A good UK crypto card needs more than broad card acceptance. The GBP funding path has to work cleanly, and cash-out should not require extra steps every time you move money back to your bank.

The shortlist below splits into a few clear groups. Some behave like familiar crypto debit cards tied to a cash or exchange balance, while others suit stablecoin users who care more about virtual-card speed and mobile-wallet support. One card in the list runs on a different model entirely, letting you spend against posted crypto collateral instead of selling first.

The cards covered here all suit different money paths. Some work better for GBP spending, some fit stablecoin balances, and one is built around collateral-backed credit. None of them forces the same approach on every user.

Top Crypto Cards in the UK

- Fast virtual card access

- Broad stablecoin and crypto funding support

- Strong travel and cross-border utility

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Up to 10% Tiered Cashback – Competitive top-end rewards for high spenders and VIP users.

- Fiat-First Spend Logic – Uses fiat balance first, auto-converts selected crypto only if needed.

- Transparent Fee Structure (EEA program) – FX (0.5%) and crypto conversion (0.9%) fees are clearly disclosed rather than hidden in spreads.

Each card in this shortlist gives a UK user at least one clear advantage over the alternatives. For a wider shortlist, compare them with Europe-friendly card options.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card |

Card type is the most useful filter here, because it shapes everything downstream: how funding moves in, what the card does at the moment of payment, and what record gets created for tax purposes. A debit card tied to a fiat balance, a stablecoin-funded card, and a collateral-backed credit product all behave differently in practice, and that gap shows up fast once you try to move money in or out under real conditions.

Foreign transaction fees follow the same pattern: a card that publishes 0% on FX is genuinely cheaper for travel than one charging 1% or more, and the gap compounds quickly across a single holiday. Apple Pay and Google Pay support is the last quiet differentiator, since a card without phone-wallet access is harder to use at UK contactless terminals and most online checkouts.

For most UK users comparing options, Uphold is the easiest fit for GBP-first spending because the rewards currency, foreign transaction rate, and phone-wallet support all line up around everyday UK use. KAST and RedotPay suit stablecoin balances better, with KAST offering the cleaner rewards setup of the two and both supporting Apple Pay and Google Pay. Nexo is the most flexible card in this shortlist thanks to its switch between debit spend and crypto-backed credit, plus the lowest weekday FX rate in the group. Coinbase works best for those already running their crypto through Coinbase, though the lack of Apple Pay and Google Pay support in the UK is a real limitation that the other four cards do not share.

Crypto Cards in the UK Reviews

Kast Card

Pros

- Virtual card is ready within minutes of approval, with no shipping wait required

- Apple Pay and Google Pay are supported from the start, so you can spend before the physical card arrives

- Stablecoin deposits (USDT, USDC, USDe, PYUSD, RLUSD) convert to USD at 1:1 with no spread

- The Standard tier costs nothing to open, which keeps the entry bar low for first-time users

- Visa acceptance and physical card delivery cover 170+ countries, which is a wider reach than most crypto cards offer

Cons

- Deposited crypto is treated as sold to KAST on entry, with no self-custody option inside the card flow

- Full KYC and partner approval can block or delay access, even for users in supported countries

- Non-USD spend adds a 0.5% to 1.75% FX fee on top of every transaction

- ATM withdrawals require the physical card, cost $3 plus 2% per transaction, and are capped at $750 per day

- Premium tiers start at $1,000 per year, which is hard to justify unless you spend a very high volume and want KAST Points and token rewards rather than cash

