Research: Quantitative Tightening has potential to be the most disruptive ever

The Federal Reserve has one core tool to combat inflation in Quantitative Tightening. Macro data suggests the upcoming period of QT will be more turbulent than ever before.

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

Quantitative tightening (QT) reduces the Federal Reserve's balance sheet. It transfers a significant amount of Treasury and agency mortgage-backed securities to investors.

The current Fed policy is to use QT as a tool to combat inflation as well as increasing interest rates.

It is the opposite of what has been more prevalent over the past several years in Quantitative Easing, whereby central banks print money to purchase securities from the open market.

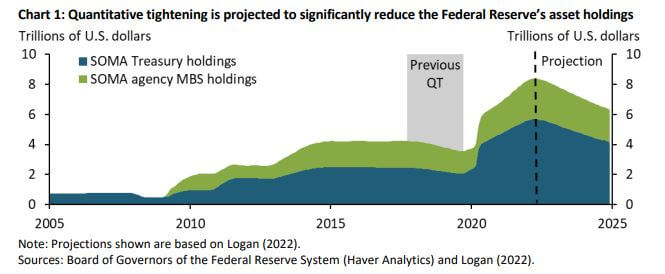

QT has not been the policy in the US since 2017, and according to macro data, this QT will be more significant when financial markets are strained. The goal is to combat surging inflation by reducing the $9 trillion Fed balance sheet.

In 2019 there was $4.2 trillion on the Fed balance sheet, and by the end of May 2022, it had risen to a staggering $8.9 trillion due to aggressive asset purchases throughout the Covid-19 pandemic.

Between 2017 and 2019, the Fed reduced its bond holding by $650B. We will start to see the impact of QT this September, and data suggests that it will be more extensive and aggressive than in 2017. The Fed will likely be offloading $95B of Treasuries and Mortgage-backed securities, based on projections of more than $2 trillion.

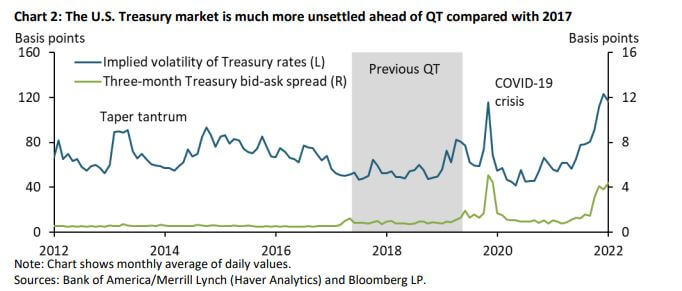

Further, the US Treasury market is also more volatile than in 2017. The blue line in the chart below shows the MOVE index, which measures future volatility in treasury rates. The volatility is well above the levels during the height of Covid-19 and the previous period of QT in 2017.

The green line represents liquidity measures such as the bid-ask spread for Treasury bills. This spread is also elevated, similar to pandemic levels.

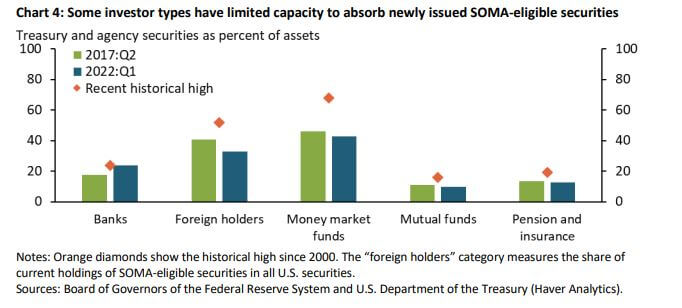

The following chart illustrates the maximum share of SOMA-eligible securities held by each investor type since 2000. This data acts as a realized benchmark for the maximum balance sheet absorption capacity. Foreign holders and money market funds (MMFs) may be able to absorb some additional SOMA-eligible securities, though the scope is likely limited. However, pensions and banks are near capacity.

The share of Foreign Holders has been declining since the global financial crisis as they pivoted to purchasing gold instead. The Fed will need much higher yields for short-term maturities, indicating that this QT episode has the potential to be more disruptive than ever before, primarily due to rising rates.

Bitcoin has no such monetary policy. There is no way to increase supply without forking the entire network, removing any party's ability to increase the Bitcoin money supply. Bitcoin is automated in terms of monetary policy, with supply tied directly to hashrate and network difficulty. These mechanics form part of the argument favoring Bitcoin as a store of value and a long-term inflation hedge.

The crypto industry has followed traditional securities markets throughout 2022. However, Bitcoin has never experienced a recession, aggressive QT, or inflation beyond 2.3%, all of which are prevalent in today's market. The following 12 months will be unprecedented territory for Bitcoin, and it will be a real test of its economical design.

TeraWulf’s Bitcoin mining revenue fell 73% as AI related leases reached 71% of sales

HPC leasing generated $31.9 million in the quarter as the company spent heavily to expand its data-center capacity.

Bitcoin treasury Strive bought 20 BTC, but 110,000 new shares left holders with less Bitcoin exposure

Bitcoin holdings rose 0.10%, while effective common shares increased 0.13% and trimmed gross per-share exposure by about 0.03%.

How dumping 1,200 Bitcoin helped a cellular chipmaker completely erase its debt and double its cash

The chipmaker ended June with 314 unrestricted coins after sales helped erase convertible debt and lift cash to $21 million.

How 4,200 malicious smart contracts tricked 5,700 victims into signing away their crypto

The unpeer-reviewed study links 4,224 contracts to 5,742 victim addresses, while its Avalanche count and collection cutoff conflict.

A tiny cluster of Solana bots unlocked a 3x trading advantage by routing through one proprietary protocol

The 62.3% versus 21.01% split covers one 12-address MEV-like group and shows association, not causation.

New Bitcoin study shows the strongest recurring liquidation warning signs cannot warn of an individual crash

The order-flow pattern stood out across six events, while two observations still overlapped ordinary-market conditions.