Europe is its own crypto-card market. A card can look global at first glance, then become awkward once country rules, bank-transfer support, euro funding, and compliance checks come into view.

The strongest options in Europe do more than allow signups from part of the region. They work well with EUR balances, fit SEPA transfers, hold up on trips outside the eurozone, and do not turn KYC, proof-of-income, or source-of-funds checks into a constant obstacle.

Top Crypto Cards In Europe

- Up to 4% back in XRP (U.S.).

- Spend 200+ assets with instant virtual card.

- No foreign transaction fees on Elite tier.

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Up to 5% CRO rewards with instant payout after each purchase.

- Instant virtual card with broad Apple Pay and Google Pay support (region dependent).

- No annual fee and high daily purchase limits up to $25,000.

- Up to 8% Cryptoback rewards (tier-based, paid in WXT)

- $0 annual fee + 0% marketed FX fees on card spending

- Multicurrency spending from fiat, stablecoins, and crypto in one app

A genuinely Europe-friendly crypto card is built around local banking and cross-border use. The difference shows up in funding speed, FX costs, and how much friction appears once account activity starts to look more like real daily spending.

In Europe, coverage, euro-bank fit, non-euro travel costs, and compliance friction often matter more than headline rewards. They decide whether a card works smoothly with local banking, local rules, and everyday cross-border spending.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Visa | Debit | Apple Pay, Google Pay | United States and the United Kingdom. In the U.S., the card is not available in New York, Louisiana, or U.S. territories. In the U.K., Crown Dependencies and British Overseas Territories are excluded. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay, Samsung Pay | Available in many regions (e.g., US, EEA/UK, SG, CA, AU, BR) with residency-based eligibility and restricted markets per Crypto.com lists. |

| | Visa, Mastercard | Debit | Apple Pay, Google Pay | Available in UK and many countries (incl. parts of EEA, AU, NZ, HK, TW), while not available in USA, Canada, China, Japan, South Korea, Philippines, Russia (among others); EEA Mastercard eligibility requires EEA residency excluding Cyprus & Liechtenstein. |

The priority changes with the funding and spending pattern. Euro bank transfers make EUR and SEPA fit more important. Frequent trips outside the euro area put more pressure on FX costs. Larger account activity makes compliance friction harder to ignore.

The Best Europe Card Depends On How You Spend

The right pick changes with the money flow. Daily euro spending, stablecoin funding, travel outside the eurozone, and support needs do not all point to the same kind of card.

| Spending Pattern | Prioritize | What Usually Decides It |

|---|---|---|

| Eurozone daily spend | Clean EUR rails | Easy funding, low friction, stable everyday use |

| Non-euro travel | FX efficiency | Foreign-currency costs and merchant reliability |

| Stablecoin-heavy use | Simple conversion path | Low drag from crypto balance to spendable card balance |

| Reward-focused use | Real net value | Caps, tiers, plan fees, and token exposure |

| Low-friction setup priority | Fast access | Clear country support and fewer extra checks |

| Users who care most about support and reporting | Back-office quality | Better statements, cleaner exports, and clearer dispute handling |

The buying logic starts with how money enters the card and where spending happens after that. Rewards matter, but they only matter after coverage, funding fit, travel costs, and wallet setup friction already make sense.

Crypto Cards In Europe Reviews

Uphold Card

Pros

- Up to 4% XRP rewards on Elite, with a promotional window for new U.S. applicants

- Spend from 200+ assets including fiat, stablecoins, and crypto from one wallet

- Instant virtual card with Apple Pay and Google Pay on both U.S. and U.K. accounts

- No annual fee on Essential

Cons

- Crypto-funded purchases carry a variable conversion spread that reduces net value

- U.S. rewards are XRP-only with no option to switch reward asset

- Essential tier has a $2,500 daily spend cap and $500 ATM limit

- Available only in the U.S. and U.K., with additional state and territory exclusions

