Crypto credit cards are a narrow category. The label gets used loosely, and that creates real confusion: most crypto-linked cards are prepaid or debit products that have nothing to do with revolving credit. True unsecured crypto rewards credit cards are rare in 2026, and crypto-backed borrowing products work on a completely different model. This page covers both because users search for them together, but the difference matters before you apply.

What changes the decision after the headline reward rate is the credit structure itself: whether the product is real revolving credit or collateral-backed borrowing, how approval works, what a carried balance costs, whether spending triggers a crypto disposal, and how much of the reward survives after caps, membership fees, and tax tracking are counted.

Top Crypto Credit Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

Gemini Card and Coinbase One Card suit users who want a familiar credit-card structure first and crypto rewards second. Nexo Card solves a different problem, and it only fits if borrowing against crypto is part of the plan from the start.

If your main goal is rewards, check our top crypto cashback cards.

Credit-card reality check: True crypto credit cards are rare. Gemini Credit Card is a conventional unsecured rewards credit card. Coinbase One Card is also a conventional credit card, but access depends on a paid Coinbase One membership. Nexo Card is crypto-backed credit, where spending power depends on collateral. This page covers both because users search for them together, but they are not the same structure.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

Gemini Card is the cleanest fit for users who want an actual crypto rewards credit card. Coinbase One Card can beat it on bitcoin rewards, but only for a narrow set of high-balance Coinbase users. Nexo Card is the only option in this roundup for EEA and UK users, and it only makes sense if you are already comfortable managing collateral inside a borrowing structure.

APR And Carrying-A-Balance Snapshot

Before comparing reward rates, look at the cost side. APR, repayment rules, and collateral terms decide whether a crypto reward card still works after the first billing cycle. Below is a breakdown of each card's carrying cost in plain terms.

Gemini Credit Card

- Purchase APR: 18.49% to 34.49% variable

- Cash advance APR: 29.49% variable

- Cash advance fee: $10 or 3% of each advance, whichever is greater

- Minimum payment: Full statement balance if under $25; otherwise the greater of $25 or 2.5% of statement balance, plus interest, fees, rewards charges, and any past-due or over-limit amounts

Coinbase One Card

- Purchase APR: 19.49% to 29.49% variable

- Cash advance APR: 32.24% variable

- Cash advance fee: $10 or 5% of each advance, whichever is greater

- Minimum payment: Full new balance if under $35; otherwise 1% of new balance plus billed finance charges, Coinbase One subscription fees, cash advance fees, card replacement fees, paper statement fees, rewards adjustment charges, penalty fees, and any over-limit amount

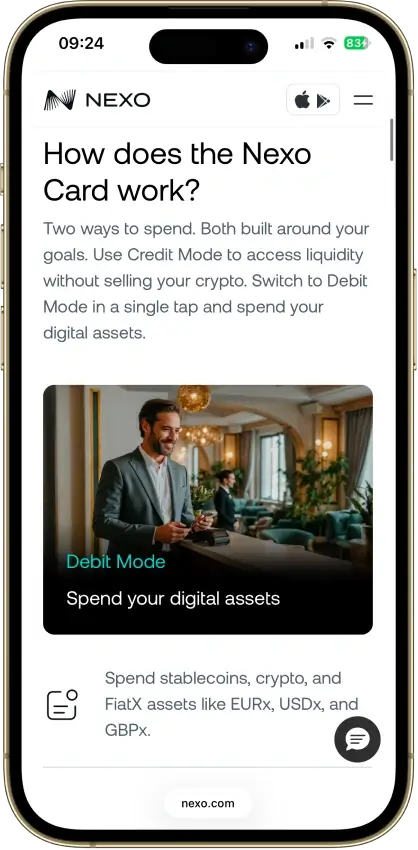

Nexo Card

- Borrowing rate: From 1.9%, based on loyalty tier and app terms

- Cash advance structure: No conventional cash advance; this is a credit line, not a revolving card

- Repayment schedule: No fixed monthly payment required; partial or full repayment can be made at any time, subject to Nexo Credit Line terms

Gemini and Coinbase One Card carry standard revolving credit risk: if you do not pay in full, the APR compounds against the balance and erases the reward value fast. At Gemini's upper APR of 34.49%, a $500 carried balance costs roughly $14 in interest per month, which wipes out the rewards on well over $1,000 in spending. Nexo shifts that risk to collateral instead of interest rate, but a sharp drop in pledged asset value can trigger a margin call that forces liquidation before you have a chance to top up.

