The information provided in this article is for educational and informational purposes only and should not be construed as financial, legal, or tax advice.

Overview

Introduction

A long-term crypto holder can still face short-term liabilities. A large tax bill, property purchase, working-capital need, portfolio rebalance, or fresh investment opportunity can create a liquidity requirement long before conviction in BTC, ETH, XRP, or SOL has changed.

That is the real framing for this guide. This is not mainly a retail debt story. It is a capital-allocation story. Once a position becomes meaningful, the question changes from “Should I take a loan?” to “What is the least damaging way to meet a liquidity need without compromising the core asset base?”

In jurisdictions where tax reporting is tied to sales, exchanges, or other dispositions, separating a liquidity decision from an exit decision can matter even more. That does not make borrowing a loophole or a substitute for tax advice. It helps explain why many long-duration holders think of selling and liquidity as two separate decisions.

What this guide covers

- Why sophisticated holders often separate liquidity decisions from sale decisions

- Why selling can be more expensive than it first appears from a portfolio perspective

- How secured borrowing can preserve exposure while creating optional liquidity

- Which risks, controls, and governance questions matter before using crypto as collateral

- How to think about CoinRabbit as one example within this category

Who this guide is for

- Intermediate crypto readers moving beyond a purely retail framing

- Long-term multicurrency holders managing meaningful positions

- Founders, operators, and treasury-minded readers thinking about capital efficiency

- Readers focused on preserving upside exposure while improving liquidity flexibility

Liquidity gap

The real question is not “should I sell crypto?” — it is “how do I stay liquid without impairing core exposure?”

Most people begin with the wrong question. They ask whether borrowing is a good idea in the abstract. Long-term holders usually ask a narrower and more useful question: do I actually want to sell this asset right now?

That distinction matters because selling is not just a cash event. It is an exposure event. Once the asset is sold, the upside is gone. Rebuilding the position later may sound simple in theory, but in practice it often means buying back at a worse level, re-entering too late, or never re-entering at all.

When conviction remains intact, the real problem is often not belief. It is liquidity. The asset may still be doing its job as a long-duration holding, but it is not solving today’s cash need. Borrowing exists to bridge that gap.

For readers managing meaningful capital, that gap becomes strategic. The issue is not whether cash is useful. It is whether selling a core reserve asset is the right way to obtain it.

Balance sheet

How sophisticated holders and treasury-minded operators frame the decision

As position size grows, the decision framework changes. A core holding stops looking like a trade and starts looking like strategic capital — something closer to a reserve asset, treasury sleeve, or balance-sheet resource.

That is why the mindset of high-net-worth individuals, founders, family offices, and treasury teams often converges. They are not asking only how to monetize an asset. They are asking how to preserve exposure, maintain optionality, and meet liabilities without disrupting the long-term allocation.

Traditional finance has always done versions of this with strong collateral. Securities-backed credit lines, real-estate-backed borrowing, and other forms of asset-backed financing all follow the same underlying principle: do not sell the asset unless you actually want to exit the asset. Use credit selectively when the asset itself remains strategically valuable.

Crypto is increasingly being evaluated through the same lens. That does not mean every holder should borrow. It means that once digital assets are treated as meaningful capital, the conversation naturally shifts from “trading” to “capital management.”

Exposure cost

Why selling is a capital-allocation event, not just a cash event

Selling solves the immediate liquidity problem, but it also changes the future portfolio. That is easy to miss when the cash need feels urgent.

A sale reduces exposure, can create a reporting event depending on jurisdiction, and forces a second decision later about if, when, and how to re-enter. For long-term holders, that future re-entry decision is often harder than the initial sale.

Borrowing changes the path rather than ending it. Instead of converting the asset into liquidity through disposal, the holder converts the asset into collateral and raises liquidity against it.

