM withdrawals and on non-USD transactions, where the FX markup can reach 1.75%.

Coinbase Visa Debit Card

- Card spend fee: 0% from Coinbase

- Spread: may apply at conversion

- ATM: operator fee may apply; no Coinbase surcharge stated

Coinbase does not charge a fee on card purchases, but a spread can apply when USDC converts to USD at the point of sale. ATM costs depend on the operator, not Coinbase, so those vary by machine.

Nexo Card

- Monthly or annual fee: none

- FX: up to 0.2% outside EEA, UK, and CH currencies

Nexo has the lightest fee profile of the five cards. There is no issuance fee, no monthly charge, and FX is capped at 0.2% in most regions. The main constraint is availability: the card is limited to EEA and UK users.

RedotPay

- Virtual card: $10

- Physical card: $100

- Crypto conversion: 1%

- Other-currency ATM fee: 1.2% plus the ATM operator fee

RedotPay charges upfront for both card types and takes 1% on each crypto conversion. For users who fund in USDC and spend frequently in non-USD currencies, the conversion and ATM fees stack quickly.

Bybit Card

- Annual fee: none

- Virtual card: free (current offer)

- Crypto conversion: typically 0.9%

- FX: typically 0.5%–2% depending on program

Bybit has no annual fee and currently issues virtual cards at no cost, but the conversion and FX fees apply every time USDC moves to a spendable balance. Users who make frequent small purchases in multiple currencies will see those percentages add up.

Worked Examples

To see how fees affect real spending, consider two scenarios.

A freelancer based outside the U.S. uses KAST Card as their primary USDC spending card. They receive a $2,000 USDC payment, deposit it into KAST at 0% top-up, and spend $1,800 on USD-denominated subscriptions and SaaS tools. Total card fee on those purchases: $0. They withdraw $200 to a local bank via Local Payout. The cost of that exit depends on the payout fee KAST applies to the Local Payout route, which should be confirmed in-app before transfer.

A user in the EEA holds USDC on the Nexo platform and uses the Nexo Card for day-to-day purchases across the eurozone. They spend EUR 500 in a month on merchants that settle in EUR. Because EUR falls within Nexo's EEA currency group, the FX fee applies at 0.2% or less, adding no more than EUR 1 to the total monthly cost. There is no annual fee and no top-up fee on USDC deposited to the Savings Wallet.

Once spread, FX markup, card fees, and withdrawal costs accumulate, a stablecoin card can end up costing more than a standard debit card or a straightforward exchange-to-bank withdrawal. The cleaner the fee structure, the less you need to track.

Taxes and Reporting When You Spend USDC

USDC card spending is usually cleaner than spending volatile crypto, but it still needs records. Keep the card statement, funding transaction, merchant receipt, USDC amount, fiat amount, and any spread, conversion, FX, or withdrawal cost tied together.

If your USDC cost basis is exactly $1.00 and the card converts or settles it at $1.00, the spend usually creates no taxable gain. If you acquired USDC below par during a depeg, then spending or converting that USDC above that basis can create a gain because the disposal value is higher than the purchase value.

The same logic applies in reverse: if USDC was acquired above par and later spent at $1.00, that may produce a loss. For frequent card use, CSV exports and clean statements are more useful than rewards because they make tax matching possible later.

Common USDC Crypto Card Problems and Fixes

USDC support alone does not guarantee smooth spending. Funding, merchant acceptance, refunds, and withdrawals can all get complicated once you start using the card regularly.

Most issues fall into a short list of repeating patterns. Testing the full flow with a small amount before relying on any of these cards for larger payments is the fastest way to avoid them:

- Wrong-network deposit: Double-check the supported network before sending and use a test transfer first.

- Merchant decline: Some merchant types, pre-authorizations, or risk filters can fail even with sufficient balance.

- Refund delay: Card refunds often take longer than standard wallet transfers.

- Cash-out friction: A card can work well for spending and still be weak for moving unused funds back out.

- Extra KYC review: Limits often appear when users try to unlock withdrawals, higher spend, or additional card features.

- Travel checkout issues: FX, merchant category blocks, and offline terminals can all create friction abroad.

USDC Price and News

USDCUSDC is a fiat-backed stablecoin issued by Circle and designed to track the U.S.

USDC Coin ProfileUSDC News

USDC redemptions just outpaced mints by $4B, but a massive new token presale is quietly doubling Circle’s revenue outlook

Redemptions exceeded mints, yet circulation rose 19% as lower reserve yield sharpened attention on an undisclosed ARC Token contribution.

Circle is arming USDC with 1,000 IBM patents to secure its grip on global banking rails

Compromised contract let hackers print 5.2 million WEMIX stablecoins, forcing a complete network freeze