Crypto cashback cards look similar on the surface. The difference shows up in the reward rules. Some cards pay fixed crypto on every purchase. Others use rotating offers, paid tiers, loyalty-token requirements, or points whose value depends on how and when you redeem them.

The headline rate alone is not enough to judge a card. The better options in this group combine solid rewards with terms that are easy to verify before signup. Published rates, reasonable unlock conditions, and low fee drag matter more than a large advertised number.

Top Crypto Cashback Cards

- No coin sold at checkout, no per-swipe tax

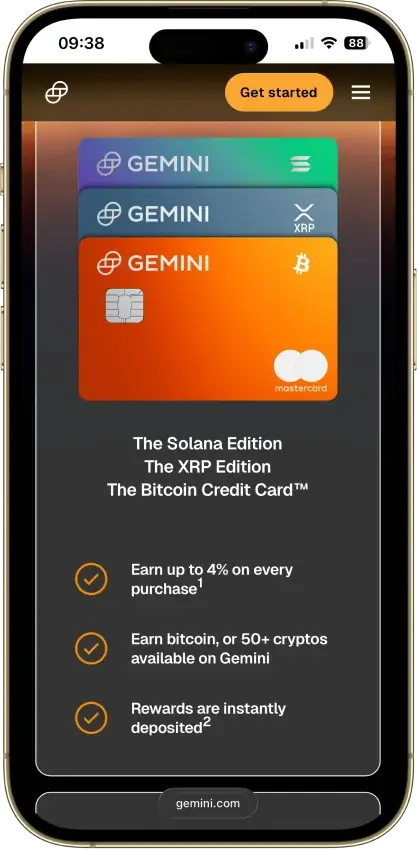

- Bitcoin, XRP, and Solana card editions

- 10% back at rotating partner merchants

- Virtual US bank numbers for ACH and wires

- Free instant transfers to other KAST users

- No card spending ceiling, USD spend at 0%

- Stablecoin funding avoids tax on each swipe

- Spend gold and silver balances at checkout

- One app for wallet, trading, and spending

- Tap to switch Debit and Credit Mode

- Fund from stablecoins, fiat, or Savings crypto

- Spend borrowed funds, keep coins as collateral

- Switch your reward coin before each purchase

- No card balance to top up or strand

- 24/7 phone support with a dedicated card line

Gemini ranks first because its reward terms are clear before approval and easy to judge from day one. Nexo and Uphold can pay more under the right conditions, but both require more from the user to get there. Coinbase has the lowest barrier to entry, and KAST suits users already spending stablecoins who are willing to track promo rules in the app.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | credit | Apple Pay, Google Pay, Samsung Pay | All 50 US states + Puerto Rico, US residents only |

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Visa, Mastercard | Debit | Apple Pay, Google Pay | United States and the United Kingdom. In the U.S., the card is not available in New York, Louisiana, or U.S. territories. In the U.K., Crown Dependencies and British Overseas Territories are excluded. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

Gemini and Uphold are the easiest to compare because their reward structures are publicly available and relatively stable. Nexo can work well for users already deep in its ecosystem, but the best rate depends on loyalty status and which card mode is active. Coinbase requires a fresh check in the app each cycle, and KAST depends more on live promo terms than on a fixed cashback schedule.

