RedotPay Overview

Additional details

RedotPay Screenshots

RedotPay Pros and Cons

Pros

- No monthly or annual fee

- 1.2% FX fee beats most prepaid rivals

- Virtual card live minutes after KYC

- Fireblocks custody, segregated addresses

- Spends in 100+ countries

Cons

- No cashback or ongoing rewards

- Non-refundable 10/100 USDT issuance fees

- 2–3% ATM fees, physical card only

- $50 chargeback fee, 3–6 month waits

- Blocked in the US and 41 other markets

Who RedotPay Is Best For — And Who Should Skip It

The card suits stablecoin holders outside the US who want spending, transfers, and swaps in one app. Users who deposit USDT on-chain and spend in the card currency pay nothing recurring after the one-time issuance fee, which is the cheapest way to keep a stablecoin balance spendable at Visa merchants.

It fails anyone comparing on rewards, because the earn rate is zero. Self-custody users lose control the moment funds land with the custodian, with no on-card fallback to withdraw independently. Heavy ATM users pay 2–3% per withdrawal, and anyone who values a disclosed issuing bank will find the trust picture incomplete.

What This Card Actually Is and How Spending Works

RedotPay is a preload card. You top up an app-held balance first (on-chain stablecoin, an exchange transfer, a EUR/GBP bank transfer, or a card payment), and every purchase draws from that balance. Conversion to fiat happens at settlement, so no crypto position is force-sold at each purchase — the entry cost sits in the top-up spread instead, which ranges from 0% on-chain to 3% by credit card.

The app bundles the card with a wallet, transfers, swaps, P2P trading, and an optional crypto-backed credit feature. That credit product is separate from the card, which extends no credit line of its own. Merchant refunds return to the app balance once processed.

Rewards Mechanics

The realized reward rate is 0%. There is no cashback tier, no travel perk, and no subscription that unlocks an earn rate. RedotPay pays two one-off incentives: a $5 USDT sign-up bonus that expires after 30 days and cannot offset the issuance fee, and USDT referral commissions for recruiting new users.

| Element | Value | Notes |

|---|---|---|

| Base rate | 0% | No cashback tier, travel perk, or subscription earn rate |

| Top rate | 0% | No subscription or tier unlocks an earn rate |

| Reward currency | USDT | Used for the sign-up bonus and referral commissions |

| Payout cadence | One-off only | Two one-time incentives, no ongoing accrual |

| Caps/minimums | $5 USDT sign-up bonus | Expires after 30 days, cannot offset the issuance fee |

| Exclusions | All ongoing spend | No cashback on any category |

The cost of that zero is easy to price. A cardholder putting $500 a month through a 2%-cashback competitor collects $120 a year, and RedotPay pays none of it. Treat the card as a spend tool priced on fees, and skip it if rewards drive the decision.

Fees and Pricing

The recurring cost is $0 — no monthly, annual, or dormancy fee. Everything else is transactional:

| Fee or charge | Amount / rate | When it applies | Notes |

|---|---|---|---|

| Virtual card issuance | 10 USDT | On ordering the virtual card | Non-refundable |

| Physical card issuance | 100 USDT | On ordering the physical card | Non-refundable |

| Virtual card replacement | $5 first, $10 after | On replacement | Minimum 31 days apart, card deletion $2 |

| FX fee | 1.2% | Spend outside the card currency | Includes foreign-currency ATM withdrawals |

| ATM withdrawal | 2% up to $10,000/month, 3% above | Cash withdrawal | Foreign-currency withdrawals also incur the 1.2% FX fee |

| Selected merchant categories | 1.5%, $0.50 minimum | Some ad platforms and gaming top-ups | After three monthly waivers |

| Top-ups | Free / 1% / 3% ($1 minimum) | Funding the balance | Free by EUR/GBP bank transfer or on-chain deposit, 1% via Binance Pay, 3% via credit/debit card or PayPal |

| Chargeback | $50 | Per chargeback request |

Both issuance fees are denominated in USDT, so at the peg they track $10 and $100 but are paid in stablecoin. The cheap path is on-chain USDT in, card-currency spend out — after issuance, that route costs only the deposit's network fee. The expensive path stacks quickly: a $500 credit-card top-up loses $15 before the first purchase, cross-currency spend adds 1.2%, and ATM cash runs 2–3% depending on monthly volume.

