A Bitcoin card should do one of two jobs well: pay rewards in BTC from normal spending, or let you spend without dumping the BTC you already hold.

Most crypto cards fail both tests. They list Bitcoin as a supported asset but pair it with hidden fees, limited availability, or a spend model that triggers a conversion every time you swipe. The result is a card that technically supports BTC but works against anyone trying to build or preserve a Bitcoin position.

Top Bitcoin Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

A card belongs here only if Bitcoin plays a meaningful role, either through BTC rewards or by letting you spend without forcing a BTC sale on every purchase.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

Gemini is the simplest fit for passive BTC accumulation. Nexo suits users who want to borrow against crypto rather than sell first. Coinbase One Card is the cleaner Coinbase option for BTC rewards because purchases run on a credit line and bitcoin back is built into the card, though the required membership changes the break-even point.

Bitcoin Cards Reviews

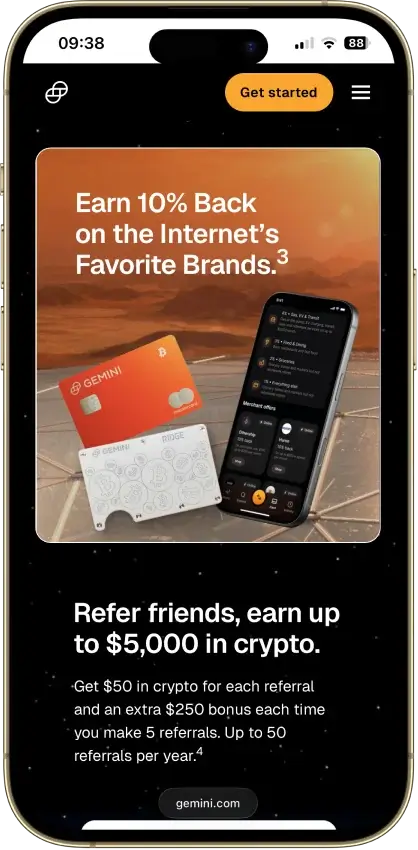

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

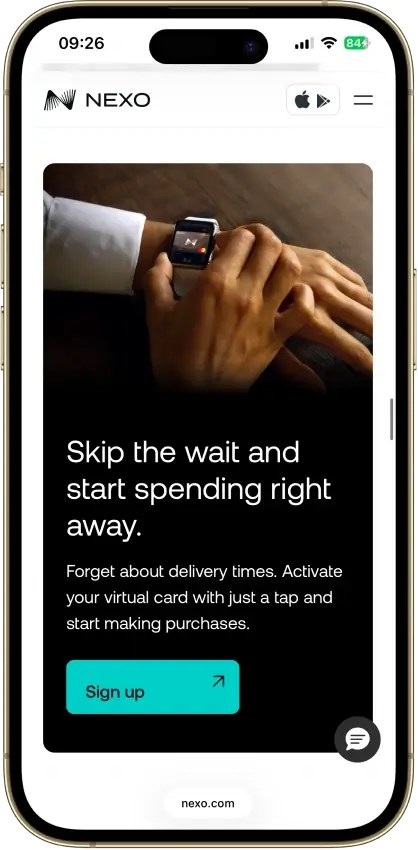

Nexo Card

Pros

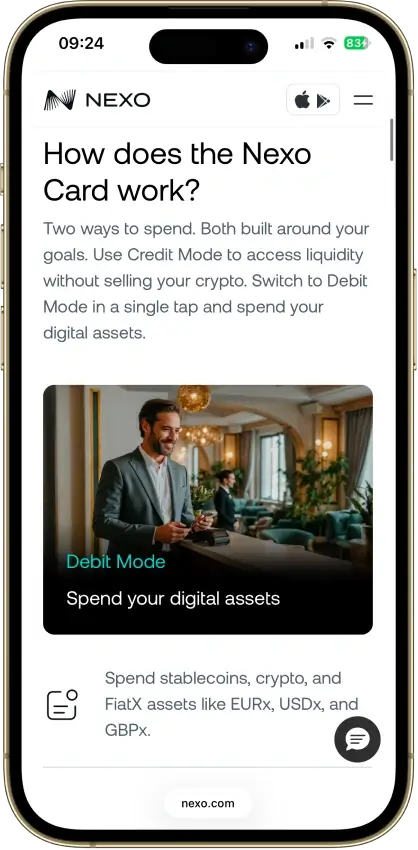

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

Our Ranking Methodology

We score Bitcoin cards on a 10-point weighted rubric. Each criterion gets a raw score of 0, 0.5, or 1.0, then we multiply that raw score by the criterion weight.

