Bybit Card Overview

Additional details

Bybit Card Screenshots

Bybit Card Pros and Cons

Pros

- 1% uncapped base cashback with no annual fee

- Fiat-first funding can skip the 0.9% spread

- No monthly, inactivity, or issuance fees

- €5,000 daily spend and €2,000 daily ATM caps

- Instant virtual card, freeze and limit controls

Cons

- EEA EUR card closed on bybit.com Jan. 1, 2026

- 0.9% spread plus a taxable sale on crypto spend

- 0.5% FX fee on cross-currency purchases

- Custodial — funds sit on the exchange

- Base rate 1%; 2%+ needs VIP tier, capped monthly

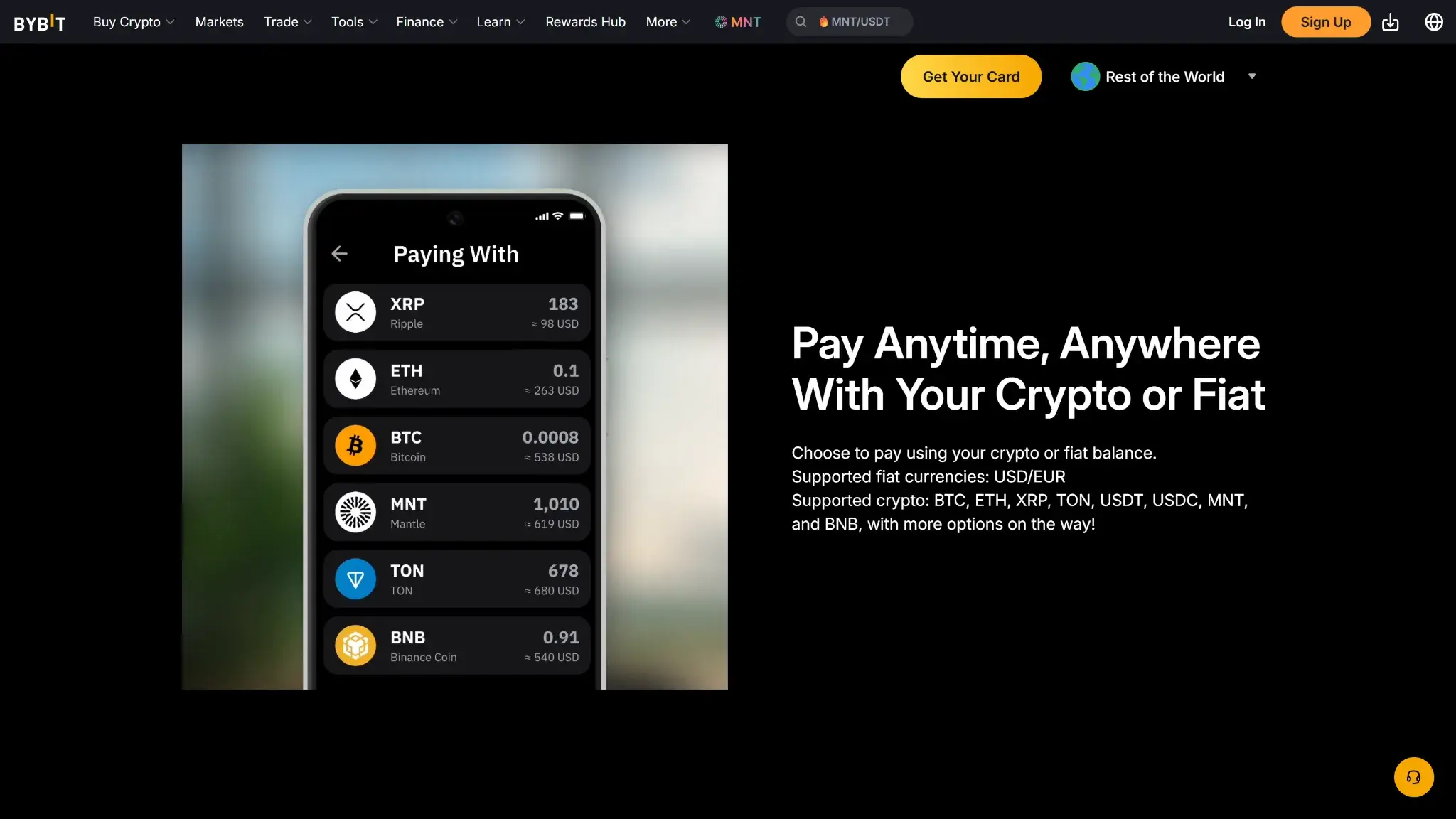

What Bybit Card Is and How It Works

The card draws on your Bybit Funding Account in real time. Fiat goes first: a purchase settles from your fiat balance, and only when that balance falls short does the card sell crypto to cover the difference, working down a priority order you set across BTC, ETH, USDC, and AVAX. Purchases post as an authorization hold and settle afterward.

The auto-sell leg is where the cost and the tax sit. Any part of a purchase settled by selling crypto pays a 0.9% spread on top of Bybit's One-Click-Sell rate and counts as a disposal of the asset in most tax systems. A cardholder who keeps the fiat balance topped up never triggers either, which makes the fiat-first design cheaper in practice than a pure auto-sell card — provided the cardholder actually maintains that balance.

Who Is Bybit Card For?

The card fits an existing Bybit user in a live region — Australia, Brazil, Argentina, Mexico, the AIFC, or Switzerland — who keeps fiat on the exchange and wants 1% back on card spend with no recurring fee. Swiss readers get the original program untouched by the EEA change.

A new EEA reader gets a worse deal, because the product this schedule describes is no longer open to them on bybit.com and both replacement routes carry unconfirmed terms. It is also the wrong card for anyone applying because of the 10% figure, which needs the top VIP tier and still delivers only a capped monthly reward (exact cap figure not published), and it is closed to US residents entirely.

