How DeFi lending can restructure older financial systems

Cryptocurrencies have opened new doors for finance and lending.

Photo by Armando Arauz on Unsplash

Since the inception of the world's first cryptocurrency, Bitcoin, we have seen innovations of all kinds – from stablecoins to full-blown decentralized finance projects. While stablecoins brought stability to highly volatile cryptos, DeFi introduced new ways to generate income. One such popular method is lending.

The onset of the pandemic has made people look for an investment option. DeFi lending presented the preposition of making money on crypto holdings without the traditional goalkeepers of loans. Instead of banks or other central entities, people could now choose a decentralized platform to borrow or lend loans. It resulted in the explosion of this new form of lending, with over $29 billion locked in different DeFi lending platforms.

In this article, we explore some of these lending protocols and find out how they work:

MakerDAO

Developed by Rune Christensen in 2018, MakerDAO is an organization building technology for lending and a stablecoin on the Ethereum network. It allows users with cryptos to lend themselves capital in a stablecoin called DAI. The platform is the top lending protocol on DeFi pulse, with over $10.11 billion of assets locked.

How It Works

Anyone can lock up cryptos in a smart contract to create a certain amount of DAI. These DAIs can then later be converted into fiat or exchanged for any other crypto asset. The more locked-up crypto, the more DAI one can take as a loan. To unlock the locked digital assets, users need to pay back their DAI loan along with MakerDAO's fees.

As most cryptocurrencies are volatile, when the price of a locked-up asset drops below a specific range, MakerDAO‘s protocol immediately sells off the collateral to pay back the borrowed DAI plus penalties and fees. This threat of liquidation keeps the project stable and ensures no one exploits the system. Whereas, when the price of a locked-up asset increases, users will get extra DAI.

In addition to DAI stablecoin, MakerDAO uses MKR tokens to govern its system and support the stability of DAI. DAI is created when someone takes out a loan, and MKR is created or burned depending on how close DAI is to its peg of $1. If DAI is stable, the protocol burns MKR to decrease the total supply. When DAI goes below the $1 peg, more MKR is issued, increasing the supply and maintaining stability of MakerDao’s lending protocol. In terms of utility, MKR holders can vote on the governance decisions of MakerDAO. Also, they get incentives for acting in the best interest of the protocol.

Compound

Invented by a former economist Robert Lishner, Compound has been leading lending protocol in the DeFi space. It enables borrowers to take out loans by collateralizing their cryptos and allows lenders to provide loans by locking up their digital assets. Compound may look like it works like other lending protocols, although it differentiates itself by tokenizing the assets locked in its system via cTokens.

How It Works

Similar to MakerDAO, Compound also uses crypto as collateral to lend out money. However, instead of DAI or some other token, Compound issues ERC-20 cTokens (or Compound Tokens) that represent users' funds locked up in its protocol. In simpler terms, when users deposit any crypto as collateral, they will get an equivalent amount of cTokens. For example, for putting up ETH, users will get cETH.

On the other hand, users can deposit their cryptos to earn interest. For example, for depositing ETH to generate interest on Compound, users receive cETH. Each asset locked up in the protocol has its value, and the amount of demand and supply of the underlying asset determines the interest rates to be received and paid by lenders and borrowers. Another unique factor of Compound is that all cTokens generated in exchange for cryptos become freely usable, movable, and tradeable in other DeFi applications.

In addition to earning interest on crypto assets, users can also borrow other cryptos on Compound by depositing collateral in return for “Borrowing Power”. The more the “Borrowing Power”, the more cryptos one can borrow. Compound avoids liquidation of locked-up assets by working on the concept of over-collateralization. It means borrowers must supply more value than they wish to borrow.

TrueFi

To bring about the next era of borrowing and lending in DeFi, TrustToken has launched TrueFi – a credit protocol for collateral-free lending. The TrueFi protocol adds something new to on-chain lending: crypto-native credit scores informed by on-chain and off-chain data, as well as the wisdom of the crowd of TRU token holders. It's unique approach has originated over $105 million in loans, with no defaults, since November 2020. As of writing, the Total Value Locked in TrueFi is close to $100 million.

How It Works

Unlike other lending protocols, TruFi doesn't require approved borrowers to deposit collateral to loan funds. Loans are drawn from lending pools funded by depositors of stablecoins like TUSD, USDC and soon USDT, on which depositors earn a competitive rate of return but also accept some risk in case of default. To borrow, applicants submit data on their business and crypto history, resulting in a credit score that sets the terms on the borrowers' TrueFi loans – and eventually, may inform loans on other DeFi platforms.

Borrowers who fail to return the money within the allotted time will face legal actions pursuant to an enforceable loan agreement signed during the onboarding process, and a hit to their credit score.

In the first version of TrueFi, loans were given based on borrower proposals voted by TRU stakers. However, in the newly launched TrueFi V3, the platform relies on a credit model informed by several factors, including repayment history, company background, operating and trading history, assets under management, and credit metrics. Moreover, with this V3 launch, TrueFi brings multi-asset support in the unsecured lending space, soon to support almost any asset on Ethereum for lending and borrowing.

Final Words

The growth of DeFi lending in recent years is proof that this trend has the potential to reshape the entire financial system. However, just like any technology, it also comes with unpleasant attributes. What if a third-party smart contract in a lending protocol is faulty? There is also the risk of borrowing APY rising dramatically within a short period.

While the entire lending process is simple on the above-listed protocols, users should be cautious and ensure they operate on a secure platform.

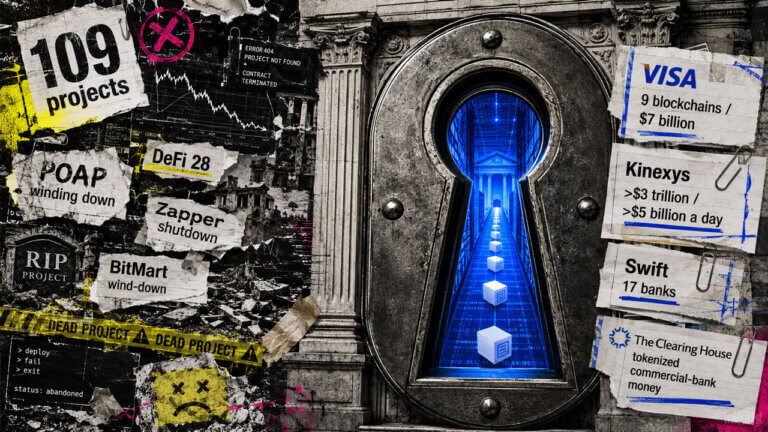

Is crypto dead yet? Project shutdowns peaked this April but the latest 2026 data hides a scarier trend

New tracker logs 109 records of crypto project shutdowns, wind-downs, and inactivity as banks build controlled blockchain rails.

On-chain options close in on crypto’s $21B-a-day perp market to deepen liquidity everywhere

Crypto options could deepen liquidity across spot, perps and DeFi by bringing hedging demand, market makers and risk-managed capital on-chain.

If Ethereum’s proposed 54% reward cut passes, DeFi’s favorite loop threatens to become a daily loss machine

A proposed Ethereum staking reward cut could squeeze ETH borrowing, leveraged loops and DeFi yields across Aave, LSTs and restaking.