Virtual card creation is fast. Physical delivery, cash access, and edge-case support are slower and less clearly defined.

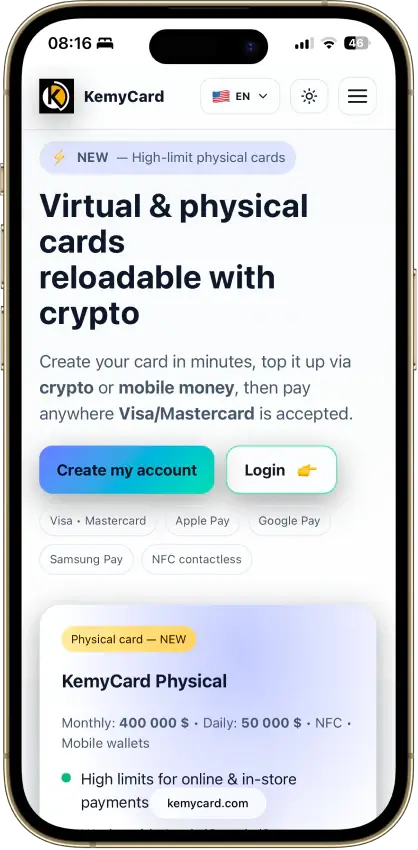

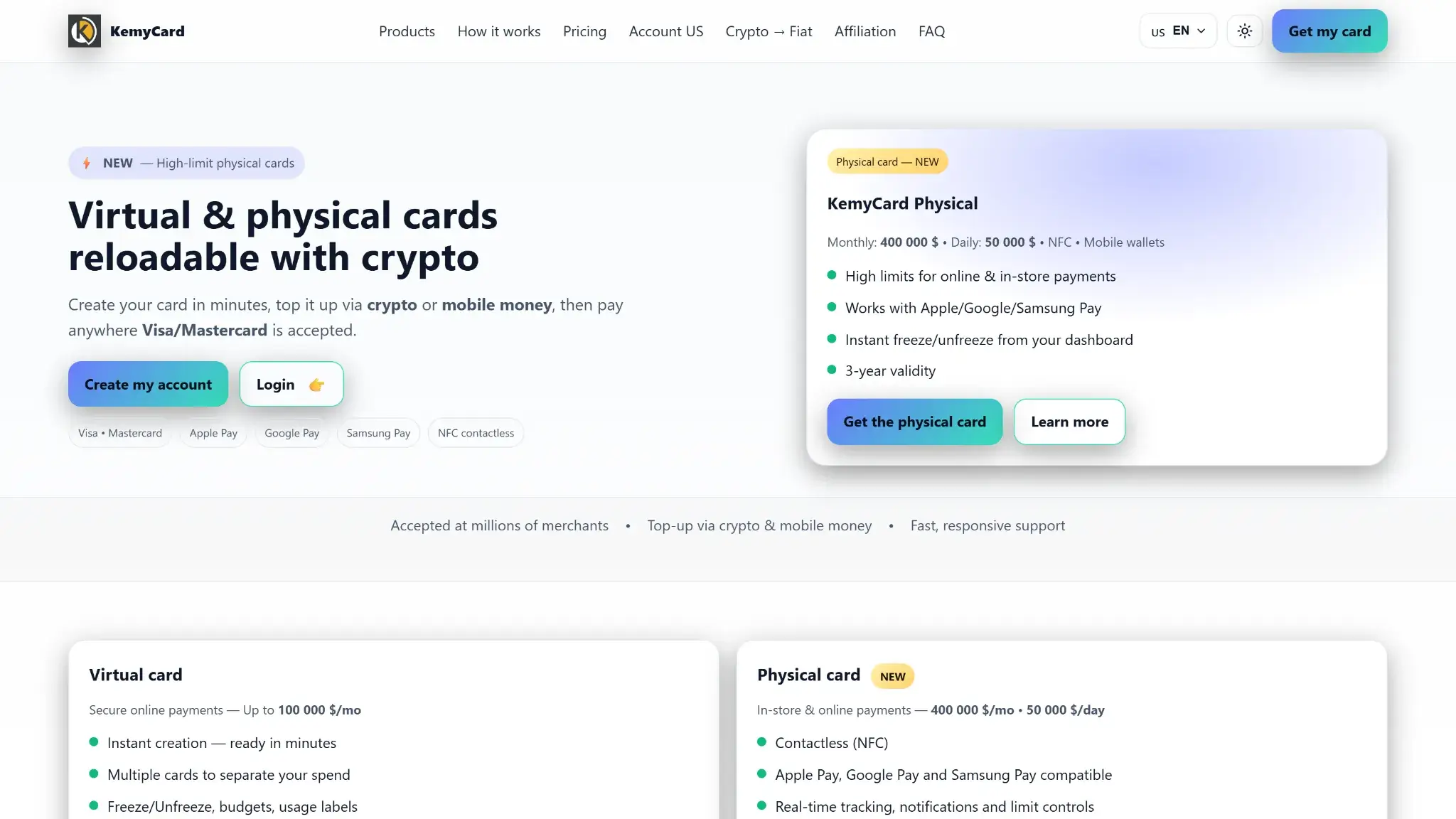

Virtual Card SetupVirtual card creation is framed around minutes, not days. Fast setup does not mean immediate unrestricted access.