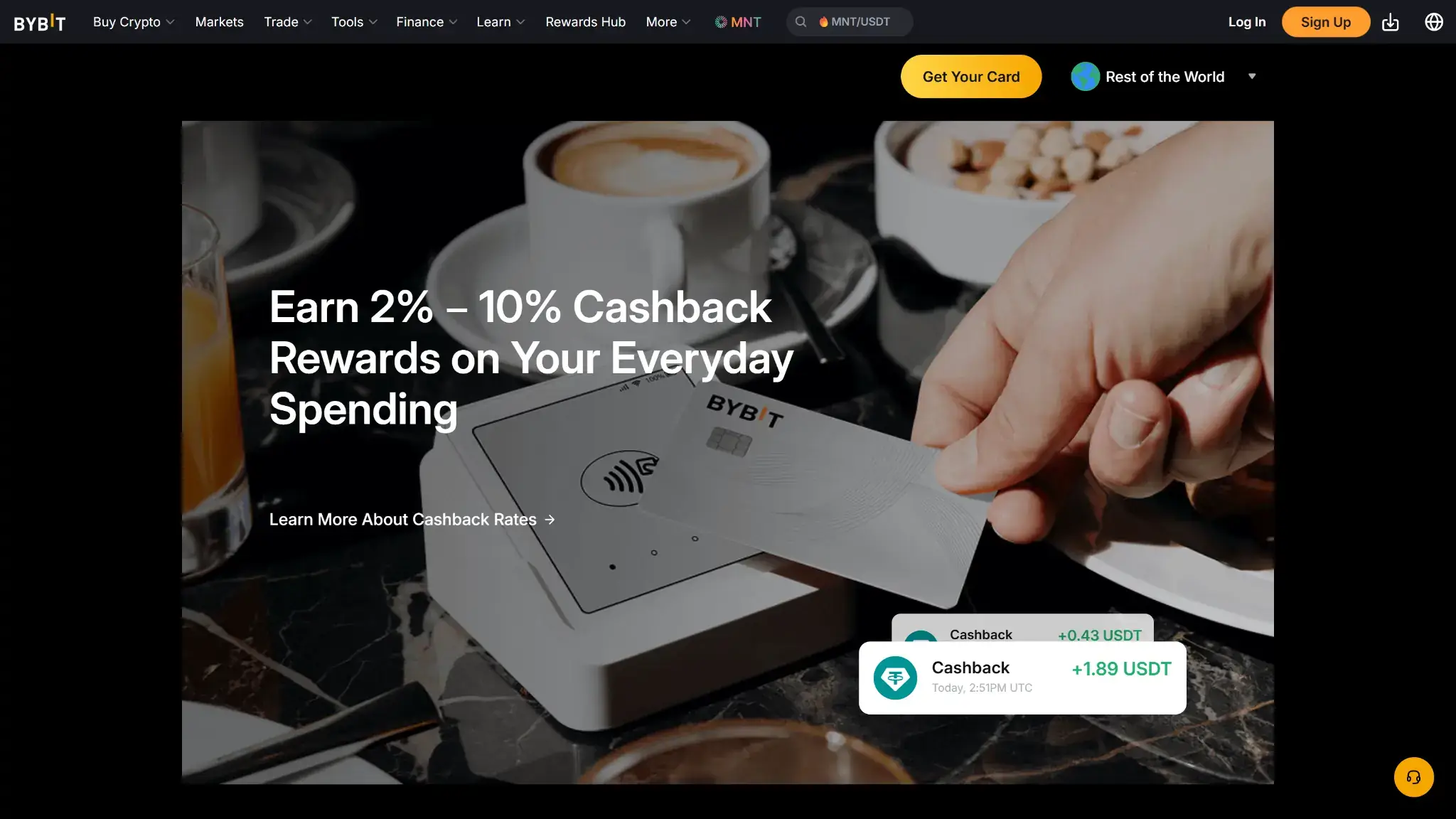

Bybit Card Rewards Mechanics

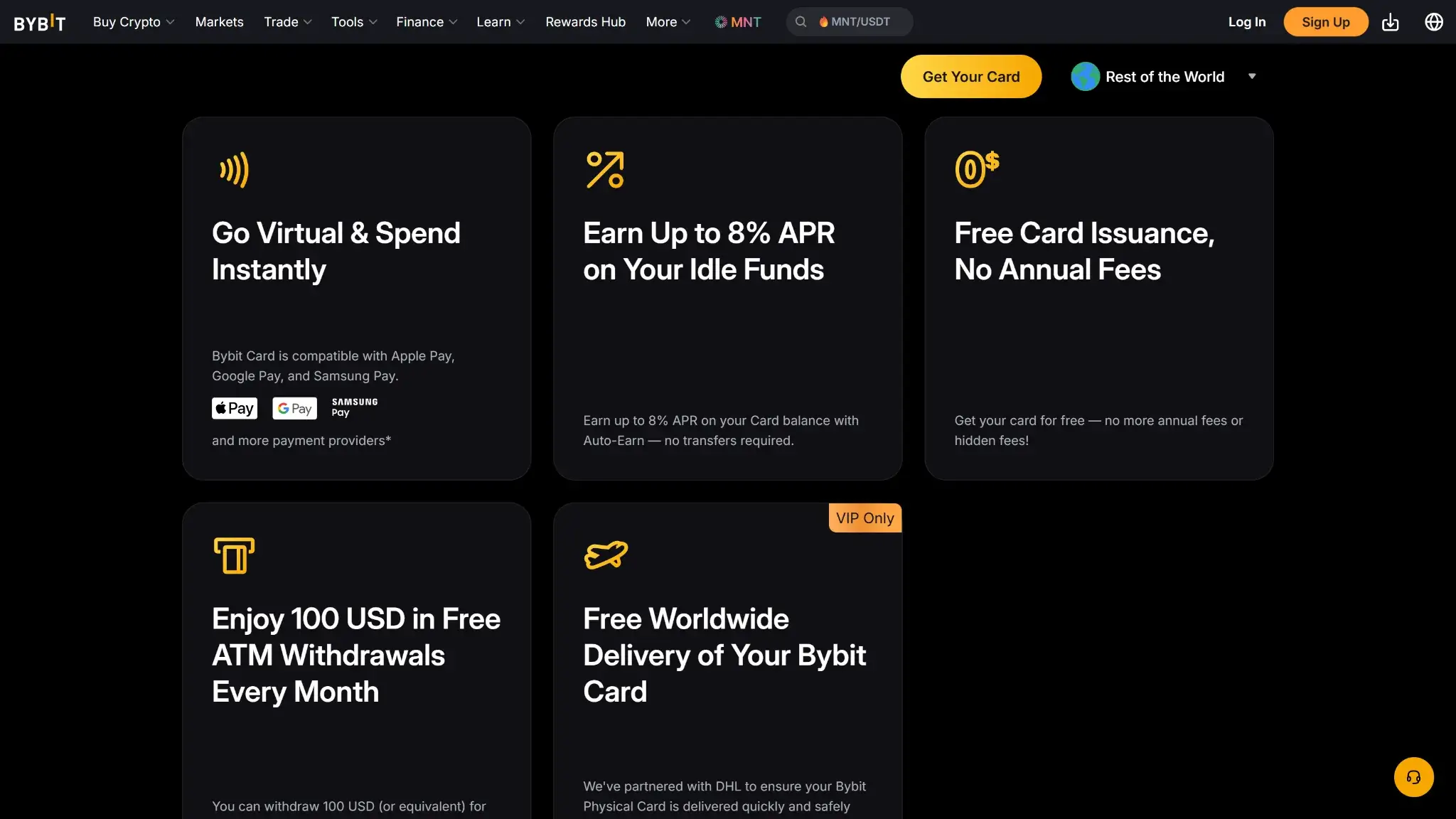

Cashback starts at 1% for non-VIP cardholders on everyday spend, with no monthly cap. It rises to 2% at the entry Beta tier (VIP1) and up the Bybit VIP ladder: Alpha (VIP2) pays 4%, Apex (VIP3) 6%, Omega (VIP4) 8%, and Infinite (VIP5) 10%, with the VIP tiers subject to a monthly cap. Rewards accrue as Rewards Points valued in USDT and convert to BTC, USDT, USDC, or AVAX, either manually through the Rewards Market or daily through Auto Cashback.

Cashback is earned on everyday spending whether the purchase draws on fiat or on crypto. Bybit's card page states the base 1% applies to everyday spend with no monthly cap, so a cardholder who keeps fiat topped