Crypto censorship resistance is questioned as major fight breaks out over who gets to freeze your digital dollars

Circle says freezes should follow lawful process. Tether is proving the appeal of fast intervention. After Drift and Rhea, stablecoin users may care more about stopping thieves than old crypto slogans.

Crypto rhetoric has long prized the ability to transact without gatekeepers, to move value across borders without asking permission, and to hold assets no institution could seize.

Crypto culture treated these as design virtues, properties that builders embedded with ethical weight by deliberate architectural choice. Then the Drift exploit happened, and the backlash told a different story.

On Apr. 1, Drift suffered a major exploit. Circle later described the publicly reported losses as exceeding $270 million, while other reports put the figure around $285 million and documented criticism that Circle had not frozen stolen USDC as it moved across its cross-chain rails.

The attacker routed roughly $232 million in USDC from Solana to Ethereum using Circle's Cross-Chain Transfer Protocol. The backlash stemmed from users and observers wanting to know why Circle had not intervened sooner.

Days later, Tether CEO Paolo Ardoino posted that Tether had frozen 3.29 million USDT tied to the Rhea Finance attacker, framing the intervention as proof that “Tether cares.”

The contrast landed hard.

Two responses, two philosophies

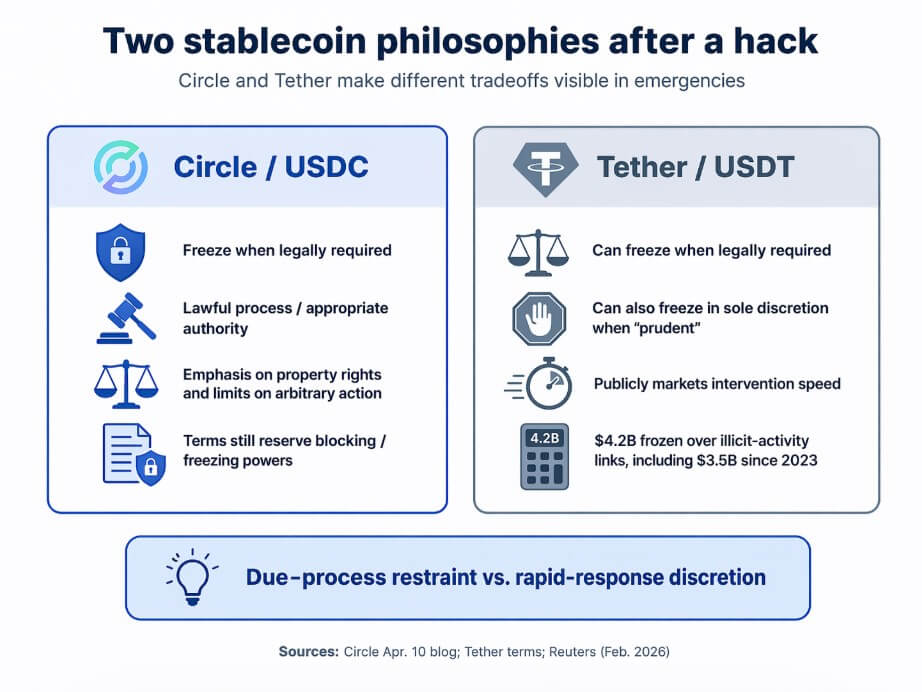

Circle published its formal response on Apr. 10, and its core argument was that USDC freezes occur when the law requires action. Circle is legally compelled by an appropriate authority through a lawful process.

Circle pushed back on the idea that an issuer should act as an ad hoc chain police force, arguing that open access to permissionless infrastructure is a feature, and that the bigger problem is that legal frameworks have not yet kept pace with the speed of on-chain exploits.

The stablecoin issuer also made a property-rights argument, claiming that arbitrary freezes set dangerous precedents for lawful users, and the power to freeze is a compliance obligation, constrained by lawful process and legal compulsion, authorized only through formal legal channels.

The complication is that Circle's own legal documents tell a more layered story.

USDC terms state that transfers are irreversible and that Circle carries no obligation to track or determine the provenance of balances.

Those same terms also reserve Circle's right to block certain addresses and, for Circle-custodied balances, freeze associated USDC in its sole discretion when it believes those addresses may be tied to illegal activity or terms violations.

Circle holds meaningful freeze power and frames it as a tightly bound compliance function, constrained by legal process and compulsion.

Ardoino's Rhea post was a boast, and Tether's terms grant it broad discretion by stating that the company may freeze tokens as required by law or whenever it determines, in its sole discretion, that doing so is prudent, and authorizing it to blacklist token addresses.

In February, Tether froze approximately $4.2 billion in USDT due to links to illicit activity, with $3.5 billion of that since 2023.

