Virtual crypto cards are faster to access than physical ones, but that speed only matters when the card actually works at checkout. The best options hand over usable card details within minutes of approval, covering online payments, subscriptions, mobile wallets, and everyday spending without the wait for plastic in the post.

The real test comes after sign-up. Region locks can block access entirely, KYC queues can stretch verification from minutes into days, merchant acceptance is uneven across issuers, wallet support varies by country, and refunds on crypto-funded cards can sit in limbo longer than expected. The cards that hold up are the ones that work through all of that, not just the first checkout.

Top Virtual Crypto Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Up to 10% Tiered Cashback – Competitive top-end rewards for high spenders and VIP users.

- Fiat-First Spend Logic – Uses fiat balance first, auto-converts selected crypto only if needed.

- Transparent Fee Structure (EEA program) – FX (0.5%) and crypto conversion (0.9%) fees are clearly disclosed rather than hidden in spreads.

- Up to 8% Cryptoback rewards (tier-based, paid in WXT)

- $0 annual fee + 0% marketed FX fees on card spending

- Multicurrency spending from fiat, stablecoins, and crypto in one app

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card |

| | Visa, Mastercard | Debit | Apple Pay, Google Pay | Available in UK and many countries (incl. parts of EEA, AU, NZ, HK, TW), while not available in USA, Canada, China, Japan, South Korea, Philippines, Russia (among others); EEA Mastercard eligibility requires EEA residency excluding Cyprus & Liechtenstein. |

The top crypto cards above cover different use cases. Rewards cards and stablecoin spend cards behave differently in practice, and regional fit usually determines whether the card is even an option. For frequent online spend, wallet support and regional availability tend to matter more than headline perks. For stablecoin-heavy use, clean USDC or USDT handling becomes the priority because extra conversion steps add friction quickly. When fast access is the goal, KYC is the first variable to check.

Virtual Crypto Cards Reviews

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

Nexo Card

Pros

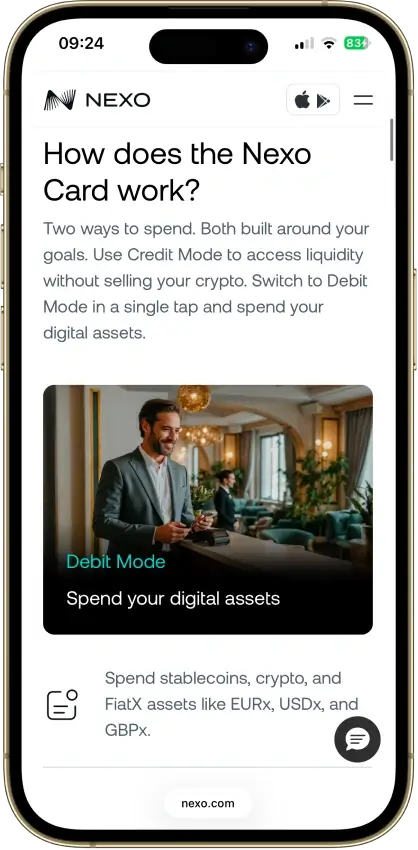

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

Bybit Card

Pros

- Up to 10% tiered cashback in Rewards Points.

- No annual, inactivity, or card cancellation fee

- Fiat-first spending can avoid crypto conversion fees.

- Strong card controls (freeze, limits, toggles).

Cons

- Limited country availability (no U.S.).

- 0.9% crypto conversion fee (EEA program).

- 0.5% FX on cross-currency spend (EEA program).

- Rewards are tier-based and capped monthly.

