Most crypto rewards cards look competitive until you read past the headline. A 4% rate can mean very little when it only applies to one spending category, requires a paid membership to unlock, or pays out in a token you would not otherwise hold. The number on the marketing page is the starting point, not the conclusion.

What works for one user often does not work for another. Some want a bitcoin rewards credit card with a clean base rate and no conditions attached. Others prioritize instant payouts, debit access, or perks that still hold value once fees are factored in. The four cards below cover that range, from the cleanest reward structure to the most tier-dependent.

Top Crypto Rewards Card

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 5% CRO rewards with instant payout after each purchase.

- Instant virtual card with broad Apple Pay and Google Pay support (region dependent).

- No annual fee and high daily purchase limits up to $25,000.

Gemini and Coinbase One put more reward value into everyday spending. Nexo is worth a closer look when borrowing against crypto matters more than a simple cashback model, while Crypto.com fits users who can make full use of its tier perks.

Reward percentages do not always show you where value starts to leak. This table focuses on what changes decisions fastest: what you earn, what you must do to keep it, and what typically cuts the return down.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay, Samsung Pay | Available in many regions (e.g., US, EEA/UK, SG, CA, AU, BR) with residency-based eligibility and restricted markets per Crypto.com lists. |

A clean base rate matters more than a high ceiling. The lower-ranked cards can still pay more in the right setup, but their reward value depends heavily on loyalty tiers, paid plans, or offers that can change.