Crypto Cashback Cards Reviews

Gemini Credit Card

Pros

- Uncapped 3% dining and 2% grocery rewards

- $0 annual fee and $0 foreign transaction fee

- Instant payout in a choice of 50+ cryptos

- WebBank-issued Mastercard World Elite

- Soft-pull pre-qualification before applying

Cons

- 4% tier capped at $300 spend a month

- 1% base rate on most spending

- 16.49%–28.49% variable APR if you revolve

- US residents only, hard credit pull

- Rewards taxable at receipt and disposal

Kast Card

Pros

- 1.5% USD cashback on the free tier

- Stablecoins load 1:1 with no spread

- Virtual card minutes after a two-minute KYC

- US-available, unlike most crypto cards

- Five stablecoins across major chains

Cons

- Volatile crypto is sold on deposit at 2%–5%

- Free-tier cashback stops at $2,000 a month

- ATM cash costs $3 + 2%, capped at $750 a day

- Top cashback rates cost $1,000–$10,000 a year

- Custodial USD balance, no self-custody

Uphold Card

Pros

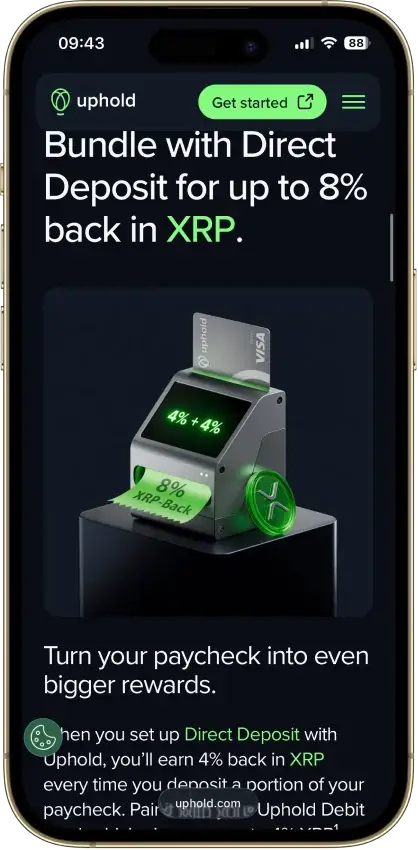

- 4% XRP on crypto-funded spend with Elite

- 0% FX and $0 ATM withdrawals on Elite

- Funds from 200+ assets, metals included

- Fiat and stablecoin funding skips the spread

- US issuer Cross River Bank is an FDIC member

Cons

- Top terms locked to the $99.99/yr Elite tier

- US rewards pay in XRP only, no switching

- Essential adds 1.50% FX and $2.95 ATM fees

- Crypto-funded spend takes a spread, plus tax

- UK card pays 1% GBP, zero on crypto funding

Nexo Card

Pros

- Credit Mode sells no crypto at purchase

- No monthly, annual, or inactivity fees

- 0.2% weekday FX in the EEA, UK, and CH

- Idle Debit Mode balance earns daily interest

- Issued by DiPocket UAB, a licensed EMI

Cons

- EEA and UK only, US persons excluded

- Physical ordering paused since Jan. 2025

- Cashback needs Credit Mode and a $5,000+ portfolio

- 2–2.5% FX outside the EEA, UK, and CH

- Base rates: 0.5% NEXO or 0.1% BTC

Coinbase Card

Pros

- $0 annual, monthly, and foreign transaction fees

- USD and USDC spend at par with no spread

- No credit check, staking, or lockup to earn

- Instant virtual card plus Apple Pay and Google Pay

Cons

- Crypto spend triggers spread plus taxable sale

- Reward rates are app-set, never published

- $2,500 daily spend cap binds on big purchases

- US-only rewards, and Hawaii is excluded

Our Ranking Methodology

This ranking focused on the reward a user is likely to keep once the fine print is applied, looking past the headline rate to check how much value remains after caps, annual fees, token requirements, FX costs, and reward format are factored in.

- Reward value after caps and exclusions

- How hard it is to unlock the best rate

- Whether rewards are paid in crypto, points, or promo tokens

- Fees, spreads, FX costs, and subscription drag

- Availability, KYC friction, and funding model

- How usable the card is in daily spending

- Tax and reporting friction when spending crypto

Cards with clear, published reward terms ranked higher. A lower rate could still beat a higher one when the value was easier to verify and did not depend on paid tiers or token holdings.

What Crypto Cashback Really Means On Reward Cards

Crypto cashback can mean different things. Some cards deposit crypto directly into the linked account after each purchase. Others pay points, limited-time promo credits, or rotating rewards that change from month to month.

That distinction changes how a reward should be judged. A stable reward table is easy to value before the first purchase. A points or promo system takes more checking because payout timing, redemption rules, and asset choice all affect what the reward is actually worth.

- Direct crypto rewards

- Reward points that need redemption

- Promo rewards that are not permanent

- Cashback rates that change by month, category, or plan

The label alone is not enough. What matters is how the reward is paid and what it is worth once the conditions are applied.