We used the same mixed-model card framework as the broader crypto card rankings, but the Bitcoin lens is stricter. A card only gets Bitcoin-card credit when BTC has a clear job: it earns BTC, spends from BTC, borrows against BTC or crypto, or helps users avoid selling BTC at checkout. Broad crypto support alone is not enough.

We score each card within its intended model. A crypto rewards credit card does not lose points because it cannot spend onchain BTC. A debit card does not lose points because it is not a credit card. But every card loses points when fees, tax tracking, conversion spread, custody limits, or setup gates weaken the real Bitcoin use case.

| Criterion | Weight | What We Check On This Bitcoin Page | Why It Matters |

|---|---|---|---|

| Availability + Setup Friction | 1.0 | Eligible regions, KYC, credit approval, plan gates, tier gates, and whether a new user can get a usable card. | A strong Bitcoin card does not help if most users cannot actually access it. |

| Funding Rails + Conversion Path | 1.25 | Whether BTC is earned, spent, used as collateral, or sold during the transaction. We also check supported assets, fiat settlement, and repayment flow. | This determines whether the card helps users stack BTC, use BTC, or preserve BTC exposure. |

| Real-World Spend Reliability | 1.5 | Card network, online spend, in-store use, mobile-wallet spend, travel holds, preauthorizations, merchant declines, and debit/prepaid quirks. | This carries the highest weight because a card has to work in normal spending before the BTC angle matters. |

| Rewards Value After Conditions | 1.0 | BTC reward availability, reward rate, caps, category rules, membership cost, asset-balance rules, loyalty tiers, and volatility. | Headline Bitcoin rewards can shrink quickly after caps and conditions. |

| Fees + Hidden Cost Drag | 1.25 | Annual fees, membership fees, interest, borrowing cost, spread, FX, ATM fees, top-up fees, replacement fees, and partner costs. | Small recurring costs can erase the value of BTC rewards or make BTC-funded spend unattractive. |

| Operational Convenience + Limits | 0.75 | Virtual-card timing, physical-card access, delivery, spend limits, ATM limits, refunds, settlement timing, and mode switching. | A Bitcoin card needs to be practical after approval, not only good on paper. |

| App + Controls + Virtual Card Tooling | 0.75 | Freeze/unfreeze, card details, alerts, virtual cards, Apple Pay, Google Pay, spending priority, statements, and exports. | Most crypto-card control happens inside the app, so weak tooling creates real spending friction. |

| Security + Custody + Freeze Risk | 1.25 | Issuer, custodian, exchange dependence, withdrawal access, collateral risk, account restrictions, and freeze or escalation risk. | BTC rewards or BTC collateral lose value when access, withdrawal, or custody controls are unclear. |

| Support + Refunds + Chargebacks | 0.75 | Human support, dispute flow, unauthorized-transaction handling, refund timing, and reward reversals. | Card problems usually happen during refunds, disputes, fraud events, or failed merchant transactions. |

| Tax + Reporting Readiness | 0.5 | Whether spending creates a BTC disposal, whether rewards have a clear receipt value, and whether records are usable for reporting. | Tax treatment varies by country, but poor tracking can make a high-reward card painful to use. |

The score is not a marketing score. It is a real-use score for someone comparing Bitcoin cards in 2026. The best card is not always the one with the highest BTC rate. It is the one where the Bitcoin role still makes sense after access, fees, tax tracking, custody, and day-to-day spend reliability are checked.

What Counts As A Bitcoin Card In 2026

Not every crypto payment card that lists BTC qualifies as a Bitcoin card. The Bitcoin role has to be central: it sits at the core of the reward model, the spending model, or the credit model. The main types work differently from each other, and the distinction matters before you apply.

- Crypto-backed credit card or dual-mode crypto card: You spend on a fiat credit line and earn BTC back on purchases. This suits users who want passive Bitcoin exposure from ordinary spending without touching their holdings.