Wirex Card

Pros

- Up to 8% rewards at higher X-tras tiers

- No annual fee

- Strong in-app controls

Cons

- Not available in US

- Rewards paid in WXT

- ATM fees after free limit

The Best Virtual Crypto Card Depends On How You Spend

The right pick shifts once rewards cards and true crypto-spend cards are separated. How the card fits the payment habit usually tells more than brand recognition or headline perks. Each of the options below suits a specific profile, and the gap between a good match and a poor one usually shows up in the funding step or the refund flow, not at checkout.

| User Type | Card |

|---|---|

| U.S. user who wants credit-card recurring billing and crypto rewards | Gemini Credit Card |

| Stablecoin user who wants fast virtual Visa access before physical delivery | KAST Card |

| EEA or UK user who wants virtual debit or credit-mode spending | Nexo Card |

| U.S. Coinbase user who wants USD or USDC-funded debit spend | Coinbase Card |

| Supported-country user who keeps spending funds in a Bybit Funding Account | Bybit Card |

| Existing Wirex user who wants separate virtual and physical card numbers | Wirex Card |

A strong match depends on what happens before and after checkout, not just at the moment of payment. Funding rails, hot wallet compatibility, region rules, and refund handling often shape the real experience more than the headline feature list.

The Best Virtual Crypto Card Depends On How You Spend

The right pick changes once rewards cards and true crypto-spend cards are separated. Looking at how the card fits the payment habit usually tells more than brand size or headline perks.

| User Type | Card |

|---|---|

| U.S. user who wants crypto rewards from online spend | Gemini Credit Card |

| EEA or UK user who wants virtual stablecoin spending first | Nexo Card |

| U.S. user who wants clean USDC wallet spending from an exchange balance | Coinbase Card |

| Supported-country user who keeps most spending funds in USDT | Bybit Card |

| User who needs broader country coverage and app-first card access | Wirex Card |

A strong match depends on what happens before and after checkout, not just at the moment of payment. Funding, wallet support, region rules, and refund handling often shape the real experience more than the headline feature list.

How We Ranked The Best Virtual Crypto Cards

We ranked virtual crypto cards by how well they work before a physical card enters the picture. A card scored higher if an eligible user can pass setup, see usable card details, fund the account clearly, make a first online payment quickly, keep subscriptions running, and recover cleanly from refunds or failed payments.

| Criterion | Weight | What We Measured |

|---|---|---|

| Virtual Availability And Setup Friction | 1.25 | Whether the virtual card is live for new users, who can apply, KYC/credit checks, country restrictions, and whether setup is realistic for an eligible user. |

| Time To First Payment And Physical-Card Independence | 1.25 | How quickly card details appear, whether the first payment can happen before physical delivery, and whether online spend works without the physical card. |

| Funding Rails And Conversion Path | 1.10 | Supported funding assets, stablecoin support, fiat funding, conversion timing, network limitations, and whether the spend balance is easy to understand. |

| Online Checkout And Subscription Reliability | 1.20 | Browser checkout, card-not-present payments, recurring billing, 3DS behavior, failed renewals, merchant restrictions, and prepaid-card quirks. |

| Wallet Support And Virtual-Card Controls | 0.90 | Apple Pay, Google Pay, Samsung Pay where relevant, freeze/unfreeze, card details, alerts, spending controls, and virtual-card management. |

| Refunds, Holds, And Chargeback Path | 0.85 | Refund destination, pending authorization behavior, failed payment holds, dispute process, chargeback timing, and escalation path. |

| Fees And Hidden Cost Drag | 1.00 | Issuance, monthly/annual fees, FX, crypto conversion spread, stablecoin deposit cost, decline fees, replacement fees, ATM fees, and partner costs. |

| Region Fit And Program Stability | 0.90 | Country coverage, excluded markets, region-specific wallet support, issuer changes, card pauses, and whether the card is open to new users. |

| Rewards Value After Conditions | 0.75 | Reward rates after caps, tiers, token exposure, staking/subscription requirements, merchant exclusions, and reward volatility. |

| Security, Custody, Freeze Risk, And Reporting Readiness | 0.80 | Custody model, account restriction risk, issuer dependence, fraud controls, statement/export quality, and tax-reporting clarity. |

We did not penalize every card for using a different model. A crypto rewards credit card was judged as a credit card. A prepaid or stablecoin-funded card was judged on funding clarity, balance controls, and conversion costs. A dual-mode card was judged on whether a normal user can understand which mode is being used at checkout.