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

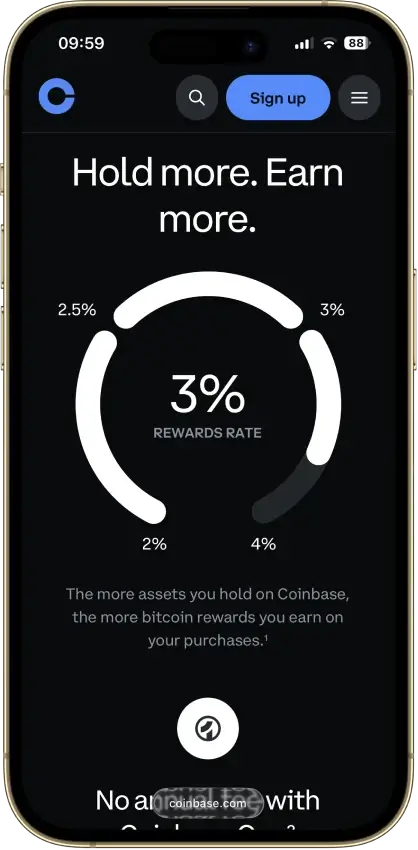

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

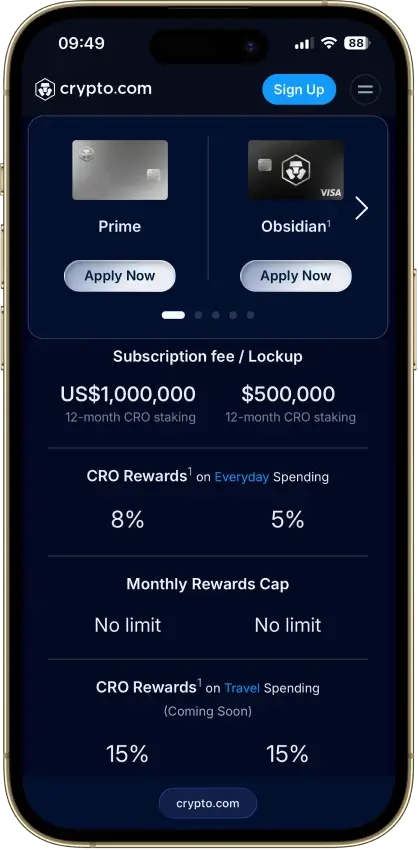

Crypto.com Card

Pros

- Up to 5% CRO back with instant rewards.

- No annual fee and high spending limits.

- Instant virtual card and strong mobile wallet support.

Cons

- 3% foreign fee on lower tiers (US market).

- Monthly cashback caps on mid tiers.

- Requires a monthly fiat subscription or a 12-month CRO lockup to earn rewards.

- Crypto funding includes a conversion spread.

Wirex Card

Pros

- Up to 8% rewards at higher X-tras tiers

- No annual fee

- Strong in-app controls

Cons

- Not available in US

- Rewards paid in WXT

- ATM fees after free limit

How We Ranked The Best Crypto Cards In Europe

The ranking favored options that seem practical for European users once real money starts moving. The strongest picks are convenient to use in supported countries, easy to fund in euros, dependable for normal spending, and manageable once compliance and reporting needs showed up.

We looked closely at:

- Real European availability and signup friction

- Euro funding, SEPA usefulness, and conversion clarity

- Normal spend reliability online, in-store, and through mobile wallets

- Rewards value after caps, tiers, lockups, plan fees, and token exposure

- Total cost across issuance, conversion, FX, ATM use, and other less obvious fees

- App quality, card controls, limits, and daily-use tooling

- Security, custody dependence, freeze risk, support quality, and dispute handling

- Reporting readiness, exports, and record-keeping practicality

Big names and loud cashback claims did not carry much weight on their own. What mattered more was whether a card was actually easy for Europeans to fund, spend with, keep compliant, and track once the first layer of marketing wore off.

Europe Is Not One Card Market

Europe is often treated like one region, but card access does not work that way. The EU, EEA, UK, and Switzerland can sit under the same marketing language while following different issuing, payment, and compliance realities.

“Available in Europe” can also mean selected countries only. Some cards support broad signups across the region. Others support only part of it, or support the app but not the card, or support the virtual card but not physical delivery.

Residency, ID country, and shipping country can all matter at the same time. A person may live in one country, hold documents from another, and want delivery in a third. That can be enough to change eligibility or slow verification.

A card can still feel weird in practice even when it is marketed to Europeans. The friction usually shows up in euro funding, local bank-transfer support, mobile-wallet compatibility, FX costs, and how often extra checks appear once spending starts to look real.

