Stablecoin boom doesn’t guarantee Bitcoin price will explode higher: economists

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

With Bitcoin seemingly finding a local top, all eyes in the crypto space have migrated to stablecoins, digital assets tied to and backed by a “stable” reserve asset. Although present in the cryptocurrency industry for 2017 and 2018, the assets have become increasingly important to the market over the past few months, as they've grown in supply.

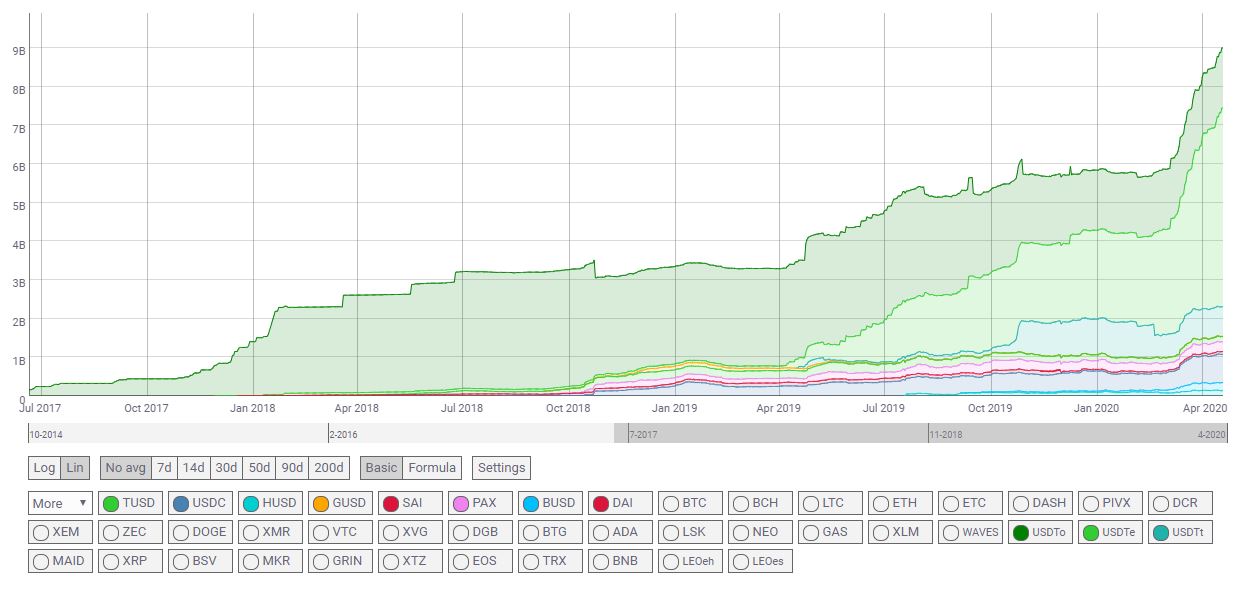

In fact, per recent data from blockchain analytics firm Coin Metrics, the value of all stablecoins in circulation just passed over $9 billion for the first time ever. What's especially interesting about this stat is six weeks ago, the aggregate value of all stablecoins was $6 billion.

That's 50 percent growth in a multi-billion-dollar statistic within a month and a half, making it clear that it isn't only central banks that are having their money printers operating at full speed. (Three hours ago as of the time of this article's writing, yet another $120 million worth of USDT was tacked onto the chart below.)

The common narrative goes that this is decisively bullish for the crypto market; investors say that the growth in stablecoin supply is indicative of money prepared to buy Bitcoin, Ethereum, and other cryptocurrencies.

But, a new report from economists has suggested that this narrative isn't 100 percent true.

Economists: Stablecoin boom isn't bullish for Bitcoin, it's neutral if anything

In a note titled “Stable coins don't inflate crypto markets” and published to economics research blog VOX, Richard K. Lyons and Ganesh Visawanath-Natraj — of UC Berkeley and Warwick Business School, respectively — poo-pooed on the sentiment that stablecoins will push Bitcoin higher.

