Elon Musk’s SpaceX IPO fever sparks $1 billion crypto bet before Nasdaq debut

The SPCX futures contract suggests expectations for a first-day pop remain intact, though the market has pulled back from its most aggressive bets.

Quick Take

- Crypto traders pushed more than $1 billion through SpaceX-linked perpetual futures in three days before the company’s Nasdaq debut.

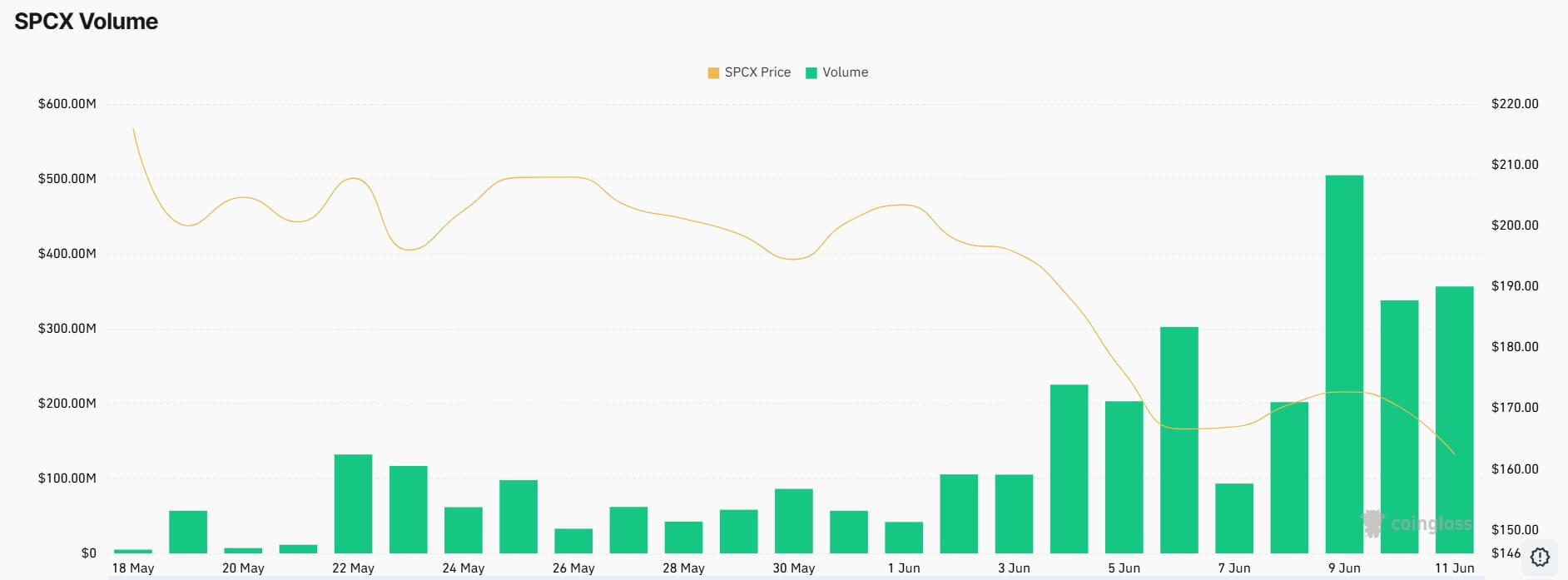

- The SPCX contract near $162 still implies a 17% premium to the $135 IPO price, signaling strong demand and price discovery.

- But the premium has faded from above $220, while Elizabeth Warren is pressing the SEC to delay the listing.

Crypto traders have turned Elon Musk’s expected SpaceX listing into a round-the-clock proxy market, pushing more than $1 billion through SpaceX-linked perpetual futures in the last three days as investors try to front-run one of the largest public offerings in Wall Street history.

The shift comes as retail investors face limited allocations in a heavily oversubscribed offering and look for other ways to gain exposure.

It also arrives with a warning from market history as some of the most celebrated technology listings of the past decade opened to enormous demand, only to punish early buyers with steep first-year losses before settling into longer-term trading patterns.

Crypto becomes the early trading floor

Before SpaceX shares begin trading on a traditional exchange, crypto venues have become the closest thing to a live market for the company’s expected public debut.

The SPCX perpetual future, a synthetic contract linked to SpaceX’s pre-IPO valuation, has drawn more than $1 billion in trading volume over the past 72 hours, CoinGlass data show. Since May 30, cumulative volume across participating platforms has exceeded $2.6 billion, with open interest around $363 million.

Unlike ordinary equity options, perpetual futures have no expiration date. Traders can hold positions indefinitely, but they must manage funding payments and the risk of liquidation if prices move sharply against them.

That structure makes the market especially attractive to crypto traders accustomed to high leverage and continuous price movement.

