Bitcoin’s historical performance: September dips and year-end rallies

CryptoSlate's latest market report dives deep into Bitcoin's historical monthly and quarterly returns, focusing on the period between 2013 and 2024 to assess the likelihood of a similar pattern unfolding in 2024.

Volatility is one of the crypto market’s defining characteristics. While a myriad of different factors causes it, it’s usually not arbitrary. It has historically followed specific patterns, which, when studied, can provide insight into future price movements.

Historically, Bitcoin has exhibited a cyclical performance, with specific months and quarters consistently showing stronger or weaker returns.

For example, data from 2013 to 2024 shows that Bitcoin typically underperforms in September, with average returns in that month coming in at -4.89%, making it one of the weakest months of the year. A recovery often follows this dip in performance in Q4, where Bitcoin’s returns have historically been strong. Q4’s average return of +88.84% suggests that Bitcoin usually recovers from the September slump, leading to positive quarter-on-quarter (QoQ) growth by year’s end.

In this report, CryptoSlate will dive deep into Bitcoin’s historical monthly and quarterly returns, focusing on the period between 2013 and 2024 to assess the likelihood of a similar pattern unfolding in 2024.

Specifically, we’ll analyze Bitcoin’s historical tendency to experience a September dip followed by a Q4 recovery. We can better understand how seasonality and macroeconomic factors influence Bitcoin’s price action in these critical months by examining past performance.

Although each market cycle is unique, specific trends—such as Bitcoin’s seasonal volatility—tend to repeat. This repetition can make historical analysis helpful in predicting the likelihood of particular market movements.

Seasonal trends, like the September dip and the Q4 rebound, have been observed across multiple years, making them a valuable reference for market participants anticipating Bitcoin’s next move. Understanding these patterns is particularly important as we approach the final months of 2024.