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

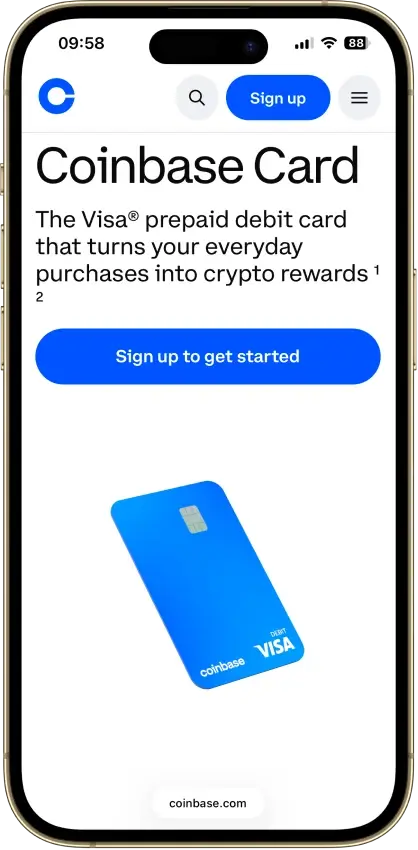

Coinbase Card

Pros

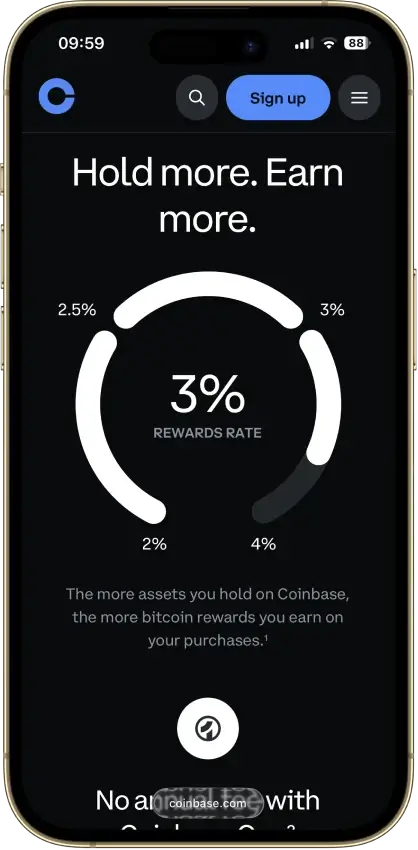

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

Bybit Card

Pros

- Up to 10% tiered cashback in Rewards Points.

- No annual, inactivity, or card cancellation fee

- Fiat-first spending can avoid crypto conversion fees.

- Strong card controls (freeze, limits, toggles).

Cons

- Limited country availability (no U.S.).

- 0.9% crypto conversion fee (EEA program).

- 0.5% FX on cross-currency spend (EEA program).

- Rewards are tier-based and capped monthly.

How We Ranked Crypto Cards In The UK

The UK ranking uses a 10-point weighted score. Each card is scored only on what a UK user can realistically use, not the strongest version advertised in another country.

Each criterion gets a raw score of 0, 0.5, or 1. The raw score is then multiplied by the weighting below. The final score is the total of all weighted points.

| Criterion | Weight | What We Measured For UK Cards |

|---|---|---|

| Availability And Setup Friction | 1.0 | UK eligibility, KYC, source-of-funds risk, card ordering, virtual-card access, physical-card access, and whether a new eligible user can actually get started |

| Funding Rails And Conversion Path | 1.25 | GBP deposits, Faster Payments support, stablecoin deposits, supported spend assets, conversion timing, and whether money can move back out cleanly |

| Real-World Spend Reliability | 1.5 | In-store use, online use, physical card support, virtual-card use, Apple Pay / Google Pay, ATM access, travel use, prepaid quirks, merchant restrictions, and pre-authorisation friction |

| Rewards Value After UK Conditions | 1.0 | UK-available cashback, points, caps, excluded spend, paid tiers, staking or token requirements, reward currency, and whether US-only rewards have leaked into UK copy |

| Fees And Hidden Cost Drag | 1.25 | Annual fees, issuance fees, physical-card costs, FX fees, ATM fees, top-up costs, withdrawal costs, conversion spreads, payout fees, and tier costs |

| Operational Convenience And Limits | 0.75 | Funding-to-spend timing, card issuance speed, spend limits, ATM limits, withdrawal timing, refund timing, holds, and cash access |

