Nexo Card Overview

Key facts

Additional details

Nexo Card Screenshots

Nexo Card Pros and Cons

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

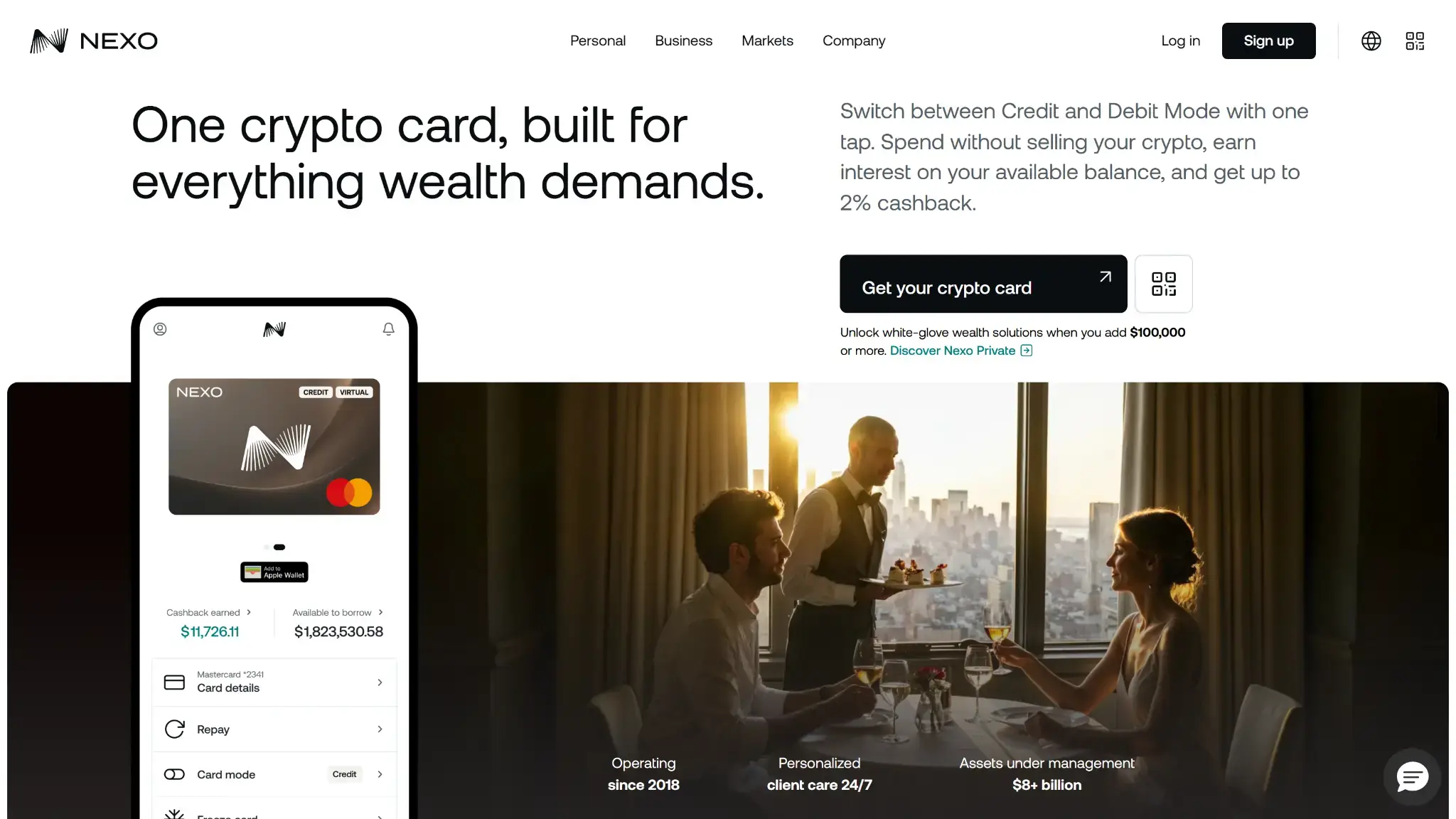

What Nexo Card Is and How It Works

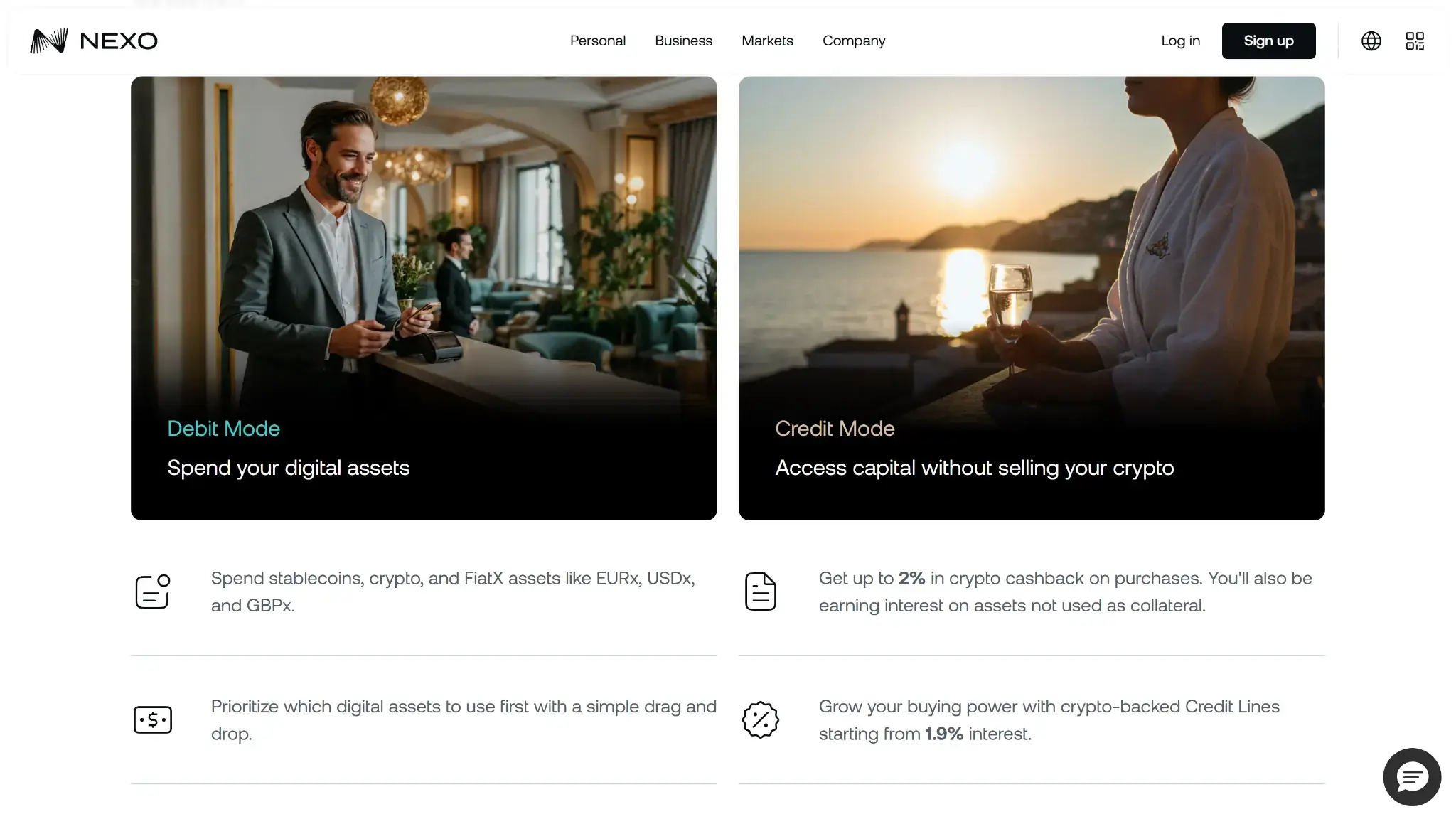

Nexo Card is a dual-mode Mastercard for eligible users in selected European countries, including the EEA and the UK. In Credit Mode, purchases draw from a credit line backed by your digital assets. In Debit Mode, payments come from FIATx balances, stablecoins, or crypto held in your Nexo Savings Wallet. Either way, the transaction settles in fiat on Mastercard rails, with your selected assets converted in real time at checkout. A conversion spread applies when that happens.