That is why the best buying criteria in Europe are simple: where the card is really supported, how cleanly it handles euros, how it behaves outside the eurozone, and how much compliance friction appears once the account is active.

What To Check Before You Apply In Europe

Before looking at rewards or perks, check whether the card can actually be opened and used in your situation. Most of the painful surprises in Europe come from setup details that seem minor at first.

- Supported country

- Resident versus citizen restrictions

- App availability in local app stores

- Virtual card versus physical card access

- Apple Pay and Google Pay support in your country

- Whether EUR funding works cleanly

- Whether SEPA is supported

- Whether source-of-funds checks are likely

A good signup screen does not always mean a smooth setup. The real friction often appears after account creation, when funding starts, documents are requested, or card access depends on checks that were not obvious at the start.

EUR Funding and SEPA Support

Euro funding shapes whether a crypto card is practical for daily use in Europe or stays stuck in backup-wallet territory. The cleaner the EUR path is, the easier it is to move money in from a bank account, see what balance is actually spendable, and use the card without guessing how conversion will work at checkout.

The SEPA capability deserves a close look, even if the card supports crypto deposits. A long token list does not help much if the euro route is slow, confusing, or full of extra steps. And spending from a custodial wallet balance is not the same as spending from a clean EUR balance that is already ready before the card is tapped.

| What To Check | Better Buying Signal | Red Flag |

|---|---|---|

| EUR funding path | EUR lands as usable spend balance | EUR only funds exchange activity first |

| SEPA support | SEPA in and out both work cleanly | One-way support or unclear withdrawal path |

| Conversion flow | Clear rate, timing, and charged balance | Auto-sell happens with little visibility |

| Spend source | Direct EUR spending is available | Card depends on last-second crypto sale |

| Refund handling | Refund returns to usable balance clearly | Refund path is slow, partial, or confusing |

| App clarity | Balance, fees, and funding status are easy to read | User has to guess what will be charged |

Travel Outside The Eurozone Changes The Decision

Once trips move outside the eurozone, the buying logic changes. The better travel card is usually the one with cleaner FX treatment, usable ATM access, and fewer surprises when payments turn into holds, refunds, or cross-border authorizations.

Midnight/Basic: 0.2% foreign transaction fee on non-EUR and GBP purchases and ATM use within the EU/UK, and 2.0% outside the EU/UK. Other card tiers: no foreign transaction fee. Free monthly ATM limits are €200 / €400 / €800 / €800 / €1,000 by tier, then 2%

| Name | FX cost | ATM access | Travel watch-out |

|---|---|---|---|

| Nexo Card | FX is 0.2% for EEA/UK/CH currencies and 2% for other currencies, plus an extra 0.5% on weekends. | ATM withdrawals are free up to the tier cap, then 2% | Stronger for normal travel spend than for tight-balance use |

| Coinbase Visa Debit Card | No card spend fee disclosed; crypto spread can still apply | No Coinbase ATM fee; operator may charge | Better as a backup travel card than a card for heavy payment holds |

| Crypto.com Visa Card | Midnight/Basic: 0.2% foreign transaction fee on non-EUR and GBP purchases. | ||

| Other card tiers: no foreign transaction fee. | Free monthly ATM limits are €200 / €400 / €800 / €800 / €1,000 by tier, then 2%. | Hotels and rentals can lock balance for longer than expected | |

| Wirex Card | No fixed card FX fee clearly disclosed; in-app conversion cost shows before exchange | Free up to €200/month, then 2% | Works best when the right fiat balance is preloaded first |

| Uphold Card | Not clearly disclosed for UK card spend | Physical card only, £2.50 UK/EU, £3.50 elsewhere | UK-only card; virtual card has no PIN |

Travel should outweigh rewards when foreign-currency spend, ATM cash, or payment holds are part of the routine. A lower-reward card with cleaner FX, clearer cash access, and fewer cross-border surprises is often the better buy.

KYC, Proof Of Income and Source-Of-Funds Checks

Low-friction signup does not always mean low-friction use later. In Europe, the real question is not only whether basic KYC is easy, but how the card behaves once limits rise, funding grows, or account activity starts to look more like normal spending rather than light testing.