Crypto Credit Cards Reviews

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Start with Gemini Card or Coinbase One Card if you want normal revolving credit. Look at Nexo Card only if a crypto-backed borrowing structure matches how you already manage assets.

Our Ranking Methodology

We score crypto credit cards differently from debit, prepaid, and stablecoin spending cards because credit structure changes the risk. A good card in this category must do more than pay crypto rewards. It must have a clear approval path, transparent APR or borrowing cost, usable credit terms, reliable card acceptance, and manageable tax or collateral friction.

A score of 1.0 means the card performs well for that criterion. A score of 0.5 means it is usable but has meaningful friction. A score of 0.0 means the feature is missing, unclear, paused, or too restrictive to reward.

| Criterion | Weight | What We Check |

|---|---|---|

| Credit Structure, Availability, And Setup | 1.25 | Whether the product is true unsecured credit, crypto-backed borrowing, or credit-adjacent; live status; region limits; KYC; credit approval; membership or collateral gates |

| Approval Path And Carrying Cost | 1.50 | Purchase APR, cash advance APR, grace period, minimum payment rules, credit check, borrowing rate, repayment schedule, and LTV rules |

| Rewards Value After Conditions | 1.25 | Reward rate, caps, category limits, merchant coding, membership requirements, asset-balance tiers, loyalty tiers, reward asset volatility, and clawbacks |

| Fees And Hidden Cost Drag | 1.25 | Annual fee, membership cost, foreign transaction fee, cash advance fee, ATM cost, replacement fee, spread, crypto conversion cost, and partner fees |

| Real-World Spend Reliability | 1.00 | Network acceptance, physical card availability, virtual card availability, mobile-wallet use, merchant restrictions, subscriptions, pre-authorizations, and travel use |

| Spending Source, Disposal, And Collateral Risk | 1.00 | Whether spending uses unsecured credit, sells crypto, uses stablecoins, borrows against collateral, or creates liquidation risk |

| App, Controls, And Virtual Card Tooling | 0.75 | Virtual card, card lock, alerts, reward tracking, mobile-wallet provisioning, statement access, and in-app account controls |

| Security, Issuer, Custody, And Freeze Risk | 0.75 | Issuer, servicer, custody model, account-link dependence, collateral custody, asset rehypothecation risk, account freeze risk, and unauthorized-use controls |

| Support, Refunds, And Chargebacks | 0.75 | Human support, dispute rights, refund handling, chargeback path, unauthorized-transaction handling, and reward adjustments after refunds |

| Tax And Reporting Readiness | 0.50 | Whether rewards are explained clearly, whether disposals can occur, whether statements or exports are usable, and what the user must still track manually |

Approval Path And Carrying Cost carries the highest weight at 1.50 because a card that pays 4% back and charges 30% APR on a revolving balance is a net negative for most users. Rewards Value After Conditions and Fees And Hidden Cost Drag are weighted equally at 1.25 because the two interact directly: a high reward rate attached to an expensive membership or a spread on every conversion can make a lower-rate card the better choice in practice.

What Is A Crypto Credit Card?

A crypto credit card can mean more than one product type, and that is where most of the confusion starts. Two distinct models share the label in search results, and they behave very differently once you get past the application page.

True Crypto Rewards Credit Cards

These work like normal unsecured credit cards. You make purchases on a revolving credit line, pay later, and earn rewards that settle in crypto instead of cash or points.

For users who want a credit card with crypto rewards, Gemini Card and Coinbase One Card are the clearest fits in this roundup. The main questions are the same as with any rewards card: approval odds, purchase APR, reward caps, membership cost, and whether the crypto payout is worth tracking after it lands. Both cards are U.S.-only, both require a linked exchange account, and neither lets you avoid a standard credit check. If you are already comparing crypto rewards credit cards more broadly, the same filters apply.

Crypto-Backed Credit Products

These do not give you normal unsecured consumer credit. Instead, you lock crypto as collateral and spend against a borrowing line that depends on your pledged assets.

Nexo Card fits this model. The appeal is that you may avoid selling crypto when you spend, but the cost shifts into borrowing charges, loyalty-tier conditions, lower usable credit than total portfolio value, and the need to actively manage collateral when prices fall. A user with 10,000 EUR in pledged BTC does not get 10,000 EUR in spending power; the usable credit depends on the loan-to-value ratio Nexo applies, which changes with market conditions. Users outside the U.S. who want to stay exposed to their assets while spending are the natural fit. Everyone else should weigh that collateral friction against what a plain crypto debit card would cost.