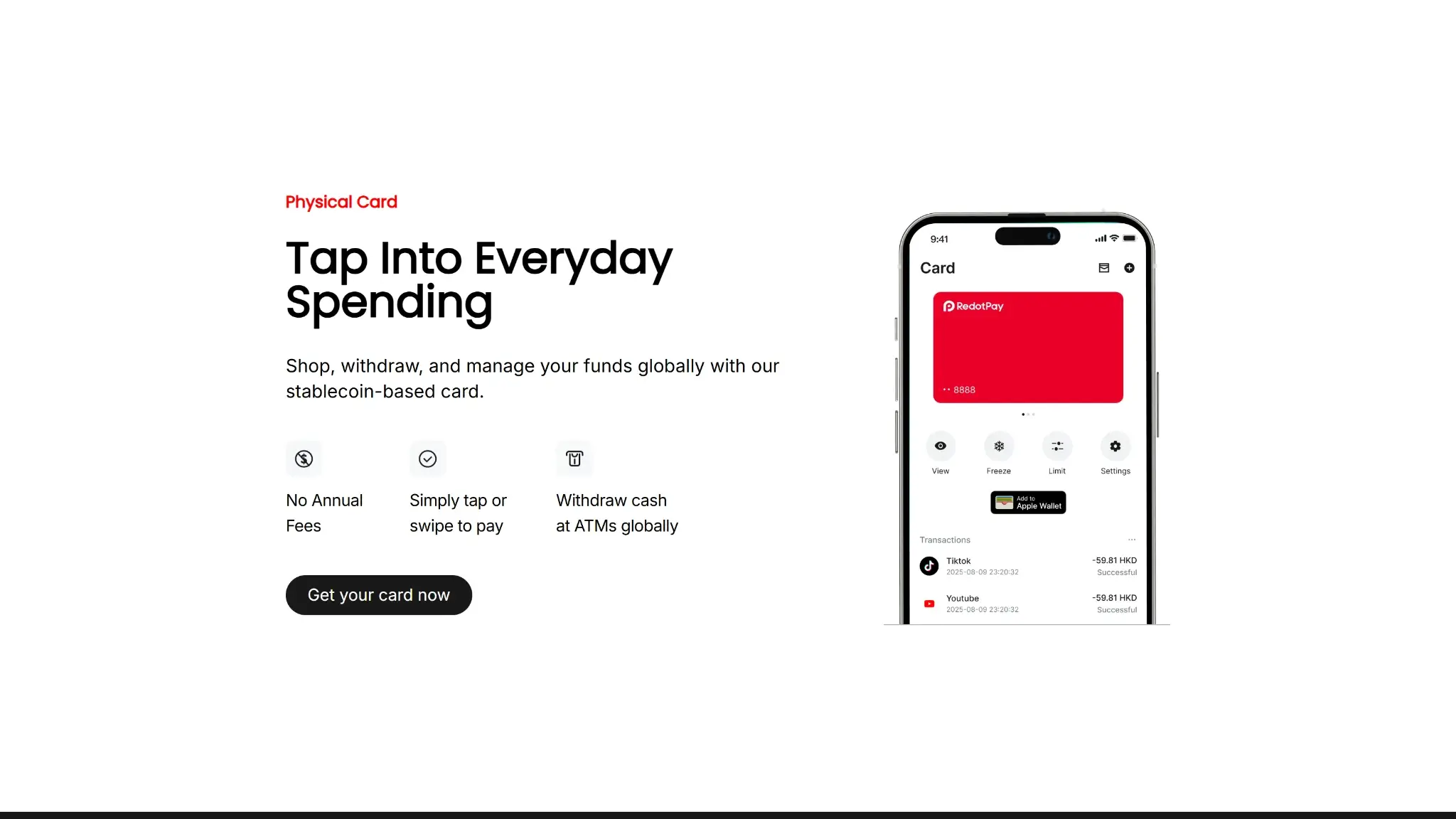

Limits, Purchase and ATM

RedotPay does not disclose a standard spend ceiling. Limits are set per card inside the app, and a security-triggered restriction caps spending at $1,000 per transaction and $1,000 per day for 24 hours. ATM access requires the physical card, priced at the 2–3% tiers above, and ATM operators can add their own charge on top.

| Limit | Amount | Notes |

|---|---|---|

| Standard spend ceiling | Not disclosed | Limits set per card inside the app |

| Security-triggered restriction (per transaction) | $1,000 | Applies for 24 hours |

| Security-triggered restriction (per day) | $1,000 | Applies for 24 hours |

| ATM access | Physical card only | Priced at the 2–3% tiers above, ATM operators can add their own charge |

Timing is quick on the way in and slower on the way back. Crypto deposits clear in 1–15 minutes, and EUR/GBP transfers land in about five minutes unless flagged for review, which stretches to 1–3 business days. Merchant refunds take 2–15 days after processing, occasionally beyond a month for some e-commerce cases, and reversals settle in 1–5 days.

Eligibility and Availability

RedotPay accepts applicants from 100+ countries, with the exact service layer (registration, card issuance, delivery) varying by market. KYC is mandatory before any feature unlocks: an ID document plus a face scan, processed by Sumsub, with one verified account per person and no credit check.

