Overview

Introduction

Crypto-as-a-Service (CaaS) is the “build crypto products without building a crypto exchange” approach. Your institution keeps the customer relationship, product governance, and brand experience; a specialist provider supplies wallet infrastructure, execution rails, custody options, and operational tooling to run crypto safely at scale.

This matters because most regulated institutions do not fail on “can we build it.” They fail on operational risk: custody controls, fraud, reporting, and the day-two responsibilities that come after launch.

In this guide, you will learn:

- Why banks, telcos, and fintechs are revisiting crypto products now, without relying on hype

- What CaaS includes (and what it does not) for procurement, risk, and compliance teams

- A reference architecture for integrating a CaaS stack into identity, core ledger, and support tooling

- A phased rollout plan for a “minimum viable crypto product,” including the guardrails that prevent regrets

- How to evaluate security, custody, compliance workflows, payments rails, economics, and vendors

Who this guide is for: fintechs, banks, neobanks, telcos, payment providers early in crypto adoption, plus brokerages and smaller exchanges adding rails.

Disclaimer: Informational only, not financial, legal, or compliance advice. Regulations vary by jurisdiction; involve your legal and compliance teams early.

Timing shift

Why CaaS now for banks, telcos, and fintechs

A few years ago, “adding crypto” often meant bolting a volatile asset class onto a consumer app and hoping demand carried the product. That era is fading. Today, institutions revisiting crypto are doing it with more pragmatic goals and tighter controls.

Demand is real, but needs governance

Customer demand exists across multiple use cases, and it is rarely “just trading.” Common asks include trading and conversion, transfers, spending, and treasury utility. The challenge is not demand, it is delivering a controlled experience with clear disclosures, predictable operations, and compliant workflows.

Competitive pressure is structural

Neobanks and super-app style fintechs increasingly bundle more financial services under one roof. Crypto is often on the shortlist because it can lift engagement and retention, but only if the product is reliable and supportable at scale.

Monetization is measurable

Crypto products can be evaluated like any other financial product line. Common levers include conversion take rate, spreads (with transparent disclosure), transaction fees, premium tiers, and retention-driven revenue per user expansion. The key is to model unit economics alongside risk and operational cost from day one.

Partnerships shorten the path

For many newly launching banks and fintech programs, the most realistic path is integration: white-label partners and core-banking providers can connect to a CaaS provider so a new institution can receive crypto functionality without standing up every component internally.

WhiteBIT tie-in: CaaS is positioned as a faster, lower-risk route than building a full stack, especially when you want to keep governance inside the institution while outsourcing specialized infrastructure.

Clear lines

CaaS explained, what it is and what it is not

In procurement-friendly terms, Crypto-as-a-Service (CaaS) is a packaged set of capabilities that lets a bank, fintech, or telco offer crypto functionality without operating an exchange stack in-house.

What CaaS typically includes

- Wallets and address generation: creating deposit addresses, tracking balances, orchestrating transactions

- Custody options: platform custody, third-party custody integrations, or hybrid designs

- Pricing and execution: fiat to crypto conversion, quote formation, execution rules, slippage and limit logic

- Compliance tooling: KYB and KYC alignment, sanctions checks, monitoring outputs, recordkeeping support

- Reporting and reconciliation: ledger feeds, statements, audit logs, operational exports

- Operational support: onboarding coordination, incident response processes, ongoing technical account support

What CaaS is not

CaaS does not outsource accountability. Your institution still owns customer outcomes, product governance, disclosures, complaint handling, fraud policy, and regulator relationships. Treat CaaS as infrastructure, not a compliance shield.

It is also not “set and forget,” and it is not one-size-fits-all. Crypto products remain operationally alive: networks change, fraud patterns evolve, and compliance expectations shift. Your implementation must be designed for ongoing operations, not just launch.