| App, Controls, And Virtual Card Tooling | 0.75 | Virtual cards, card freeze/unfreeze, PIN controls, alerts, balance controls, Apple Pay / Google Pay, transaction history, and export basics |

| Security, Custody, And Freeze Risk | 1.25 | Custody model, issuer clarity, regulatory setup, account security, proof-of-funds risk, compliance holds, and escalation risk |

| Support, Refunds, And Chargebacks | 0.75 | Human support, dispute route, refund handling, unauthorised-transaction path, help-center quality, and complaint escalation |

| Tax And Reporting Readiness | 0.5 | Whether card spend can create HMRC disposal records, how easy it is to separate GBP spend from crypto-funded spend, and whether transaction exports are usable |

A 1.0 raw score means the card performs well for that criterion in the UK. A 0.5 means it is usable but has meaningful limits, conditions, or missing public detail. A 0 means the feature is unavailable, too unclear, or not useful enough to count.

Best Crypto Cards In The UK By User Type

The same card will not suit every UK user. The better pick depends on whether your working balance starts in GBP, stablecoins, or long-term crypto you do not want to sell.

| User Type | Best Pick |

|---|---|

| Fiat-first UK spender | Uphold Card |

| Stablecoin-first spender | KAST Card |

| Cashback-first UK user | Uphold Card |

| User who wants to spend without selling | Nexo Card |

| Traveler who cares about FX | Uphold Card |

| User who wants the least setup friction | Coinbase Visa Debit Card |

Use this section to match the shortlist to your actual money flow. Those who care mostly about rewards should also compare the top crypto rewards cards before deciding.

GBP Funding and Withdrawal Reality

GBP support is not the same as GBP-first usability. The table below separates cleaner bank-transfer paths from stablecoin-first flows where GBP is mainly a payout or currency-account feature.

| Card | GBP Path Summary |

|---|---|

| KAST Card | Not a GBP-first card; fund mainly with stablecoins or USD bank transfer where available. Stablecoin deposits convert to USD inside KAST; exact timing depends on network and review. Stablecoin-to-USD shown at 0% spread; non-stablecoin and payout fees can apply. GBP Local Payout to bank account, with a 1% FX conversion fee plus a $3 transfer fee. |

| Nexo Card | GBP bank transfer to GBPx/FIATx balance; card can also spend stablecoins or crypto. Faster Payments-supported for GBP transfers; exact availability and holds vary by account. Public fee detail is not clear enough to publish a fixed GBP transfer fee; confirm in app. Cash-out or bank transfer from Nexo balance where available, with fees not verified clearly in public help. |

| Coinbase Visa Debit Card | GBP balance funding through linked UK bank account / Faster Payments. FPS-supported; linked-bank funds may not be spendable immediately. No Coinbase card spending fee; add-cash fees, if any, are shown in preview. Withdraw GBP balance to UK bank account via Faster Payments; cash-out fees can vary by method and are shown in preview. |

For UK users, the cleaner setup is a card that lets pounds go in and out without forcing extra asset conversions. Stablecoin-first cards can still work, but the payout and conversion path matters more than the headline card fee.

How To Choose The Right Crypto Card In The UK

The right choice usually becomes clear once you check the full money path: how funds get in, what gets converted at checkout, and how cash-out works.

Run through these checks before committing to any UK crypto debit card or credit card:

- Decide whether you want to spend GBP, spend stablecoins, or borrow against crypto.

- Check whether the card rewards still hold up in the UK.

- Test how easy it is to fund the card in GBP and move money back out.

- Confirm whether the card sells crypto every time you tap it.

- Compare the real FX and ATM cost, not just the annual fee.

- Verify how fast the virtual card works and whether Apple Pay or Google Pay is supported.

- Check whether the card is usable for travel, refunds, and merchant categories you actually spend in.

- Confirm whether the reporting is good enough for UK tax records.