up still earns it. That resolves the earlier question over whether cashback required crypto-funded transactions: it does not, so the fiat-first thesis of this review — top up, skip the 0.9% spread, still earn cashback — holds.

| Element | Value | Notes |

|---|---|---|

| Base rate | 1% | non-VIP everyday spend, no monthly cap; 2% at VIP1 (Beta) |

| Top rate | 10% | Infinite tier (VIP5), under a monthly cap |

| Earning basis | everyday spend, fiat- or crypto-funded | not restricted to crypto-funded transactions |

| Reward currency | BTC, USDT, USDC, or AVAX | accrued as Rewards Points valued in USDT |

| Payout cadence | manual or daily | Rewards Market manually or Auto Cashback daily |

| Caps/minimums | 1% base uncapped; VIP tiers capped monthly (exact figure not published) | external sources describe per-tier point caps, not a flat €200 spend cap applied identically across tiers |

The base 1% is uncapped. The VIP-tier rates carry a monthly cap, though the exact cap figure is not published on Bybit's marketing page; external sources describe per-tier point caps rather than a flat €200 spend cap applied identically to every tier. Either way the cap keeps the realized VIP ceiling low, so a normal cardholder plans around the uncapped 1% — 2% at VIP1. The upper tiers require exchange holdings and trading volume most cardholders never carry, and the cap flattens the difference between tiers anyway. Payout assets are liquid, which spares cardholders the volatile-token payouts some rival cards attach to their headline rates.

