Global cryptocurrency regulation is turning bearish in these five countries

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

As the cryptocurrency markets are in freefall, global cryptocurrency regulation appears to be turning bearish as well. While one SEC Commissioner proposes a “safe harbor” for cryptocurrency projects, the US Secretary of the Treasury announces “significant” new regulation. So, what gives?

Top five countries promising stricter cryptocurrency regulation

1. Brazil

The cryptocurrency scene in Brazil has taken several hits lately. Once thriving and “crypto-friendly”, the South American country’s IRS imposed stricter cryptocurrency regulation in August 2019.

According to the Brazilian crypto news site, Porto do Bitcoin, from that date, all exchanges have had to report all transactions monthly to the Federal Revenue Service — no matter the amount. They have also been subject to greater compliance burdens.

Brazilian cryptocurrency exchanges have been struggling to meet the criteria. But this month saw Access Bitcoin exchange closing its doors while another, Latoex, is reportedly in trouble. Former CPO of Access Bitcoin Pedro Nunes said:

“After the rules of the Federal Revenue, we noticed a significant decrease in the volume traded within our market. We also feel that the market has cooled for smaller exchanges.”

2. Russia

Russia’s stance on cryptocurrencies has been murky at best. The country seems to be sending out mixed signals as to how it wants its cryptocurrency regulation to develop.

With some of the most active traders in the world, major cryptocurrency exchange Binance’s CEO Changpeng Zhao said: “Russia is our key market” a few months ago. Binance also added support for the Russian Ruble just last week.

However, today, according to Russian news site RBC, the country is now stepping up its stance on AML. That means clamping down on crypto. The Russian Central Bank highlighted its plans to adjust banks’ roles and their ability to define the criteria for “unusual operations” when it comes to AML.

In other words? Opening up its authority to freeze cryptocurrency-linked bank accounts.

3. United States

We may celebrate the small victories as ‘Crypto Mom’ Hester Peirce keeps on trying. Yet, it seems the U.S. with its current regime refuses to warm to cryptocurrencies.

Indeed, as pro-Bitcoin candidate Andrew Yang withdrew from the presidential race, we’re left with an anti-crypto misogynist at the helm of the world’s most powerful nation:

I am not a fan of Bitcoin and other Cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air. Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity….

— Donald J. Trump (@realDonaldTrump) July 12, 2019

The president’s sentiment has been echoed by the US Secretary of the Treasury Steven Mnuchin. He told the Senate Finance Committee the U.S. Treasury Department's Financial Crimes Enforcement Network (FinCEN) is preparing “significant new requirements” for cryptocurrencies.

He added that we’ll “be seeing a lot of work coming out very quickly” and that both FinCEN and the Treasury Department had been “spending a lot of time” on this.

“We want to make sure that technology moves forward but, on the other hand, we want to make sure that cryptocurrencies aren't used for the equivalent of old Swiss secret number bank accounts”

On top of that, the DoJ also labeled bitcoin mixing a crime last week, while the Minneapolis Federal Reserve President Neel Kashkari called the cryptocurrency space “a giant garbage dumpster.”

4. Belgium

Another new development in cryptocurrency regulation comes out of the heart of the EU —Belgium. The country’s Financial Services and Markets Authority (FSMA) just revealed that it has been in discussions with the government of Belgium to enforce greater regulation on digital currencies for transactions.

Senator Jean-Paul Servais, chairman of FSMA, reportedly stated that the industry is clearly “growing at an alarming rate”. He urged lawmakers to establish a “legal framework for the sale, purchase, and use of virtual currencies and all related financial products.”

That doesn’t necessarily mean that cryptocurrency regulation here will be bearish. However, he cited following the lead of countries like China, Russia, and Algeria — countries that have either banned cryptocurrencies or heavily regulated them.

5. China

China may have doubled down on blockchain technology and announced plans for its own central bank-backed digital currency, but it remains vehemently opposed to cryptocurrencies.

In fact, when President Xi Jinping came out in support of blockchain last fall, the markets pumped with many in the crypto space calling him “Crypto Dad.” Beijing was quick to shut that down. The type of ledger that China is interested in is the permissioned one that it can control. Permissionless currencies like bitcoin are not part of the Communist Party of China's remit.

So, is there any hope? Well, since India’s Supreme Court finally declared that bitcoin and other crypto-assets are not illegally last month, investors are pouring in. Many players are taking advantage of here from Binance to OKEx announcing local partnerships.

It’s still somewhat disheartening though as we accelerate on so many fronts — and regulation remains firmly two steps behind.

Washington gave crypto every legal win it begged for then lost the market anyway

Washington removed crypto’s favorite excuse for failure, and the market responded by exposing a problem no regulator could fix: too few buyers.

CME freezes Nasdaq’s major Bitcoin launch, warning a legal loophole could upend the entire commodities market

The review will test whether a securities exchange can list direct Bitcoin index options in a market CME says belongs exclusively under CFTC oversight.

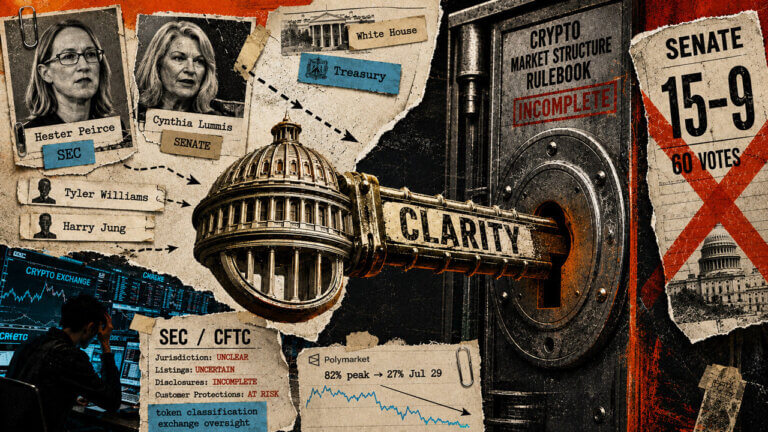

Odds of CLARITY crypto legislation passing sink to 27% as Treasury, White House, SEC, and Senate leads quit

Four crypto allies are exiting Treasury, the White House, SEC and Senate as lawmakers race to finish the US digital asset rulebook.