- Bitcoin debit card: You spend from a linked cash or crypto balance. Bitcoin may sit on the funding side, the reward side, or both. Conversion costs and disposal tracking add friction that a credit setup avoids.

- Generic crypto card with a BTC option: Bitcoin appears in a broader crypto-card setup but is not the primary use case. These cards can earn or spend BTC, but the card is not designed around it.

Two cards can both mention Bitcoin while doing very different jobs. One builds BTC from ordinary spending. Another mainly converts crypto into spendable card balance. The card type determines which problem actually gets solved.

Bitcoin Credit Cards Vs Bitcoin Debit Cards

Where BTC sits in the transaction determines nearly everything else: the tax burden, the conversion cost, and what the card is actually useful for day to day.

| Factor | Bitcoin Credit Card | Bitcoin Debit Card |

|---|---|---|

| What you spend | Borrowed fiat credit line | Your cash or crypto balance |

| How BTC usually shows up | Reward asset | Funding asset or optional reward |

| Tax friction on normal use | Usually lower on the swipe itself | Usually higher if crypto is sold on spend |

| Best fit | Passive BTC stacking | Direct crypto spending |

| Main risk | Reward value may be modest | Every swipe can create tax tracking |

For most users, the cleanest choice is the one that matches how they already spend. Those who want BTC rewards with less swipe-level tracking usually lean toward a bitcoin rewards credit card. Those who want direct access to crypto at the point of sale often end up weighing debit friction against convenience. Neither card type is better in the abstract; the gap shows up in the day-to-day cost of using them.

Which Bitcoin Card Type Fits Your Goal

The reward model, funding flow, and risk profile change depending on whether the goal is stacking BTC, spending crypto, or unlocking liquidity without selling. Getting the structure wrong is how a card with a strong headline rate ends up being a poor fit in practice.

The table below maps common goals to card structures. For each row, the “What To Watch” column is where most users get caught out.

| Your Goal | Best Card Structure |

|---|---|

| Stack BTC from everyday spend | Bitcoin rewards credit card |

| Spend from crypto | Bitcoin debit card |

| Avoid selling first | Bitcoin rewards credit card |

| Keep setup simple | Mainstream exchange-linked card |

| Use the card mainly on phone | Virtual-first or strong mobile-wallet card |

- Stack BTC from everyday spend: A bitcoin cash back credit card keeps holdings intact and adds BTC passively. Watch for caps, category exclusions, and annual-fee drag that reduce the effective rate.

- Spend from crypto: A bitcoin debit card is the most direct path. Watch for conversion cost on each transaction and the disposal tracking burden that comes with it.

- Avoid selling first: A credit card that earns bitcoin keeps your stack untouched at checkout. Watch for interest charges, collateral ratios, and liquidation risk on collateral-backed setups.

- Keep setup simple: Exchange-linked cards like Gemini or Coinbase One have straightforward onboarding. Watch for custodial dependence and withdrawal restrictions if the platform has issues.

- Use the card mainly on phone: Virtual-first cards or those with solid Apple Pay and Google Pay support work better for daily phone-wallet use. Watch for merchant quirks and preauthorization failures on prepaid or debit setups.

Most users choosing a bitcoin card are deciding between passive BTC accumulation and preserving existing holdings. Those are different goals, and the better card type is rarely the same for both.

How Bitcoin Rewards Actually Work

Bitcoin rewards do not all land the same way. Some cards post BTC instantly after the purchase settles, while others wait until statement close or a later posting window. Timing matters because it changes how quickly the reward starts tracking the market and how easy it is to reconcile BTC against the original spend date.