Inside the app, you can switch between modes at any time. If you use Debit Mode, you can set a spending priority to control which assets are used first. Holding FIATx or stablecoins for the purchase avoids selling non-stablecoin crypto, which keeps costs more predictable. Some purchases begin as a pre-authorization hold before they settle, and refunds are processed through the original transaction flow.

For the full fee breakdown, see Fees and Conversion Costs below.

Who Nexo Card Is Best For — And Who Should Skip It

Nexo Card fits best when you already use the Nexo ecosystem and want flexibility in how you fund spending. The card is strongest for users who can make use of Debit Mode for routine purchases and still benefit from Credit Mode when they want to avoid selling assets.

| User Type | Fit | Why |

|---|---|---|

| Everyday Spender | High | Low fixed card fees, Apple Pay and Google Pay, and flexible Debit Mode funding |

| Traveler | Medium | Physical card helps, but FX fees and post-allowance ATM charges still matter |

| Stablecoin User | High | Debit Mode supports stablecoins and can reduce extra conversions |

| Self-Custody User | Low | Spending runs through Nexo balances or a Nexo credit line, not self-custody rails |

| Cashback Hunter | Medium | Up to 2% is available, but only in Credit Mode with >$5,000 and loyalty thresholds |

| Heavy Spender | Medium | Spending Controls help, but higher throughput is linked to Nexo Private |

| Low-KYC User | Low | Identity Verification with a supported European ID is required |

| User Who Wants Simple Taxes | Low | Debit Mode can still be taxable, and exports do not remove the manual work |

The natural fit is an existing Nexo user in an eligible European market who wants one card for both direct balance spending and asset-backed borrowing. Stablecoin users also get a cleaner day-to-day path than users who spend volatile crypto at checkout.

The friction gets harder to justify when you want simple rewards, broad geographic access, or cleaner tax handling. It is also a weaker fit for self-custody users and frequent travelers who want fewer FX and ATM costs.