Related Card Types Worth Checking

Some users begin looking for a crypto credit card and then realize unsecured credit is not the real goal. They may want easier approval, direct stablecoin spending, or a card that works without a standard underwriting decision.

USDC spending cards, USDT spending cards, and virtual crypto cards can still help in those cases. They are different products, but they solve nearby problems for users who want crypto-linked spending without a credit application. None of them offer revolving credit or purchase APR protection, but they also carry no risk of a balance compounding against you.

How Crypto Credit Card Rewards Work

Crypto credit card rewards only look simple at the headline level. The real value depends on how the reward is paid, when it posts, what unlocks the top rate, and what you give up to keep earning it.

Several factors tend to move the result more than the headline percentage does. The list below covers the main ones to check before you commit:

- Rewards paid in crypto automatically, which makes the experience easy but starts price exposure immediately

- Spending categories that keep the best rate tied to narrow merchant types

- Spend caps that cut the effective rate once monthly volume rises

- Memberships, loyalty tiers, or asset balances that gate the best reward level

- Headline rates that look less impressive once token risk or required fees are counted

- Direct crypto rewards versus plain cashback converted later, which can change both usability and tracking

Gemini Card illustrates the cap problem clearly: the 4% rate on gas and transit cuts to 1% after $300 per month in that category, so a driver who spends $500 per month on gas earns 4% on the first $300 and 1% on the remaining $200, for a blended rate of about 2.8% on that spend. Coinbase One Card avoids a category cap but imposes an asset-balance gate instead. Neither model is cleanly superior; the better one depends on how your actual spending is distributed.

APR, Membership Costs and Where The Real Cost Shows Up

Most crypto credit cards lead with the reward rate and bury the cost layer. That cost layer matters more than the headline reward once you carry a balance, pay for access, or hold assets just to keep the rate from dropping.

Before you focus on reward rates, work through the full cost stack. Most of the real friction sits in one of these items:

- Purchase APR

- Penalty risk if the balance revolves

- Membership or subscription cost

- Foreign transaction fee

- ATM cost if relevant

- Spread or token-conversion drag

- Opportunity cost when a plain cashback card could be cheaper overall

Coinbase One Card makes this trade-off concrete. The $49.99 annual membership is a fixed cost regardless of how much you spend or earn. At 2% bitcoin back on $200 per month in spending, the card returns $4.80 in rewards monthly, or $57.60 per year — a net gain of roughly $7.61 after the membership cost. Increase the spend to $500 per month and the net gain climbs to roughly $70.61. The card only makes financial sense above a certain spending threshold, and the threshold rises further if your Coinbase balance does not unlock the 4% tier. Comparing no annual fee crypto cards and low-fee crypto cards first gives you a baseline before you decide whether the membership cost is worth it.

Approval, Credit Check, KYC and Regional Availability

Access is often the first real filter. A card can rank well on rewards and still be irrelevant if the application path is narrow, the exchange account setup is heavy, or the product is not live where you live.

These access points are worth checking before you spend time comparing reward rates:

- Soft pull versus hard pull

- Open application versus limited rollout

- KYC and exchange-account requirements

- State, country, or regional restrictions

- Real availability where you live

- Approval friction versus reward upside

The regional split in this roundup is blunt: Gemini Card and Coinbase One Card are U.S.-only, and Nexo Card covers selected EEA countries and the UK. That means a user in Germany, France, or Portugal has exactly one option from this list, and it is a collateral-backed product rather than an unsecured credit card. U.S. users in states with restricted crypto activity should also verify availability before applying, as both Gemini and Coinbase have paused or limited access in certain states at various points. For users where geography is the main blocker, crypto cards available in Europe covers a wider set of options. If approval friction matters more than region, no-KYC crypto cards are worth checking, though none of them are true credit products.

Crypto Credit Card Fees

The fee stack is where the gap between marketing and real cost shows up most clearly. Reward rates are always quoted before fees, and for two of the three cards here, the fee structure either directly reduces the net reward or introduces a cost that compounds with heavier use. Below is a breakdown for each card, followed by worked examples.

