US economic indicators point towards contraction as unemployment stays at historic lows: MacroSlate Weekly

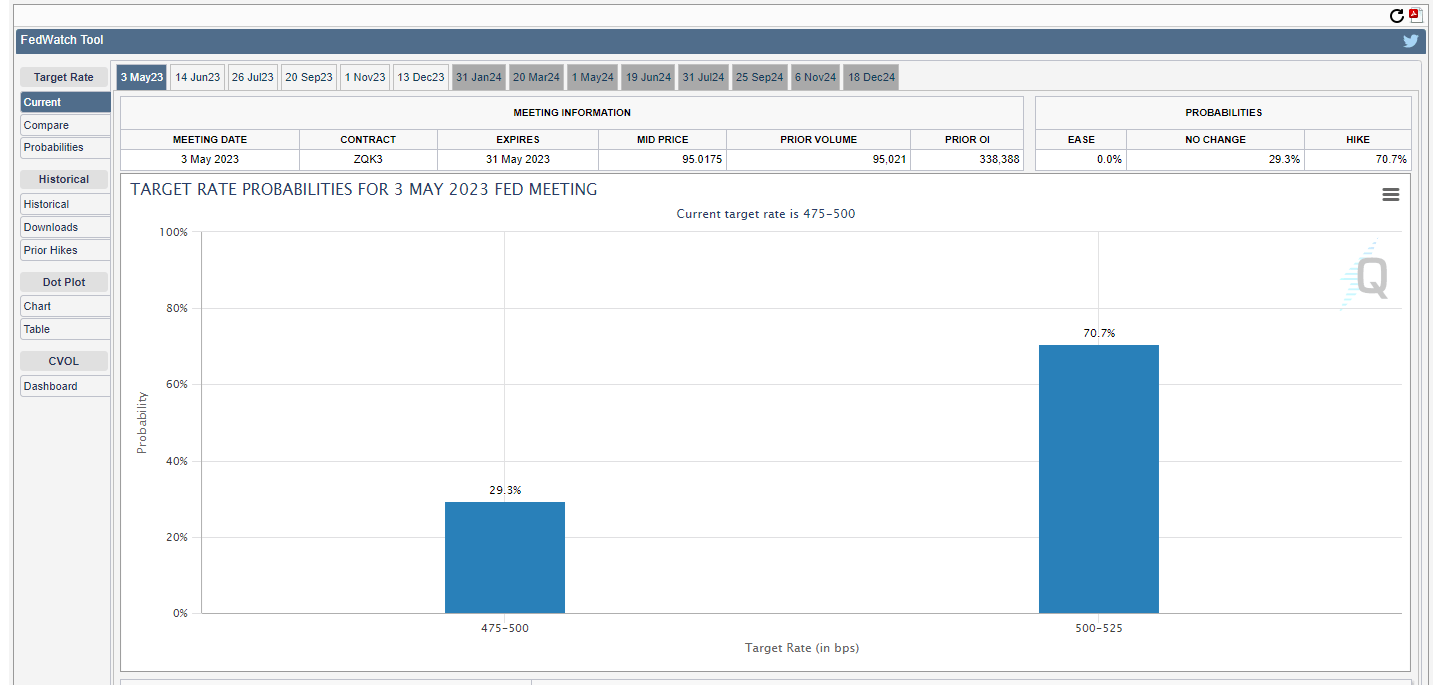

Markets now see a 69% chance of another .25 rate hike at the May FOMC meeting

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

GFC vs. 2023

It seems contraction in the U.S. economy is starting to appear. However, a recession is not scheduled for the time being. Comparing previous eras and recessions might fit human psychology, but it will undoubtedly be different. But most likely, the Federal Reserve will continue to hike rates until something materially breaks.

We have had a banking crisis, which is fundamentally different from 2008. In 2008, we had mortgage defaults and saw a knock-on effect with house prices falling drastically. At the same time, banks had deep losses on loans on their balance sheets. SVB was fundamentally different as depositors panicked about severe unrealized losses on their treasury portfolio.