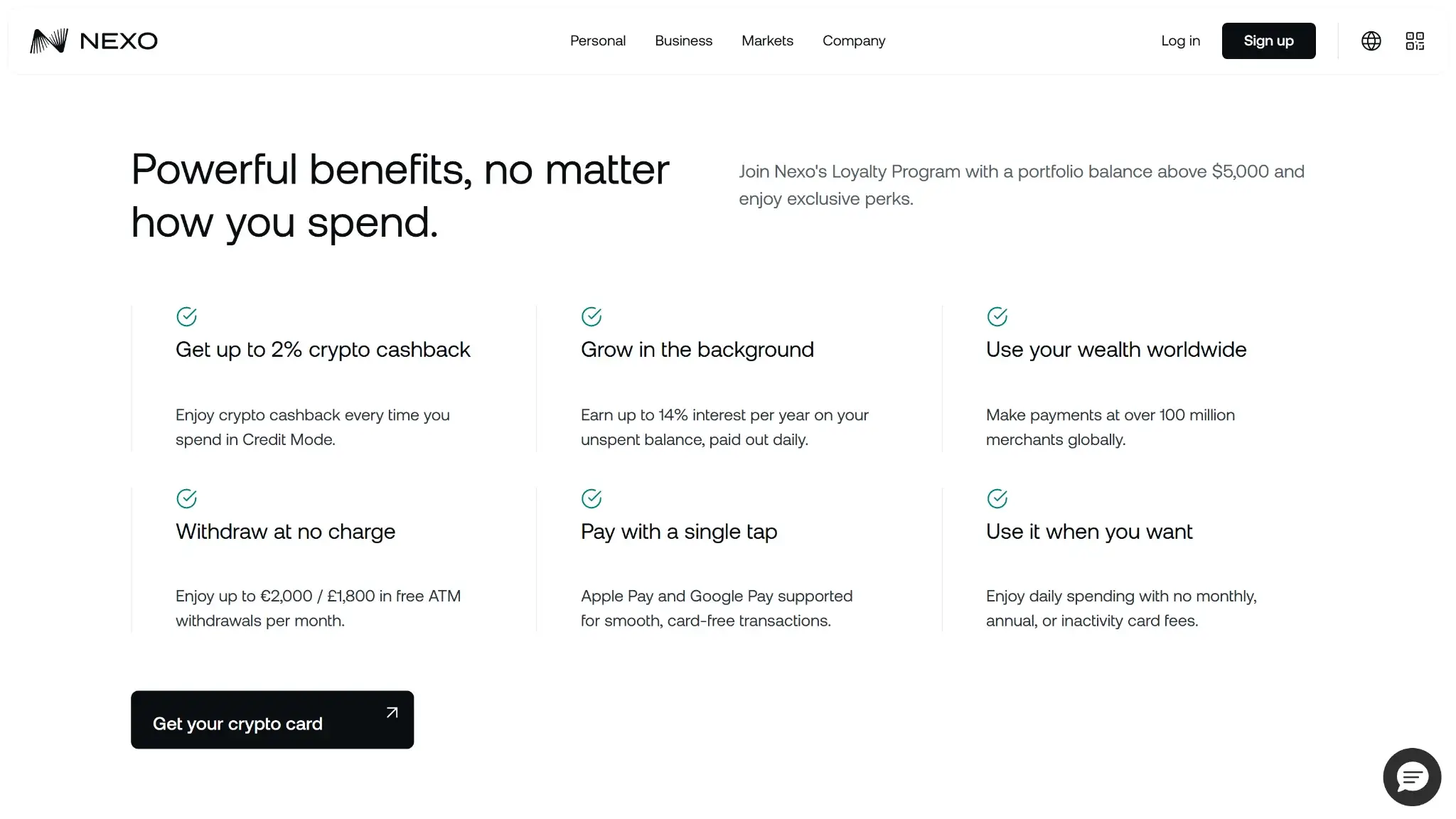

Nexo Card Rewards Mechanics

Nexo structures rewards as tier-based crypto cashback, not a rotating rewards list. Your rate depends on your Loyalty Tier, and you can choose to earn in NEXO tokens or BTC from within the card settings. Cashback is credited after a purchase settles, and its fiat value can change because it is paid in crypto.

Compared with other crypto cards, Nexo's published top rate is lower than some exchange-issued cards that advertise headline cashback above 5%. The trade-off is that Nexo offers a BTC rewards option rather than paying exclusively in a platform token, and the tier structure is fixed rather than rotating monthly. The main barrier is the eligibility threshold: the $5,000 portfolio minimum and loyalty tier are required before any cashback is earned.

Nexo Card Fees and Pricing

Nexo does not charge annual, monthly, or inactivity card fees, which keeps fixed costs low. Variable costs apply when you spend across currencies or withdraw from ATMs past your tier allowance, so those are where to focus when comparing against alternatives.

| Fee | Amount | Notes |

|---|---|---|

| Annual fee | $0 | No monthly, annual, or inactivity fees |

| Foreign transaction (EEA/UK/CH weekday) | 0.2% | Applies when spending in a different currency |

| Foreign transaction (EEA/UK/CH weekend) | 0.7% | Rate increases on weekends |

| ATM withdrawal | Free to tier allowance, then 2% (min 1.99 EUR/GBP) | Allowance resets monthly; ATM operators may add their own fee |

| Replacement card | Not disclosed | Check in-app card settings and cardholder terms |

| Conversion spread | Variable | Applies in Debit Mode when assets are converted at checkout |

The conversion spread is the gap between the rate Nexo applies at checkout and the mid-market rate. In Debit Mode, any stablecoins, crypto, or FIATx converted at the point of sale is subject to this spread. Cross-currency purchases can also carry both the Mastercard conversion and Nexo's FX fee, and that FX fee shifts between weekdays and weekends. To reduce the number of conversions in a single purchase, spending from FIATx or a stablecoin balance is simpler than spending volatile crypto directly.

