Tokenized Real World Assets (RWA): Where are they now?

How tokenization is on the brink of transforming global liquidity, asset ownership and economic systems.

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

There is nothing in the world that is more scrutinized than money. How could it not be when money relays information on the value of…everything? And all economic activity arises from that record-keeping, if it is conducted accurately.

When Bitcoin launched in 2009, it opened a new door, a new perspective on how that information is managed and transferred. Or, more precisely, blockchain technology did. While Satoshi Nakamoto envisioned Bitcoin as self-contained and sovereign even from governments and central banks, blockchain is a neutral tool.

One that can spur another FinTech wave – tokenization of real-world assets (RWAs). These types of tokens have all the hallmarks of blockchain assets – transparency, efficiency and self-custody – backed by real-world assets.

Internet > Blockchain > Tokenization

Blockchain technology was critical in establishing the trust needed for Bitcoin to evolve into a digital asset worth half a trillion dollars. By leveraging cryptography with chained data blocks, wherein each new block is dependent on the previous one, Bitcoin is the pioneering proof-of-concept that digital records can be made immutable.

And if real-world value can be brought into the digital world securely, we are at the doorstep of a new era. The era of the tokenization of real-world assets (RWAs). If something is legally definable as an asset, that logic can be tokenized into a tradable asset. For this reason, the RWA scope is limitless, ranging from real estate, art and securities to debt instruments, luxury goods and fund-raising equities.

RWA tokenization is groundbreaking in that it opens 24/7 trading doors to a global market, previously reserved for exclusive institutions. On top of that, even non-fungible assets like machinery or commodities could be made fungible with fractional ownership. Above all else, RWA tokenization reduces the friction of capital flows by removing, or drastically reducing, intermediaries.

Yet, regarding something as important as value, “groundbreaking” innovation often takes a back seat to caution. Moreover, it is unclear that intermediaries could be removed in all instances, which would mute the entire point of tokenized RWAs. With that in mind, how do we view the current state of RWA tokenization and its future?

Measuring the Momentum of Monetary Innovation

Blockchain technology is both new and revolutionary. One approach to gauge its adoption rate is to view investor interest. However, this often results in hype bubbles that don’t indicate its longevity. By the same token, bubbles are another indicator if framed properly.

Fourteen years after Bitcoin emerged, 4.2% of the global population, over 420 million, engage with blockchain technology by holding crypto assets. Is this percentage good or bad? How do we anchor it in a reference point to measure the RWA tokenization rate?

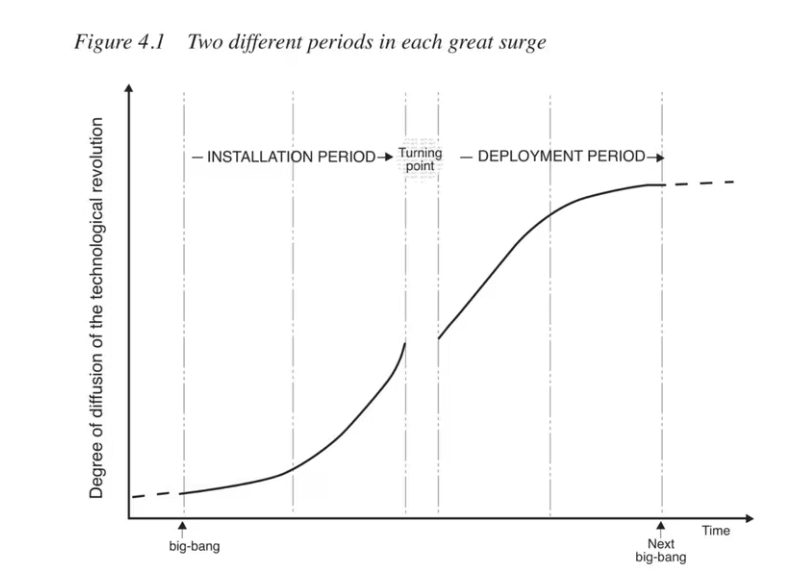

Economist Carlota Perez developed a framework to gauge the long-term dynamics of technological disruption. This “Perezian framework” revolves around the adoption phases of a cycle:

- Irruption – New tech emergence that disrupts existing industries.

- Installation – The economy and society restructures around the new tech, accompanied by new business models and regulatory frameworks.