Crypto Rewards Card Reviews

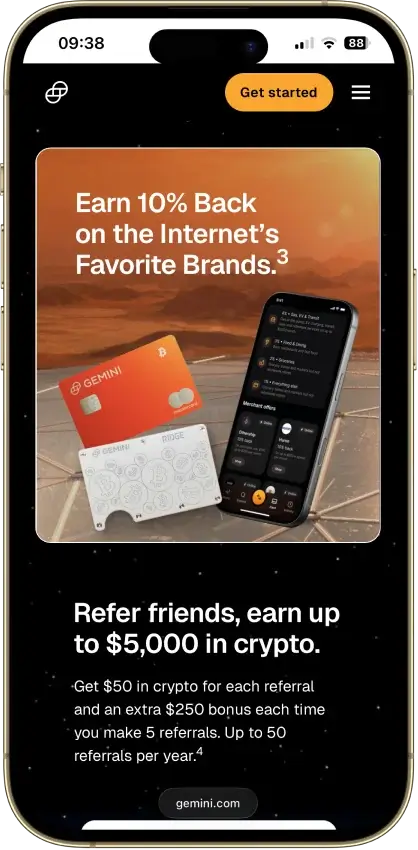

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

Nexo Card

Pros

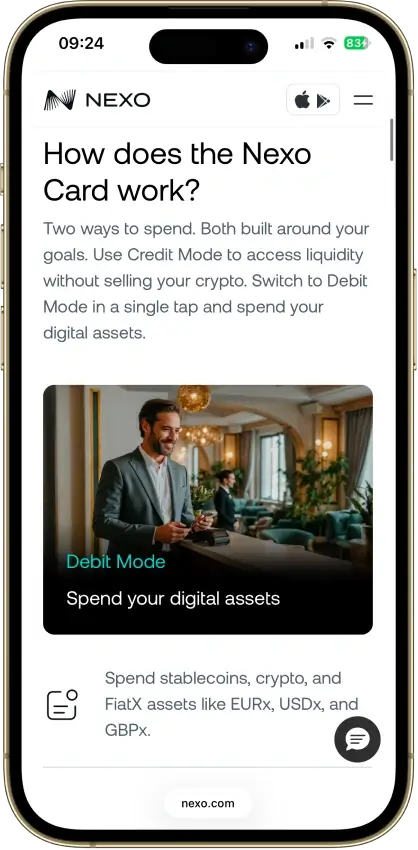

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

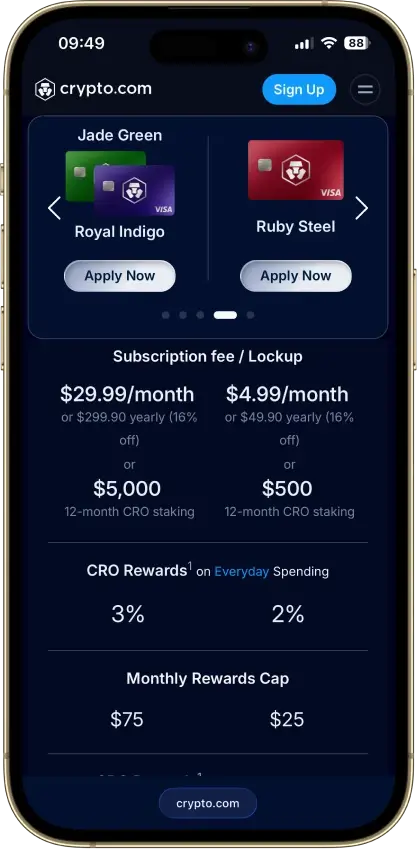

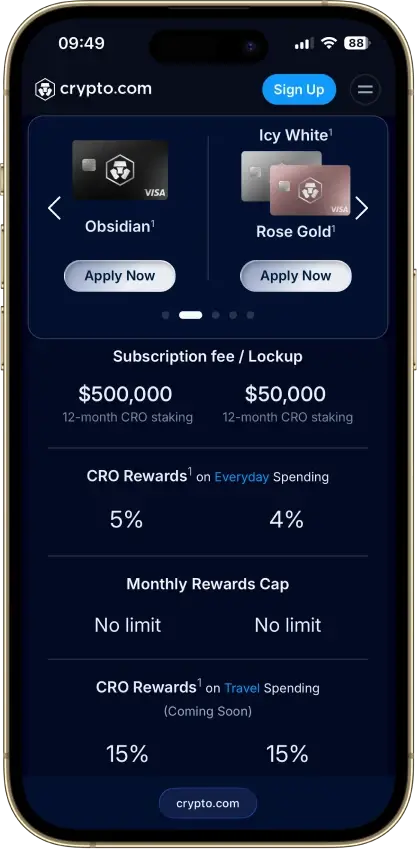

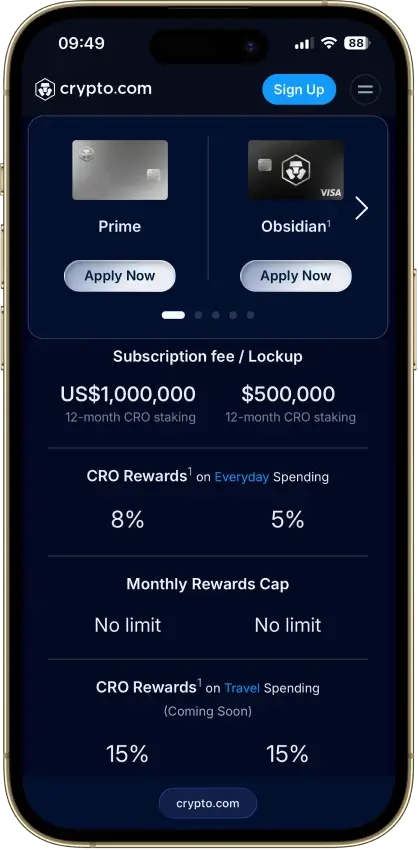

Crypto.com Card

Pros

- Up to 5% CRO back with instant rewards.

- No annual fee and high spending limits.

- Instant virtual card and strong mobile wallet support.

Cons

- 3% foreign fee on lower tiers (US market).

- Monthly cashback caps on mid tiers.

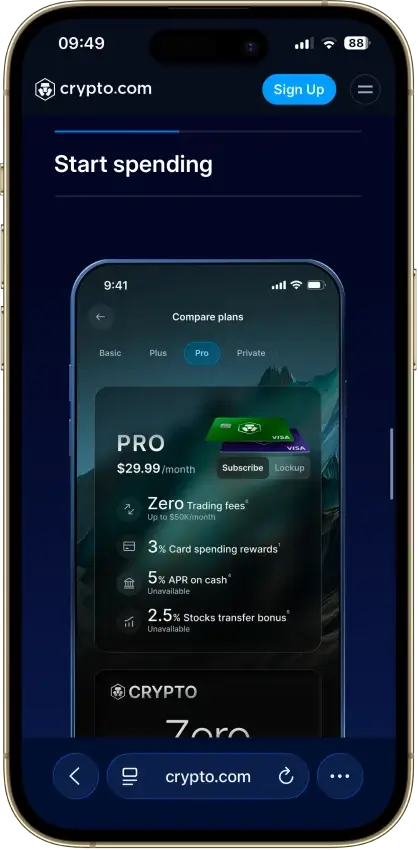

- Requires a monthly fiat subscription or a 12-month CRO lockup to earn rewards.

