Free crypto cards get attention for one simple reason: no one wants to pay upfront just to test whether a card works. A card with no application fee, no issuance fee, or a free virtual version removes the first barrier for users who want to spend crypto or stablecoins without committing money before they know the card is worth it.

But free access only covers the entry point. Some cards stay practical after signup. Others recover the cost through shipping fees, conversion spread, FX charges, ATM fees, or paid upgrades. The better options keep the starting cost at zero without making everyday use quietly expensive.

Top Free Crypto Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Fast virtual card access

- Broad stablecoin and crypto funding support

- Strong travel and cross-border utility

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Stablecoin-led global spending

- Virtual and physical card access

- Card, wallet, transfers, swaps and credit in one app

Coinbase is the clearest free crypto debit card for U.S. users. Nexo is stronger in Europe if you meet its eligibility requirements. KAST is the better pick for stablecoin-first virtual spending, and Bybit works best when the virtual card is enough.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay | 100+ countries, varies by jurisdiction. |

A card can be free to start and still become expensive once FX and ATM costs apply. Nexo and KAST hold up better if travel or cash access matters. Coinbase and Bybit are better judged on their virtual-card path and local spend performance first.

Which Type Of Free Crypto Card Fits Your Use Case?

The right free crypto card depends on what “free” needs to cover. For some users, that means no application fee. For others, it means a free virtual card, a free physical card, or a card that handles foreign spend without adding heavy costs. The table below matches user type to the card most likely to stay low-cost through real use.

| User Type | Best Card | Why |

|---|---|---|

| U.S. user wanting free entry | Coinbase Card | Strongest zero-entry path for eligible U.S. users who spend USD or USDC |

| Stablecoin-first online spender | KAST Card | Free virtual-card path in most countries and clear stablecoin-first spending |

| Eligible European virtual-card user | Nexo Card | No monthly, annual, or inactivity card fee, with a virtual-card path in supported European markets |

| Existing Bybit user | Bybit Card | Useful when the free virtual card is enough and funds already sit on Bybit |

| User who needs a physical card first | Coinbase Card or Nexo Card, depending on region | Physical-card costs and availability need the closest check before applying |

| Travel user trying to avoid cash-access costs | Nexo Card | Free ATM allowance is more useful than a card that only waives the signup cost |

Coinbase is the best free crypto debit card for most U.S. users, but it is not the right answer for every situation. KAST is better when the goal is stablecoin-first virtual spending, and Nexo is stronger when you want free physical access in supported European markets.

Free Crypto Cards Reviews

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

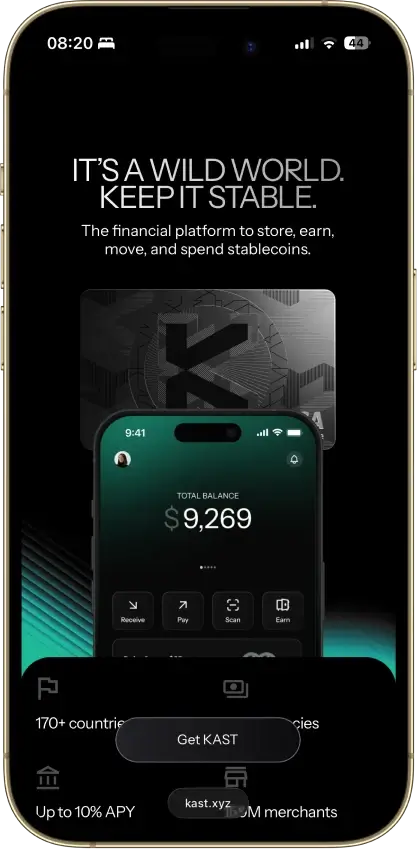

Kast Card

Pros

- Virtual card is ready within minutes of approval, with no shipping wait required

- Apple Pay and Google Pay are supported from the start, so you can spend before the physical card arrives

- Stablecoin deposits (USDT, USDC, USDe, PYUSD, RLUSD) convert to USD at 1:1 with no spread

- The Standard tier costs nothing to open, which keeps the entry bar low for first-time users

- Visa acceptance and physical card delivery cover 170+ countries, which is a wider reach than most crypto cards offer

Cons

- Deposited crypto is treated as sold to KAST on entry, with no self-custody option inside the card flow

- Full KYC and partner approval can block or delay access, even for users in supported countries

- Non-USD spend adds a 0.5% to 1.75% FX fee on top of every transaction

- ATM withdrawals require the physical card, cost $3 plus 2% per transaction, and are capped at $750 per day

- Premium tiers start at $1,000 per year, which is hard to justify unless you spend a very high volume and want KAST Points and token rewards rather than cash

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

RedotPay

Pros

- Virtual card activates fast after KYC and funding, so online spend starts within minutes of approval.