Gemini Card

- Issuance cost: No separate issuance fee

- Annual fee: None

- Membership requirement: None

- ATM and cash advance fee: $10 or 3% of each cash advance, whichever is greater; ATM transactions and cash advances do not earn rewards

- Crypto reward fee: No fee to receive crypto rewards; later sells or swaps follow Gemini's normal trading or conversion fee schedule

- Foreign transaction fee: 0%

Coinbase One Card

- Issuance cost: No added card fee with active membership

- Annual fee: Requires active paid Coinbase One membership; basic annual plan is $49.99/year; Preferred and Premium plans also qualify

- Membership requirement: Coinbase One membership required

- ATM and cash advance fee: $10 or 5% of each cash advance, whichever is greater; ATM withdrawals and other cash-like transactions are rewards-ineligible

- Crypto reward fee: Bitcoin rewards priced when credited; later sells follow normal Coinbase pricing; Coinbase One trading still has spread

- Foreign transaction fee: 0%

Nexo Card

- Issuance cost: No issuance fee publicly shown

- Annual fee: None, but Loyalty Tier affects benefits

- Membership requirement: None for card access, but tier changes what you earn

- ATM and cash advance fee: Free monthly allowance by tier, then 2% fee with a minimum of 1.99 EUR or 1.99 GBP

- Crypto reward or conversion fee: Credit Mode avoids a forced crypto sale; Debit Mode converts through Nexo Exchange

- Foreign transaction fee: 0.2% for EEA, UK, and Switzerland; 2% for rest of world; weekend FX adds 0.5%

Worked Examples

These examples use realistic monthly spending figures to show how the fee and reward structures interact. The figures are illustrative and based on published rates; individual results will vary depending on merchant coding, loyalty tier, and whether balances revolve.

Gemini Card — $1,500 monthly spend

A cardholder spends $200 on gas, $300 on dining, $200 on groceries, and $800 on general purchases. At published rates that produces roughly $8 on gas (4%), $9 on dining (3%), $4 on groceries (2%), and $8 on other spend (1%), for a total of about $29 in crypto rewards per month. No annual fee applies and the foreign transaction fee is 0%. If the balance is paid in full, the only remaining cost is any trading fee when the reward crypto is eventually sold. At Gemini's standard conversion fee the drag on a $29 reward is small but not zero. The reward also degrades in dollar terms if the received crypto falls in price before the user converts or spends it.

Coinbase One Card — $1,500 monthly spend, basic membership, balance under $200,000

At a 2% bitcoin-back rate on $1,500 monthly spend, the card returns $30 in bitcoin. The $49.99 annual Coinbase One membership costs roughly $4.17 per month, reducing the net monthly reward to about $25.83. Over a full year, gross rewards total $360 against a $49.99 membership cost, for a net of $310.01 — assuming no balance is carried, no cash advances are taken, and Coinbase's pricing on bitcoin sales does not erode the reward further. If the user carries a balance at 29.49% APR, even a small revolving amount cancels the annual reward gain within a few months.

Nexo Card — 1,000 EUR monthly spend, base loyalty tier, EEA

In Credit Mode at the base tier, the card pays up to 2% cashback, returning roughly 20 EUR on 1,000 EUR in spend. Domestic EEA transactions carry a 0.2% FX fee, adding about 2 EUR per 1,000 EUR on cross-border purchases within the region. ATM withdrawals beyond the free tier allowance cost 2% with a minimum of 1.99 EUR per transaction. A user who travels outside the EEA on a weekend faces a 2.5% FX rate (2% base plus 0.5% weekend surcharge), which turns a 2% cashback card into a net-negative on those transactions alone. Collateral risk sits outside the fee stack entirely but represents the largest variable cost for any user running a meaningful credit balance against pledged assets.

Virtual Cards, Apple Pay and Everyday Spending

Getting approved is only the first step. The card still has to work cleanly in daily use, and that is where weak mobile wallet support, delayed virtual access, or inconsistent merchant handling start to matter.

The points below are the practical ones to check before committing to any card in this category:

- Instant virtual card, or wait for the physical card

- Apple Pay and Google Pay support

- Smooth online checkout and subscription billing

- Reliable recurring-bill handling

- Better acceptance for travel, hotels, and foreign merchants

- Less friction on holds, reversals, and refunds

- App controls for freeze, unfreeze, and spend alerts

Network matters here beyond just acceptance rates. Coinbase One Card runs on the American Express network, which has lower merchant acceptance than Visa or Mastercard in some international markets and at smaller retailers. Gemini Card runs on Mastercard. Nexo Card also runs on Mastercard. If travel or international spend is part of your use case, the Amex network on Coinbase One Card is worth factoring in before you apply. For users where mobile-first use is the priority, crypto cards with Apple Pay and Google Pay covers a wider comparison. For travel-specific use, international crypto cards is the more relevant starting point.

Credit Limits, Payments and Account Management

Daily spend is only part of the experience. The account side decides whether the card stays usable after the first statement, especially if you rely on it often or carry a low starting limit.