That is where proof-of-income and source-of-funds checks enter the picture. These checks are common enough on higher-activity accounts, but they still shape the buying decision because they can slow upgrades, delay funding access, or turn a simple support issue into a longer review.

| Check Area | What It Usually Means For Buyers | Common Friction Point |

|---|---|---|

| Standard KYC | Basic identity and address verification | Delays from document mismatch or country limits |

| Enhanced checks | More review on higher-risk or higher-activity accounts | Extra wait time and more document requests |

| Proof of income | Explaining ongoing earnings or salary source | Harder for freelancers, mixed-income users, or informal earners |

| Source of funds | Showing where larger deposits or transfers came from | Bank, exchange, and wallet history may be requested |

| Higher limits | More usable card and transfer capacity | More scrutiny usually comes with limit growth |

| Trigger events | Bigger top-ups, unusual geography, pattern changes, or profile mismatch | Checks often appear after the account is already active |

| Support after review starts | How easy it is to resolve issues during compliance review | Slow escalation can make a usable card feel unreliable |

A best option is always the one that has transparency in its process, asks for reasonable documents, and stays predictable when the account grows beyond light everyday use.

Crypto Card Rewards

Rewards only add value after the card already works where and how a European user wants to pay. The bigger filters are the payout asset, the cost to unlock the reward, and whether the card asks the user to hold a volatile platform token just to reach a headline rate.

That gets more noticeable in Europe because the reward may land in CRO, NEXO, BTC, GBP, or another asset instead of EUR. A high percentage can look appealing, but it feels weaker once plan fees, token lockups, monthly caps, and extra conversion steps start eating into the real benefit.

| Name | Reward | Requirement | Plan Cost | Real Feel In Europe |

|---|---|---|---|---|

| Wirex Card | Standard Entry 0.5%, Standard Enhanced 1%, Premium Entry 1%, Premium Enhanced 2%, Premium Ultimate 3%, Elite Entry 4%, Elite Enhanced 6%, Elite Ultimate 8% in WXT | Free Standard plan or paid Premium/Elite, with higher tiers unlocked by WXT lockups | Standard free; Premium €9.99/mo or €102/yr; Elite €29.99/mo or €306/yr | Better for heavy spenders who accept WXT |

| Nexo Card | 0.5% to 2% in NEXO or 0.1% to 0.5% in BTC. | Cashback is tied to Credit Mode and requires at least a $5,000 portfolio balance to access Loyalty perks. | No monthly or annual fee | Better if you already hold NEXO |

| Uphold Card | 1% cashback in GBP on purchases funded by GBP balance | No staking shown | No setup or annual fee | Simple, but less clean for EUR users |

| Crypto.com Visa Card | 0% Midnight Blue, 2% Ruby, 3% Jade/Royal, 4% Icy/Rose, 5% Obsidian in CRO | Paid tier or CRO lockup | Free to paid monthly plans on Crypto.com | Headline rate depends on tier |

Rewards add real value when the card already fits the user's country, wallet setup, and spending flow, and when the payout asset is something the user actually wants to keep. They distract when the user has to buy into a token system, pay for a plan, or accept a reward currency that adds another conversion step on top of normal spending.

Taxes, Statements and EU/UK Reporting Reality

EU users now sit under DAC8 reporting rules from 1 January 2026, while UK users do not. That raises the reporting bar for EU-facing crypto platforms, but it still does not remove the need to keep your own transaction records and rebuild cost basis when card spending triggers a crypto disposal events.

| Name | Best If You Want | Export Quality | Biggest Record-Keeping Gap | Reporting Load |

|---|---|---|---|---|

| Wirex Card | Basic statements | PDF or CSV only | No clean card-only ledger; reward and wallet basis still manual | High |

| Nexo Card | One-platform tracking | Good CSV and statements | Card, wallet, and mode changes still need manual tax logic | High |

| Coinbase Card | Cleaner spend history | Better card history inside account | External-wallet basis and sold-to-spend basis still manual | Medium |

| Uphold Card | Simple account export | Decent CSV export | FX detail and external-wallet basis still need manual work | Medium |

| Crypto.com Visa Card | More card-specific export | Stronger export set | Top-ups, liquidations, and rewards still need rebuilding | High |

The most useful exports are card transaction history, full wallet or account history, fee visibility, and a clean timestamped CSV. Reporting usually becomes annoying when the user mixes external wallets, tops up from different chains, earns rewards in a separate asset, or needs to reconstruct the exact point where crypto turned into spendable card balance.