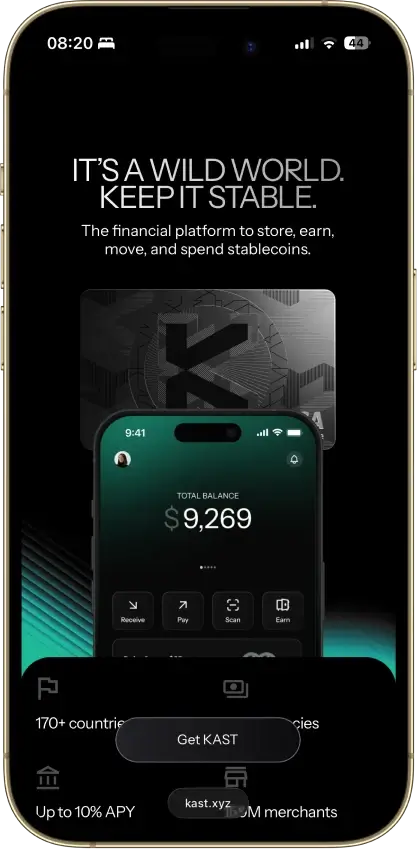

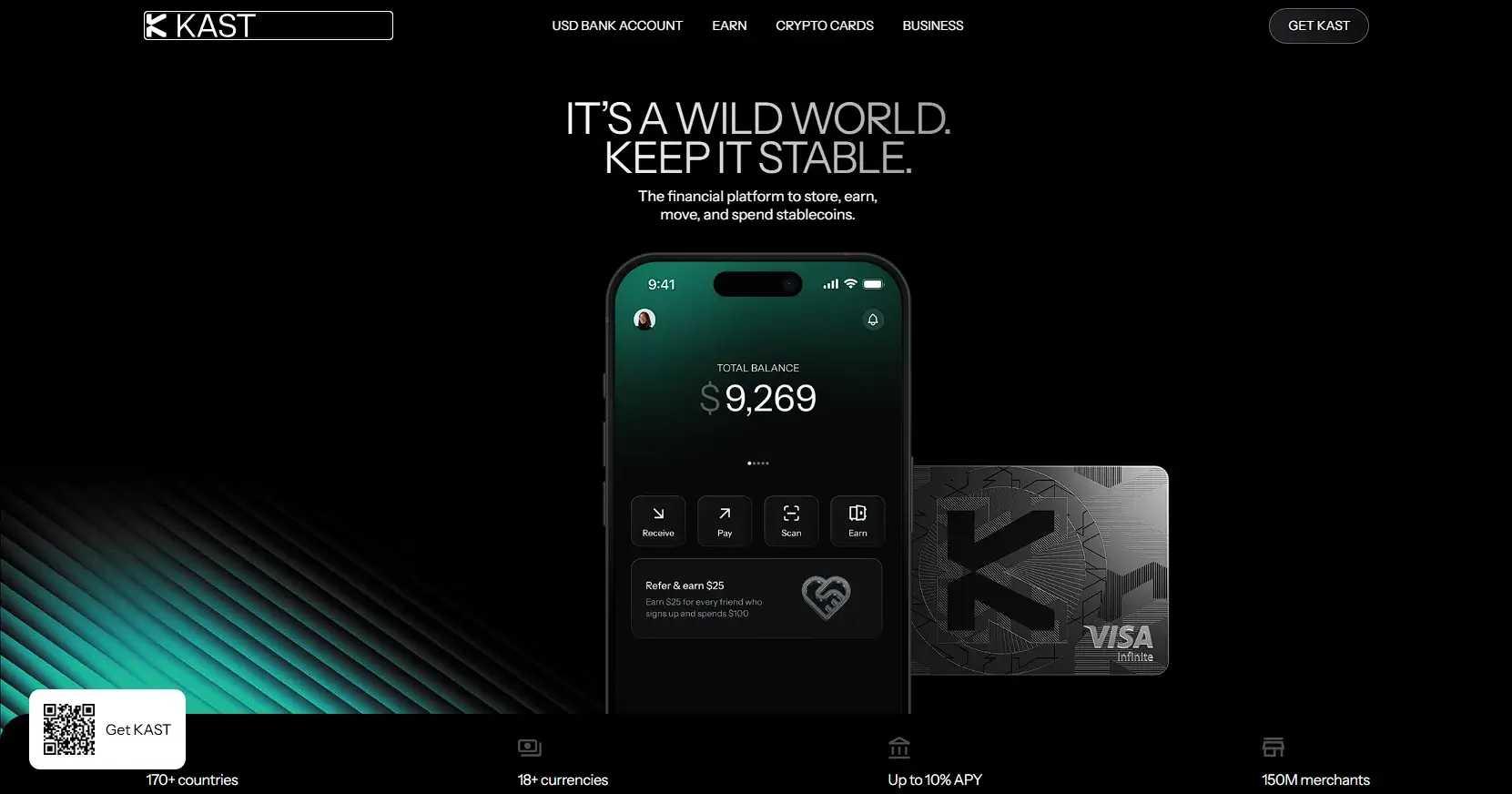

Kast Card Overview

Additional details

Kast Card Screenshots

Kast Card Pros and Cons

Pros

- 1.5% USD cashback on the free tier

- Stablecoins load 1:1 with no spread

- Virtual card minutes after a two-minute KYC

- US-available, unlike most crypto cards

- Five stablecoins across major chains

Cons

- Volatile crypto is sold on deposit at 2%–5%

- Free-tier cashback stops at $2,000 a month

- ATM cash costs $3 + 2%, capped at $750 a day

- Top cashback rates cost $1,000–$10,000 a year

- Custodial USD balance, no self-custody

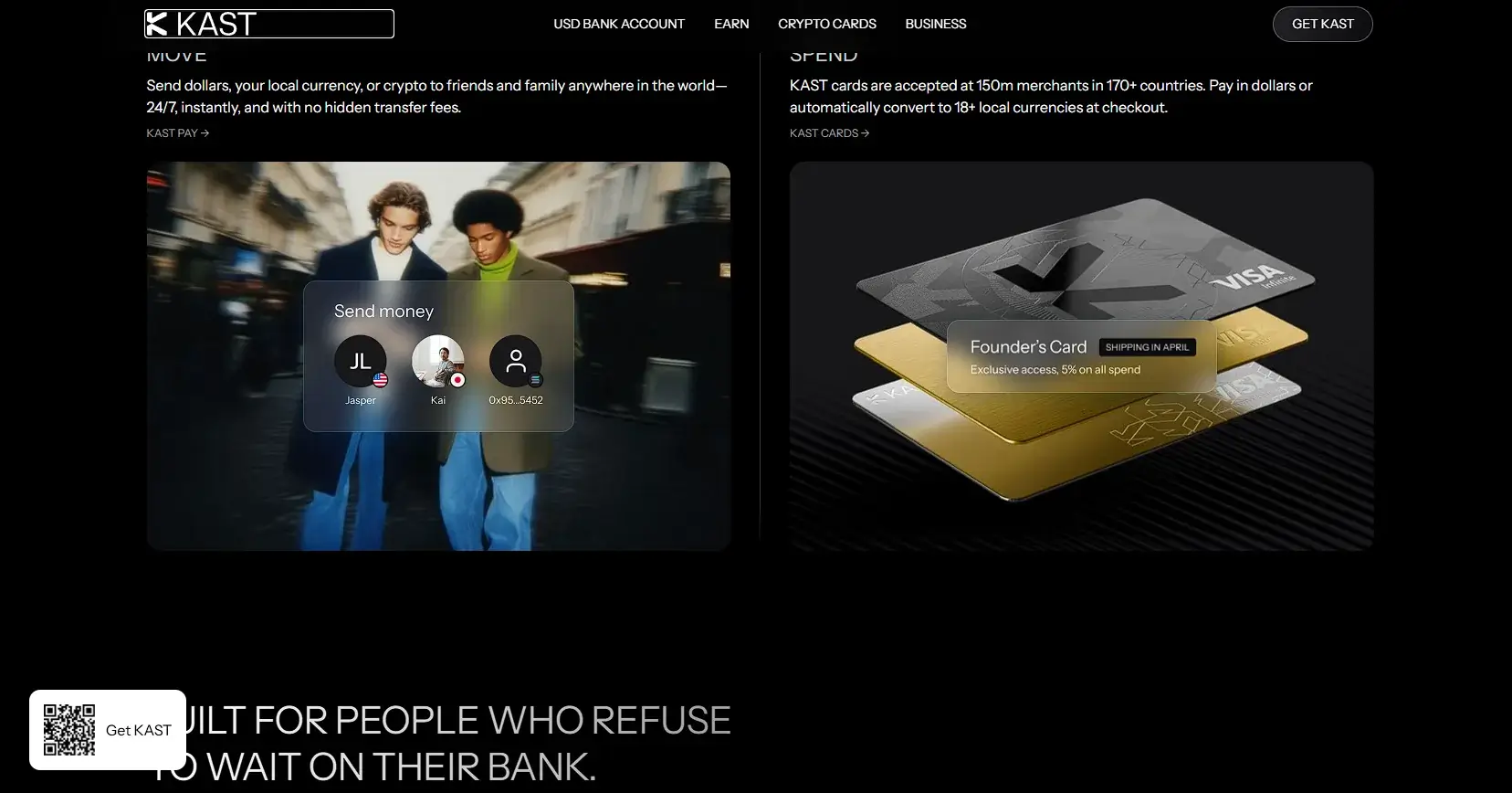

What This Card Actually Is and How Spending Works

KAST is a preload card. You deposit crypto first, the balance converts to USD, and the Visa spends that balance. The funding model splits into two paths with very different costs. Stablecoins (USDT, USDC, USDe, PYUSD, RLUSD) credit 1:1 with a 0% deposit fee. Volatile coins (BTC, ETH, SOL, XRP, BNB) are sold to KAST the moment they arrive, at a 2%–5% conversion rate that varies by token.

