G20 Refrains from Regulation, Vows to Fight Money Laundering at Recent Summit

At the last G20 summit in March 2018, financial leadership from twenty of the world’s most significant economies had wildly divergent opinions about the validity and risk of cryptocurrencies. While some countries feared that official actions by the group would provide more legitimacy than the relatively new currencies deserved, others worried that an unregulated crypto market could upend the established financial system.

Differences aside, when the meeting was over, participants pledged to enact cryptocurrency legislation at their July meeting.

However, the July meeting has come and gone, and the G20 neglected to issue sweeping regulatory guidelines for digital currencies.

Crypto Doesn’t Present a Problem

In the lead up to the summit, the Financial Stability Board (FSB), the G20s regulatory watchdog, concluded that cryptocurrencies do not pose a substantial risk to the global economy, but were deserving of further observation.

In their official communique following the event, the G20 echoed that sentiment writing,

“While crypto-assets do not at this point pose a global financial stability risk, we remain vigilant.”

In short, crypto markets, while robust, are not widely integrated into the traditional financial system, so it’s unlikely that a crypto crash would impact the broader financial system.

As Jeffrey Kleintop, chief global strategist at Charles Schwab, recently told Time,

“For a potentially destructive bubble to form, cryptocurrencies need to be far more adopted and become a much larger share of household assets or the assets of leveraged investors like banks or some hedge funds.”

Moreover, in an unidentified but unmistakable way, the G20 heaped high praise on blockchain technology that underpins cryptocurrencies, noting in a communique,

“Technological innovations, including those underlying crypto assets, can deliver significant benefits to the financial system and the broader economy.”

However, the G20 expressed several concerns about the proliferation of crypto-assets including:

- Consumer and investor protection

- Market integrity

- Tax evasion

- Money laundering

- Terrorist fundraising

The latter two concerns received a date for further planning and policy adoption.

Money Laundering Initiative Underway

The FSB’s guidelines already include measures for monitoring money laundering and terrorist fundraising, and the G20 is relying on their expertise as well as the directions from the Financial Action Task Force (FATF) to guide their initiatives.

The G20 meets again in October, and they’ve requested the FATF to clarify how their standards apply to digital assets.

Money laundering and terrorist fundraising became a concrete concern this month when a U.S. Federal Indictment charged 12 Russian agents with money laundering using Bitcoin to finance their hack on governmental institutions.

However, the collection of countries exercised caution against overly hasty regulation or rulemaking, and cryptocurrency prices generally responded favorably.

Crypto prices are determined by many factors, but concerns about overly restrictive regulation have impacted crypto enthusiasts throughout the year. As far as the G20 is concerned, they are seriously considering how to regulate cryptocurrency, they heavily endorse blockchain technology, and they are committed to fighting money laundering and terrorist fundraising in the industry.

Athena Bitcoin agreed to a $4.5 million settlement, but claimants may have less than $3 million to split

If the court grants the proposed fee and expenses stay within the stated estimate, at least $2.985 million remains before other deductions.

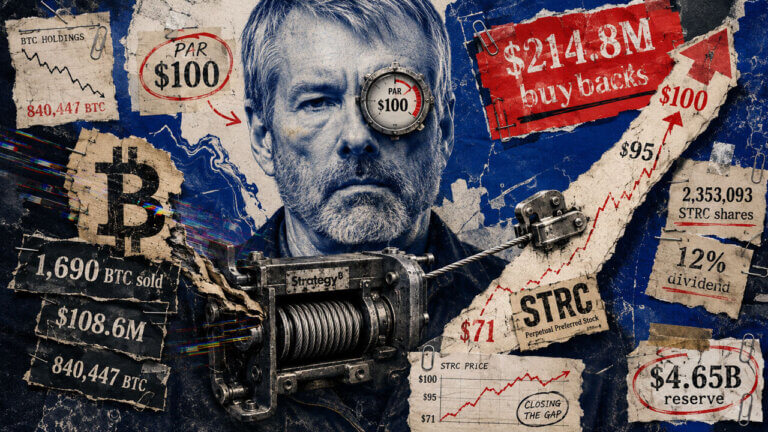

Strategy has $785 million left to close STRC’s final $5 gap after selling $213 million in Bitcoin

The company sold another 1,690 BTC to fund preferred-stock buybacks while its USD reserve climbed to a record $4.65 billion.

Kraken holds the instant liquidation switch on a crypto firm’s 479 Bitcoin if price drops to $45,094

The Aug. 7 filing ties 479 pledged Bitcoin to the higher balance, making the dated, principal-only threshold calculable.

Athena Bitcoin agreed to a $4.5 million settlement, but claimants may have less than $3 million to split

If the court grants the proposed fee and expenses stay within the stated estimate, at least $2.985 million remains before other deductions.

Multi-trillion-dollar offshore engine driving 90% of crypto trading arrives in America – and CME is suing to crush it

Coinbase became the latest exchange to bring crypto's dominant leveraged contract onshore even as a federal lawsuit contests the approval that made the move possible.

The $25 million Bitcoin glitch hiding inside Wall Street’s clearinghouses

Six regulated paths offer Bitcoin exposure, yet new research reveals pricing gaps that can reach $25 million.