Bybit Card Fees and Pricing (EEA/CH Program)

These figures describe the EEA/CH schedule attached to the bybit.com EUR card, which closed to new EEA applicants on Jan. 1, 2026. Switzerland stays on this program. The bybit.eu EUR card and the bybit.com USD card carry their own schedules.

| Fee or charge | Amount / rate | When it applies | Notes |

|---|---|---|---|

| Crypto conversion | 0.9%, minimum €1/$1 | Whenever a purchase or ATM withdrawal sells crypto to settle | On top of Bybit's One-Click-Sell rate; the €1/$1 floor makes small crypto-settled purchases proportionally more expensive |

| Foreign exchange | 0.5% | Spend outside the card currency | On top of Mastercard's rate |

| ATM | Free to €100 a month, then 2% | Withdrawals above the monthly free allowance | 2% on the excess |

| Physical card issuance or replacement | About €5 | Issuing or replacing a physical card | |

| Annual, monthly, inactivity, and cancellation fees | None |

The 0.9% is the number to price in, because it applies per purchase on the crypto leg — subject to a €1/$1 minimum that bites hardest on small crypto-settled purchases — and compounds with the taxable-sale consequence described under Tax below. A cardholder who funds with fiat pays none of it, and a cardholder who spends purely from crypto pays it on everything.

Bybit Card Limits, Purchase and ATM

On the EEA/CH schedule the card allows €5,000 per transaction and €5,000 a day in purchases, with monthly and annual ceilings above that, and physical cards withdraw up to €2,000 a day at ATMs. The Virtual Card Lite tier carries a €150 lifetime spend cap and exists for trial use. Limit increases are requested from the card dashboard and take up to seven business days to review. For everyday spending the standard caps rarely bind.

| Limit | Amount | Notes |

|---|---|---|

| Per-transaction purchase | €5,000 | EEA/CH schedule |

| Daily purchase | €5,000 | Monthly and annual ceilings above that |

| Daily ATM withdrawal | €2,000 | Physical cards |

| Virtual Card Lite lifetime spend | €150 | Exists for trial use |

Eligibility and Availability — Countries and States

Applicants must be 18 or older with a verified Bybit account and completed ID verification, and some programs ask for a proof of address issued within the last three months.

Live programs cover the EEA and Switzerland (with the closure below), Australia, Argentina, Brazil, Mexico, Kazakhstan through the AIFC, and parts of Asia-Pacific.

Since Jan. 1, 2026 the EUR card is closed to new EEA users on bybit.com. Bybit is moving its EEA business to bybit.eu, its MiCA-licensed EU entity, with all EEA users due on the new platform by Jul. 1, 2026. An EEA reader keeps a EUR card by registering on bybit.eu and applying there, or takes a USD card on bybit.com. Whether the January closure also affects existing cardholders' renewals is unconfirmed, as are both replacement fee schedules.

Restricted Countries

The following markets are excluded from every Bybit Card program:

- United States

- United Kingdom

- Chinese Mainland

- Hong Kong

- Singapore

- Canada

- North Korea, Cuba, Iran, Sudan, and Syria, along with other sanctioned jurisdictions

On the UK specifically: Bybit's exchange re-entered the UK in Dec.

Funding Rails

Funding runs through the Funding Account itself. Fiat arrives by Bybit's regional deposit rails, and the crypto side draws on four priority assets — BTC, ETH, USDC, and AVAX — sold automatically at the point of sale when fiat runs short. The sale prices at Bybit's One-Click-Sell rate plus the 0.9% spread.

The model sits between a preload card and a pure auto-sell card. Held fiat behaves like a preload balance with no conversion cost. The crypto leg behaves like Coinbase-style auto-sell, with the spread and a taxable disposal attached to every purchase it settles. Ranking USDC first in the priority order keeps any reportable gain on those forced sales near zero, since a stablecoin rarely moves against its purchase price.