Custody sits with KAST throughout. Deposited crypto is treated as sold on entry, so there is no self-custody fallback, and the volatile path is a taxable disposal before a single purchase happens. Once funded, the card behaves like any USD prepaid Visa: it passes KYC, issues a virtual card within minutes, and links to Apple Pay and Google Pay immediately.

Who KAST Is Best For — And Who Should Skip It

The card suits people who hold stablecoins and want to spend them at Visa merchants without an off-ramp to a bank. A US resident, or anyone in the 170+ supported markets, gets a free card, a 0% loading rail, and 1.5% back in dollars for no annual cost. Users paid in USDT or USDC, from freelancers to remote workers banking around a weak local currency, fit the product exactly.

It fits badly for anyone holding mostly BTC or ETH, because the 2%–5% sale on deposit erases years of cashback before spending starts. Heavy cash users hit the $750-a-day ATM ceiling and the $3 + 2% fee on every withdrawal. Residents of the 49 restricted markets, including Canada, Australia, and Japan, cannot open an account at all.

Rewards Mechanics

The realized reward on the free tier is 1.5% cashback, paid in USD to the card balance, on the first $2,000 of card spend each month. That works out to a maximum of $30 a month, or $360 a year, at zero annual cost. There is no token lockup, no seasonal multiplier, and no volatile payout asset behind the headline number.