Cashback Rates, Caps and Excluded Purchases

A cashback rate only helps if it applies to the purchases a user makes most often. Caps, bonus categories, excluded merchants, and refund rules can reduce the real payout faster than most first-time card users expect.

| Reward Rule | What To Check | Why It Matters |

|---|---|---|

| Base reward rate | Standard rate outside promos and bonus categories | This is the floor on normal spend |

| Max reward rate | Highest published rate and exact conditions | Shows whether the top number is widely usable |

| Monthly reward cap | Spend limit, reset timing, and post-cap rate | Caps can lower the real rate quickly |

| Category bonuses | Eligible categories and merchant coding rules | Wrong merchant coding can cut the reward |

| Excluded merchant types | Cash-like payments, gift cards, fees, tax payments | Common spend may earn nothing |

| Reward reversals on refunds | Whether refunds claw back rewards and when | Returns can reduce later payouts |

| Reward expiry or rotation | End dates, monthly changes, and promo windows | Harder to value over time |

A lower rate can still be the better deal if the base rate applies broadly and the exclusions stay narrow. The weaker setups advertise a high number, then reduce the real value with tight categories, low caps, or frequent changes.

Bitcoin, Stablecoin and Token Rewards Explained

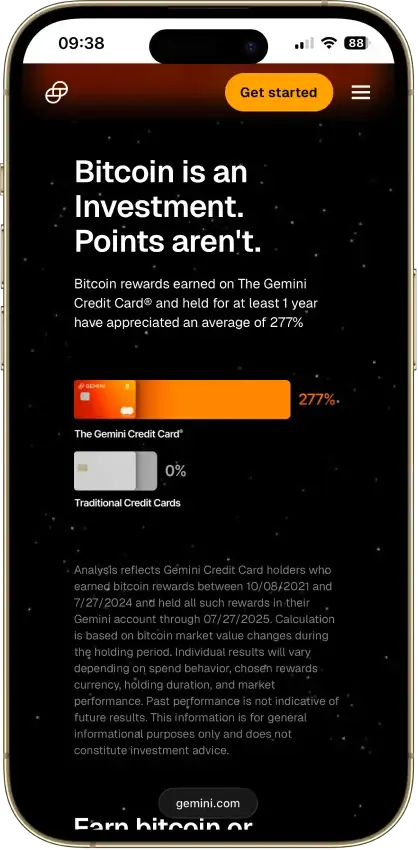

Two cards can both advertise 2% back and still produce very different results. A reward paid in bitcoin behaves differently from one paid in a stablecoin, a platform token, or points. The reward asset affects price risk, liquidity, and how easy it is to hold, sell, or track after payout.

Bitcoin rewards are the easiest to understand because BTC is liquid and widely supported. Stablecoin rewards are easier to budget around because the value holds after payout. Platform tokens, smaller altcoins, and points balances need a closer look because the final value depends on platform rules, market liquidity, and redemption options.

- Bitcoin rewards: easy to price and sell

- Stablecoin rewards: lower volatility after payout

- Exchange-token rewards: often tied to platform loyalty

- Altcoin rewards: more price risk after payout

- Reward points: value depends on redemption rules

For most users, the safer reward is the one that is easiest to price on day one and easiest to use a month later. A lower rate paid in bitcoin or a stablecoin can be more practical than a higher rate paid in points or a thinly traded token.

Crypto Cashback Taxes and Reporting

Tax treatment depends on jurisdiction, but the reporting burden can be heavier than most card users expect. In places that treat crypto as property, spending crypto or stablecoins can create a disposal event, and selling reward assets later can create another one.

- Receiving rewards

- Spending crypto

- Spending stablecoins

- Swapping reward tokens

- Refunds and chargebacks

- Exporting transaction history

A small cashback rate can stop looking attractive when every purchase adds a record-keeping obligation. Users who want lower reporting friction are usually better served by fiat-funded cards, stablecoin-funded spend, or cards that make transaction history easy to export.

Important: Tax reporting can differ between crypto rewards credit cards and debit-based crypto cards.

Common Crypto Cashback Mistakes

Most mistakes start with treating the cashback rate as the whole story. The reward only makes sense once the card model, funding source, and full cost structure are checked together.

- Chasing the headline rate

- Ignoring caps

- Ignoring token price risk

- Treating points like cash

- Spending volatile crypto for small purchases

- Missing category exclusions

A useful test is one month of normal spending. That shows what the reward is actually worth after fees, limits, and payout rules are applied.