- Physical card unlocks ATM access and in-store use, not just checkout payments.

- Apple Pay support means you can tap to pay in supported regions without carrying the physical card.

- No monthly or annual fee keeps the holding cost flat once you've paid the issuance fee.

- One app covers cards, wallet balances, transfers, swaps, P2P, and crypto-backed credit.

Cons

- Full KYC including ID upload and face scan is required before any core feature is accessible.

- Physical card issuance costs $100 and that fee is non-refundable.

- A 1.2% FX fee applies on every cross-currency transaction, including ATM withdrawals in a foreign currency.

- Custody sits with RedotPay and its partners, so balances can be frozen if compliance checks flag the account.

- The $50 chargeback fee and 3-to-6-month resolution timeline make disputes expensive and slow.

Our Ranking Methodology

We rank free crypto cards by zero-entry usefulness, not by the broadest rewards program or the lowest possible fee in one narrow use case.

For this page, “free” means an approved user has a credible way to start with no card purchase fee, no issuance fee, no annual fee, or a genuinely free virtual-card path. That does not mean the card stays free after signup. FX fees, ATM charges, shipping, conversion spread, paid tiers, borrowing costs, and tax friction still affect the score.

Each card is scored across 10 criteria. Every criterion gets a score of 0, 0.5, or 1.0, then that score is multiplied by the criterion weight.

Final score = sum of (criterion score x weight)

Total possible score: 10

| Criterion | Weight | What We Measure |

|---|---|---|

| Availability + Free-Path Setup Friction | 1.25 | Supported regions, KYC, eligibility, approval friction, and whether a new user can reach a usable free virtual or physical card path |

| Funding Rails + Conversion Path | 1.25 | Supported funding assets, fiat or stablecoin rails, top-up flow, checkout conversion, and whether the user can avoid forced volatile-crypto selling |

| Real-World Spend Reliability | 1.50 | Online spend, in-store spend, mobile-wallet use, subscriptions, pre-authorizations, merchant acceptance, and physical-card backup where relevant |

| Rewards Value After Conditions | 0.50 | Cashback, points, token rewards, caps, exclusions, paid tiers, staking/token holds, and reward volatility |

| Fees + Hidden Cost Drag | 1.75 | Issuance, annual/monthly fees, shipping, replacement, spread, FX, ATM, top-up, inactivity, declined-transaction, gas, and partner fees |

| Operational Convenience + Limits | 0.75 | Issuance timing, funding-to-spend timing, limits, refunds, cash access, and physical-card delivery |

| App + Controls + Virtual Card Tooling | 0.75 | Virtual cards, Apple Pay, Google Pay, freeze/unfreeze, alerts, PIN controls, card details, and basic transaction visibility |

| Security + Custody + Freeze Risk | 1.00 | Custody model, issuer dependence, account controls, freeze risk, platform trust, and incident history |

| Support + Refunds + Chargebacks | 0.75 | Human support, dispute path, unauthorized-transaction process, refund handling, and escalation clarity |

| Tax + Reporting Readiness | 0.50 | Statements, CSV exports, tax reports, cost-basis clarity, and whether spending creates manual reporting work |

A high score does not mean the card is free in every situation. It means the card has a credible zero-entry path and does a better job controlling the first real costs that appear after signup.

Free Crypto Card Costs Explained

A free crypto card removes the signup barrier, but the costs that follow are where the real comparison starts. The list below covers each cost type and what to check before applying.

- Card Issuance Fee: The cost to activate the base card path. Check whether the free path is virtual only or includes the physical card.

- Annual Or Monthly Fee: A recurring cost to keep the card active. Confirm the free tier still works without an upgrade.

- Physical Card Or Shipping Fee: The cost to receive or replace the physical card. Check shipping, replacement pricing, and whether ATM withdrawals work only with a physical card or also through a digital wallet at contactless ATMs.

- Crypto Conversion Fee: A stated fee when the card sells crypto for a payment. Check whether USD, fiat balance, or stablecoins can avoid it.

- Spread: The hidden price gap between market value and spend value. Check the actual rate used at checkout.

- FX Fee: An extra charge on non-home-currency purchases. Check weekday, weekend, and cross-border rules.

- ATM Fee: A flat or percentage charge for cash withdrawals. Check the free allowance and the fee after it.

- Small Transaction Or Declined Transaction Fee: An extra charge on failed or low-value payments. Check micro-transaction rules and insufficient-balance fees.

- Inactivity Fee: A fee after long periods without use. Confirm it is truly $0 and not just a launch perk.

A card can waive the annual fee and still be a poor free-card option. The first three checks are whether the base card costs $0, whether the physical card also stays free, and whether spending triggers spread or tax friction.