For this page, payment readiness counted more than broad crypto-card benefits. Cards that need a physical card to feel complete, have unclear subscription behavior, hide the funding path, or make refunds hard to track ranked lower even if their headline rewards looked stronger.

Virtual Card Availability And Time To First Payment

Virtual access is the first real filter in this category. Some cards hand over usable details almost immediately, while others still put approval steps, region checks, or wallet limits between signup and the first payment.

| Card | Availability and Time To First Payment |

|---|---|

| Gemini Credit Card | Instant virtual card. Same day after approval. Watch for credit decision delays or extra virtual-card verification. |

| KAST Card | Instant virtual card. Minutes after eligible KYC and card setup where supported. Watch for country eligibility, KYC review, and unsupported funding routes. |

| Nexo Card | Instant virtual card. Same day after virtual activation. Watch for eligibility checks, verification, selected card mode, and available balance or credit line. |

| Coinbase Card | Instant virtual card. Immediately once the card account is created. Watch for address review, identity review, and pending holds reducing available funds. |

| Bybit Card | Instant virtual card in active programs. Same day after card approval where online payments are enabled. Watch for regional issuer review, 3DS issues, and program-specific wallet support. |

| Wirex Card | Instant virtual card. Immediately once issued in the app and funded. Watch for jurisdiction checks, identity review, and minimum funds required to order. |

The smoother options reach a usable card on the same day. Once regional rollout, extra review, or wallet limits enter the picture, the virtual advantage starts to shrink.

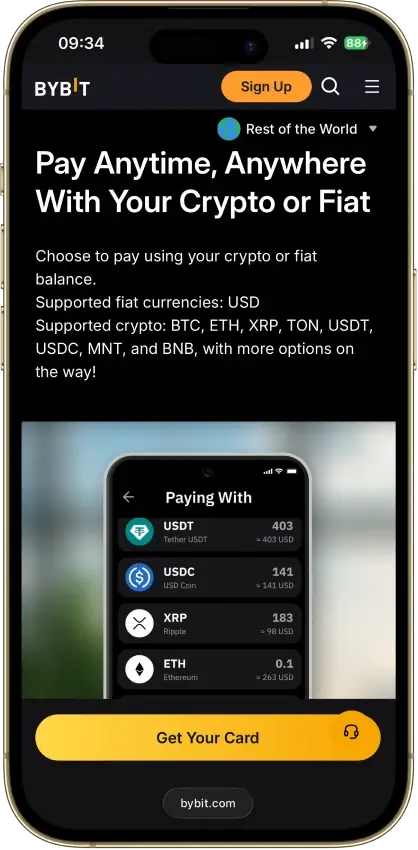

USDC And USDT Support

Stablecoin support shapes how quickly funds turn into usable card balance. On a virtual card, that can matter more than rewards.

Most cards do not spend directly from a self-custodial wallet. USDC or USDT usually lands in an app balance first, then converts either when funds arrive or when the card is charged. Chain support still comes into play, because a crypto wallet linked to a card may support the coin name but only on certain networks, which affects fees, speed, and whether funding feels straightforward or frustrating.

Stablecoin support alone is not enough to make a card work well for stablecoin spending. The cleaner options let funds arrive on a supported network, convert clearly, and become spendable without extra swaps or hidden steps.

Apple Pay And Google Pay Support

Wallet support becomes most useful when the virtual card needs to work beyond manual card entry. It improves mobile checkout and, in some cases, makes the card usable in stores before any physical card arrives.

A few consistent patterns show up across the cards in this category. Apple Pay support tends to be narrower than Google Pay. Google Pay coverage is wider in some markets but still not universal. Support often changes by country, and a live card does not always mean a live wallet integration. Some cards treat wallet support as part of the core experience. Others offer it as an add-on that works only in certain regions, on certain tiers, or on specific operating systems.