Build vs buy vs partner

| Decision path | Best when | Watch-outs |

|---|---|---|

| Build in-house | You have deep crypto engineering plus 24/7 operations and want full control over custody and execution | Long time-to-market, higher security and compliance burden, harder to maintain across chains |

| Buy point solutions | You want best-of-breed vendors (custody, analytics, payments) and can manage multi-vendor integration | Integration complexity, vendor sprawl, unclear incident ownership, slower delivery |

| Partner via CaaS | You want fast, controlled launch with fewer moving parts and clearer shared processes | Must negotiate strong SLAs and evidence, confirm jurisdictional permissions, plan exit strategy |

Optional add-on, yield style products

Some institutions explore yield-like features for eligible users and jurisdictions, such as crypto lending. Treat this as a separate risk decision with its own approvals, disclosures, and controls.

WhiteBIT tie-in: WhiteBIT positions “one place for institutional crypto needs” with modular services and tailored onboarding, which can be helpful when your roadmap expands from conversion to custody and payments.

System map

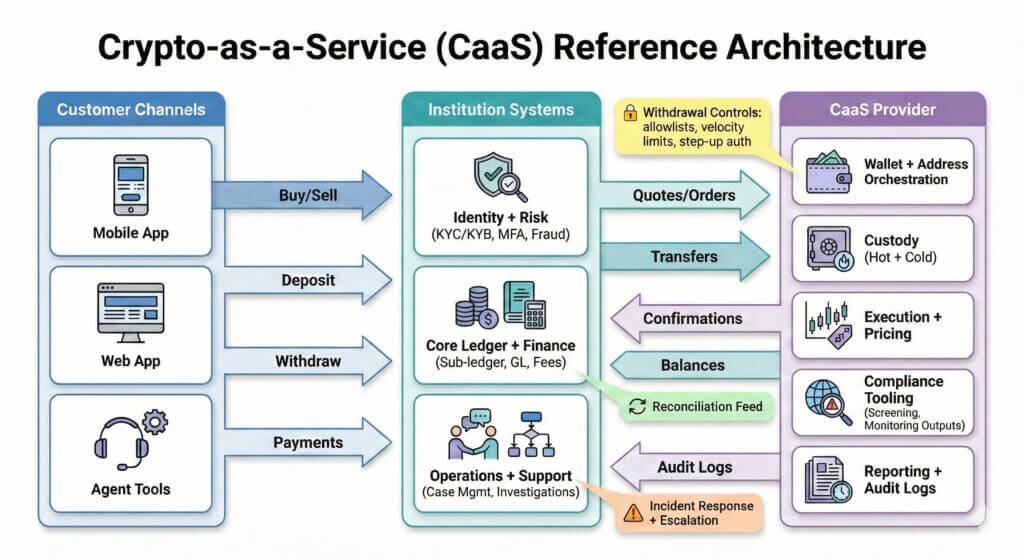

The reference architecture, how a CaaS stack fits into your systems

A successful CaaS launch starts with a clear integration map, not just API endpoints. The question is: where does crypto live in your operating model, and how does it connect to identity, ledger, and support workflows?

Core systems to connect

Most institutions integrate CaaS across four layers:

- Channels: mobile app, web app, agent tools, or telco channels

- Identity and risk: KYC and KYB, MFA, device intelligence, fraud scoring, step-up auth

- Core ledger and finance: sub-ledgers, GL mapping, fee logic, reconciliation, reporting exports

- Operations and support: case management, investigations, customer support tooling, incident playbooks

Wallet orchestration is the hard part

The tricky part is not “making a wallet.” It is address management and transaction orchestration across networks: deposit address generation, withdrawal controls (whitelists, velocity limits), chain incident handling, fee volatility, and operational visibility.

Execution, reconciliation, and reporting

Even for a simple “buy and hold” product, finance and audit teams will ask how prices are formed, how conversion is executed, how balances reconcile between your ledger and custody environment, and what logs exist for every administrative action and customer transaction.