- Bubble – Frenzy stage during installation in which investors become overly optimistic, accompanied by speculation and financial bubbles leading to crisis (bubble bursts) and stagnation.

- Synergy – The post-bubble burst recovery, wherein the surviving investors adopt the new tech more efficiently.

In the golden phase, maturity, the new tech is fully integrated into the social and economic fabric. This typically lasts several decades until the point of diminishing returns or until the next irruption.

As one reads through these phases, one can immediately recall the dot-com bubble in the late 1990s, wherein the core “irruption” was the internet itself, as a prerequisite for Bitcoin and tokenization.

By October 2002, the Nasdaq Composite, representing internet-centered companies, plunged 740% from its peak in March 2000. If we apply the Perezian framework, we have already gone from one irruption (the internet) to the next (blockchain).

Further, considering the relentless string of bankruptcies in 2022, from Terra and Celsius to FTX, we have reached the bubble burst stage. This is also apparent from a withdrawal of VC capital. According to PitchBook data, the first half of 2023 saw only 814 crypto deals go down, compared to 1,862 in 2022.

Reminiscent of the dot-com bubble burst, this capital drought translates to only $325 million in investments in crypto startups in Q2 2023 vs. $3.5 billion in the peak of Q1 2021. In other words, RWA tokenization is leaving behind the bubble phase to the synergy phase.

RWA Tokens: Resilience from Decentralization

As previously noted, tokenized RWAs only constitute “irruption” if it is possible to reliably claim an asset without an intermediary. Case in point, let’s say a farmer buys a token to expand operations. This particular tokenized RWA would represent farming equipment like a tractor.

This token is available on a certain platform. The farmer would pay less for the token/tractor because he wouldn’t have to deal with an intermediary such as a dealership. But what happens if that platform goes bust for some reason?

Without the platform that issued the token, how would the farmer redeem the token or claim ownership of the tractor in the future when he intends to sell it?

The solution comes in the form of smart contracts that are hosted on a large blockchain network, such as Ethereum. One may recall that the US Treasury sanctioned currency mixer Tornado Cash. Yet, even with the sanction, the underlying smart contract continued to be hosted, although without the web interface provided by Infura/Alchemy.

Then, it was only a matter of circumventing the block with Interplanetary File Storage. This is the kind of decentralized finance (DeFi) resilience investors expect when buying hard assets as tokens. As long as the blockchain network is live, secured by thousands of nodes across the globe, redeemability is independent of trust on any Web3 platform.

In other words, tokenized RWAs serve as redeemable smart contracts, irreversible to cancellation. We have already seen it with non-fungible tokens (NFTs) which can define the conditions of ownership/royalties, including fractional ownership. RWA tokens will further expand smart contract logic to cover disputes by decentralized dispute resolvers.

The Current Landscape of Tokenized RWAs

As fiat currency tokenizers, stablecoins have been pushing the RWA market the , while cryptocurrencies can monetize specific projects or serve as scarce commodities. For instance, Bitcoin mimics digital gold. On the other hand, NFTs tokenize general property rights for ebooks, albums and artworks. General RWA tokenization is the natural step forward.

The first wave will deal with assets that don’t require additional infrastructure, such as the Internet of Things (IoT). After all, hard assets would have to integrate real-time tracking in order for their status (location/price) to be broadcasted to blockchain networks.

The earliest form of this technology is present in parcel tracking. For this reason, more abstract RWAs will have priority. Larry Fink, the CEO of the world’s largest asset manager, BlackRock, had hinted that these would be familiar stocks, bonds, and other financial instruments.

Blackrock is the world's largest asset manager with $10 trillion in AUM. 💰💰💰

Blackrock CEO Larry Fink:

“I believe the next generation for markets… for securities, will be tokenization of securities.” pic.twitter.com/f3MmASXywi

— The Tokenist (@thetokenist) January 20, 2023

Startups Tzero and Securitze have established themselves as veteran tokenizers. Likewise, Goldman Sachs’s Digital Asset Platform (DAP) went online in January. Major US banks and Big Tech companies have joined to build tokenized products on a permission blockchain network called Canton.

Digital Asset developed the Canton Network, with Goldman Sachs as the main DA investor. Surprisingly, even outside financial institutions joined in. The European Investment Bank (EIB) had already issued a second euro-denominated digital bond on Canton.