Setup follows one path:

- Download the app and register an account.

- Complete KYC with an ID document and face scan.

- Fund the balance with at least the issuance fee.

- Order the virtual (10 USDT) or physical (100 USDT) card.

The virtual card activates about 5–10 minutes after approval and funding. The physical card takes 10–15 days to produce plus 5–30 days to ship.

Restricted Countries

US residents cannot pass KYC or use RedotPay at all. The issuer publishes the full exclusion list, reproduced here in full because it decides eligibility outright:

- Afghanistan

- Albania

- Belarus

- Bosnia and Herzegovina

- Bouvet Island

- Burkina Faso

- Burundi

- Central African Republic

- Congo (Democratic Republic of the)

- Croatia

- Cuba

- Eritrea

- Ethiopia

- Guinea-Bissau

- Haiti

- Iran

- Iraq

- Kosovo

- Lebanon

- Liberia

- Libya

- Mainland China

- Mali

- Montenegro

- Myanmar

- Netherlands Antilles

- Nicaragua

- North Korea

- North Macedonia

- Russia

- Serbia

- Singapore (residents ineligible for virtual and physical cards; cannot register a billing address)

- Slovenia

- Somalia

- South Sudan

- Sudan

- Syria

- Ukraine

- United States

- Venezuela

- Yemen

- Zimbabwe

RedotPay notes the list may change as regulations evolve, so applicants in borderline markets should confirm in-app before paying an issuance fee.

