Blockstack reports insane user growth, but crypto analysts think it’s a money grab

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

Blockstack – a “decentralized computing network and app ecosystem” – announced in a recent blog post that they hit a massive network milestone of acquiring one million users on the platform, allowing them to unlock $6.8 million in additional funding, per the terms of their 2017 crypto token offering.

It is important to note that this shocking news regarding the platform’s meteoric growth has drawn the skepticism of analysts within the crypto industry, with some noting that it seems to be a simple money grab.

Blockstack sees unprecedented user growth, unlocks massive crypto funding

Recently, it was announced that Blockstack had passed the one million verified user milestone, thus allowing them to access $6.5 million in achievement-based funding that was locked following their crypto token raise in 2017.

When Blockstack conducted its Initial Coin Offering for the crypto token associated with their platform – dubbed STX – they put in place a legal mechanism that would only allow them to access portions of the funds raised from investors based on their achievements.

This type of system incentives the team to reach goals in an expedited manner, and it offers some peace of mind to investors.

In spite of this, the merit of this system is now being questioned, as some analysts believe that the company may simply be lying about their growth in order to access the locked funding.

Larry Cermak, the Director of Research at The Block, mused this possibility in a recent tweet while referencing the news about Blockstack’s massive user growth, saying:

“Blockstack apparently has one million verified users, which unlocks $6.8 million for them. That’s more than Bitcoin active addresses. And Blockstack has less than 36k followers on Twitter. But suuuure, they have one million verified users.”

Blockstack clarifies that users are not the same as “usernames”

The blowback from their announcement regarding having one million users led them to address the controversy in a follow-up blog post, in which they note that they have on-boarded over 1 million registered usernames, not users, claiming that this fits the initial premises of their ICO’s original legal parameters.

“Blockstack PBC has on-boarded over 1 million registered usernames… That being said, registered usernames are not the same as daily active users, nor have they ever been presented as such. Back in 2017, when we were setting up the legal definition of users in the self-imposed milestone, we precisely defined a user as a registered username on the blockchain (not active user).”

It does appear that this whole imbroglio has boiled down to a debate surrounding legal jargon, but the bottom line is that this milestone achievement allowed the company to unlock a significant amount of capital – regardless of whether or not it was achieved legitimately.

This controversy also shines a light on the fact that it is difficult for investors to verify a crypto project’s quantifiable progress.

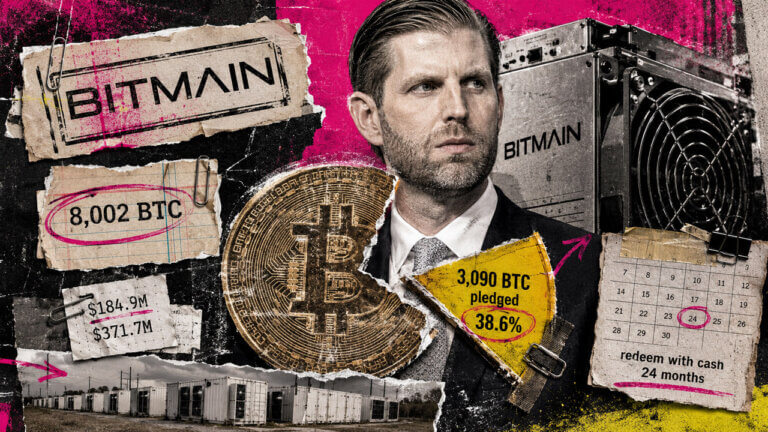

Eric Trump’s American Bitcoin has pledged nearly 40% of its Bitcoin to buy mining equipment

Nearly 40% of American Bitcoin’s 8,002 BTC reserve is tied to Bitmain mining equipment agreements that could move the coins off its balance sheet.

Airbnb CEO retracts positive tokenization statements claiming social media was hacked

Chesky announced no product. His trust thesis points toward regulated financing built on verified bookings, contingent payouts and specialist-held legal claims.

Crypto hacks hit a record count but the biggest threat isn’t smart contracts

The industry's security problem is changing shape: more hacks, lower typical losses, and a handful of infrastructure compromises still defining the first half's damage.