Hyperliquid helped pioneer the SPCX contract, but activity has since spread beyond decentralized finance. Binance, the world’s largest crypto exchange by trading volume, now accounts for a large share of the market, showing how quickly a synthetic product can become a major venue for price discovery before the underlying stock exists in public markets.

Meanwhile, the market is attracting bullish bets. Arkham Intelligence said one trader using the handle “wenyu8888888” had placed a $5.7 million, 2x short on SPCX, describing it as the largest SpaceX short it had tracked.

The position highlights how the synthetic market has also become a venue for traders willing to bet that the IPO premium will fade once public trading begins. It also shows how quickly a single leveraged account can become part of the broader spectacle around the listing.

For traders shut out of the official bookbuild, the contract offers a way to express a view on SpaceX before the opening bell.

For market watchers, it offers something Wall Street’s formal IPO process does not: a continuously moving price backed by real capital, leverage, and liquidation risk.

That makes the SPCX market a rough but useful gauge of speculative appetite, as it shows where traders willing to take immediate financial risk believe the stock could trade once public markets get their first chance to price it.

However, it does not grant ownership in SpaceX, voting rights, or any claim on shares.

The premium is still there, but smaller

The futures market continues to suggest that traders expect SpaceX to open above its reported IPO price.

The company’s offering has been priced at $135 a share, giving SpaceX an expected valuation of roughly $1.75 trillion to $1.8 trillion. At about $162, the SPCX contract implies a premium of roughly 17% to the listing price.

While that represents a meaningful gap, it is also a sharp reset from the early days of the contract, when speculative buying drove prices above $220 and, at one point, near $230.

At those levels, traders were pricing in a far larger first-day jump and treating SpaceX as a scarcity asset before its stock became widely available.

The compression in that premium is important because it shows the market has become more selective even as headline demand remains enormous.

Underwriters have drawn hundreds of billions of dollars in investor interest for a planned $75 billion raise, making the deal several times oversubscribed.

In many IPOs, that kind of demand would allow bankers to lift the final price range before shares begin trading. SpaceX’s fixed-price structure leaves less room for that adjustment, forcing investors to accept the $135 price or walk away.

Retail demand has added another layer of pressure. SpaceX reserved a larger-than-usual portion of the offering for individual investors, but the scale of demand means many buyers are likely to receive only part of what they requested.

Some of that frustrated demand appears to be spilling into synthetic markets, where traders can build exposure immediately but take on risks that differ markedly from those of owning common stock.

IPO history gives buyers reason to pause

The rush for SpaceX exposure is running into a warning from the recent history of major technology listings: even strong companies can deliver painful early returns when investors buy at aggressive valuations.

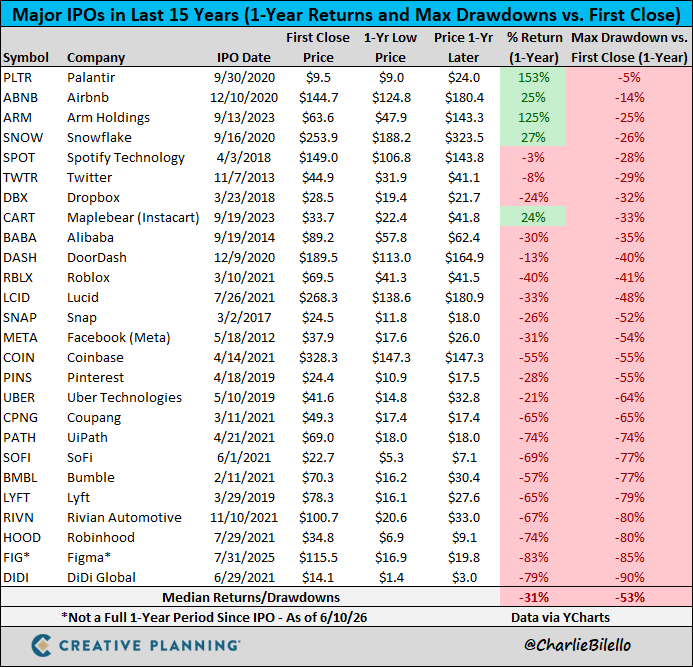

Charlie Bilello, chief market strategist at Creative Planning, has argued that one common mistake investors make during high-profile listings is treating a great business as a great investment at any price.

His analysis of major IPOs shows that the median offering loses 31% in its first year and suffers a peak-to-trough drawdown of 53% along the way.

That point has become more relevant as some investors compare SpaceX, OpenAI, and Anthropic with the early public-market days of Amazon, Google, and Meta. They argue that buying the next generation of dominant technology companies at IPO could resemble buying the last generation of internet giants before they became some of the most valuable businesses in the world.

However, Jim Chanos, the veteran short seller, rejected that comparison and argued that the valuation gap is too large to ignore.

According to him, Amazon went public in 1997 at a valuation of about $450 million, or roughly three times revenue. Google was listed in 2004 at about $23 billion and roughly seven times revenue. Meta debuted in 2012 at a valuation of about $104 billion and around 20 times revenue, then sold off sharply after listing.