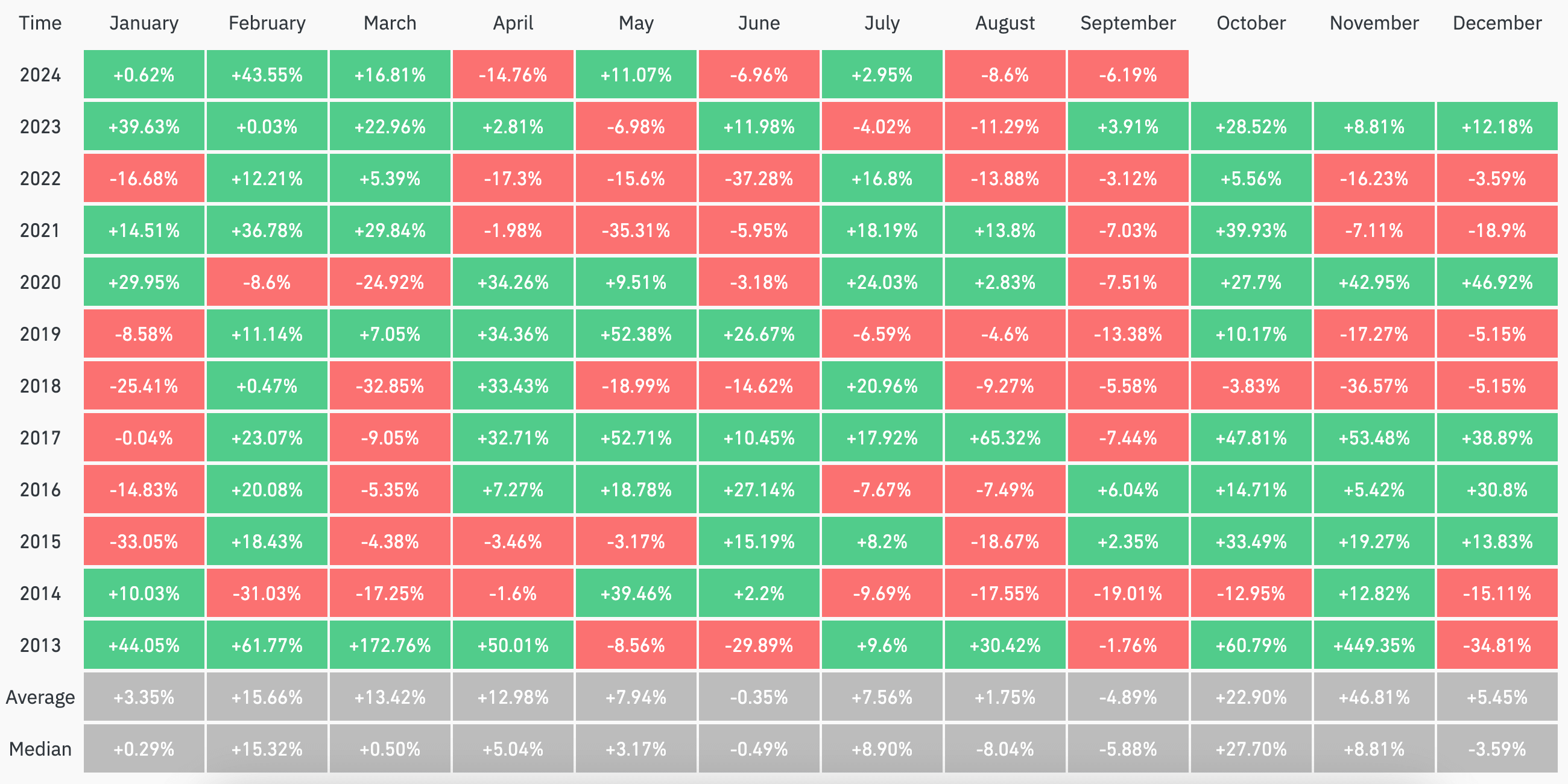

Historical monthly performance

Bitcoin’s monthly returns have also demonstrated a clear cyclical pattern, with certain months consistently delivering better performance than others. Analyzing CoinGlass data from 2013 through 2024 shows recurring trends that reflect this seasonality. On average, Bitcoin has performed well during the beginning and end of the calendar year, while the middle of the year, particularly the summer months, tends to exhibit weaker performance.

Historically, January has been relatively unpredictable, with an average return of +3.35% and a median return of +0.29%. February, however, shows a more consistent positive trend, with an average return of +15.66% and a median return of +15.32%. March tends to follow this up with moderate gains, averaging +13.42%. These first-quarter months often see a rebound from the previous year’s market sentiment, driven by renewed institutional interest and macroeconomic catalysts.

However, Bitcoin’s performance historically weakens as we move into the second quarter and the summer months. June, for example, has an average return of -0.35%, reflecting the reduced trading volumes and general market fatigue that tend to occur during these months.

July and August also show mixed results, with August posting an average decline of -8.04%, indicating that summer generally brings bearish momentum to Bitcoin’s price.

Table showing Bitcoin’s monthly returns from 2013 to 2024 (Source: CoinGlass)

Notably, September is typically one of the worst-performing months for Bitcoin, with an average return of -4.89%. This makes it the second weakest month in Bitcoin’s historical performance data.

Conversely, October and November are two of the strongest months for Bitcoin, with October posting an average return of +22.90% and November delivering an impressive +46.81%. These months often mark the beginning of a Q4 recovery, driven by market optimism and the anticipation of year-end events.

September

For instance, in September 2019, Bitcoin saw a significant -13.38% decline, followed by a similarly bearish month in 2020, with a -7.51% loss. September 2022 also saw Bitcoin drop by -3.12%.

Several factors contribute to September’s historical underperformance. First, macroeconomic events tend to weigh on Bitcoin’s price during this month. September often marks a period of global economic shifts, including the end of summer holidays, the approach of central bank policy updates, and institutional portfolio rebalancing.

These factors often increase selling pressure in both traditional and crypto markets. Additionally, liquidity tends to dry up this month, exacerbating Bitcoin’s volatility and leading to steeper price declines.

Another essential aspect to consider is market sentiment. September has historically coincided with a period of caution in the market. Investors typically prepare for Q4 by reducing risk exposure, leading to reduced buying momentum for Bitcoin. This drop in market activity contributes to the broader bearish trend during this time.

October and November

While September is often challenging, Bitcoin’s seasonality patterns point to a strong recovery in October and November. Historically, Bitcoin tends to rally during these months, with October’s average return of +22.90% and November’s stellar average of +46.81%.

For example, in October 2020, Bitcoin saw a +27.7% gain, followed by a significant rally in November with a +42.95% increase. Similarly, in 2021, Bitcoin posted +39.93% in October, signaling a sharp rebound after September’s weak performance.