- Crypto funding includes a conversion spread.

Our Ranking Methodology

These cards were ranked on the reward a normal user can keep after fees, caps, plan costs, and funding friction. A high rate helped, but it did not decide the ranking on its own. Cards moved up when solid rewards came with clean approval, practical spend flow, and terms that did not require unusual effort to maintain.

The heaviest weight went to factors that affect day-to-day use: whether the card worked reliably for ordinary purchases, whether the reward stayed competitive after conditions applied, and whether the funding path stayed simple enough for someone not trying to optimize every step. That mattered more than promotional ceilings, especially when looking alongside crypto debit cards, cards built for contactless mobile payments, and options with lower ongoing fees.

| Factor | What Mattered | Weight Out Of 10 |

|---|---|---|

| Availability + Setup Friction | We checked whether a new user could apply, get approved, pass required verification, and start using the card without unusual delays or regional hurdles. | 1.0 |

| Funding Rails + Conversion Path | We scored how easy it was to move value in, understand the spend path, and avoid confusion around fiat funding, crypto conversion, or balance requirements. | 1.25 |

| Real-World Spend Reliability | We gave the most weight to normal use. That included whether the card handled common purchases cleanly instead of looking good only in ideal conditions. | 1.5 |

| Rewards Value After Conditions | We looked past the headline rate and checked caps, categories, memberships, asset requirements, token exposure, and whether the reward still held up after those conditions. | 1.0 |

| Fees + Hidden Cost Drag | We counted annual fees, membership costs, FX fees, spread, ATM charges, and other costs that can reduce what the user keeps from the reward. | 1.25 |

| Operational Convenience + Limits | We checked spending limits, timing, balance rules, and how easy the card was to live with week to week. | 0.75 |

| App + Controls + Virtual Card Tooling | We scored how well the user could manage the card through the app, including useful controls and the quality of virtual card access. | 0.75 |

| Security + Custody + Freeze Risk | We checked how clearly the trust model was explained, where funds or collateral sat, and how exposed the user was to freezes, holds, or issuer-side control. | 1.25 |

| Support + Refunds + Chargebacks | We looked at whether a normal user could get help when something broke, including disputed charges, refund issues, and basic support responsiveness. | 0.75 |

| Tax + Reporting Readiness | We gave some weight to statements, transaction history, and how manageable the reporting burden looked for a typical user. | 0.5 |

The model also gives credit to cards that reduce friction after approval. Clean controls, usable virtual issuance, and a practical fit for spending while traveling abroad helped when they made the card easier to use without adding extra cost or confusion.

What A Crypto Rewards Card Actually Is

A crypto rewards card can sit on top of very different spending systems, and the reward headline only tells part of the story. The more important question is whether you are spending an issuer credit line, a funded fiat balance, a prepaid balance, or a collateral-backed limit, because the mechanics of each are different enough to change how much the reward is actually worth.

A crypto rewards credit card gives you a credit line and pays rewards in crypto after each purchase. A debit or prepaid rewards card usually spends loaded fiat or an exchange balance instead. Some cards only earn crypto rewards, while others let users spend crypto, stablecoins, or platform balances directly. The key difference is not the branding. It is how spending works and how rewards are posted.

That distinction matters when comparing across card types. A credit card that pays bitcoin back works very differently from cards funded with USDC or USDT-backed spend products, even when the cashback percentage looks similar on paper.

