Bitcoin’s hard-money thesis is colliding with 5% Treasury yields

The bond market was supposed to be Bitcoin's origin story, not its daily price driver. And yet here we are in May 2026, watching crypto traders refresh yield curves on a Saturday morning.

Bitcoin was created as a response to the kind of debt-financed monetary disorder now playing out across global bond markets. The original thesis was that when governments borrowed recklessly and debased their currencies, hard-money assets would absorb the resulting demand.

What that thesis left unresolved is the possibility that the debt spiral could tighten financial conditions strong enough to suppress speculative assets before the hard-money argument has time to play out.

In 2026, the long-term narrative and the short-term mechanics are running in opposite directions, and understanding why requires spending a few minutes with the most consequential number in global finance right now.

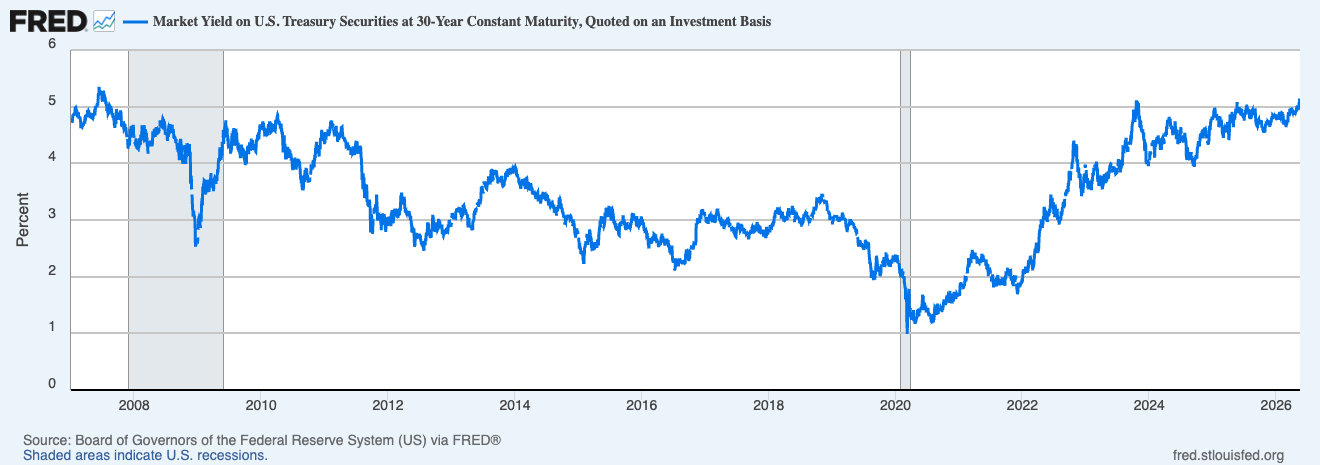

On May 20, the 30-year Treasury yield reached 5.18%. A $25 billion auction of new 30-year bonds on May 13 was awarded at 5.046%, the first time investors have received 5% on the long bond since 2007, driven by surging energy prices and rising expectations that inflation could prove more durable than markets assumed.

The last time yields were at these levels, Bear Stearns was still a concern, and quantitative easing was still a theoretical concept. Everything that's happened in markets since (the post-2008 era of suppressed rates, central bank asset purchases, near-zero borrowing costs) was predicated on yields eventually coming back down and staying there, and the current repricing is challenging that assumption across the entire curve.

America is borrowing money to pay interest on borrowed money

The inflation drivers behind this move are well documented: US Treasury yields moved higher as investors weighed the implications of more costly energy prices tied to the Iran war, with WTI crude settling above $106 a barrel and Brent climbing to $114.44.

Energy is a real factor, but the deeper structural force (and the one with more staying power) is the sheer volume of US government debt that has to be refinanced and issued into a market that's already repricing inflation risk. The US Treasury will likely have borrowed more than $2 trillion by the end of the fiscal year, with the Office of Management and Budget projecting a deficit of $2.06 trillion for FY2026, higher than the Congressional Budget Office estimates.

To service that borrowing, the Treasury paid out nearly $530 billion in interest between October 2025 and March 2026, more than $88 billion a month, a figure that's roughly equal to spending on both the Department of Defense and the Department of Education combined.

This problem feeds on itself. Interest payments on the national debt have been 6.1% higher than the previous year through the sixth month of FY2026 and have become the second-largest spending category in the federal budget, outpacing all budget categories except Social Security. The CBO projects those annual costs climbing from $1 trillion in 2026 to $2.1 trillion by 2036.