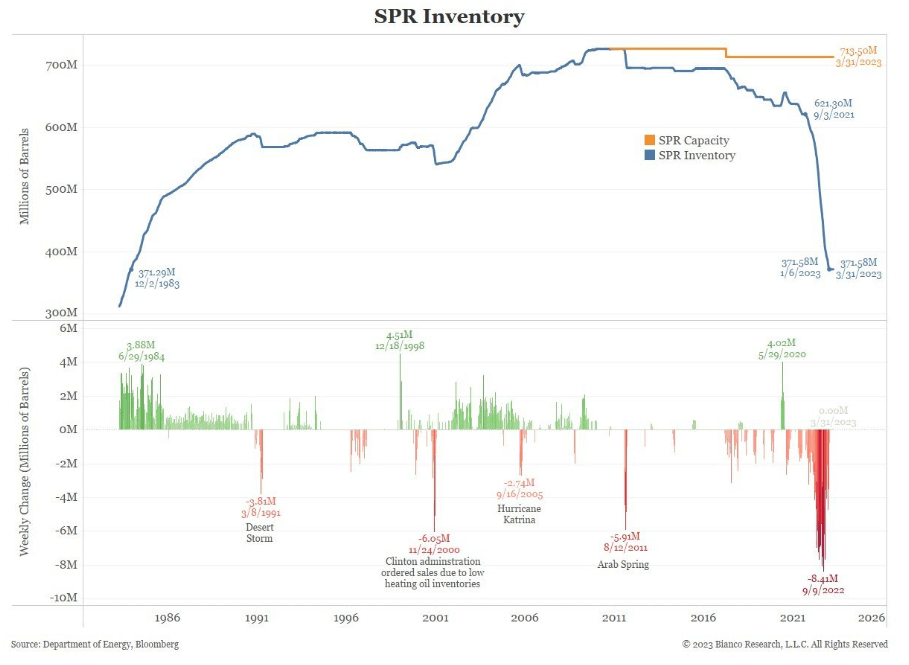

OPEC +

To start the week, we had OPEC + announcement of cutting over 1m barrels/day starting next month, while 2m barrels/day are being cut from October. CryptoSlate analyzed the repercussions of these cuts; not only is this pure signal of demand collapsing. It also left the Biden administration in trouble after drawing down on the Strategic Petroleum Reserve while failing to build on the reserves when prices were surpassed. Crude Oil WTI (NYM $/bbl) closed the week at $80/ barrel while it was as low as $67, with some analysts expecting triple digits.

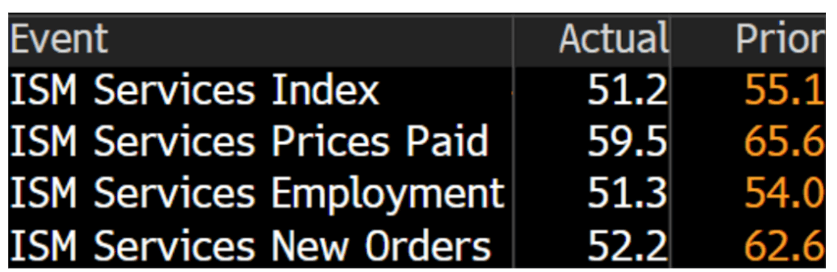

U.S. manufacturing slumps

The March ISM manufacturing survey continued its decline, staying within the contraction zone of 46.3, undershooting expectations. In addition, JOLTS data printed 9.93 million vs. the 10.5 million expected. This was the smallest print since April 2021. While every part of ISM Services PMI also continued to drop. New orders are down to 52.2 from 62.6.

Unemployment at record lows

Staggeringly, unemployment dropped to 3.5% from 3.6%. At the same time, the U.S. Bureau of Labor Statistics employment report showed 236,000 nonfarm jobs added for March. Economists expected 239,000 jobs.

As a result, we now see a 69% chance of another .25 rate hike at the May FOMC. This would put the federal funds rate over 5%.

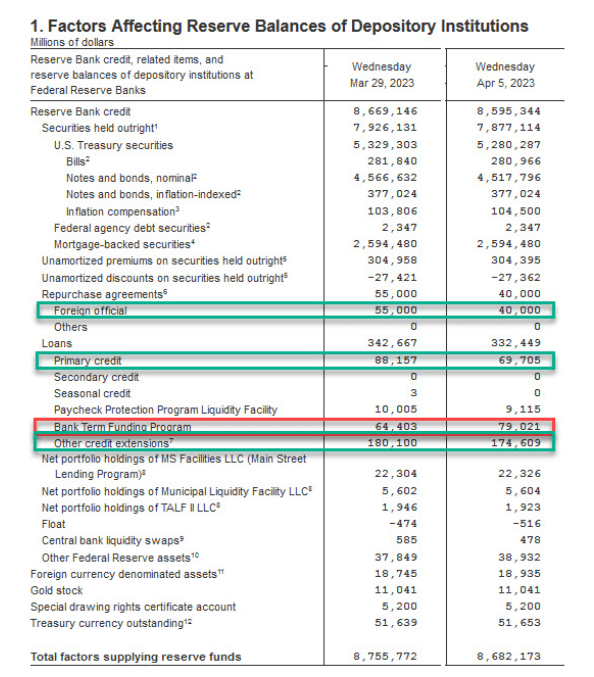

Fed balance sheet update

Thursday afternoon clock watch of the fed balance sheet is now becoming a main event. The fed balance sheet fell by $74 billion this week, roughly reduced by $100 billion in the past two weeks. The fed balance sheet is now shrinking faster than before the SVB collapse.