Phased launch

Launch path, the “minimum viable crypto product” in phases

The safest institutional pattern is to launch crypto in phases. Each phase expands surface area, assets, networks, corridors, only after controls prove stable and operations can support real usage.

Phase 1, convert and hold

Start with buy and sell conversions and custody, using a limited asset allowlist and conservative limits. Keep the experience simple, optimize onboarding and disclosures, and verify reconciliation and support readiness before expanding features.

Phase 2, deposits and withdrawals

Add deposit addresses and withdrawals on approved networks. This is where operational complexity increases: chain fees, address mistakes, fraud attempts, and compliance workflows will surface. Expand networks slowly, and ship “withdrawal safety” features early.

Phase 3, advanced utility

Recurring buys, broader conversion paths, B2B payouts, merchant settlement, and treasury workflows come last. These features can be valuable, but they magnify compliance and operational demands.

Guardrails that prevent regrets

Regardless of phase, the core guardrails are consistent: asset allowlists, transaction limits, network risk scoring, and step-up authentication for high-risk actions.

| Phase | What customers get | Controls and KPIs to gate expansion |

|---|---|---|

| Phase 1, convert plus hold | Fiat to crypto conversion, custody portfolio, basic statements | Controls: small allowlist, conservative limits, step-up auth, clear disclosures. KPIs: conversion success rate, fraud rate, support tickets per 1,000 users, reconciliation breaks. |

| Phase 2, transfer rails | Deposits and withdrawals on approved networks, address book | Controls: withdrawal whitelists, velocity limits, network risk scoring, recordkeeping for transfers. KPIs: withdrawal failure rate, time-to-resolution for incidents, suspicious activity alert backlog. |

| Phase 3, utility plus B2B | Recurring buys, B2B payouts, merchant settlement, treasury conversion | Controls: counterparty controls, enhanced KYB, payout screening, settlement rules, stronger SLAs. KPIs: retention uplift, revenue per user uplift, payout SLA adherence, audit findings severity. |

Safety rails

Security and custody design choices institutions must get right

Custody is usually the biggest blocker because it concentrates operational, legal, and reputational risk in one place. Start by choosing a custody model aligned to your governance requirements, then focus on the controls that govern day-to-day operations.

Custody models to consider

| Model | Strengths | Risks to mitigate |

|---|---|---|

| Platform custody | Fastest go-live, fewer vendors, simpler customer UX | Provider concentration risk, require evidence of controls, segregation clarity, withdrawal governance |

| Third-party institutional custody | Clear separation, aligns with some governance models | Integration overhead, operational handoffs, slower incident response if roles are unclear |

| Hybrid custody | Segmented risk and flexibility by segment or asset type | More complex reconciliation, higher governance burden, avoid shadow processes |

Controls that matter most

Security discussions often over-focus on “cold vs hot.” For institutions, the non-negotiables are operational controls:

- Withdrawal whitelisting and address books

- Multi-approver withdrawals with segregation of duties

- Role-based access controls for internal operators

- Incident response playbooks plus audit-ready logging

- Strong customer authentication and account takeover defenses

Non-negotiable controls checklist

- Withdrawal allowlists plus velocity limits

- Maker-checker approvals and segregation of duties

- RBAC plus privileged access management

- Incident response, defined escalation paths, post-incident reviews

- Audit logging for administrative actions and fund movements

If a vendor cannot evidence these controls, “fast launch” becomes an institutional liability.

How WhiteBIT approaches it

Industry challenge: Institutions need enterprise-grade custody controls, but many crypto stacks were built for retail speed over institutional governance.

What institutions should require: Clear custody documentation, withdrawal governance, access controls, and independent validation that matches the scope of services used.

WhiteBIT approach: WhiteBIT positions custody as part of a broader institutional stack, including integrations with institutional custody infrastructure, alongside an onboarding model designed to align operational controls with institutional requirements.