The “keep fiat topped up, skip the 0.9% spread, and still earn cashback” payoff holds. Bybit's card page states cashback is earned on everyday spending whether the purchase is funded from fiat or from crypto, so the fiat-first advantage stands rather than being conditional on crypto-funded spend.

UX and Support for Bybit Card

The card is custodial from end to end. The balance behind it lives on the Bybit exchange, and on the EEA/CH program Harmoniie SAS (ACPR-regulated) is the issuer of record while Moorwand Ltd holds the Mastercard license, both e-money institutions, with Bybit acting as the program partner. Naming the issuers counts in the program's favor, but the e-money layer governs the card rails only — the money itself is exchange custody.

The decisive question for a custodial card is whether funds come back out when something goes wrong: an account review, a compliance freeze, a disputed charge. Recovery runs through Bybit's own processes, with no independent issuer holding your deposit. Size the balance you keep on the exchange with that in mind.

UX, App, and Support

The card sits in the main Bybit app next to the exchange, so setup, funding, and controls stay in one place for an existing user. A virtual card is issued on approval, usually within minutes and at most within seven working days, and the dashboard handles freezing, spending limits, and per-channel toggles. Google Pay works on every program, and Apple Pay covers the EEA, Australia, Argentina, and Brazil.

Support is Bybit's standard exchange support, reachable in-app. Card disputes route through the program and account-level problems route through the exchange, which is where custodial card support typically slows down.

Tax and Record-Keeping

Fiat-settled purchases create no tax event. Crypto-settled purchases each sell an asset in real time, and in most jurisdictions each sale is a reportable disposal, so a cardholder who spends from crypto all month generates a matching list of small taxable sales on top of the 0.9% spread. Bybit provides transaction history and account statements to reconstruct them, with no dedicated cost-basis or tax-export tooling for the card, so reconciliation lands on the cardholder.

Bybit Card Alternatives

If Bybit Card's regional restrictions, tier requirements, or fee structure do not fit your situation, these three alternatives cover the most common reasons to look elsewhere.

| Alternative | Why choose it instead |

|---|---|

| Coinbase Card | US-issued access, no staking requirement, monthly reward-asset choice |

| Crypto.com Visa Card | More card tiers and perks, no foreign transaction fees on most tiers in some regions |

| Wirex Card | No annual fee, no FX fees, rewards in platform token without tier-based cashback caps |

Coinbase Card is the cleaner option if US availability is the deciding factor. Crypto.com suits users who want more tier variety and extras alongside their crypto spending. Wirex works better for anyone who prioritizes FX simplicity over chasing Bybit's tiered cashback ladder.

For a broader comparison of low-fee crypto card options, including cards with no foreign transaction fees, the category page covers the main alternatives side by side.

Final Verdict

Where the card is open, it does the job: Mastercard acceptance, wallet support, 1% back with no recurring fee, and limits that stay out of the way. The fiat-first funding design beats a pure auto-sell card for anyone disciplined about keeping fiat on the account. The bybit.com EUR card closed to new EEA applicants on Jan. 1, 2026, and the two replacement products carry unconfirmed terms. Add a 10% ceiling that needs VIP5 under a capped monthly reward, plus a 0.9% spread and a taxable sale on every crypto-settled purchase, and the fair rating is a competent 1% card (2% at VIP1) in its live regions with an unresolved availability question hanging over the EEA.

Set your own crypto auto-sell priority, Named EEA e-money card issuers, Cashback paid in liquid BTC, USDC, or AVAX

Why it stands out

- 1% uncapped base cashback with no annual fee

- Fiat-first funding can skip the 0.9% spread

- No monthly, inactivity, or issuance fees

- €5,000 daily spend and €2,000 daily ATM caps

- Instant virtual card, freeze and limit controls

What to consider

- EEA EUR card closed on bybit.com Jan. 1, 2026

- 0.9% spread plus a taxable sale on crypto spend

- 0.5% FX fee on cross-currency purchases

- Custodial — funds sit on the exchange

- Base rate 1%; 2%+ needs VIP tier, capped monthly

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.