This recovery can be attributed to several factors. First, renewed institutional interest often drives prices higher as funds and institutional investors reallocate capital heading into Q4. Additionally, anticipating holiday spending, macroeconomic events, and even regulatory updates provides positive momentum for Bitcoin during these months.

Moreover, the broader crypto market also tends to see increased activity as retail investors re-enter toward the end of the year. Historically, this increases buying pressure, pushing Bitcoin’s price higher and reversing the bearish trend from previous months.

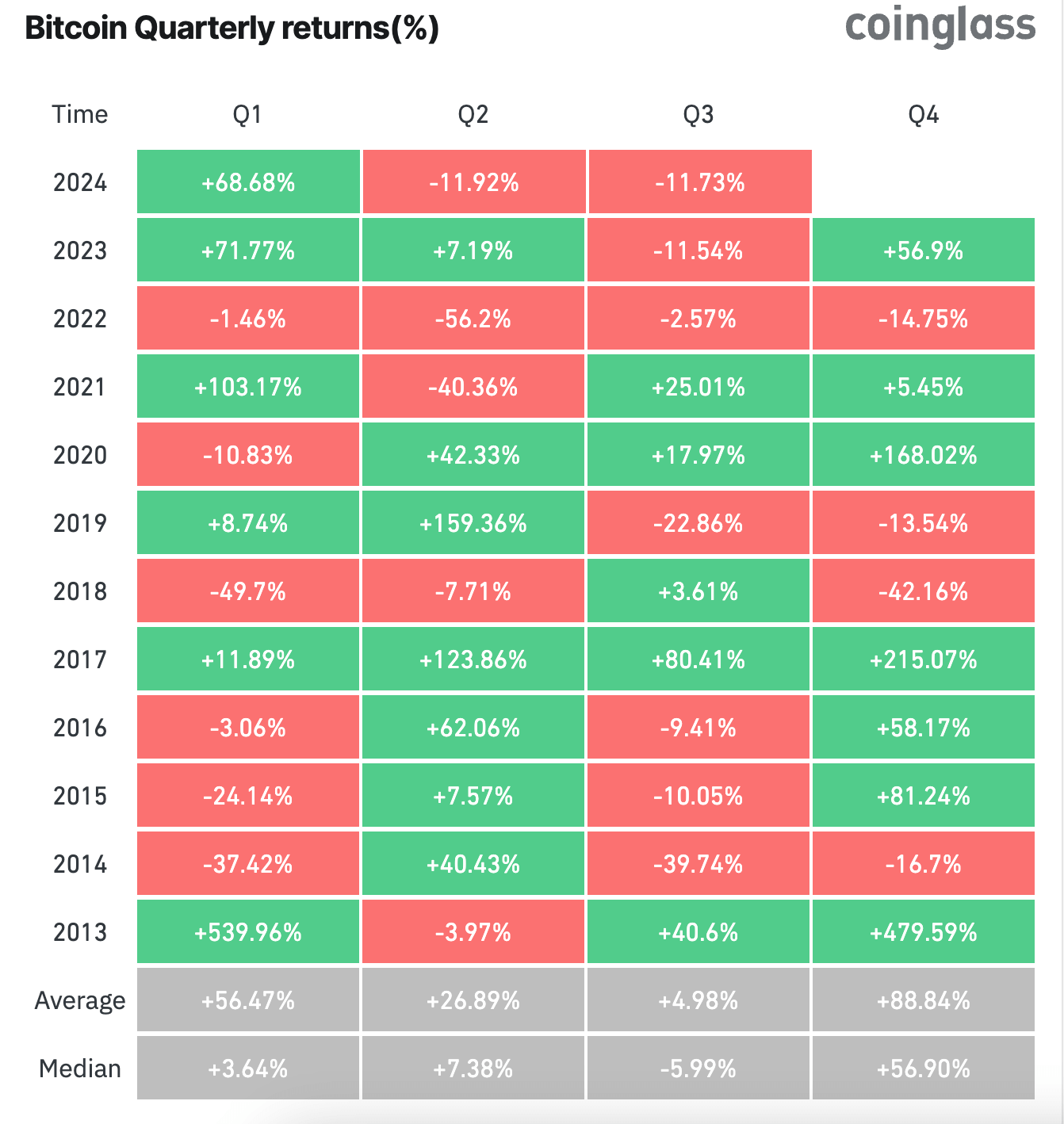

Historical quarterly performance

Looking across quarters, the data shows Bitcoin’s tendency to outperform in the first quarter (Q1) and the fourth quarter (Q4), while the second (Q2) and third (Q3) quarters tend to be more mixed.