| Element | Value | Notes |

|---|---|---|

| Base rate (Standard) | 1.5% cashback in USD | Free tier, on the first $2,000 of monthly card spend, up to $30/month or $360/year |

| Top rates | Premium 2% on up to $10,000/month · Private 3% on up to $40,000/month | Premium $1,000/year, Private $10,000/year |

| Reward currency | USD, paid to the card balance | No volatile payout asset |

| Payout cadence | Per eligible spend | No token lockup, no seasonal multiplier |

| Caps and minimums | Standard $2,000/month · Premium $10,000/month · Private $40,000/month | Caps on rewarded monthly spend |

| Secondary layer | KAST Points on paid tiers, 1% Premium and 2% Private | Convertible toward the MOVE token |

Premium ($1,000 a year) lifts the rate to 2% on up to $10,000 of monthly spend, and Private ($10,000 a year) pays 3% on up to $40,000. Both paid tiers add KAST Points on top (1% and 2% on eligible spend) and both come on a Visa Infinite card with up to $1.5 million in travel accident insurance, purchase and price protection, and access to 1,200+ airport lounges. The math gates the paid tiers to heavy spenders: Premium only beats Standard above roughly $5,700 of monthly card spend, and Private only beats Premium above roughly $32,000 a month, counting cashback alone.