On fixed fees, Nexo is competitive. The area where it can be less favorable is cross-currency spending: the FX fee applies even within EEA and UK, and the weekend rate is notably higher. Some competing low-fee crypto cards market zero FX fees outright, while others layer crypto conversion costs on top. Check where you spend most before deciding whether the fee structure fits.

Nexo Card Limits — Purchase and ATM

Nexo gives users direct control over card limits through Spending Controls in the app, alongside program-level caps that Nexo sets. Here is a summary of how limits are structured.

| Transaction type | Limit structure | Notes |

|---|---|---|

| Card purchase | User-set via Spending Controls | Custom limits per transaction, daily, weekly, and monthly; program caps also apply |

| ATM cash withdrawal | Tier-based monthly free allowance; overall monthly cap | ATM operators may impose their own per-transaction limit |

| Contactless tap | Follows local terminal rules | Chip and PIN may be required after certain contactless thresholds |

If you need higher throughput, Nexo links elevated spending limits to Nexo Private, which is positioned for clients with larger balances. For standard users, the practical path is to adjust Spending Controls in the app and confirm you have sufficient balance or collateral for the mode you are using.

The most common reasons a Nexo Card is declined are insufficient available balance in Debit Mode, not enough credit line in Credit Mode, a Spending Controls cap being hit, the card being frozen, or the merchant category being blocked. The free ATM allowance resets monthly, and any limits set in Spending Controls reset on their own schedule.

Eligibility and Availability — Countries & States

Nexo Card is available to citizens and residents of selected European countries. Eligibility is not the same as being available across all of Europe or the EEA; Nexo applies country-level restrictions, and UK users may face additional onboarding checks. Here is the access breakdown.

- Regions supported: Selected European countries, including EEA and UK.

- U.S. states: Not supported. The United States is on Nexo's exclusions list, with no state-level exceptions.

- Age and KYC: Identity Verification is required using a supported European identity document. Onboarding includes a liveness check, and Nexo may request additional checks such as wealth verification in some cases.

- Excluded jurisdictions: Afghanistan, Bulgaria, Canada, Central African Republic, Crimea, Cuba, Donetsk, Iran, Kherson, Libya, Luhansk, Myanmar, North Korea, South Sudan, Sudan, United States, Yemen, and Zaporizhzhia.

- Digital wallets: Apple Pay and Google Pay are both supported.

- Physical card: Physical card ordering is temporarily paused. The virtual card is the only option until that changes.

If you are in Europe but outside the EEA, or if your country sits in a grey area, confirm access in the app before making plans around the card. Regional rules can shift, and Nexo's in-app eligibility check is the most reliable source for your specific situation.

UX and Support for Nexo Card

Most Nexo Card actions happen inside the app. From the Card tab, you can switch between Credit Mode and Debit Mode, activate the virtual card, add it to a digital wallet, set Spending Controls, and manage notifications. The controls are organized in one place, which makes day-to-day management straightforward once you are set up.

The practical friction points tend to come at onboarding and in specific execution scenarios, such as understanding conversion costs in Debit Mode or getting timely support if an account review interrupts card access. In 2025, Nexo received external recognition tied to the card experience: at The Digital Banker's 2025 Digital CX Awards, Nexo won Best Wealth Client Loyalty Program for Digital CX and Best PayTech for Digital CX, while the Nexo Card was named Most Exciting Payments Solution of 2025 at the INATBA Awards.