If low day-to-day cost is the main priority, compare low-fee cards before locking in.

Crypto Debit Cards Vs Crypto Credit Cards In The UK

In the UK, most crypto cards work like debit or prepaid products rather than consumer credit cards. You spend from a loaded balance, a fiat wallet, or a crypto balance that gets converted at checkout, with the card behaving more like a payment rail on top of an existing account than a borrowing facility.

Only a smaller group lets you borrow against posted crypto collateral instead. Even those products are structured around loan terms rather than the revolving credit model UK users get from a high-street bank. The distinction matters because it changes what protections, rewards, and tax records apply once you start spending.

A few practical differences shape which model works for which user:

- Most UK options are balance-led cards, so the money usually comes from preloaded fiat, stablecoins, or crypto converted at checkout

- Debit or prepaid models fit better when you want spending capped to available funds and fewer surprises after each purchase

- Collateral-backed credit fits better when you want liquidity without selling long-term holdings, though it adds borrowing cost and liquidation risk

- If the card sells crypto when you tap, each payment can create disposal records; if it lends against collateral, the admin shifts toward loan use, interest, and repayment tracking

- Normal credit-card expectations around protections, billing, rewards, and repayment do not carry over cleanly

For many UK users, debit-style crypto cards are the cleaner fit because budgeting stays simpler, the funding source is visible at all times. Tax records are also easier to manage without collateral risk sitting underneath everyday spending. Collateral-backed cards still have a place for holders who want to spend without selling, but they shift the work from cashback tracking to loan tracking, which most casual users underestimate at signup.

Who Should Skip Crypto Cards In The UK

Some UK users are better off ruling crypto cards out early, especially when the real goal is strong consumer protection and clean records rather than spending crypto.

The profile below describes users who tend to regret picking up a crypto card:

- Users who mainly want Section 75 protection and the familiar rules of a normal UK credit card

- Users who want cashback without also tracking disposals, exclusions, or platform-specific reward conditions

- Users who mostly pay rent, tax, utility bills, or other categories that often do not earn rewards or can trigger declines

- Users who want one clean GBP statement without crypto conversions, token rewards, or multiple balance types mixed in

- Users who do not want later source-of-funds checks, compliance reviews, or requests for extra documents

For those users, a standard UK payment card is usually the better fit. Section 75 protections are clearer. The dispute process is faster. The compliance path is less likely to create surprises later, especially when a larger transaction triggers a source-of-funds review. A crypto card can still sit alongside a normal card for specific use cases like travel or stablecoin payouts. It rarely makes sense as the main everyday card for users in this group.

HMRC Reporting Friction

Crypto card spending can create tax records even when the card feels like a normal debit card. HMRC treats using tokens to pay for goods or services as a disposal, so a card payment funded by crypto or stablecoins can require gain and loss tracking.

For the 2025/26 tax year, the annual Capital Gains Tax exemption for individuals is £3,000. That does not mean small card payments can be ignored. Frequent taps can still create a long transaction trail if the card sells tokens at checkout.

A few practical habits keep the paperwork lighter:

- Spend from GBP cash when the card supports it.

- Keep exports for card spend, funding source, conversion value in GBP, fees, cashback, and withdrawals.

- Avoid using crypto-funded card taps for dozens of small daily purchases unless you are ready to reconcile them.

- Treat cashback paid in crypto or points separately from the card purchase record.

If HMRC reporting matters more than rewards, favor GBP-funded spending over crypto-funded spending. The reward gap is usually smaller than the bookkeeping gap.