Wallet support can be the deciding factor when phone-first checkout or tap-to-pay is part of daily use. When most spending happens through saved card details at online checkout, wallet support is useful but less decisive.

Online Shopping And Subscription Use

Fast issuance only matters if normal card-not-present payments keep working. A virtual crypto card should handle checkout, billing address checks, merchant verification, pre-authorizations, and payment retries without forcing the user into a support conversation for every small issue.

Among the cards here, Gemini behaves most like a standard U.S. credit card for recurring billing. KAST has explicit subscription support, but failed renewals can trigger a declined-transaction fee if the balance is short. Coinbase works best for U.S. users spending USD or USDC from a funded balance. Nexo depends on whether the account is in Debit Mode or Credit Mode. Bybit and Wirex can work for subscriptions, but regional rules, frozen authorizations, card-number changes, and reissues all need closer tracking.

Refunds are the second test. Some refunds return to the card or app balance after the merchant and card network process them, while chargebacks can take far longer. For virtual cards, a delayed refund or frozen authorization can cut into the balance needed for the next online payment, which makes this more than a cosmetic concern.

Subscription Renewal And Recurring Billing Reality

Recurring billing is one of the strongest virtual-card tests because the charge happens when the user is not actively watching the app. A card that clears one checkout can still fail on renewal if the balance, card number, issuer region, 3DS behaviour, or card status changes between billing cycles.

| Card | What To Know |

|---|---|

| Gemini Credit Card | High fit for eligible U.S. users. Watch for credit limit, fraud review, expired card, and returned-purchase reward adjustments. |

| KAST Card | High fit where KAST is supported. Watch for insufficient balance, declined-transaction fee, and country or compliance restrictions. |

| Coinbase Card | Medium-high fit for U.S. USD or USDC funding. Watch for pending holds, wrong funding asset, locked card, and replacement card details. |

| Nexo Card | Medium-high fit for eligible EEA and UK users. Watch for Debit/Credit Mode mismatch, insufficient balance or credit line, and verification review. |

| Bybit Card | Medium fit. Watch for regional program rules, 3DS issues, frozen authorizations, and card review. |

| Wirex Card | Medium fit. Watch for new card number or expiry after reissue, subscription details not updated, and account review. |

For many virtual crypto card users, this matters more than mobile wallet setup. The better card is often the one that keeps SaaS tools, streaming apps, cloud services, app stores, and memberships renewing without a support ticket.

KYC And Account Verification

Most virtual crypto cards still require real identity verification. Even when signup feels quick, the provider usually needs enough identity data to issue the card, approve funding, and keep the account within its own compliance rules.

A faster onboarding flow does not always mean an easier support experience later. Some providers ask fewer questions at the start, then ask for more once spending increases, deposits get larger, or activity starts to look unusual. The table below covers the KYC posture and account risk profile for each card.

| Card | Details |

|---|---|

| Gemini Credit Card | Full KYC + credit check. Source-of-funds checks possible on flagged activity. Moderate freeze risk. Support via Help Center, request form, and 24/7 card phone. |

| Nexo Card | Full KYC. Source-of-funds checks can trigger on wealth review. Moderate freeze risk. Support via 24/7 live chat, ticket, and email. |

| Coinbase Card | Full KYC. Source-of-funds checks can trigger on account review. Moderate freeze risk. Support via in-app card support, chat, and phone. |

| Bybit Card | Full KYC + extra due diligence. Source-of-funds checks common on flagged transactions. Higher freeze risk. Support via support hub, case ticket, and 24/7 support. |

| Wirex Card | Full KYC. Source-of-funds and source-of-wealth checks can trigger. Moderate freeze risk. Support via live chat and request form. |

Source-of-funds checks often appear after the easy part of onboarding is done. They can surface when a user tops up more than usual, moves funds from a different wallet, changes countries, or triggers a pattern the provider wants explained. When access is frozen, the real issue is rarely the pause itself. The bigger problem is how clearly the reason is explained, how much evidence is requested, and how quickly normal access returns.