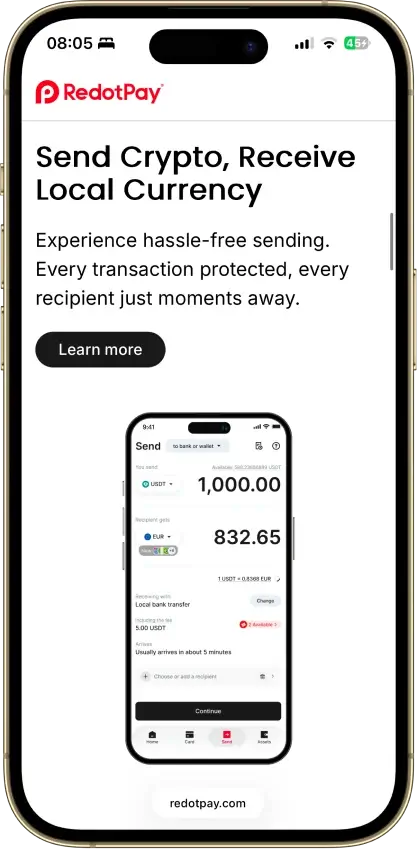

Stablecoin Spending Vs Selling Crypto At Checkout

Stablecoin spending is often the cleaner route on a free crypto card because the value at checkout is easier to predict. If the card lets you spend from USDC or USDT with a near-1:1 conversion into a spending balance, budgeting stays simpler and the free card claim holds up better under real use.

Spending BTC or ETH at checkout can still be useful, especially for users who want direct access to a volatile balance. But it often adds spread and reporting friction. That is why users searching for a free virtual bitcoin debit card often end up preferring a broader virtual card that handles stablecoins well first.

If your main spend balance is stable, compare more options in USDC cards or the guide to USDT spending cards.

Foreign Transaction Fees And ATM Fees On Crypto Cards

Foreign spend is where many free crypto cards give up on savings. A card can cost nothing to activate and still become expensive once the transaction settles in another currency or the user pulls cash from ATMs while traveling. The table below covers each cost area and why it changes the real price.

Cost area breakdown:

- Foreign Purchase Fee

- What to check: Whether the issuer adds a stated cross-border charge

- Why it changes the real price: A free card can still become expensive on non-local purchases

- FX Spread Or Markup

- What to check: The exchange rate used for foreign purchases

- Why it changes the real price: A weak FX rate can cost more than a visible fee

- Weekend FX Rule

- What to check: Whether pricing changes outside market hours

- Why it changes the real price: Weekend travel spend can cost more than weekday spend

- ATM Fee

- What to check: The flat or percentage fee charged by the issuer

- Why it changes the real price: Small withdrawals become expensive quickly once the fee starts

- Free ATM Allowance

- What to check: How much cash is free before the fee applies

- Why it changes the real price: A usable allowance matters more than a low headline fee

- Operator Fee

- What to check: Extra fee charged by the ATM owner

- Why it changes the real price: Even a good card cannot remove the machine operator's surcharge

Here is a quick comparison of all the cards above based on extra fees. Each card's costs are broken down in the same order so the comparison is direct.

Coinbase Visa Debit Card

- Spread Or Conversion Cost: 0% on USD or USDC; other crypto spend uses spread

- ATM Fees And Limits: $0 Coinbase ATM fee; ATM operator fee may apply; public limit is up to 3 ATM or OTC cash withdrawals from each, no more than 6 per day, and no more than $1,000 per 24 hours

- Annual Or Monthly Fee: $0 / $0

Nexo Card

- Spread Or Conversion Cost: Debit Mode converts through Nexo Exchange; Credit Mode avoids a sale but can add borrowing cost

- ATM Fees And Limits: Free to tier limit, then 2% with minimum €1.99/£1.99

- Annual Or Monthly Fee: $0 / $0

KAST Card

- Spread Or Conversion Cost: Stablecoins convert 1:1 to USD; non-stablecoin deposits convert at 2%-5%

- ATM Fees And Limits: $3 + 2%; up to $250 per withdrawal and $750 per 24 hours

- Annual Or Monthly Fee: $0 / $0 on Standard

Bybit Card

- Spread Or Conversion Cost: Usually 0.9% crypto conversion; FX conversion cost varies by card program; current FX fees range between 1%-7%, with separate FX padding of 0%-5% depending on program

- ATM Fees And Limits: 2% after the free monthly allowance, but the allowance is program-specific: first 100 USD monthly in Australia, AIFC, and Georgia; first 95,000 ARS in Argentina; first 550 BRL in Brazil; and first 1,800 MXN in Mexico. ATM operators may also charge their own fee.