This shows fewer banks and less distressed assets are needed to be supported by the Fed. In addition, BTFP loans rose to $79 billion from $64.4 billion as the Fed discount window usage dropped to $69.7 billion from $88.2 billion.

It's safe to say this was not a round of quantitative easing but short-term emergency loans that will be paid back.

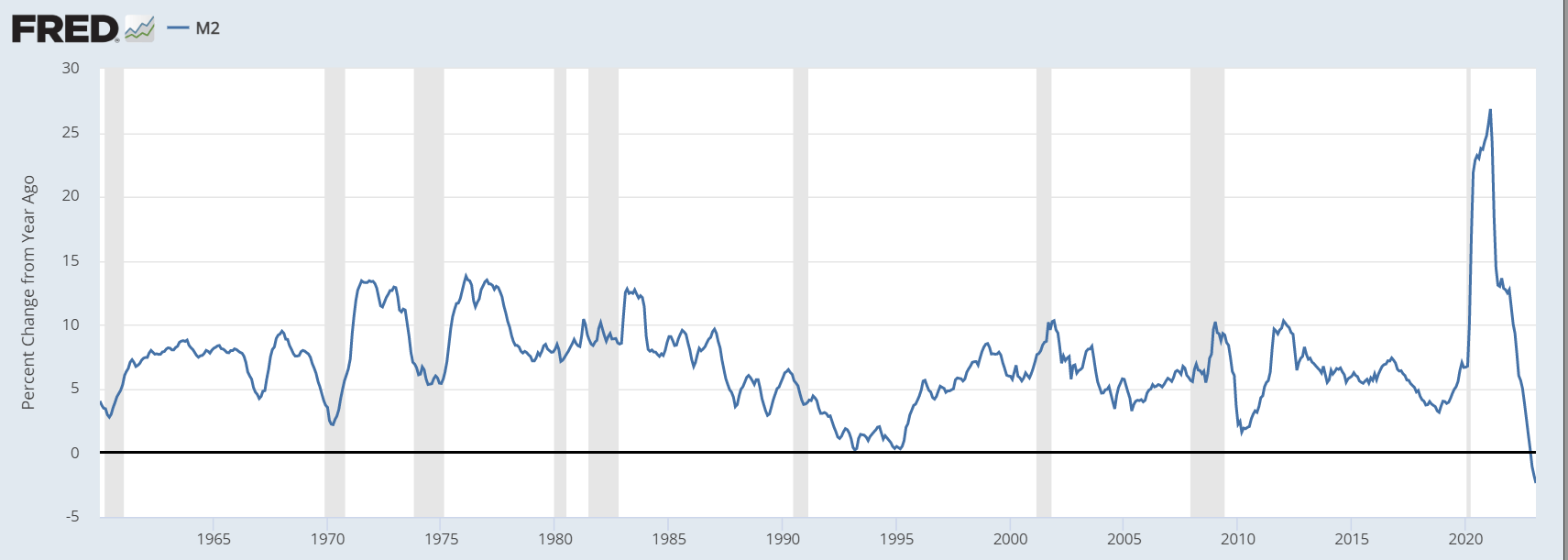

But the key issues here are quantitative tightening and liquidity being drained from the system. We have witnessed the fastest tightening cycle in history; the money supply measured by M2 has fallen 2.5% since last year, the sharpest deterioration since the great depression in 1929.

Even small contractions in the money supply can cause big economic problems and lead to bank runs. You would assume banks will start to cut back lending and hold more cash on hand, which will potentially cause a credit crunch. No doubt lending standards will tighten.