KAST Points are the secondary layer, convertible toward the MOVE token, and belong in the bonus column when comparing cards. The retired structure (Limited and Luxe cards, and the Season 5 points rates of 2%–8% that ended March 31, 2026) is gone, and older writeups quoting an 8% headline describe a product KAST no longer sells.

Fees and Pricing

The free tier costs nothing to open and nothing per year, and the stablecoin loading rail is the one part of the card that stays at 0%. The costs sit around that core:

| Fee or charge | Amount / rate | When it applies | Notes |

|---|---|---|---|

| Membership | $0 Standard · $1,000/yr Premium · $10,000/yr Private | Ongoing | |

| Card spend in USD | 0% | USD purchases | |

| FX fee | 0.5%–1.75% | Non-USD spend | |

| ATM | $3 + 2% per withdrawal | Cash withdrawal | Plus the FX fee on non-USD cash and any operator charge |

| Volatile-crypto deposit | 2%–5% auto-conversion | BTC, ETH, SOL, XRP, BNB deposits | Varies by token |

| Fiat top-up | $2 by ACH · $15 by FedWire | Fiat deposit | Stablecoin deposits free |

| Physical card | $40 shipping on Standard, included with Premium and Private | Card issuance | 7–10 business days |

| Virtual cards | First two free on Standard, then $2 each | Card issuance | |

| Small non-USD transactions | $0.10 | Purchases under $25 | |

| Declined transaction | $0.50 | Insufficient balance | |

| Inactivity | $1 a month | After 12 months dormant | |

| Stablecoin withdrawal | $0.20–$6 plus 0.1% | On-chain withdrawal | Depends on network, $5 minimum |

Fund with stablecoins and spend in USD, and the card runs close to free while paying 1.5%. The drag concentrates in three places: foreign-currency spend, ATM cash, and volatile-crypto funding. A $1,000 BTC deposit can lose $20–$50 before it becomes balance, which is the single most expensive line on this list.

Limits, Purchase and ATM

Card spending has no published ceiling — KAST applies no card transaction limit and no deposit or balance cap, so large purchases clear without tier upgrades. Cashback caps are the binding numbers instead: $2,000 of rewarded monthly spend on Standard, $10,000 on Premium, $40,000 on Private. Spend past the cap still works, it just earns nothing.

ATM access is tight. Withdrawals cap at $250 each, with a maximum of three withdrawals or $750 per rolling 24 hours, and every one costs $3 + 2% before operator fees. Anyone planning regular ATM use should price that ceiling first.

| Limit | Amount | Notes |

|---|---|---|

| Card spending | No published ceiling | No card transaction limit, no deposit or balance cap |

| Cashback caps (rewarded monthly spend) | Standard $2,000 · Premium $10,000 · Private $40,000 | Spend past the cap still works, it earns nothing |

| ATM per withdrawal | $250 | Costs $3 + 2% before operator fees |

| ATM per rolling 24 hours | Three withdrawals or $750 |

Eligibility and Availability

KAST is live in 170+ countries and open to new applicants, including US residents — the app issues virtual US bank account numbers for receiving ACH and FedWire payments, with some state-level limits on that banking feature shown in-app. Signup takes minutes:

- Download the app and register.

- Pass Sumsub KYC with a government ID and a selfie, about two minutes, no credit check.

- Receive the virtual card within minutes of approval.

- Order a physical card if wanted ($40 shipping on Standard, 7–10 business days).

Physical delivery has its own coverage list of about 180 markets, including the US, UK, and Hong Kong. If KAST does not ship to a country, the virtual card and wallet features are the product there.

Restricted Countries

KAST publishes country eligibility only inside its signup flow, and the terms reserve the right to change “Restricted Locations” without notice. The list below is compiled from KAST's terms, its published card-shipping coverage, and third-party card listings, not from a single issuer page. Confirm in-app before planning around it.

Singapore is absent from KAST's shipping coverage and marked unsupported by multiple 2026 sources, so it is treated as restricted here. Hong Kong appears on KAST's own shipping list and is treated as supported, though one third-party listing disputes it.