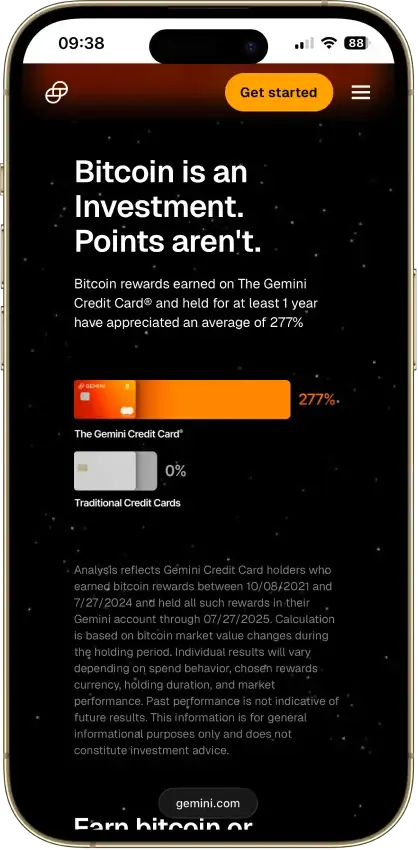

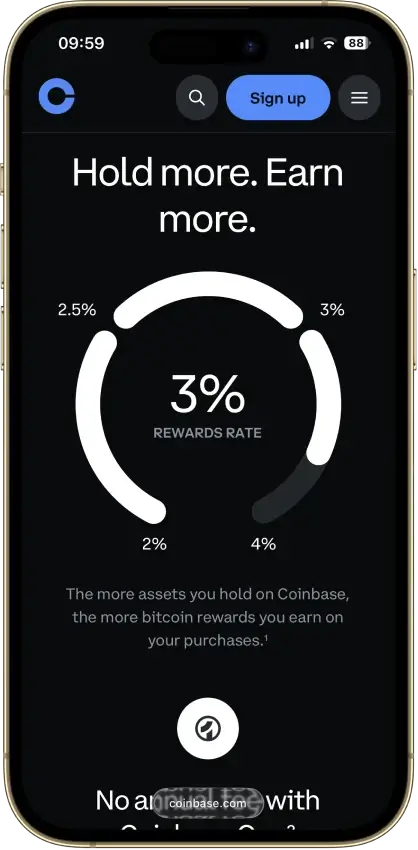

The reward structure also varies across cards on this list. On some, BTC is the default payout asset. On others, it is one option among several, and the rate may be fixed, tied to spending categories, or adjustable over time. Gemini, for example, advertises up to 4% back but applies category caps that reduce the effective rate on most everyday spending. Coinbase One Card pays tiered rates of 2% to 4% depending on assets held on Coinbase, with the higher tiers capped at $10,000 in eligible purchases per calendar month.

The last check is whether the reward arrives as real, portable BTC or as something that still needs conversion inside the issuer ecosystem. Off-platform withdrawal friction reduces reward value quickly. A lower BTC rate can still be the better deal when the payout is cleaner, the limits are lighter, and the Bitcoin can move out without extra steps.

Taxes, Reporting and Selling Friction

The first question is whether Bitcoin stays on the reward side only or enters the spending flow. When a debit card sells BTC to fund a purchase, that sale is typically a taxable disposal in most jurisdictions, including the US and most of Europe. A credit card that pays BTC rewards avoids that problem at the point of sale, though the rewards still need a cost basis recorded when eventually sold.

The next issue is what happens after the reward posts or the card is repaid. Rewarded BTC usually needs a clear acquisition value once it is later sold or swapped. When a crypto-backed card is repaid with crypto, the repayment may itself count as a disposal of the asset used to settle it.

Reporting quality still makes a real difference. Statement detail, CSV exports, and transaction history are not equally useful across card issuers, and tax software still struggles with crypto rewards, conversion events, and card-funded spend flows. In practice, the easiest setup to track is a fiat credit card that pays BTC rewards, followed by a card funded from cash or stablecoins rather than Bitcoin itself.

Custody, Withdrawals and Counterparty Risk

A Bitcoin reward is worth less when it cannot move easily or sits inside a setup with weak withdrawal controls. This matters most for users who plan to sweep rewards into their own self-custody Bitcoin wallets on a regular basis.

The questions below apply to all three cards on this list. Each one changes how much practical value the BTC reward actually holds.

| Question To Check | Why It Matters |

|---|---|

| Where do rewards sit after posting? | Custody and withdrawal rules change the real value of the reward |

| Can you withdraw BTC rewards quickly? | Portability matters if you do not want platform risk to build up |

| Can the issuer pause withdrawals or card use? | Convenience means less if funds can get stuck |

| Does the card depend on a custodial exchange balance? | This changes freeze risk and self-custody flexibility |

| Can rewards move to your own Bitcoin wallet? | A Bitcoin card is more useful if the BTC is portable |

| What does support actually handle during disputes? | Refunds, fraud issues, and reward-posting errors are where support quality matters |

All three cards here are tied to custodial platforms. Gemini holds rewards in your Gemini account until withdrawn. Nexo holds both collateral and rewards within its own platform. Coinbase rewards sit in a Coinbase account. None of them give you direct on-chain control until you withdraw, and each platform has its own withdrawal limits, verification requirements, and history of pausing user access during periods of stress.