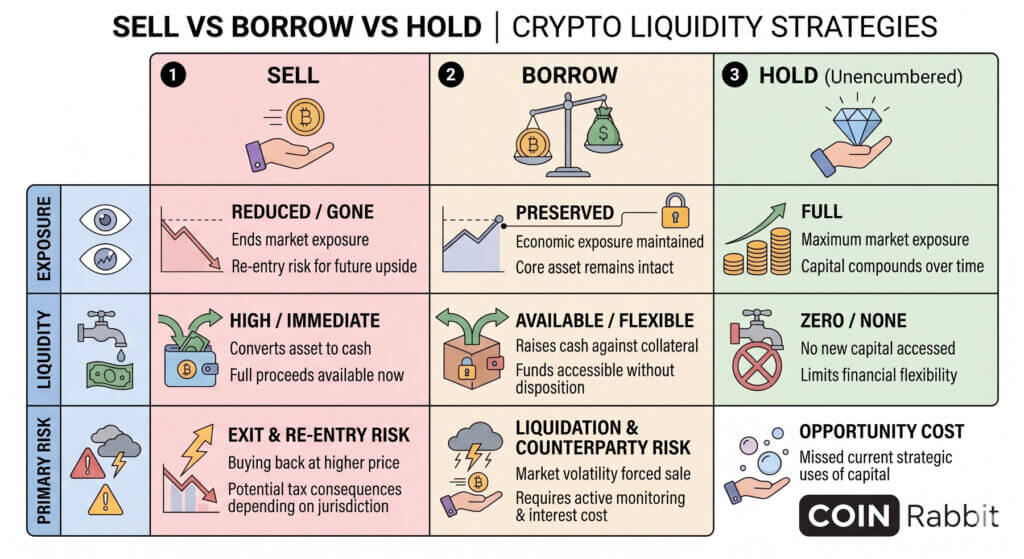

Sell, borrow, or hold

| Action | Portfolio result | Main tradeoff |

|---|---|---|

| Sell down core holdings | Immediate liquidity, reduced exposure | Exit risk, re-entry risk, possible tax/reporting consequences depending on jurisdiction |

| Borrow against holdings | Liquidity while preserving economic exposure | Interest cost, liquidation risk, counterparty risk, active monitoring |

| Hold unencumbered | Full exposure, no added complexity | No new liquidity |

Seen through that lens, selling is rarely just a funding decision. It is a capital-allocation decision with portfolio consequences that can last far beyond the initial cash need.

Optionality first

Why secured borrowing can fit a capital-preservation mandate

A collateralized loan can make sense when the asset thesis is unchanged but the timing of the cash need is inflexible.

For one holder, that might mean paying a large bill without liquidating a concentrated long-term position. For another, it might mean funding working capital, seeding a new allocation, or creating a liquidity buffer while leaving the core asset base intact. The attraction is not a theater. It is optionality.

From a capital-management perspective, the appeal is collateral efficiency. The holder is converting balance-sheet value into usable liquidity without immediately disposing of the reserve asset. In that sense, crypto-backed borrowing is generally closer to secured finance than to unsecured consumer debt.

This is also why the strategy should not be romanticized. Borrowing does not remove downside. It relocates it. Instead of realizing an exit today, the borrower accepts financing cost and risk-management obligations in exchange for preserving exposure.

Long horizon

Why the “buy, borrow, die” shorthand keeps resurfacing

The phrase became popular because it compresses a real capital-management instinct into a memorable shorthand. In more formal terms, the idea is simple: accumulate a scarce asset, avoid unnecessary dispositions, meet liquidity needs through secured borrowing when appropriate, and let the core position compound across time.

That framing resonates most with holders who think in decades rather than quarters. For private wealth, founders, family offices, and long-duration allocators, the objective is usually continuity of exposure, not constant monetization.

The larger the capital base, the more the mindset shifts from “How much can I spend from this asset?” to “How do I manage around this asset without weakening it?” That is why the strategy often shows up in conversations about generational wealth, treasury resilience, and long-term stewardship.

None of that makes the approach universal. It simply explains why selling can feel like the most expensive choice even before the market proves whether that instinct was correct.

Risk discipline

What borrowers must underwrite before using crypto as collateral

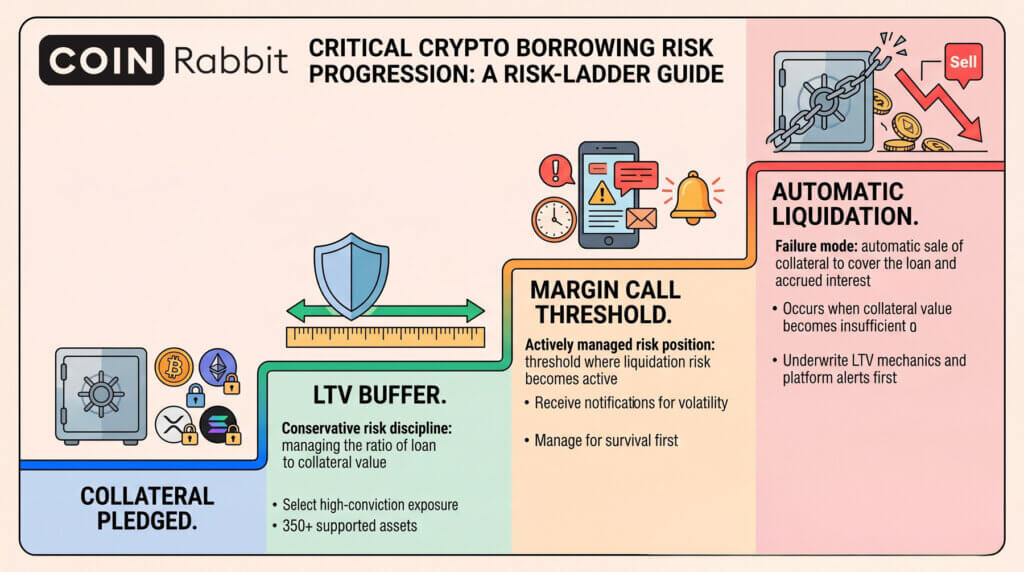

Before anyone borrows against crypto, they need to underwrite more than a headline rate or a fast funding promise. They need to understand collateral terms, LTV policy, liquidation mechanics, custody, reserve model, legal structure, and operational response times.