Funding Rails

Five stablecoins load at 1:1 with no deposit fee. USDT and USDC are supported across major chains, so picking a cheap network (such as TRON or Solana) keeps the entire loading cost at the chain fee. KAST supports a wide network set overall; confirm the exact chain for any given coin in-app before depositing, since sending on an unsupported network risks loss.

The volatile path is a different product. BTC, ETH, SOL, XRP, and BNB deposits are sold to KAST on arrival at 2%–5%, the position is gone, and the sale is a taxable event in most jurisdictions. Fiat comes in by ACH ($2) or FedWire ($15) through the US virtual account numbers, and stablecoins go back out on-chain for $0.20–$6 plus 0.1% depending on network.

Security, Custody, and Freeze Risk

The balance is custodial. KAST holds the USD value, deposited crypto is treated as sold on entry, and recoverability rests on KAST and its banking partners with no self-custody exit. The Global Account runs on Bridge with banking through Lead Bank, Member FDIC — that coverage applies to the banking rails, and KAST's digital-asset balance itself is not FDIC-insured. The card issuer is named: the cardholder agreement states that the issuer for the card program is Third National.

The corporate structure is the other trust input. The app operator is KAST Tech, incorporated in Anjouan, Comoros, while the cardholder agreement names Troia Corp as the card-program entity. No documented pattern of frozen balances or stuck withdrawals surfaced during the audit period, which puts KAST ahead of the gray-market end of this market. The issuer being disclosed strengthens the custody picture, but the offshore KAST Tech/Troia structure and the uninsured digital-asset balance keep it at adequate-and-disclosed rather than proven.

UX, App, and Support

The app covers the full loop: KYC, virtual card issuance in minutes, card freezes, Apple Pay and Google Pay linking, stablecoin deposits and withdrawals, and free instant transfers to other KAST users (up to $10,000 a day). Physical cards upgrade the form factor by tier, from plastic on Standard to metal and a gold card on Private.

Support is in-app and web-based, with 24/7 concierge coverage advertised. The unproven part is the one that decides custodial cards: the dispute and frozen-account path. KAST does not disclose chargeback fees or dispute timelines, so test support with a small balance before loading meaningful money.

Tax and Record-Keeping

The preload model keeps everyday spending simple. The card spends a USD balance, so purchases do not sell a crypto position, and stablecoin deposits convert at 1:1 with negligible gain or loss to report. The tax event lives at the funding step: every BTC, ETH, SOL, XRP, or BNB deposit is a disposal at the moment KAST buys it, and cashback may count as income depending on jurisdiction.

KAST does not disclose CSV export, cost-basis tracking, or tax-software integration. Cardholders reconciling disposals from volatile-crypto deposits need to keep their own records of what was sent and the USD value credited.

Final Verdict

KAST does one job precisely: it turns a stablecoin balance into a spendable USD Visa at 1:1 with no spread, in 170+ countries including the US, with a virtual card minutes after a two-minute KYC and 1.5% back in dollars on a free membership. That is the product sold today, re-scored on the May 2026 membership model — the 8% points headlines attached to the retired Limited and Luxe cards are history. The free tier's cashback caps out at $30 a month. The cost drag outside the stablecoin lane (0.5%–1.75% FX, $3 + 2% ATM cash, 2%–5% on volatile-crypto deposits) is real money for travelers and BTC holders. And the custody stack, with an Anjouan-incorporated app operator (KAST Tech) and the card program run through Troia Corp, asks for more trust than an onshore, insured setup — even with the issuer, Third National, now named in the cardholder agreement. Fund it with stablecoins, spend it in dollars, and the card costs almost nothing to hold while paying 1.5%. Fund it with anything else and the fees eat the pitch.

Virtual US bank numbers for ACH and wires, Free instant transfers to other KAST users, No card spending ceiling, USD spend at 0%

Why it stands out

- 1.5% USD cashback on the free tier

- Stablecoins load 1:1 with no spread

- Virtual card minutes after a two-minute KYC

- US-available, unlike most crypto cards

- Five stablecoins across major chains

What to consider

- Volatile crypto is sold on deposit at 2%–5%

- Free-tier cashback stops at $2,000 a month

- ATM cash costs $3 + 2%, capped at $750 a day

- Top cashback rates cost $1,000–$10,000 a year

- Custodial USD balance, no self-custody

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.