Over the years, the average return for Q1 has been a strong +56.47%, and Q4 typically stands out with an average gain of +88.84%. However, the Q2 and Q3 averages show more variability, at +26.89% and +4.98%, respectively.

For instance, 2021 saw Bitcoin rise by an impressive +103.17% in Q1, followed by a sharp correction of -40.36% in Q2. However, despite this significant retracement, Bitcoin recovered +25.01% in Q3 before posting more modest gains of +5.45% in Q4.

In contrast, 2022 displayed one of Bitcoin’s worst overall annual performances. Q1 posted a slight loss of -1.46%, but Q2 saw a significant drop of -56.2%, exacerbated by global economic uncertainty and a crypto market downturn. Q3 attempted a recovery with a smaller decline of -2.57%, but Q4 also ended the year negatively with a loss of -10.45%.

The sharp losses in 2022 illustrate the importance of macroeconomic factors, including regulatory crackdowns and declining liquidity, which play critical roles in shaping Bitcoin’s quarterly performance.

In years like 2020 and 2017, Bitcoin showed substantial QoQ growth in Q4 after lackluster Q3 performance. In 2020, after a modest +17.97% gain in Q3, Bitcoin soared by +168.02% in Q4, driven by the increasing institutional adoption and heightened investor demand as the year ended.

Similarly, in 2017, Bitcoin followed up with a Q3 gain of +80.41% and a spectacular +215.07% in Q4, fueled by the retail FOMO that led to Bitcoin’s price reaching all-time highs.

Q3 weakness and Q4 recovery

Bitcoin has historically had a consistent trend of underperforming in Q3. Between 2013 and 2024, the average return for Q3 was only +4.98%, with a median of -5.99%. This trend can often be traced back to September’s persistent weakness, where the average monthly return is -4.89%, as Bitcoin typically faces a bearish period toward the end of Q3.

Table showing Bitcoin’s quarterly returns from 2013 to 2024 (Source: CoinGlass)

The data shows a robust historical recovery in Q4. This recurring pattern of weakness in Q3, followed by significant gains in Q4, can be attributed to several macroeconomic and market trends.

Institutional investors often harvest tax loss in Q3, selling off assets at a loss to offset capital gains from other investments. This trend tends to depress prices, especially in risk assets like Bitcoin. However, heading into Q4, these same investors often re-enter the market, reallocating capital as they position for year-end gains and new opportunities.

The 2020 and 2017 recoveries are prime examples of this Q3-Q4 trend. In 2020, Bitcoin followed a weak Q3 (+17.97%) with a massive rally of +168.02% in Q4, primarily driven by increased institutional interest, particularly from companies adding Bitcoin to their balance sheets.

Likewise, in 2017, after an already strong Q3 (+80.41%), Bitcoin exploded in Q4 (+215.07%) as retail investors poured into the market, pushing prices to new highs.

Bitcoin's 2024 performance

Bitcoin’s performance in 2024 started strong in the first quarter, followed by a series of pullbacks in the subsequent quarters, a pattern that aligns with historical trends. As of the end of Q3, Bitcoin has delivered a volatile but significant set of returns.

The year began with Bitcoin posting a modest +0.62% return in January, followed by an explosive +43.55% rise in February. March capped off Q1 with another strong performance, up +16.81%. Altogether, Q1 2024 saw Bitcoin rise by +68.68%, signaling a resurgence of institutional interest and a recovery from the prolonged bear market of 2022. This early-year surge was driven by several factors, including improving macroeconomic conditions, a slight easing in regulatory pressures, and renewed optimism among institutional investors.

However, Q2 2024 marked a reversal of fortunes. April saw Bitcoin dip by -14.76%, and while May brought a modest recovery with a +11.07% return, the quarter ended on a weak note, with June posting a loss of -6.9%. The overall Q2 result was a decline of -11.92%, reflecting the impact of rising interest rates, increasing regulatory scrutiny in key markets like the US, and reduced liquidity in crypto exchanges. This pullback mirrored Bitcoin’s historical tendency to cool off following a strong Q1, as seen in previous years like 2021 and 2019.