That is because crypto-backed borrowing is not a passive convenience product. It is an actively managed risk position. The borrower is taking a volatile asset, encumbering it, and relying on both the platform and their own discipline to keep the position healthy.

On CoinRabbit, as in the category more broadly, LTV refers to the ratio between the loan amount and collateral value. A margin call is the threshold at which liquidation risk becomes active. Liquidation is the automatic sale of collateral to cover the loan and accrued interest when the collateral value becomes insufficient. Those mechanics are not side notes. They are the structure of the product.

Service model

Where a managed lender like CoinRabbit fits in the category

At the category level, centralized lenders appeal to borrowers who value service, speed, and clear operational support alongside access to collateralized credit. DeFi can offer transparency and permissionless execution, but it also asks the client to manage wallet operations, onchain interactions, liquidation logic, and self-directed risk controls in real time. Some borrowers prefer that. Others prefer a managed service model.

This is the context in which CoinRabbit fits. The stronger framing is not “here is a place to get a loan.” It is “here is one example of a managed, service-led lender operating inside the crypto-backed liquidity category.”

That positioning is visible in the company’s own language. CoinRabbit describes itself as a crypto asset management platform, says it offers safe custody since 2020, promotes a Private Program for clients with $500,000+ in capital, and emphasizes fully reserved assets, no rehypothecation, cold-wallet multisig custody, and 24/7 human support. Its loans page positions the product around access to liquidity without selling, says funding can happen in about 10 minutes, and says borrowers can use more than 350 supported assets as collateral.

Practical answers

FAQ

When does borrowing against crypto make more sense than selling?

It tends to make more sense when the holder still wants the asset exposure, but the cash need cannot wait. In that case, selling and liquidity are two different decisions. Borrowing can preserve the long-term position while solving the short-term funding need, provided the borrower is comfortable with the added risk and monitoring burden.

Who typically uses this strategy?

Not only whales, but the logic usually becomes clearer as position size, concentration, and tax sensitivity increase. Long-duration holders, founders, operators, high-net-worth individuals, and treasury-minded allocators often think this way because they are managing capital, not just chasing short-term cash flow.

Does borrowing actually preserve upside exposure?

Economically, that is the main appeal. The borrower raises liquidity while keeping exposure to the underlying asset instead of selling it outright. That said, the exposure is only preserved if the position remains healthy and avoids liquidation.

Is this primarily a tax strategy?

It is better understood as a liquidity and capital-management strategy. Tax treatment is one reason some holders prefer not to sell appreciated assets, but the primary decision is about preserving exposure and avoiding an unnecessary disposition. Actual tax outcomes depend on jurisdiction, facts, and what happens around the loan.

What are the main risks to underwrite before borrowing?

The big ones are collateral volatility, LTV drift, liquidation mechanics, counterparty risk, custody, and legal structure. A borrower should also understand whether the platform reuses collateral, how quickly it notifies users when risk rises, and what support exists during fast market moves.

How conservative should a borrower be with LTV?

In general, more conservative structures leave a wider buffer than the maximum borrowing capacity would allow. High LTV can improve immediate liquidity, but it reduces room for error in volatile markets. Borrowers who care about capital preservation usually optimize for resilience before efficiency.

Is this a set-it-and-forget-it strategy?

No. Crypto-backed borrowing works best when it is actively monitored. Even strong borrowers can get into trouble if they treat a volatile collateral position like passive cash management.

What separates a disciplined lending setup from a fragile one?

A disciplined setup pairs a clear liquidity use case with conservative sizing, healthy collateral buffers, and a platform that can explain its custody, reserve model, liquidation process, and borrower support. Platform selection is not a side decision in this category. It is part of the risk itself.

Due diligence

Next step

The next question is not how quickly a borrower can raise a loan. It is how to tell the difference between durable credit infrastructure and fragile credit infrastructure.

Guide #2 will cover collateral reuse, counterparty risk, trust signals, legal structure, and the evaluation checklist readers should use before posting meaningful capital. That is the natural next step, because borrowing against crypto only makes sense when the platform structure is strong enough to deserve the collateral.

Unlock and manage liquidity without selling

Don’t sell. Preserve your capital through a more strategic, portfolio-focused approach.