KYC, Source-Of-Funds Checks and Limits

Verification usually feels simple at signup. The friction tends to appear later, when limits, withdrawals, or higher-value transactions prompt extra document requests. It is worth checking not just whether ID is required, but what documents can appear later and where spending or payout friction tends to show up.

| Card | KYC and Friction Profile |

|---|---|

| Uphold Card | ID verification and selfie before full card use. Payment-method reviews and extra verification can affect access or limits. Limits vary by verification level, payment method, and region. Cleaner once approved, but still a full-KYC product rather than a light-onboarding card. |

| KAST Card | Level 2 verification is required to create virtual or physical cards. Proof of funds, proof of address, and source-of-funds documents can be requested. Large transactions can trigger compliance review even without preset spend caps. Better suits users comfortable with a document-heavy stablecoin setup. |

| Nexo Card | Full identity verification is required before products unlock. Regulatory profile, source of funds, source of crypto, and wealth checks can appear. Account access and some limits depend on verification depth and risk review. Strong fit for users already willing to complete full-platform verification. |

| Coinbase Visa Debit Card | Identity and address verification are required for card approval. Further verification may be needed for higher account limits or certain payment methods. Risk checks can reduce limits, and linked-bank funds may not be spendable right away. Easiest when Coinbase is already your main verified account. |

| RedotPay | ID document and face verification are required before use. Address checks, source-of-funds review, and added documents can be requested. Region mismatches, document issues, or security reviews can slow access or reduce limits. Works better when you expect full compliance checks rather than fast anonymous spend. |

Treat this table as a guide to where friction tends to appear, not just what ID is needed at signup.

Virtual Cards, Apple Pay, Google Pay and ATM Use

Virtual card availability, phone-wallet support, and ATM access change day-to-day convenience more than many users expect. A card that works well online may still be weak at ATMs, and a strong physical card matters less if most spending already happens through a phone wallet. For users who spend mostly online, the virtual cards shortlist is worth a look, and those who lean on phone wallets should browse crypto cards with Apple Pay and Google Pay.

| Card | Virtual, Wallet, ATM, and Best Use |

|---|---|

| Uphold Card | In-app virtual card. Apple Pay and Google Pay both supported. Physical card available. ATM access with physical card. Best for GBP spending and travel. |

| KAST Card | Instant virtual card. Apple Pay and Google Pay both supported. Physical card available. ATM access with physical card only. Best for stablecoin-funded online and phone-wallet spend. |

| Nexo Card | Virtual card available before physical card. Apple Pay and Google Pay both supported. Physical card available. ATM access with tier-based allowance. Best for borrow-against-crypto spend with mobile wallet support. |

| Coinbase Visa Debit Card | Virtual card available right away in app. Apple Pay and Google Pay not supported in UK. Physical card available. ATM access with physical card and PIN. Best for Coinbase-native spend with simple online setup. |

| RedotPay | Virtual card available. Apple Pay and Google Pay both supported. Physical card available. ATM access with physical card only. Best for borderless stablecoin spend and online payments. |

Common UK Crypto Card Problems And Fixes

Most crypto card problems do not start at signup. They usually show up a few transactions in, when rewards fail to post or cash-out takes longer than expected.

The list below covers the issues UK users hit most often:

- Cashback missing: Check excluded merchant categories before assuming the rate applies everywhere.

- Cashback reversed later: Some merchants can trigger a clawback even when the reward first appears.

- GBP spend is fine but travel spend is weak: Look at the FX treatment, not just the local spend pitch.

- Virtual card works but phone wallet does not: Card issuance and Apple Pay or Google Pay support do not always go live at the same time.

- Top-up is easy but cash-out is slow: The inbound and outbound rails are often unequal in quality.

- Crypto-funded spend creates tax admin: Small daily taps can still create a long record-keeping trail.

- Big purchase gets blocked or reviewed: Source-of-funds checks often show up after the card starts being used.

- Refunds take longer than expected: Card refunds usually move more slowly than wallet transfers.

- HMRC or bill payment does not earn rewards: Government-style or bill-like merchant categories can behave differently.

Most of these problems are easier to avoid than to fix. Test the card with smaller transactions first before relying on it for everyday UK spending. Keep at least one normal UK debit or credit card available for the categories where crypto cards tend to fail. That covers bill payments, government charges, and large one-off purchases that might trigger a compliance review.