Chanos argues that SpaceX is starting from a valuation that already dwarfs those early public-market entry points, leaving less room for investors to benefit from multiple expansion if growth falls short of the market’s most aggressive expectations.

He also pointed to Uber as a cautionary example of how large addressable-market forecasts can fail to translate directly into public-market value. Uber pitched a total addressable market of more than $12 trillion when it went public in 2019. Its market capitalization is now about $150 billion, a little over 1% of that projected opportunity.

Using a similar approach, Chanos argued, would imply a much lower value for SpaceX than the roughly $2 trillion level now being discussed by the market.

Thierry Borgeat, co-founder of the financial research firm Arvy, reached a similar conclusion after tracking the post-listing performance of prominent technology and growth companies over the past decade.

According to him, the record shows that first-year volatility has been the rule, even for companies that later became major market winners.

For context, Facebook fell 54% from its first-year high before recovering. Snap, Uber, Pinterest, Lyft, Rivian, and Robinhood suffered even deeper drawdowns, with declines ranging from 56% to 90% during their first year as public companies.

According to Borgeat, the pattern was not confined to broken listings. Zoom Video Communications finished its first year up 142%, but only after enduring a 40% drawdown. Palantir Technologies closed its first public year up 153%, while still forcing early holders through a 53% decline before the rebound took hold.

Additionally, CrowdStrike, Datadog, and MongoDB also ended their first year in positive territory, but each experienced sharp interim declines.

The lesson from those listings is that early demand can lift a stock on debut without preventing a severe reset once the market begins testing valuation, growth assumptions, and investor patience.

That history complicates the current SpaceX trade. Crypto derivatives still suggest traders expect the company to open above its IPO price.

However, they offer a weaker guide to what happens after the first burst of demand is filled and public-market investors begin deciding whether a valuation near $1.8 trillion leaves enough room for error.

Regulatory scrutiny follows SpaceX's IPO

Meanwhile, the scale of the listing has drawn scrutiny in Washington, where Sen. Elizabeth Warren has urged the Securities and Exchange Commission (SEC) to delay the offering until regulators address risks to retail investors and market structure.

Warren, the top Democrat on the Senate Banking Committee, warned SEC Chair Paul Atkins that a SpaceX listing of this size could create unusual risks for public markets. Her concerns focus on valuation, shareholder rights, and the company’s governance structure.

The letter argued that public investors could be exposed to a company in which control remains heavily concentrated among Musk and insiders.

According to the lawmaker, supervoting shares, mandatory arbitration provisions, and Texas corporate law could limit outside shareholders' ability to challenge management decisions or seek legal remedies in disputes.

Warren also raised concerns about passive investors. At a valuation near $1.8 trillion, SpaceX would likely become a major component of market indexes after listing. That could force millions of investors in index funds and retirement accounts to gain exposure to the company even if they never chose to buy SpaceX directly.

In view of this, Warren stated:

“These are not normal circumstances: a number of additional factors exacerbate concerns and require action by the SEC to meet its investor protection and market integrity mandates by delaying the [SpaceX] IPO.”

The warning adds a political layer to an offering already defined by unusual scale and retail attention. It does not mean the IPO will be delayed. Registration materials have moved through the SEC process, and underwriters are preparing for a debut that could become one of the most closely watched market events in years.

However, Warren’s intervention gives skeptics a clear framework for questioning the deal. The concerns are no longer limited to whether SpaceX opens higher than $135.

They now extend to whether ordinary investors understand the legal, governance, and valuation risks embedded in the offering.

Cardano finally cleared the SEC shortcut for a spot ETF, but its last remaining sponsor quit two days too early

Cardano lost its only dedicated US spot ETF filing just as ADA cleared the six-month CME futures milestone that could make a launch easier.

Athena Bitcoin agreed to a $4.5 million settlement, but claimants may have less than $3 million to split

If the court grants the proposed fee and expenses stay within the stated estimate, at least $2.985 million remains before other deductions.

Nasdaq puts $675 million Avalanche Treasury on the clock over two listing failures

AVAT’s stock needs to more than triple to clear the $1 bid-price test, while a separate $35 million market-value hurdle remains.

Nasdaq puts $675 million Avalanche Treasury on the clock over two listing failures

AVAT’s stock needs to more than triple to clear the $1 bid-price test, while a separate $35 million market-value hurdle remains.

Traders holding $39.5 million in BitMEX Bitcoin perps have 16 days to exit before forced closures begin

New positions stop Aug. 26, while contracts left open face a wind-down that ends in forced closure Sept. 23.

AI financial advisers carry a hidden Bitcoin bias activated by a single specific switch

AI models can favor Bitcoin under crisis and machine-economy prompts, exposing a new risk for banks using automated financial advice.