- Annual Or Monthly Fee: $0 / $0

Worked Examples

These examples use realistic spend scenarios to show what each card actually costs in use.

Scenario 1: $500 online purchase in USD, paid from USDC balance

Coinbase charges no FX fee and no conversion fee on USDC spend. The $500 purchase costs $500. KAST converts stablecoins 1:1, so the same purchase also costs $500 with no spread. Nexo converts through Nexo Exchange in Debit Mode, so the cost depends on the rate applied at checkout. Bybit charges a crypto conversion fee of around 0.9%, which adds roughly $4.50 to a $500 purchase before any FX padding.

Scenario 2: EUR100 purchase while traveling, paid from a USD balance

Coinbase has no FX fee, so the cost is close to the spot rate. KAST charges 0.5%-1.75% on non-USD spend, adding EUR0.50-1.75 to a EUR100 purchase. Nexo charges 0.2% for EEA currencies on weekdays, so EUR100 costs about EUR100.20; on weekends, the surcharge adds another 0.5%, bringing it to EUR100.70. Bybit's FX fee for the same purchase depends on the card program, but the stated range of 1%-7% means a EUR100 purchase could cost between EUR101 and EUR107 before any FX padding.

Scenario 3: $100 ATM withdrawal

Coinbase charges no issuer ATM fee up to the public limit of 3 withdrawals per day, so $100 out costs $100 plus any machine operator fee. KAST charges $3 + 2%, so the same withdrawal costs $5 in issuer fees, plus any operator fee. Nexo covers ATM withdrawals free up to the tier limit; above it, the fee is 2% with a minimum of €1.99/£1.99. Bybit charges 2% after the monthly free allowance is used, so a $100 withdrawal above the limit costs $2 in issuer fees plus any operator fee.

If travel matters, this page is a starting point. The wider travel angle, including FX and ATM rules, is covered in international crypto card options.

Are Crypto Cashback Cards Worth It After Fees?

A reward rate only matters after the card's other costs are counted. A free crypto card with 1% or 2% cashback can still be poor value if the user pays spread on every BTC purchase, needs a paid tier to unlock rewards, or pays extra on foreign spend.

Token rewards and points also lose value quickly when redemption is limited. If the reward is easy to use or convert, simple spend savings are often worth more than a larger-looking cashback rate. The crypto rewards cards page covers this comparison in more detail.

Free Crypto Virtual Cards Vs Physical Crypto Cards

Many of the best free crypto cards are better described as free virtual cards first. That matters most for users who shop online, use mobile wallets, or want instant access after approval.

For more on this side of the market, see the lists of top virtual cards and crypto cards with Apple Pay and Google Pay support.

The decision between virtual and physical usually comes down to how you spend. The points below split the cases where each format has a real advantage.

Virtual cards matter more when:

- You mainly shop online

- You want instant access after approval

- You use Apple Pay or Google Pay often

- You want to avoid shipping or replacement costs

Physical cards matter more when:

- You need ATM access

- You travel often

- You pay at merchants that reject wallet payments

- You want a backup if your phone or app is unavailable

A free crypto virtual card can be all you need if most of your spending is online or through mobile wallets. Once ATM access, wider merchant acceptance, or travel becomes important, the physical card cost becomes part of the decision.

Crypto Debit Cards Vs Crypto Credit Cards On Fees

Free crypto debit cards and free crypto credit cards solve different problems. Debit cards work better when you want direct control over a spending balance. Credit cards work better when you want to avoid selling crypto at checkout and repay from cash later. The comparison below covers the main cost difference between the two models.

Card model comparison:

- Crypto Debit Card

- Usually cheaper for: Spending from USD, USDC, or a stablecoin balance

- Main cost risk: Spread and tax friction when the card sells volatile crypto

- Best fit: Users who want direct balance spending and tight budget control

- Crypto Credit Card

- Usually cheaper for: Everyday spending when the balance is repaid on time

- Main cost risk: Interest, late fees, and cash-advance costs

- Best fit: Users who want crypto rewards without liquidating crypto at checkout

If you are still choosing between card models, the comparison of the best crypto debit cards is a good place to narrow the shortlist.

Common Crypto Card Fees To Avoid

The most expensive card terms are often the ones hidden behind the word “free.” A free crypto debit card can still be a poor pick when the entry path looks far better than the long-term usage path. The list below covers the costs most likely to be missed before signup.

- Free virtual card, but paid physical card and shipping

- No application fee with expensive conversion spread

- Great rewards locked behind staking or paid tiers

- Small transaction fees that punish daily use

- Inactivity fees on abandoned balances

- Declined transaction fees

- Cheap domestic spend but weak foreign spend

- Free ATM allowance followed by steep fees

- Rewards paid as points or token perks rather than usable cashback