Control plane

Compliance and AML, responsibilities, workflows, and reporting

Crypto compliance is not a single checkbox. It is an operating workflow spanning onboarding, monitoring, investigations, and audit-ready recordkeeping. A CaaS model can provide tooling and support, but the institution must still own governance decisions and regulator-facing accountability.

What “compliance” looks like in practice

- KYB and KYC alignment: onboarding, risk tiering, beneficial ownership for business accounts

- Sanctions screening: counterparties, jurisdictions, and relevant indicators

- Transaction monitoring: typologies, structuring patterns, mule behavior, unusual flows

- Recordkeeping: audit trails for decisions, approvals, and administrative actions

- Investigations: case management, escalations, SAR or STR workflows (as applicable)

Travel Rule and recordkeeping, high-level considerations

Transfer rules and recordkeeping requirements differ by jurisdiction and can affect user experience, especially for withdrawals and transfers involving self-custody. Treat these obligations as product requirements, not back-office details, because they directly impact funnel conversion and support load.

RACI snapshot, who does what

| Process | Institution owns | Provider supports |

|---|---|---|

| Asset and network allowlist | Governance, approvals, disclosures | Asset availability, technical constraints, network risk inputs |

| Customer onboarding | KYC and KYB policy, risk tiering, communications | Integration guidance, operational coordination, tooling support |

| Monitoring and investigations | Case handling, filing decisions, audit responses | Monitoring outputs, logs, data exports, escalation support |

| Incident response | Customer comms, product decisions (pauses, limits) | Technical incident handling, restoration updates, root-cause inputs |

Money movement

Payments and corridors, where WhitePay fits

For many institutions, crypto becomes real when it becomes money movement: merchant acceptance, treasury conversion, and payouts across borders. That is where acquiring and rails turn crypto into a product line, not a feature.

Merchant and PSP use cases

- Accept crypto payments: offer crypto as a payment method at checkout or invoice

- Settlement choices: settle into crypto, stable assets, or preferred balances depending on setup

- Treasury conversion: convert inflows under defined FX and settlement policies

- Mass payouts: creator payouts, affiliate payouts, rewards, and cross-border disbursements

Why corridors and payout options matter

Corridors shape adoption. The more predictable the path from “customer pays” to “merchant settles,” the easier it is to operationalize. Institutions should define which corridors are allowed, how counterparties are screened, and what settlement timing customers and merchants can expect.

Operational considerations

Payments introduce real-world messiness that must be designed in:

- Refund handling: define how refunds work and how FX is treated

- Rate transparency: define how rates are set, when they are locked, and how spreads are disclosed

- Settlement timing: define SLAs and handling for delayed or failed settlement

- Reconciliation: ensure finance receives clean, audit-ready exports

WhitePay is positioned for crypto acquiring and rails, which can complement a CaaS rollout when you move from conversion into merchant and payout use cases.

Unit math

Economics and KPIs, how leaders evaluate success

The economics of a crypto product are easy to overestimate if you look only at trading fees. Leaders should evaluate a broader model that includes conversion, retention, operational cost, and risk outcomes.

Revenue drivers

- Conversion take rate for fiat to crypto and crypto to fiat

- Spread capture, with transparent disclosure and governance

- Payments economics, acquiring fees, settlement spreads, treasury conversion

- Premium tiers, higher limits, advanced features, priority support

- B2B pricing, bespoke commercial terms for corridors, payouts, and treasury

Cost drivers

- Compliance operations, investigations, staffing, audits

- Fraud and account takeover losses, plus prevention tooling

- Support burden, especially around withdrawals and verification

- Chain fees and network operations

- Vendor costs, minimums, and ongoing maintenance

KPI dashboard template

| KPI | Definition | Why it matters |

|---|---|---|

| Activation rate | Percent of eligible users who complete onboarding and make first conversion | Measures funnel health and flags KYC or UX friction |

| Retention, 30 and 90 days | Users returning to convert, hold, transfer, or pay | Validates product fit and supports LTV modeling |

| Crypto balances held | Total customer crypto balances held, by asset | Signals adoption and informs custody and liquidity planning |

| Incident rate | Count of security or compliance incidents per month | Board-level risk signal and control maturity indicator |

| Reconciliation breaks | Count and severity of ledger mismatches | Core finance risk, should trend toward zero |

| Support burden | Tickets per 1,000 active users plus satisfaction proxy | Signals UX clarity and operational readiness |

WhiteBIT emphasizes fair pricing positioning and customizable commercial models, which should be evaluated against your unit economics, SLAs, and operational requirements.