Privacy and dispute resolution often pull in opposite directions. The less information a provider collects upfront, the harder it can be to sort out a problem, unlock an account, or prove ownership later. The risk is real, but manageable when the provider is transparent, support is reachable, and the funding trail is easy to explain.

Virtual Crypto Card Fees

Virtual cards can look cheap at first because the visible charges are small. The full cost typically shows up later, once funding, conversion, FX, failed payments, and refund timing all enter the picture.

Here is what the fee picture looks like across each card:

- Gemini Credit Card

- No issuance fee

- No monthly fee

- No FX charge on purchases

- No top-up cost

- Conversion does not apply in the traditional sense since this is a credit card backed by USD

- Nexo Card

- No issuance fee for the virtual card

- No monthly fee

- FX charges range from 0.2% to 2.5% depending on the transaction

- SEPA transfers under EUR 100 carry a EUR 5 fee

- Conversion spread is not publicly disclosed as a single rate

- Coinbase Card

- No issuance or monthly fee

- USD and USDC transactions carry 0% conversion cost

- Other crypto assets are sold at Coinbase's spread at the time of the transaction

- Bank funding is free

- FX is not separately disclosed

- Bybit Card

- No issuance or monthly fee for the virtual card

- Conversion spread runs between 0.5% and 0.9% plus the sell rate at the time of the transaction

- FX charges vary by region, ranging from 1% to 7%

- There is no separate card top-up fee since funds come from the Bybit account balance

- Wirex Card

- No issuance or monthly card fee

- The exchange rate used for conversions is Wirex's in-app rate, which includes a spread

- FX charges are 0% within the card's home currency

- Local card top-up fees vary by funding route

Here are a couple of example to show how these fees work:

Example 1 (Nexo, EEA user): A user in Germany sends EUR 500 via SEPA to fund the card. The SEPA transfer is free above EUR 100. They then spend USD 100 at a U.S. merchant, which triggers a 0.2% FX fee on the lower end, adding roughly EUR 0.20 to the cost. If the account holds USDC, the conversion step is skipped entirely.

Example 2 (Bybit, international user): A user in a supported EEA country wants to spend USDT on a USD-priced SaaS subscription. The USDT sells at the current rate plus a 0.5% conversion spread. If the subscription is billed in USD and the card settles in EUR, a regional FX charge between 1% and 3% applies on top. A USD 50 monthly subscription could cost roughly USD 51.50 to USD 52.00 in total after spread and FX.

Issuance and monthly fees are the obvious costs. Spread, conversion, FX charges, and top-up fees usually take longer to notice because they show up inside the funding and spending flow rather than as a clear line item at checkout. Failed payment holds and slow refunds also add friction that the fee schedule alone does not capture.

How To Choose A Virtual Crypto Card

The best choice often depends on what goes wrong first. Some cards look fast at signup, then become awkward at checkout. Others take longer to unlock but feel smoother once real spending starts.

For fast online payments, the most important factors are quick card issuance, clean performance at browser and app checkouts, and fewer repeated verification prompts after the initial approval.

For USDC or USDT spending, keep the funding path simple. The supported network should be clearly stated, the conversion should be easy to follow, and the balance should become spendable without extra steps.

For wallet-based spend, check whether Apple Pay or Google Pay feels built into the card experience or loosely attached. Better wallet support helps with mobile checkout and with tap-to-pay if that is part of the daily routine.

For lower-friction setup, look past the first approval screen. Region rules should be clear before sign-up, verification should not drag into extended review easily, and funding should not trigger avoidable compliance checks right away.

For support and reliability, think about the bad days. Failed charges should come with a clear explanation. Refunds should return cleanly and within a reasonable window. Support should be reachable when the account is restricted, not only when everything is working.