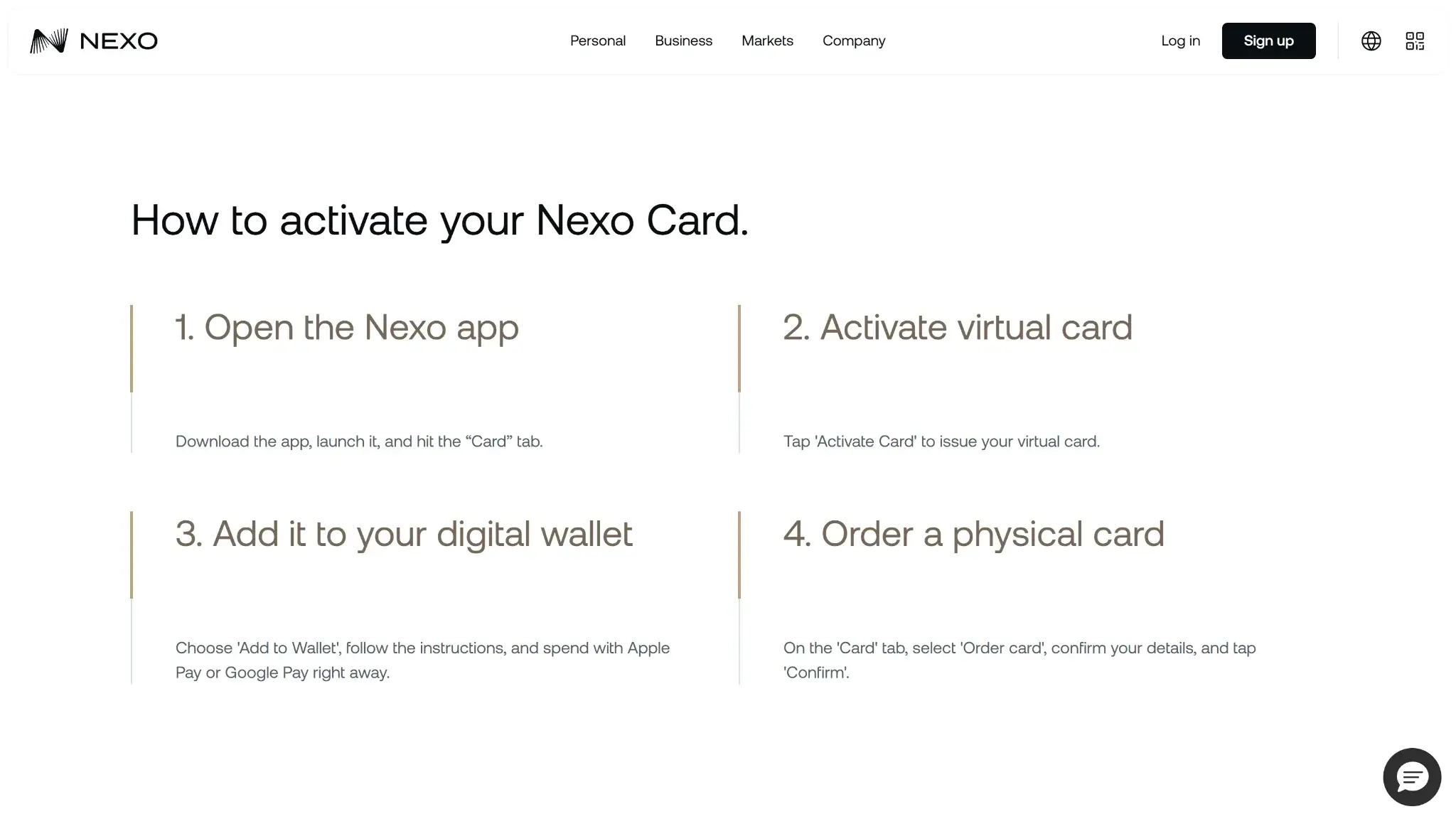

How to Apply for Nexo Card and Get Started

Getting started requires completing identity verification and meeting the minimum balance before the virtual card can be activated. The steps below cover the standard setup path.

- Download the Nexo app, create an account, and complete Identity Verification.

- Add funds so your account meets Nexo's $50 minimum to activate the virtual card.

- Open the Card tab and activate your virtual Nexo Card.

- Add the card to Apple Pay or Google Pay if supported on your device.

- Choose Debit Mode or Credit Mode, and set your Debit Mode spending priority if you plan to spend from balances.

- If you qualify for a physical card and ordering resumes, you can request it in-app and confirm delivery details.