Mobile Wallet Support, Virtual Cards and Travel Use

A Bitcoin card that works cleanly in a phone wallet, arrives quickly as a virtual card, and handles travel merchants without friction will get used more often than one with a slightly better headline rate. These are the practical factors that separate the cards in real daily use.

The list below covers the specific things worth checking before you rely on any of these cards for travel or regular phone-wallet spending. Each point is where one or more of these three cards has a documented gap or advantage.

- Virtual card availability before the physical card arrives

- Apple Pay and Google Pay support and whether it requires any card tier or additional setup

- Physical card usefulness for travel, hotels, and car rentals

- Preauthorization friction at fuel pumps, hotels, and transit

- Refund timing and how reversed transactions affect rewards

- Foreign-spend experience, local-currency conversion, and travel merchant acceptance

- Whether the card works best as a daily phone-wallet card or only as a backup

- How it compares with other virtual crypto card options or crypto cards built for international travel

Hotel preauthorizations are where crypto debit cards tend to break down. A hotel hold can lock more than the room rate, and if the card draws from a crypto balance, the conversion happens at hold time rather than checkout. Credit-mode cards like Nexo handle this more predictably because the hold sits against a credit line. Gemini Card and Coinbase One Card handle hotel and travel preauthorizations more predictably than crypto-funded debit flows, while Nexo's Credit Mode can also reduce conversion friction at hold time.

Common Bitcoin Card Problems And Fixes

Most of the problems users run into with a bitcoin card are preventable. The list below covers the issues that come up most often and what to do about each one.

- Reward posts in the wrong asset or at the wrong rate: Check whether the active reward selection expired or changed before the transaction posted.

- Crypto spend creates a tax mess: Use a rewards card or a collateral-backed setup if you do not want every swipe tracked as a disposal.

- Card works online but fails in-store wallet taps: Check whether mobile-wallet provisioning is live for your region and card tier.

- Reward rate looks good but real value is weak: Recalculate after annual fees, spreads, FX, and any lockup requirement.

- Support is slow during disputes: Freeze the card first, then document the transaction and reward state before contacting support.

- Refund takes longer than expected: Card refunds and reward reversals usually move slower than standard crypto transfers.

- BTC rewards feel trapped on-platform: Check withdrawal minimums, network support, and extra verification before relying on the reward flow.

Most of these problems are easier to prevent than fix. The cleaner setup comes from choosing the right card structure first, then verifying the reward flow, funding path, and withdrawal rules before the card becomes part of daily spending.

How To Choose The Right Bitcoin Card

Most mistakes happen when a user wants one thing, such as passive BTC accumulation, but picks a card built for a different flow, such as crypto spending or collateral-backed borrowing.

Before applying for any bitcoin rewards card, work through these eight checks in order. Each one can change whether a card that looks right on the surface actually fits your situation.

- Check whether you want to earn BTC, spend from crypto, or borrow against crypto.

- Check whether normal spending creates a crypto sale.

- Check whether the reward is real BTC or a later conversion path inside the issuer's platform.

- Check the real cost after annual fees, spreads, FX, and reward caps.

- Check whether the card is available where you live.

- Check whether rewards can move to your own wallet cleanly.

- Check mobile-wallet support, refunds, and merchant friction.

- Check reporting quality before assuming the card is easy to live with.

The right bitcoin card usually looks less impressive in a headline than in real use. The better fit comes from matching the card structure, reward flow, and cost profile to the exact job you want it to do.

Bitcoin Price and News

BTCBitcoin News

Bitcoin price has a $64.5k trap as Sunday’s close forces traders between a $68k relief rally or a drop to $60k

Bitcoin’s Sunday close will determine whether $68,000 comes into view or $60,000 returns as the next major test.

Bitcoin is about to give miners a 16% lifeline, but $19 billion in AI deals is luring them away anyway

The $25 million Bitcoin glitch hiding inside Wall Street’s clearinghouses