Buying crypto with a card is convenient, but convenience usually comes at a price. Credit and debit cards let users fund an account quickly and start trading without waiting for a bank transfer to clear, which is one reason they remain popular with first-time buyers. The trade-off is that card purchases often carry higher all-in costs through platform fees, wider spreads, or both.

That makes card funding best suited to speed and simplicity rather than low-cost accumulation. Readers comparing exchanges should look closely at card availability, supported regions, settlement speed, and the real cost of a transaction, not just whether a platform says it accepts cards.

Buying Crypto With a Credit Card

Buying crypto with credit card support can be useful when speed matters and a bank transfer is too slow. On some exchanges, credit cards work as a fast on-ramp for smaller purchases, especially for users who want quick access to Bitcoin, Ethereum, or stablecoins without moving funds through a separate banking flow.

The downside is that credit card purchases are often one of the most expensive ways to buy crypto. Some issuers also treat crypto purchases as cash-like transactions, which can lead to declines, extra charges, or restrictions that come from the bank rather than the exchange itself. That is one reason purchase crypto with credit card intent should always be paired with a fee check before confirming the order.

Buying Crypto With a Debit Card

Buying crypto with debit card support is usually more widely available than credit card funding, and for many casual users it is the simplest path from fiat to crypto. Debit cards are commonly used for quick purchases, smaller top-ups, and first-time account funding because approval flows are often more straightforward than with credit cards.

Even so, debit card fees and transaction limits can still vary meaningfully between exchanges. Some platforms cap first purchases, apply extra verification steps, or restrict card funding in specific regions. Debit is often the more practical card option, but it still pays to compare the final checkout price against a bank transfer before buying.

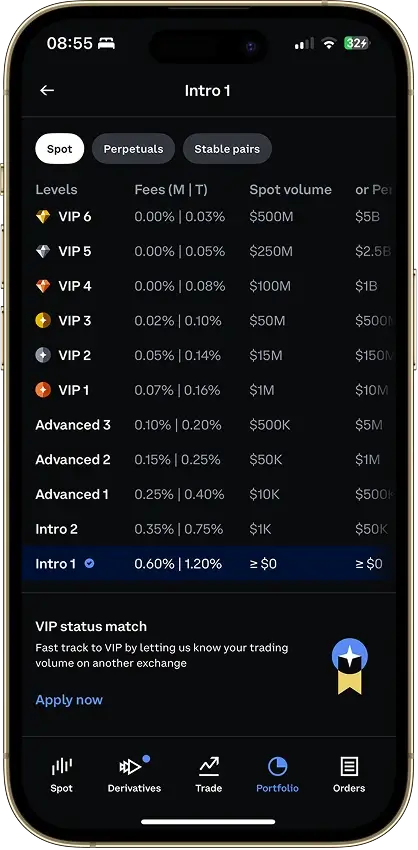

Card Fees, Limits, and Decline Reasons

Card transactions can fail for reasons that are not always obvious at first glance. On many exchanges, crypto or fiat withdrawals may be temporarily restricted after a card purchase while the payment settles. These holds vary by platform and payment provider, and they can last anywhere from minutes to several days depending on the exchange’s risk controls.

Other common issues include issuer restrictions, regional blocks, verification friction, fraud checks, and temporary holds triggered by unusual transaction patterns. In other cases, the exchange supports card buying in principle, but the card network, country, or account state prevents the payment from going through.

Limits matter too. Some exchanges allow only modest first-time card purchases before additional checks are completed, while others increase card limits after account verification or transaction history builds over time. For readers weighing convenience against cost, the key question is not just whether card funding works, but how reliably it works in their region and at what total price.

| Funding method | Speed | Cost | Convenience | Typical limits |

|---|

| Card funding | Usually fast | Usually highest | Very convenient | Often tighter at first |

| Bank transfer | Slower | Usually lowest | Less instant, but practical for larger buys | Often higher once verified |

| Wallet transfer | Fast after network confirmation | Varies by network | Best for users who already hold crypto | Depends on asset and network |

For most readers, the simplest rule is this: use cards when speed and ease matter most, and use bank transfers when cost matters more. Wallet transfers sit in the middle and are often the most efficient choice for users who already have crypto elsewhere.