On permissionless networks, tokenized bonds constitute a $630.2 million market, at an average yield of 5.25%. Notably, German tech giant Siemens used Polygon to issue its first corporate digital bond worth €60 million, with a maturity of one year.

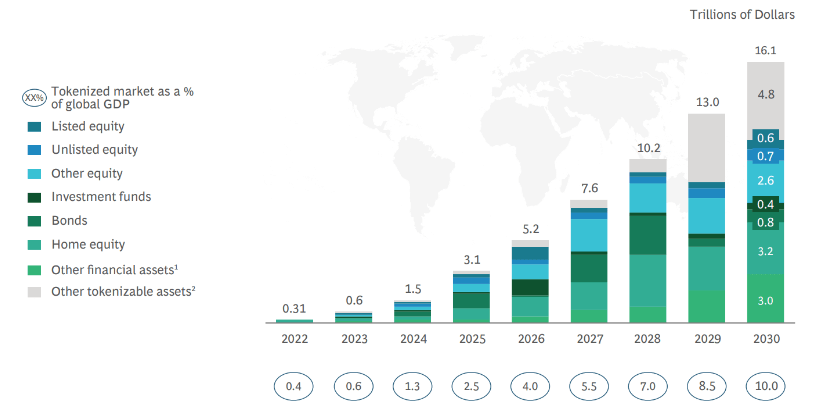

One RWA dApp, as an outgrowth of the popular lending dApp AAVE, holds a $7 million market size. Suffice to say, all of these are way under one-billion figures. This is why the range for the global RWA market is so speculative right now. Boston Consulting Group forecasts on-chain RWA activity to reach between $4 trillion to $16 trillion by 2030.

The rise in retail trader communication as seen through Discord servers focused on stock trading has the potential to forge a path into tokenized RWAs too. According to CySEC, nearly 22% of retail investors source their trading ideas from social media platforms. Furthermore, these communities serve as a breeding ground for innovative ideas, so it’s not hard to see tokenized RWAs getting traction there as well – in this new ‘home’ of the retail trader.

In the near future, as a percentage of global GDP, the tokenized market should reach 2.5% by 2025, mainly in home equity and bonds. The real adoption should manifest with more diverse “other tokenizable assets” in late 2020s.

Alongside blockchain and crypto assets, understanding traditional financial instruments like options trading is very important as they still continue to play a role in market dynamics. Their coexistence and potential synergies with tokenized assets could become a fascinating area of study and investment as this new era of financial diversification unfolds.

RWAs’ End-Goal: Turing-Complete Economy

Due to the investment drought left over by the crypto winter, termination of the banks embracing cryptocurrency, and the Fed’s hiking cycle that made capital more expensive, we are still in the pioneering stage of the global RWA market.

Nonetheless, the world’s premiere network that combines academic, social, political and economic capital, the World Economic Forum (WEF), is fully onboard with tokenization. According to prof.Jason Potts from RMIT University, the end-goal of RWA tokenization is to “replicate real-world social infrastructure in a digital world.”

Under the Agenda 2030, prof. Potts envisions a new kind of commerce that seamlessly fuses physical and digital economy into a “computable economy”. That is the last cog of the tokenized puzzle. If all the world’s assets are tokenized, and accessible on a public ledger, this would enable a “turing-complete economy”.

Mirroring the Turing machine theory, such an economy could model any possible economic system because there would be total accounting of assets. In that scenario, the entire economic system could be simulated. And if something can be simulated, it can be directed to follow optimal outcomes.

This is a natural outgrowth of the WEF’s stakeholder capitalism concept, which branches out from the narrow shareholder interest to all stakeholders in wider communities.

Conclusion

Ownership representation has come a long way from stone tablets. It turns out, the method of representation matters greatly. When the internet came along, people were amazed they could communicate permissionlessly with anyone worldwide.

Another amazement is on the way, in the form of tokenized real-world assets (RWAs). Just as one taps into a social network, it will be possible to access global ownership ledger. Although divided between permissioned and permissionless, a tokenized market will bring a new era of liquidity.

In that arena, both buyers and sellers can acquire and sell assets easily, transparently and with less capital friction typically generated by intermediaries. In the end-game of tokenization, we might even see a shift to a new economic paradigm as new monetary systems are simulated and enacted.