The feature nobody advertised

What Drift and Rhea forced into the open is a question that stablecoin competition had not yet fully surfaced: in a hack, what do users actually want from an issuer?

The anti-censorship instincts that shaped crypto's early culture tend to lose their force the moment users need an emergency brake. Affected protocols, exchanges holding stolen funds, and victims watching their balances drain want to know who can stop the thief.

That reframes freeze capacity as more of a consumer-protection feature.

Tether has been accumulating a record of intervention and visibility. Ardoino's Rhea post was designed to be read as a product statement, and in the context of a fresh exploit, it worked.

The emotional and practical logic is accessible, showing that one issuer froze stolen funds the same day an attacker moved them, while another issuer said legal timelines tied its hands.

This makes optics difficult for Circle regardless of the legal merits of its position.

Stablecoins are quietly differentiating themselves in emergency governance, alongside reserve composition and exchange liquidity.

The cost of the feature

The case for Circle's position is real and does not require dismissing the Drift backlash to hold. Broad issuer discretion over freezes creates risks that extend far beyond hack scenarios.

An issuer that can freeze tokens in its sole discretion when it determines it is prudent can freeze tokens for reasons unrelated to protecting victims. Politically contentious addresses, disputed transactions, regulatory scrutiny from a single jurisdiction, or simple operational error can all trigger freezes under terms as broad as Tether's.

The same capacity that lets an issuer stop a thief also lets it stop a protester, a dissident from a sanctioned country, or a business whose activity it finds inconvenient.

Circle's public writing on the Drift exploit is, among other things, a defense against that risk. The argument that emergency intervention needs new legal frameworks and safe-harbor structures is also an argument that the current situation is a problem, even when the targets are criminals.

The absence of defined standards means an issuer can act generously today and overreach tomorrow, with no formal mechanism to distinguish the two.

Tether's freeze record has not yet produced a major documented wrongful-freeze controversy, but that record is also vast and not fully transparent.

Reports on the $4.2 billion in frozen USDT withhold the details of each decision, the legal process underlying each freeze, and the error rate across thousands of enforcement actions.

Fast intervention looks different in the abstract when the process generating those interventions is opaque.

| Benefit of fast freezes | Cost of broad freeze discretion |

|---|---|

| Can slow or stop stolen funds | Can enable arbitrary intervention |

| May improve recovery odds | Can affect lawful users |

| Helps exchanges/protocols in crises | Can reflect political or regulatory pressure |

| Looks like consumer protection in hacks | Process may be opaque |

| Becomes a due-diligence feature | Wrongful-freeze risk may be hard to challenge |

Two paths from here

The bull case for intervention-first issuers runs in a world where hacks keep coming, and recoverability keeps rising on the priority list.

More regulatory scrutiny on exchanges to show they take asset protection seriously, and more institutional users who need to demonstrate due diligence in custody and recovery. These are factors that push emergency freeze capacity to the center of stablecoin evaluation.

In that scenario, Tether's public freeze record and broad discretionary terms become genuine competitive assets. Exchanges and protocols that have experienced exploits now treat fast-intervention capacity as a due diligence criterion when choosing which stablecoin to hold as primary liquidity.

Circle has to either act faster through new legal mechanisms or accept that some market segments will treat its rule-of-law posture as a liability in crises. Ardoino's Rhea post, in retrospect, looks like an early entry in a competition that the market eventually formalizes.

The bear case for that same model runs through wrongful freezes, regulatory backlash, and the discovery that broad discretion is often a liability as much as a virtue.

A high-profile incorrect freeze, such as an address flagged as malicious that belongs to a legitimate user, a jurisdiction-specific enforcement action that appears to be politically targeted at users in other markets, or an operational error that freezes clean funds during a market stress event, turns the same emergency-governance story toxic.

In that world, Circle's insistence on lawful process and defined standards looks like principled restraint, a deliberate commitment to defined limits over speed, and users place a real premium on an issuer whose freeze decisions carry formal accountability.

The crypto community's historical skepticism toward centralized control reasserts itself as hard-won practical wisdom, grounded in the documented costs of unchecked issuer discretion.

The stablecoin winners in that scenario are the ones whose intervention power is real but bounded. Issuers who can act in genuine emergencies and demonstrate they held back in ambiguous ones.

As stablecoins deepen their role in institutional payments, treasury workflows, and regulated financial infrastructure, governance under stress becomes as material as reserve quality or distribution reach.

The question that Drift and Rhea put on the table of how much control users want an issuer to have has no clean universal answer. Institutions with large exposures and recovery obligations may want emergency brakes, while individuals holding stablecoins across politically sensitive jurisdictions may want the opposite.

Protocols with mixed user bases need to answer for both.

The real contest now is for the version of stablecoin governance that earns enough trust from enough users to become the default.