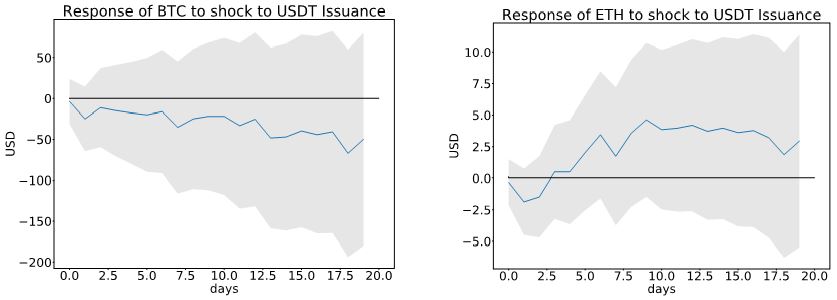

The core of their argument came down to the two charts seen below, which depict the average performance of both Bitcoin and Ethereum — two of USDT's biggest crypto markets — in the wake of Tether's issuance of coins.

They found that from August 2017 to November 2019, there was no obvious trend to the prices of BTC and ETH in the three weeks after USDT issuances.

In fact, on average over the sampled time frame, Bitcoin trended lower immediately after Tether minted coins, but that trend may just be related to the fact the period they observed was marked by bear trends.

Notably, the data they sampled doesn't take the past few months into account, which have contained the biggest bouts of USDT's growth ever, and may have skewed their thesis and conclusion.

Even still, they came to the following conclusion:

“This column answers a series of questions relevant to whether stable coins have an inflationary effect on crypto asset prices. The bottom line: We find no systematic evidence that stable coin issuance affects cryptocurrency prices. Rather, our evidence supports alternative views.”

What's behind the trend then?

That begs the following question: if it isn't buyers looking to buy Bitcoin, who's or what is behind the surge in demand for stablecoins?

According to them, the minting of stablecoins coincides with “deviations of the secondary market rate” of USDT compared to the pegged rate of $1, suggesting that it is arbitrageurs that are causing the stock of stablecoins to increase. This, the economists claimed, is a sign that Tether acts as a reserve asset for cryptocurrency investors, as opposed to “real” dollars:

“In periods of risk, some investors will choose to exchange into a better store of value. Portfolio rebalancing toward Tether and other stable coins provide this function with minimal intermediation costs.”

After all, USDT is simply more available and liquid than Bitcoin-to-fiat currency trading pairs.

This is an assertion very similar to that made by Sam Bankman-Fried, CEO of crypto exchange FTX and crypto fund and OTC desk Alameda Research.

Per previous reports from CryptoSlate, he said that per his data, the phenomenon of the rapidly-increasing stock of USDT is primarily due to traders selling Bitcoin to USDT to hedge risk, just as the economists in the VOX column described.

Tether claims $1.5B profit, but hidden math reveals a $4.2B hit that halved its safety cushion in 90 days

Tether’s attestations imply a $4.2 billion Q2 financial hit, cutting its reserve cushion to $4.1 billion, or 2.2% of liabilities.

Circle is arming USDC with 1,000 IBM patents to secure its grip on global banking rails

USDC leads adjusted transaction volume, but Tether retains scale while OUSD targets Circle’s institutional economics.

US turns stablecoin issuer Tether into a financial weapon against Iran, freezing nearly $500 million

Tether’s ability to blacklist wallets has given U.S. authorities a new point of control over offshore digital funds.

Bitcoin price breaking out toward $69,000 now opens a turbo path toward $84,000

A Bitcoin breakout above $69,000 could open a thinner supply zone toward $84,000, but Friday’s jobs report and weak ETF demand may decide whether the move holds.

A massive 100 million PROVE tokens unlock today, but razor-thin liquidity reveals a market unprepared for a 51% supply shock

CoinGecko shows 208.33 million and Tokenomics.com 233.332 million, but accessible official terms confirm only the investor-and-contributor tranche.

USDC redemptions just outpaced mints by $4B, but a massive new token presale is quietly doubling Circle’s revenue outlook

Redemptions exceeded mints, yet circulation rose 19% as lower reserve yield sharpened attention on an undisclosed ARC Token contribution.