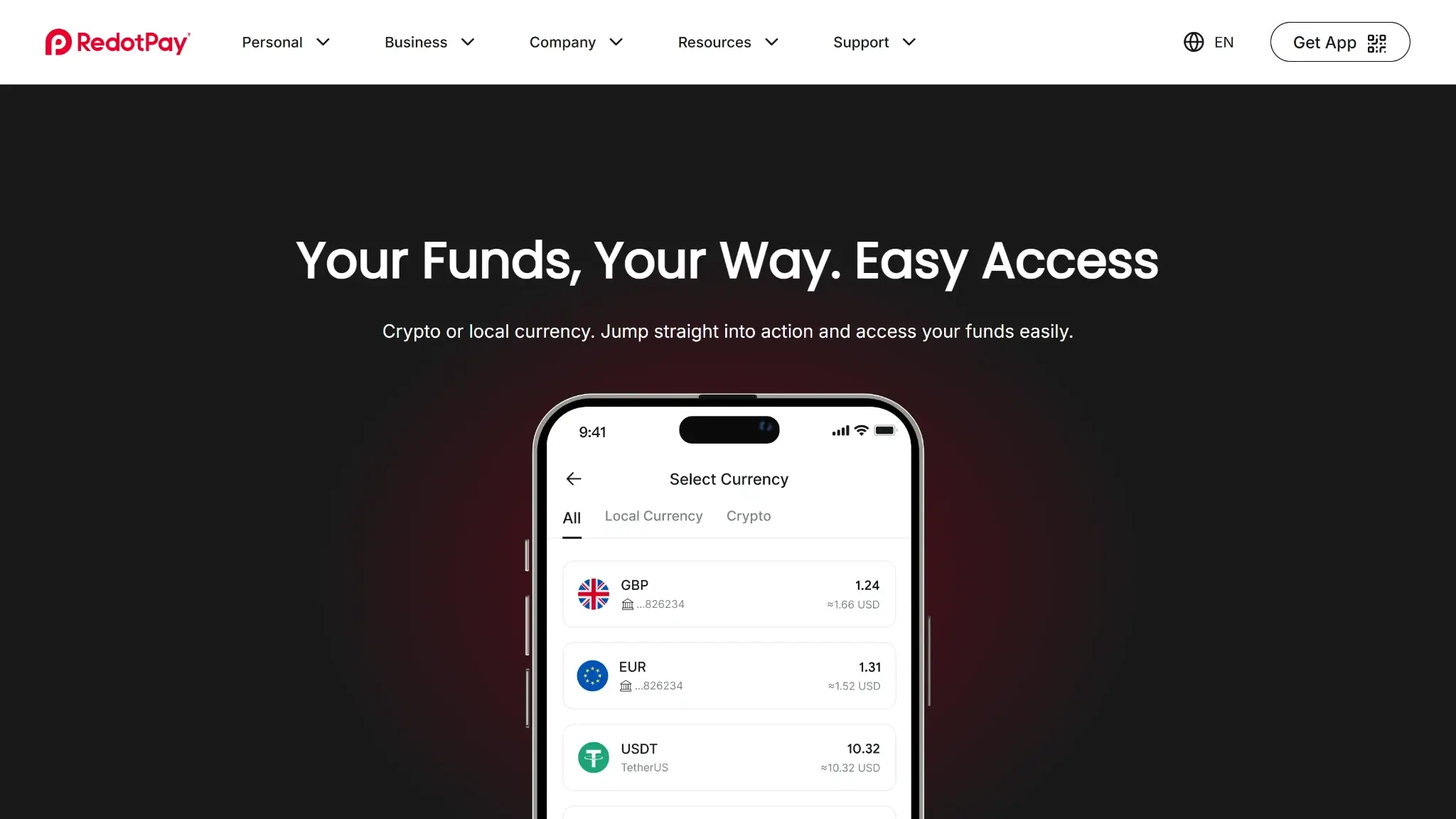

Funding Rails

Core deposit assets are USDT, USDC, BTC, and ETH, with app balances also held in BNB, SOL, TON, TRX, and XRP. Stablecoin deposits ride ERC20, BEP20, or TRC20 — USDT on TRC20 clears in about five one-minute confirmations and is the lowest-cost route in.

Because the model is preload, funding is where conversion happens. A stablecoin deposit matches settlement 1:1 with no spread, while card and PayPal top-ups price convenience at 3% and Binance Pay at 1%. EUR/GBP bank transfers through a currency account are free. Spending itself triggers no forced sale of a volatile position, which keeps per-purchase tax exposure lower than auto-sell cards, though the fiat conversion at settlement can still count as disposing of the stablecoin (see Tax below).

Security, Custody and Trust

Custody is the best-documented part of the product. Funds sit on Fireblocks institutional MPC infrastructure, with a segregated blockchain address assigned per user that separates card funds from the platform wallet. Sumsub handles identity checks, Beosin provides transaction monitoring (KYT — know your transaction), and the operating entity holds a Hong Kong license alongside a FinCEN MSB registration. That US registration covers internal and cross-border operations only, and grants no access to US residents.

Two gaps keep the trust picture mid-tier. RedotPay does not disclose its issuing bank or BIN sponsor, and it does not disclose deposit insurance or PCI-DSS certification, so treat balances as institutionally custodied but uninsured on the public record. The custodial model also carries the standard freeze exposure: a KYC or AML flag lets RedotPay and its partners refuse top-ups, restrict access, freeze a balance, and report activity, with no self-custody escape hatch.

UX, App, and Support

One app holds the card, wallet, transfers, swaps, and P2P, with per-card spending limits and freezes set by the user. Google Pay works in eligible regions. Apple Pay needs a closer look: after Apple's review of Hong Kong card programs, Apple Pay enablement was paused for cards issued after Aug. 22, 2025, and RedotPay has been restoring it through a free card upgrade rolling out since Jan. 15, 2026. Ordering today you may need to request that upgrade in-app before Apple Pay links.

Support runs through in-app live chat with a one-business-day response target, backed by a help center covering cards, transactions, refunds, fraud, and security. The dispute path is the weak point. Chargebacks must be filed within 60 days of settlement, cost $50 per request, and take 3–6 months to resolve, so on a small purchase the fee exceeds the amount in dispute. Support can freeze cards, take fraud reports, and produce billing statements, but cannot cancel merchant subscriptions or reverse completed internal transfers.

Tax and Record-Keeping

The app produces downloadable billing statements and monthly card history, and nothing more. There is no CSV export, no cost-basis tracking, and no disclosed tax-software integration, so reconciliation is manual. Because stablecoin converts to fiat at settlement, card spend can count as a taxable disposal in many jurisdictions, and the $5 sign-up bonus and referral commissions may be reportable income. Cardholders tracking gains need to log source assets, conversion values, and refunds themselves.

Final Verdict

The case for RedotPay is narrow and coherent: hold stablecoins outside the US, fund on-chain for free, and spend at Visa merchants for $0 a month with a 1.2% FX fee. Fireblocks custody with segregated per-user addresses gives the custodial model more substance than most prepaid rivals document. What holds the score at mid-tier is everything around that core. The card pays zero rewards, charges non-refundable 10/100 USDT issuance fees, prices ATM cash at 2–3%, bills $50 per chargeback, keeps its issuing bank undisclosed, and takes 1–3% on the convenient top-up rails. Spenders who avoid those edges get a cheap, functional stablecoin card. Everyone else is paying entry costs for a product that never pays anything back.

Free on-chain and EUR/GBP funding rails, No forced crypto sale at each purchase, Hong Kong-licensed, FinCEN MSB registered

Why it stands out

- No monthly or annual fee

- 1.2% FX fee beats most prepaid rivals

- Virtual card live minutes after KYC

- Fireblocks custody, segregated addresses

- Spends in 100+ countries

What to consider

- No cashback or ongoing rewards

- Non-refundable 10/100 USDT issuance fees

- 2–3% ATM fees, physical card only

- $50 chargeback fee, 3–6 month waits

- Blocked in the US and 41 other markets

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.