Account details worth checking before you commit include the following:

- Credit limits in real approvals, not just marketing examples

- How fast available credit refreshes after payment

- Autopay support and billing controls

- Clear statement dates, due dates, and category tracking

- Reward posting speed after purchase or statement close

- Refund timing and credit restoration

Credit limit transparency is a consistent gap across this category. None of the three cards publish typical starting limits, and actual approvals vary significantly based on credit profile. A low starting limit on a card with a 3% to 4% category reward creates a practical ceiling on monthly reward earnings regardless of what you actually spend. For Coinbase One Card, that ceiling interacts with the $10,000 monthly spend cap on the boosted rate: a user approved for a $2,000 limit never reaches the threshold where the cap becomes relevant, but they also never fully stress-tests the card's reward structure.

Taxes, Reporting and Selling Friction

Crypto rewards are easy to like when they hit the account. Tracking them later is where the friction starts, especially once rewards are sold, swapped, or mixed with other crypto activity.

Tax and reporting points that tend to change the experience the most include the following:

- Whether rewards are usually treated more like cashback or like income

- Cost basis once reward crypto is sold or swapped

- Whether spending crypto creates a taxable sale

- Whether paying a bill with crypto can create a taxable event

- Statement and CSV quality

- What tax software still gets wrong

- Which setups are easier to track in real use

The tax treatment of crypto rewards is not settled uniformly across jurisdictions. In the U.S., rewards on credit cards are generally treated as rebates rather than income at receipt, but the IRS has not issued definitive guidance specific to crypto rewards, and the cost basis clock starts when the reward lands. Every subsequent sale or swap of that reward crypto is a separate taxable event. Nexo Card in Credit Mode introduces a different question: if you are borrowing against collateral and the collateral is liquidated, the tax treatment of that forced sale depends on how the liquidation is classified in your country. Both Gemini and Coinbase provide transaction history exports, but neither produces a ready-to-file tax report — users with high reward volume or frequent conversions will still need dedicated crypto tax software to reconcile accurately.

Common Crypto Credit Card Problems and Fixes

Most problems with cards in this category come from the gap between marketing messages and how the card behaves once merchant coding, issuer policy, and platform rules all interact. Knowing which layer caused the problem makes the fix faster.

Common issues and the usual fix:

- Card declined at an exchange or wallet-like merchant: use ACH, debit, or bank transfer instead — many issuers treat these payments as restricted or cash-like.

- Reward category did not track as expected: check the posted merchant category code before assuming the rate was missed.

- Membership or token lock wiped out the reward edge: rework the math on net value, not the headline rate.

- Available credit has not updated after payment: wait for full posting, then contact issuer support if the hold lingers.

- Virtual card works online but not in a mobile wallet: re-add the card, update the app, and check whether wallet support is live for that product and region.

- Refund took longer than expected: leave spare limit for travel, fuel, and other transactions that use holds or slow reversals.

- Reward posted late or at a different rate: check exclusions, caps, and statement timing before opening a case.

- Bank blocks direct crypto purchases on a normal credit card: use a linked bank transfer or debit route instead.

Merchant category coding causes more reward misses than most users expect. A gas station that also sells groceries may code as a general merchandise merchant rather than fuel, which drops the Gemini Card rate from 4% to 1% on that transaction with no warning. Checking the merchant category code on the posted transaction, not the pending one, is the only reliable way to confirm whether the expected rate applied.

How To Choose The Right Crypto Credit Card

The right card is usually the one that stays useful after approval, billing, and tracking are counted. A product with a lower headline reward can still be the better fit if the structure is cleaner and the ongoing friction is lower.

Work through these questions in order before you apply:

- Check whether it is a true credit card, a crypto-backed credit product, or a debit/prepaid workaround.

- Check whether the reward is simple or tied to membership, holdings, or token exposure.

- Check APR, membership cost, FX fees, and other drag before focusing on headline rewards.

- Check approval friction, KYC burden, and region availability.

- Check whether virtual-card access and mobile-wallet support fit daily use.

- Check protections, dispute handling, and who actually services the card.

- Check tax and reporting friction before making it your main spending card.

- Check whether a debit, stablecoin, or no-annual-fee alternative fits better.

For most U.S. users who want a true crypto rewards credit card with no conditions attached, Gemini Card is the default choice in 2026. Coinbase One Card makes sense only if the membership is already paid and the asset balance is high enough to move the reward rate. Nexo Card is not a substitute for either — it is a different product that fits a different need, and treating it as a like-for-like alternative will produce the wrong result.