Meanwhile, the Treasury's own borrowing calendar keeps upward force on the long end, with $189 billion expected in the second quarter and $671 billion in the third, meaning the bond selloff has shelf life well beyond any individual Iran headline.

This is what the bond market is actually pricing: weak foreign demand, enormous supply, and an inflation backdrop that's giving the Federal Reserve very little room to maneuver. Futures markets now assign more than a 44% chance of a Fed rate increase by December, a sharp shift from expectations of multiple cuts earlier in the year. Barclays has moved its first expected Fed cut to March 2027. Rate cuts, which crypto markets spent most of 2024 and 2025 treating as a reliable tailwind, are now being actively repriced off the table.

How a Treasury auction ended up moving Bitcoin

Bitcoin's retreat below $80,000 last week shows how quickly the bond market has reclaimed control of crypto trading, even after lawmakers advanced one of the industry's most closely watched regulatory bills.

The CLARITY Act was expected to generate a sustained positive tone across the crypto market.

Instead, US spot Bitcoin ETFs saw roughly 14,000 BTC in weekly outflows, ending a six-week inflow streak, as hotter inflation data forced markets to reassess risk exposure. Spot net-volume on Binance dropped from approximately $50 million to $6.5 million, and on Coinbase from $30 million to $5.7 million.

This is a direct transmission mechanism. An institutional allocator who can now get 5% on a 30-year government bond, guaranteed, faces a different decision than one who was working with 3.5% yields two years ago. Rising Treasury yields raise the opportunity cost of holding a volatile, non-yielding asset like BTC, making institutional buyers more selective as government debt offers a stronger return profile.

Tokenized US Treasuries have hit a record $15.35 billion in on-chain market value, up roughly 70% year-to-date, as yield-sensitive capital finds a home that combines crypto infrastructure with bond-market returns.

This is the structural consequence of the ETF era that CryptoSlate has been tracking: Bitcoin is now embedded in traditional portfolio allocation frameworks, which means it responds to the same macro inputs as any other risk asset. Before ETFs, crypto traded largely on its own internal dynamics, driven by altcoin rotations, on-chain metrics, and retail sentiment.

Today, a Treasury auction that prices 20 basis points above expectations can move BTC faster than any on-chain development. As CryptoSlate noted in late April, Bitcoin's recovery rests on renewed institutional inflows and the assumption that liquidity conditions won't tighten again. And if Treasuries choose a direction before that assumption is tested, the bond market could drive Bitcoin's next move independently of any crypto-specific catalyst.

Strategy adds another layer of complexity here. JPMorgan estimated in early May that Strategy could purchase roughly $30 billion in Bitcoin through 2026 if it maintains its current purchasing pace, a figure that would put it alongside ETF flows and miner supply as one of the strongest structural forces in Bitcoin's demand.

The complication is that Strategy's capital structure, which relies on issuing equity and preferred stock to fund its Bitcoin purchases, becomes more expensive to operate as yields rise and borrowing costs across the system increase. The higher yields climb, the more the flywheel depends on sustained investor appetite for a model that converts yield demand into BTC demand.

The paradox Bitcoin was built for

There's a longer argument worth holding onto here, even amid the short-term pressure. The rotation out of traditional safe havens into Bitcoin as a perceived alternative store of value reflects the fiat debasement narrative gaining renewed traction as fiscal deficits expand and central bank balance sheets remain structurally large.

As sovereign debt sustainability concerns accumulate and the rate of American borrowing becomes harder to ignore, the long-cycle argument for Bitcoin as a monetary hedge tends to grow alongside it.

In the near term, 5% Treasury yields are a headwind: they tighten financial conditions, raise the opportunity cost of speculative positions, and drain the marginal liquidity that's historically fueled Bitcoin's larger rallies.

Across a longer horizon, though, the fiscal conditions producing those yields, deficits projected to increase from 5.8% of GDP in 2026 to 6.7% in 2036, with net interest payments growing each year in relation to the size of the economy, are precisely the conditions that make a hard-money, fixed-supply asset like Bitcoin compelling to a growing class of institutional holders.

For years, crypto markets obsessed over the Federal Reserve, watching rate decisions and dot plots as the primary macro input. What 2026 is making clear is that the Fed's room to maneuver is increasingly constrained by a bond market pricing in something more durable than a temporary inflation spike.

The next phase of Bitcoin's trajectory won't depend on what central bankers decide, but on whether global bond investors are beginning to lose patience with the American debt. Which is, if you trace it all the way back, precisely the scenario Bitcoin was designed to outlast.