The main trust sits with KAST and its partners. Once assets enter the card flow, they are treated as sold to KAST, handled through partner custody and payment providers, and shown in the app as a USD-denominated obligation rather than a bank deposit or user-controlled crypto balance.

The main risk is custody and issuer dependence. Card-level risks like fraud or declines are secondary. Self-custody is not part of the spending setup, and if the account is restricted or flagged for compliance, KAST and its partners can freeze access, limit transactions, or require more checks before funds move. Device access, login security, and phishing remain relevant risks regardless of the custody model.

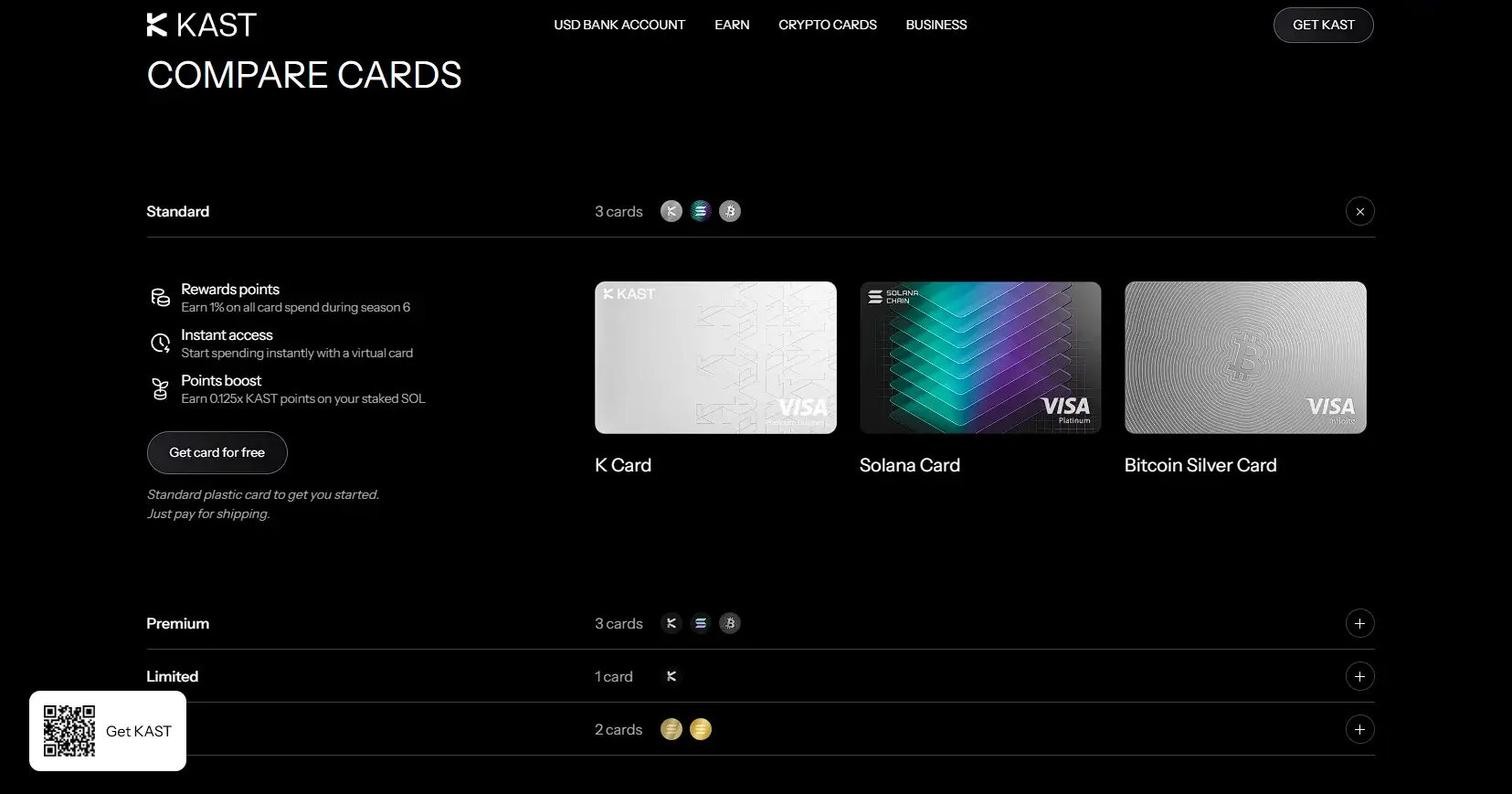

There is also a merchant-use risk that goes beyond an ordinary decline. KAST Card should not be used for banned or high-risk merchant categories such as weapons, firearms, ammunition, knives and related accessories, controlled substances, prescription drugs, steroids, counterfeit goods, fake IDs, darknet or Tor marketplaces, adult content, pseudo-pharmaceuticals, and businesses tied to fraud, money laundering, terrorism financing, pyramid schemes, or multi-level marketing programs. A payment can be flagged even when the merchant appears legitimate, if the merchant category or transaction pattern matches a restricted use case.

The risks are broader than a single failed payment. A flagged transaction can lead to a blocked purchase, extra KYC or source-of-funds checks, a temporary account freeze, card suspension, asset restrictions, forced review by a partner, chargeback complications, account closure, or a permanent ban from the service. If KAST or a partner believes the activity breaks card-network rules, sanctions controls, AML checks, or platform terms, they can also stop future transactions and keep the account limited until the review is complete.