Q3 has continued this downward trend, with July managing only a +2.95% increase and August slipping by -8.6%. Preliminary September data indicates another potential decline, with early signs pointing to negative returns that may extend the current correction. As of mid-September, Bitcoin has been down by 11.73% for Q3, marking a continuation of historical patterns where Bitcoin typically experiences weakness in Q3 before a potential Q4 recovery.

September expectations

As stated above, September has historically been one of the worst-performing months for Bitcoin. Early indicators for the first few days of September also suggest a similar trajectory for 2024, with BTC continuing to face selling pressure.

Traditionally, in September, institutional investors reassess their portfolios ahead of Q4. This portfolio rebalancing often reduces risk exposure, with assets like Bitcoin typically seeing lower demand. Additionally, September often marks a transitional period where central banks, particularly the US Federal Reserve, release policy updates that influence risk sentiment across global markets. In 2024, continued uncertainty around inflation and interest rate hikes has likely played a role in Bitcoin’s underperformance.

Liquidity remains another issue. As institutional players recalibrate and traders reduce positions, liquidity in the crypto market tends to dry up. This reduced liquidity leads to exaggerated price movements, as smaller orders can disproportionately affect Bitcoin’s price. As a result, Bitcoin’s September performance often suffers from these macro trends and internal market factors.

Another significant factor that could influence Bitcoin’s price in September 2024 is the upcoming US presidential election in November. Historically, major political events such as presidential elections tend to heighten market volatility as investors assess potential changes in economic policy. In the lead-up to the election, all markets tend to see increased uncertainty. Given that Bitcoin has become a highly contested topic in the election, the outcome of this election has the potential to drastically change the regulatory landscape for the entire market. As a result, September 2024 could see additional volatility, with market participants positioning themselves ahead of potential policy shifts, exacerbating the month’s already historically bearish trend.

Predicting Q4 performance

The fourth quarter has been one of the strongest quarters for Bitcoin, with an average return of +88.84% and a median return of +56.90%. In several years, such as 2017 and 2020, Bitcoin posted significant gains in Q4 after experiencing weakness earlier in the year. For instance, in 2020, after a relatively modest Q3, Bitcoin surged by +168.02% in Q4, driven by growing institutional interest and favorable market conditions.

These historical trends suggest that while Bitcoin may experience a September dip, there is a strong possibility of a Q4 recovery. That being said, it’s important to note that each market cycle is unique. While historical patterns offer valuable insights, they do not guarantee future performance.

Based on Bitcoin’s historical Q4 performance, there are several reasons to believe it could rebound and finish 2024 with a positive return. One key factor is macroeconomic catalysts. As we move into the year’s final quarter, institutional investors often re-enter the market after Q3 portfolio rebalancing. This can increase buying pressure, especially in risk assets like Bitcoin. Additionally, Q4 is typically characterized by more favorable liquidity conditions, which could further support a price recovery.

Another potential driver of a Q4 rebound in 2024 is market sentiment. Historically, Bitcoin tends to perform well in the year’s final quarter as investor optimism grows ahead of year-end. This sentiment is often driven by anticipation of positive macroeconomic developments, including potential monetary policy shifts from central banks or improving global economic conditions. If inflationary pressures ease or interest rate hikes slow down, it could create a more favorable environment for risk assets, including Bitcoin.

Despite these positive factors, there are also risks and uncertainties that could hamper Bitcoin’s Q4 recovery. One significant risk is the ongoing global economic instability. If inflation remains persistently high or central banks continue to raise interest rates to combat inflation, it could create a challenging environment for risk assets. In such a scenario, Bitcoin could struggle to gain traction, as investors may continue to favor more stable assets like bonds or commodities.

Regulatory crackdowns are another potential headwind. The results of the upcoming US Presidential elections could drastically increase volatility, dampening Q4 performance.

While historical trends suggest a strong possibility of a Q4 recovery for Bitcoin, investors should remain cautious given the ongoing macroeconomic challenges and regulatory uncertainties. If the broader economic environment stabilizes and regulatory developments favorably, Bitcoin could finish 2024 positively.