How to Add Money to the Nexo Card

Nexo’s funding path gives you more options than most crypto cards, but cheaper is not always simpler. Which rail makes sense depends on what currency you spend in, whether you want to avoid conversion spread, and how much tax complexity you can tolerate.

| Funding Rail | Supported Assets | Typical Speed | Main Friction |

|---|---|---|---|

| Debit Mode from FIATx | FIATx balances, incl. EURx / USDx / GBPx | Spend once funded | FX fee if spend currency differs |

| Debit Mode from stablecoins | Supported stablecoins in Savings Wallet | Real time at checkout | Conversion spread at purchase |

| Debit Mode from crypto | Supported crypto in Savings Wallet | Real time at checkout | Conversion spread + tax complexity |

| Credit Mode | Asset-backed credit line | At purchase if credit is available | Requires collateral; rewards threshold still applies |

The table shows four paths, but the practical split is two. Debit Mode from FIATx or stablecoins suits users who want predictable costs and cleaner records. Credit Mode suits users who want to preserve their crypto positions and earn cashback, provided they can meet the collateral and loyalty requirements. Spending crypto directly in Debit Mode sits in the middle: it works, but it introduces the most friction across conversion costs, price exposure, and potential tax events.

To top up, open the Add Funds flow in the app. Bank transfers credit FIATx balances using the on-screen banking details. Crypto top-ups require selecting the asset and network, then sending to the deposit address shown.

Security and App Experience

Nexo covers the standard security controls expected from a card linked to a crypto account. Below is a breakdown of what is available.

- Two-factor authentication: Nexo supports 2FA with an authenticator app, passkeys, and email and SMS as backup methods.

- Card freeze: You can freeze and unfreeze the card from the Card tab. Freezing pauses all card spending until reversed.

- PIN management: The card PIN can be revealed and changed in-app. Some actions require a 2FA confirmation step.

- Card details: Card number, expiry date, and CVC are viewable in the app or web platform.

- Transaction alerts: The Notification Center covers card activity alerts. For some transactions, Nexo may request in-app approval if push notifications are off. Transaction history can be filtered and exported.

- Status page: Nexo publishes a public Status Center with real-time service health, maintenance updates, and incident history.

- Zero liability: Mastercard publishes Zero Liability Protection for unauthorized transactions, subject to conditions and issuer rules. For the terms that apply specifically to your card, refer to DiPocket's cardholder terms and Mastercard's Zero Liability policy.

The one thing worth checking independently is whether alerts and prompts are working correctly on your device. If push notifications are off, some in-app approval prompts may not surface in time.

Nexo Card Alternatives

If Nexo Card does not fit your needs, these alternatives cover different use cases. The table below outlines who each card suits better, followed by more detail on each option.

| Card | Why choose it instead |

|---|---|

| Wirex Card | Better for debit-first spending with no annual fees and no foreign transaction fees, without a credit line requirement |

| Bybit Card | Better for higher headline cashback potential (up to 10%) in eligible markets, for users comfortable with a points-based rewards system |

| Crypto.com Visa Card | Better for a larger tier ladder with ecosystem perks, for users already in the Crypto.com platform |

Wirex and Bybit are the closest functional alternatives for European users. Wirex removes FX fees entirely, which makes it simpler for cross-currency spending. Bybit's tiered cashback can reach higher rates, though the system involves points conversion rather than direct crypto payouts. Crypto.com suits users who want perk-style benefits across streaming and travel and are already using the exchange or app. None of the three offer the dual-mode credit line that makes Nexo Card distinct.

Final Verdict

Nexo Card is a useful option for eligible European users who want one card for both Debit Mode spending and a crypto-backed credit line. Its biggest strengths are the dual-mode setup, low core card fees, and the option to earn cashback in BTC or NEXO if you meet the loyalty requirements. The main limitations are regional availability, cashback restrictions, and FX costs that can reduce value on cross-currency spending. Before applying, check the latest card limits, regional access rules, and whether physical card ordering is currently available in the app.

Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets)., No annual card fees — No monthly, annual, or inactivity fees on the card itself., Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

Why it stands out

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

What to consider

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.