Buyer checklist

Vendor evaluation checklist, questions to ask in procurement and security review

A CaaS vendor may look complete in a demo, but institutions should evaluate evidence, not claims. The goal is to answer three questions:

- Can this provider support your operating model and regulator expectations?

- Are responsibilities and incident paths crystal clear?

- Can you exit or change scope without being trapped?

Due diligence checklist

| Area | Questions to ask | Evidence to request |

|---|---|---|

| Technical | Is the API mature? Is there a sandbox? How are breaking changes communicated? What logs and webhooks exist? | API docs plus changelog, sandbox access, uptime history, sample logs and webhooks |

| Security | What is the custody model? How are withdrawals governed? How is access controlled? What is the incident response process? | Security overview, withdrawal policy, RBAC model, incident runbook, audit or certification scope |

| Compliance | How do KYB and KYC workflows integrate? What monitoring outputs exist? What reporting exports support audits? | Workflow documentation, export formats, sample case fields, data retention and audit logging description |

| Commercial | What are fees and minimums? What are SLAs? What is the implementation timeline and post-launch support coverage? | MSA plus SLA, pricing schedule, implementation plan, named escalation path and support model |

How WhiteBIT approaches it

Industry challenge: Procurement and security reviews often stall because vendors cannot produce audit-ready evidence quickly.

What institutions should require: Clear SLAs, defined custody controls, compliance workflow documentation, and a named escalation path for incidents and operational issues.

WhiteBIT approach: WhiteBIT positions a comprehensive institutional suite across CaaS, custody, and payments, with a relationship-led model intended to reduce procurement friction when paired with clear evidence, documentation, and implementation planning.

Implementation path

FAQ plus next steps

How long does launch really take?

Timelines depend on scope (convert-only vs transfers vs payments), your KYB and KYC readiness, your control requirements, and how many systems you need to integrate. Treat any public “go-live” claims as a starting point, and insist on a concrete implementation plan with milestones and acceptance criteria.

What assets and networks should we start with?

Start with a conservative allowlist and the simplest networks you can operationally support. Expand only after withdrawal controls, monitoring, and support playbooks perform reliably at real volumes.

Who holds customer funds, and how is segregation handled?

That depends on your custody model (platform, third-party, or hybrid). Ask for clarity on account structures, withdrawal governance, reconciliation processes, and what segregation means operationally in your specific setup.

What data and reporting do regulators and auditors expect?

Expect to produce onboarding evidence, transaction histories, monitoring outputs and case outcomes, and audit logs for administrative actions. If you support transfers, plan for jurisdiction-specific recordkeeping and data requirements as part of product design.

How do we handle fraud, account takeovers, and withdrawals?

Treat withdrawals as the highest-risk flow. Use step-up authentication, allowlists, velocity limits, and internal approval workflows. Invest early in customer education and support scripts, because many high-volume “fraud” tickets start as UX confusion at withdrawal time.

Can we add crypto payments later?

Yes. Many institutions start with convert and hold, then add payments and corridors once operational maturity is proven. Payments require additional work around refunds, settlement timing, FX policy, and reconciliation exports.

Build your institution’s CaaS launch plan with WhiteBIT

If you are evaluating a crypto rollout, start by mapping your reference architecture, custody model, and compliance responsibilities. A short scoping call can clarify your minimum viable phase and the controls required to scale safely.