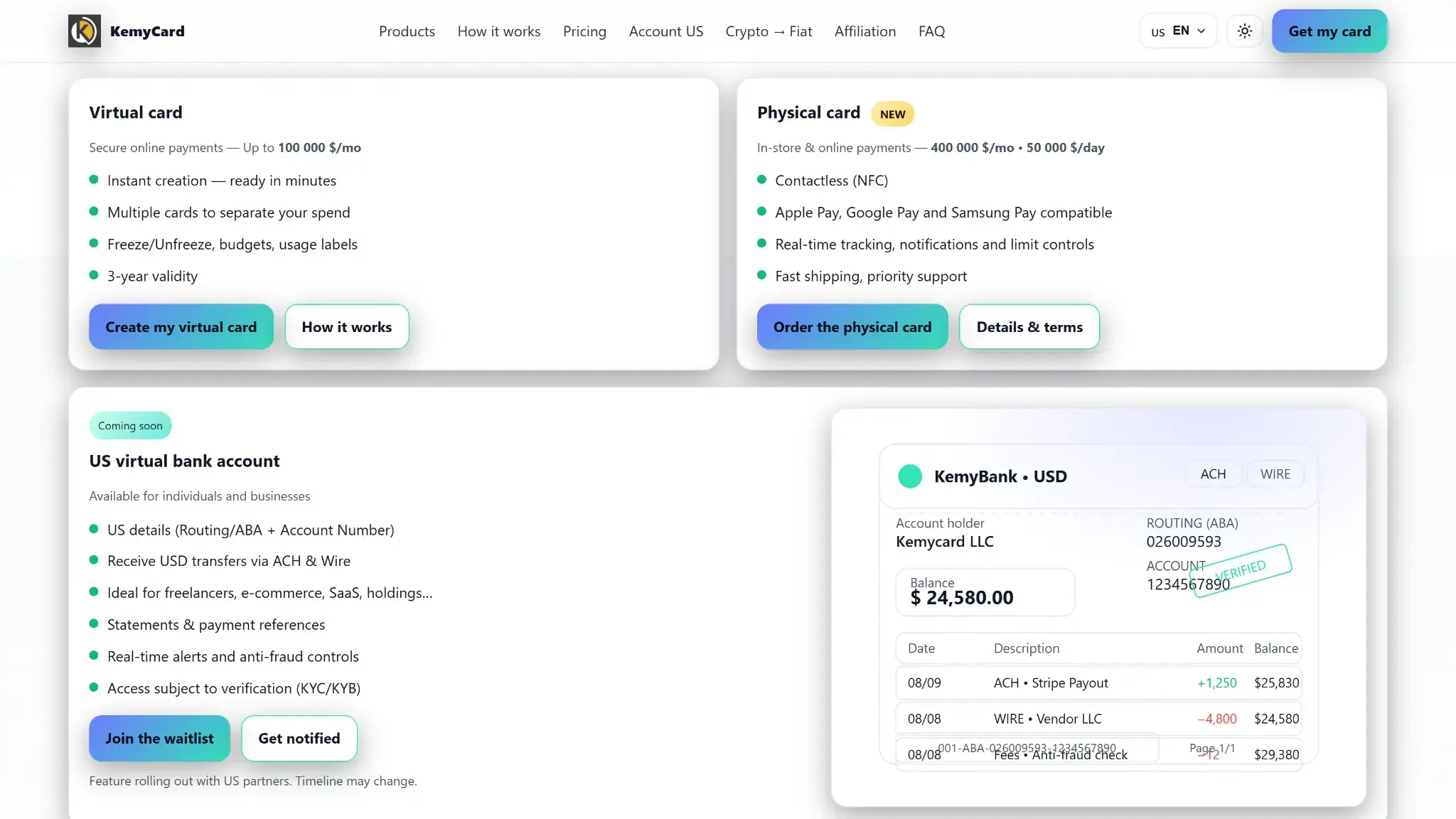

Physical Card DeliveryPhysical card delivery uses DHL Express.