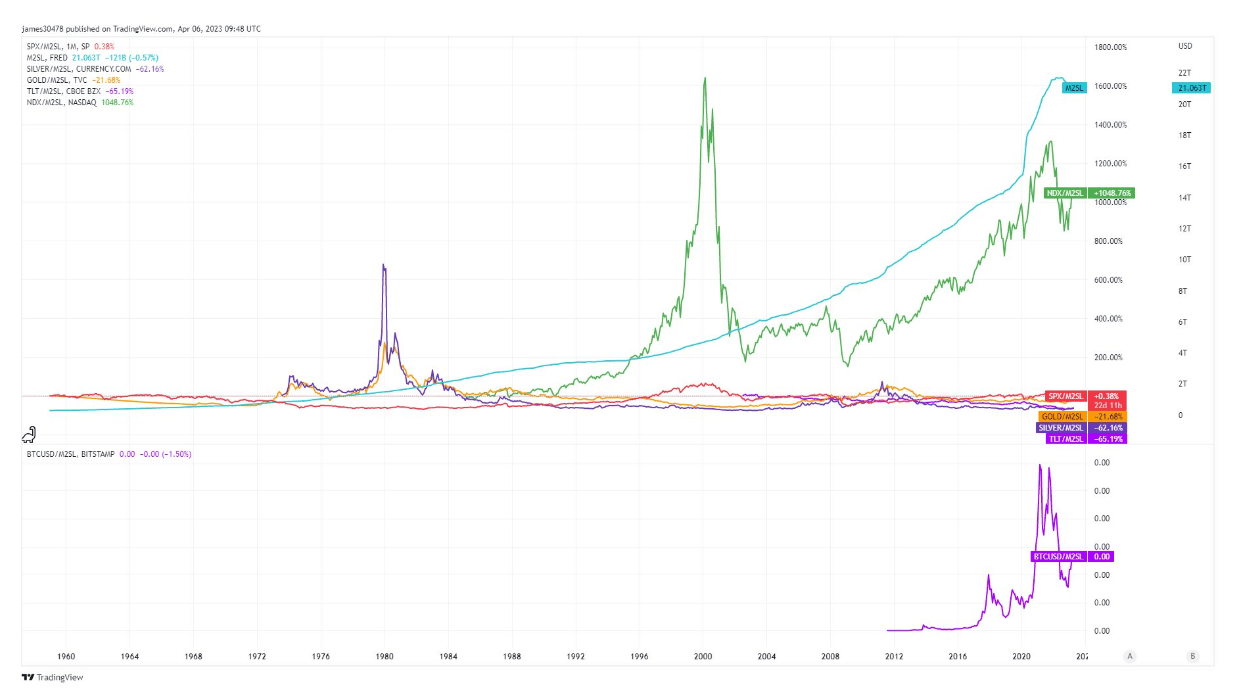

Bitcoin vs. M2

In the short term, it is very hard to give definitive answers about a credit crunch, a recession, and if Bitcoin will exceed a certain price target. But we champion Bitcoin because it's an asset that allows you to ignore all the macro uncertainty and geo-political games and focus on the bigger task at hand. An asset with no counter-party risk doesn't suffer from the contagion potential of TradFi assets.

The long game is money supply will continue to expand; the balance sheet will expand, inevitably inflating all our assets.

CryptoSlate analyzed major assets vs. M2 money supply, and it's clear to see one winner in this game. The illusion of money printing makes you think you are getting wealthier; however, in real terms, you are not even staying afloat.

Bitcoin remains the number one asset to keep you ahead of the devaluation of the currency.

TeraWulf’s Bitcoin mining revenue fell 73% as AI related leases reached 71% of sales

HPC leasing generated $31.9 million in the quarter as the company spent heavily to expand its data-center capacity.

Bitcoin treasury Strive bought 20 BTC, but 110,000 new shares left holders with less Bitcoin exposure

Bitcoin holdings rose 0.10%, while effective common shares increased 0.13% and trimmed gross per-share exposure by about 0.03%.

How dumping 1,200 Bitcoin helped a cellular chipmaker completely erase its debt and double its cash

The chipmaker ended June with 314 unrestricted coins after sales helped erase convertible debt and lift cash to $21 million.

Tomorrow sees a massive liquidity trap for Bitcoin as the US Treasury is quietly draining $77 billion from bank reserves

The Aug. 5 bill-coupon mix will show whether financing pressure reaches Bitcoin-sensitive risk appetite or leaves reserves stable.

Why Bitcoiners should care that Washington joined a $96B yen rescue to shield over $1 trillion in US Treasuries

Preliminary BOJ data suggest Tokyo intervened over two days as rising Japanese bond yields threaten to pull capital from global risk markets.

Bitcoin must clear $65,000 before Friday, or jobs data could turn $62,000 into a trapdoor to $60,000

Bitcoin faces a week of jobs data with $65,000 as the breakout level and $62,000 as the line protecting a slide toward $60,000.