Crypto Rewards Credit Card Vs Crypto Rewards Debit Card

Most confusion starts here. Two cards can both advertise crypto rewards, but the user experience diverges quickly once you look at approval requirements, funding mechanics, reward posting speed, and where extra costs appear.

| Card Model | How It Works And Where Friction Shows Up |

|---|---|

| Crypto rewards credit card | You spend an issuer credit line, repay later, and usually get cleaner reward math. Approval, APR, and credit profile matter more. |

| Crypto rewards debit card | You spend loaded cash, exchange balance, or sold crypto. Setup is often easier, but reward offers and conversion cost can change the outcome fast. |

| Crypto prepaid card | You fund the card before spending. Budget control is simple, but top-up rules, merchant acceptance quirks, and weaker perks can limit value. |

| Hybrid or collateral-backed card | You borrow against crypto or switch spend modes. This can avoid an immediate sale, but collateral rules, loyalty tiers, and liquidation risk add more complexity. |

For pure reward value, credit cards often keep the structure simpler. Debit, prepaid, and hybrid cards can still work well, but the reward depends more on funding friction, balance management, or collateral conditions.

Bitcoin Rewards Credit Cards Vs Flexible Crypto Rewards

This choice affects both convenience and long-term value. Some users want every reward paid in bitcoin. Others want the option to change assets as prices, taxes, or portfolio goals shift. The table below covers what each approach gives you and what it costs.

| Reward Style | What You Get And What You Give Up |

|---|---|

| Bitcoin-only rewards | Simple reward tracking and direct BTC exposure. You give up flexibility if another asset would suit your goals better. |

| Flexible crypto rewards | More choice across reward assets and a better fit for active portfolio management. Menus vary, and not every asset is equally useful or liquid. |

| Platform-token rewards | The headline rate can look high and may unlock extra perks. Value depends more on token price, loyalty rules, and issuer-specific risk. |

| Points that convert into crypto | You may get redemption flexibility, but the extra conversion step can weaken pricing and add friction before the reward becomes usable crypto. |

Users who want a bitcoin rewards credit card usually benefit from simpler reward decisions. Flexible or token-based systems can still pay more, but only when the asset choice, redemption path, and fee structure line up cleanly.

You may also browse our list of top bitcoin reward cards.

Crypto Rewards Cards Vs Normal Cashback Cards

Crypto rewards cards beat normal cashback cards in a more situations than the marketing often suggests. They work best when the reward asset is one you already want to hold, when the card does not add much extra cost, and when the reward arrives in a form that is easy to keep or sell.

Once those conditions fall away, normal cashback cards regain the edge. Fiat cashback is easier to value, easier to compare, and easier to use.

The table below covers the situations where each type tends to win.

| Situation | Which Usually Wins And Why |

|---|---|

| Long-term bitcoin accumulation | Crypto rewards cards usually win if the card pays BTC directly and you planned to accumulate BTC anyway. |

| Simple everyday spending | Normal cashback cards usually win because the reward value is easier to track and fewer conditions sit behind the headline rate. |

| Travel and foreign transactions | It depends. Crypto rewards cards can win with 0% FX and clean acceptance, but mainstream cards are safer when crypto card fees vary by region or tier. |

| Tax simplicity | Normal cashback cards usually win because crypto rewards can create extra reporting work once sold, transferred, or swapped. |

| Predictable reward value | Normal cashback cards usually win because fiat value stays fixed, while crypto rewards can move up or down before you use them. |

A crypto rewards card is usually the better fit for someone who treats rewards as a slow accumulation tool rather than a spending rebate. For everyone else, a normal cashback card often delivers a cleaner result: simpler bookkeeping, more stable reward value, and less time spent checking caps, tiers, and conversion rules.

How To Choose The Best Crypto Rewards Card

The right card depends less on the highest advertised rate and more on how that rate holds up against your actual spending pattern. Before committing, it helps to work through a short checklist.

- Decide whether you want a true crypto rewards credit card or a debit or prepaid rewards card.

- Decide whether you want bitcoin rewards only or more flexible crypto reward options.

- Check the best usable rate on your actual spending categories.

- Check the monthly cap before trusting any headline percentage.

- Check whether you need a paid membership, staking, or platform balance to unlock the best rate.

- Check FX, spread, and reward-sale friction, not just the card fee.

- Check how easy it is to hold, sell, or transfer the reward asset.

- Check how painful taxes and reporting could be in your jurisdiction.

A good crypto rewards card should still look competitive after those checks. If the value only works with a paid plan, a loyalty token, or a narrow bonus category, a standard cashback card may leave you with more usable value in practice.