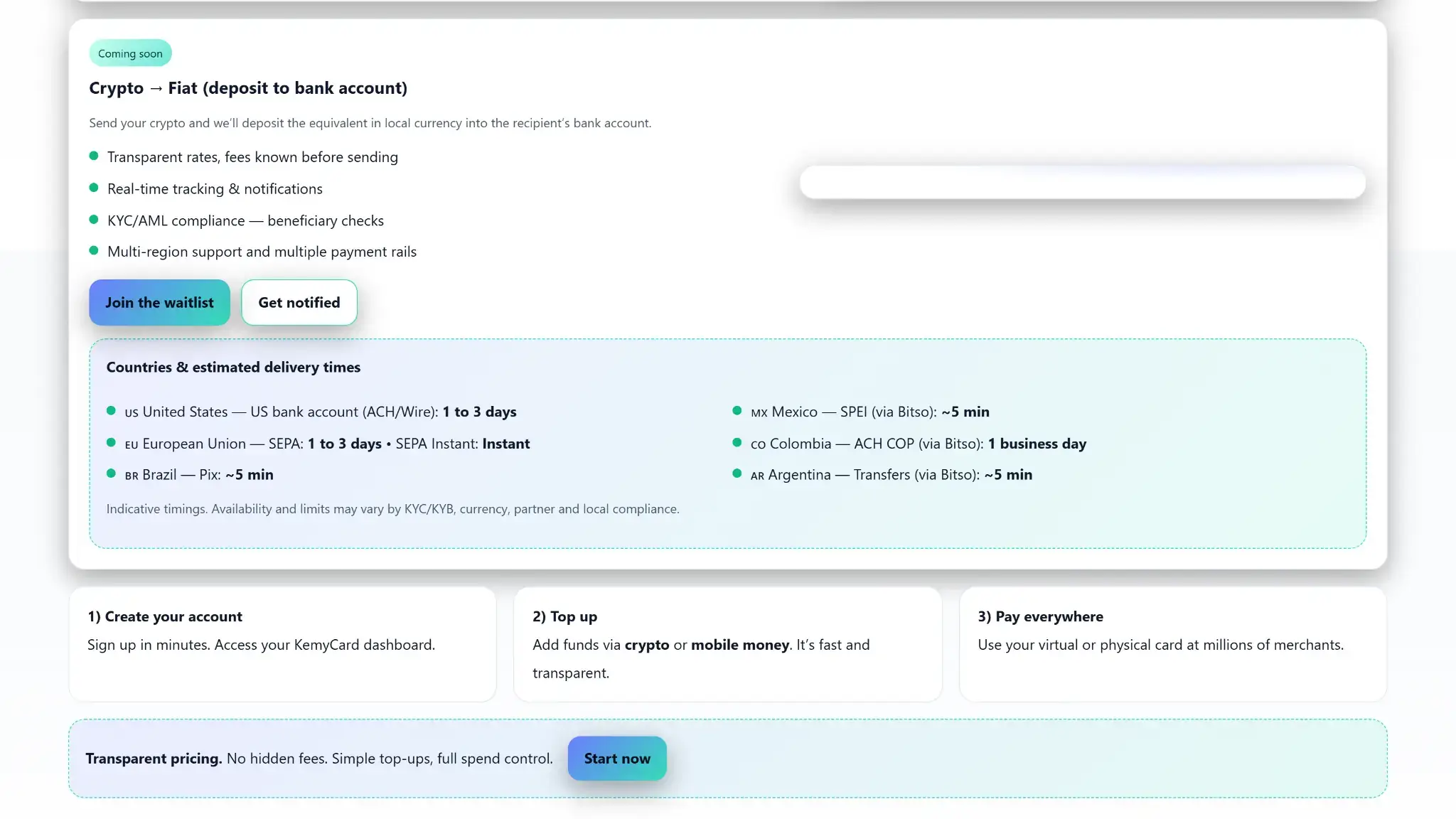

Funding To SpendFunds become spendable after crypto confirmation or mobile money processing. Timing depends on the rail used and any review that follows.

Compliance ClearanceNo public timing is disclosed. Fast signup does not guarantee fast clearance.

Virtual Card Limits$100,000 ceiling and $10,000 max per transaction. Strong enough for large online payments.

Physical Card Balance$400,000 maximum balance. Higher than most consumer card limits.

Physical Transaction Limit$25,000 max per transaction. Better suited to larger purchases than many rivals.

Physical Spend Limit$50,000 daily spend and a $400,000 monthly spend ceiling. Spend capacity is much stronger than cash access.

Spending CeilingsCertain security-related changes can temporarily reduce card spending to $1,000 per transaction and $1,000 per day for 24 hours.

ATM AccessPhysical card only. No cash access from the virtual card.

ATM Withdrawal Limits$500 per day and $15,000 per month. Cash withdrawals are much tighter than card spend limits.

Refund TimingNot disclosed. Hard to plan around merchant reversals or disputes.

Reversal TimingNot disclosed. The same uncertainty applies to canceled or failed transactions.

Common Delay PointsBlockchain confirmation, mobile money processing, compliance review, and physical shipping. Delays usually sit outside the card swipe itself.

KemyCard approves and issues virtually fast. Funding speed depends on the rail. Spending is faster once the balance is live. Cash access is slower and depends on the physical card and tighter ATM limits.