Spending crypto in the real world used to mean jumping through hoops. Today, a handful of cards make it straightforward — but straightforward does not mean identical. The gap between the best crypto cards and the ones that eat into your balance through fees, spreads, and fine print is wide enough to matter.

This page compares the leading options across rewards, fees, conversion costs, limits, and usability. Whether you want a crypto debit card for everyday spending, a crypto credit card for rewards, or a virtual crypto card you can use within minutes, the right choice depends on how you actually spend, what fees you can absorb, and whether the reward structure works for your region and funding style.

Top Crypto Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Fast virtual card access

- Broad stablecoin and crypto funding support

- Strong travel and cross-border utility

- Up to 4% back in XRP (U.S.).

- Spend 200+ assets with instant virtual card.

- No foreign transaction fees on Elite tier.

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Fast virtual issuance

- No-KYC virtual card path

- BTC, ETH, USDT, and USDC funding

- Up to 10% Tiered Cashback – Competitive top-end rewards for high spenders and VIP users.

- Fiat-First Spend Logic – Uses fiat balance first, auto-converts selected crypto only if needed.

- Transparent Fee Structure (EEA program) – FX (0.5%) and crypto conversion (0.9%) fees are clearly disclosed rather than hidden in spreads.

- Stablecoin-led global spending

- Virtual and physical card access

- Card, wallet, transfers, swaps and credit in one app

- Up to 5% CRO rewards with instant payout after each purchase.

- Instant virtual card with broad Apple Pay and Google Pay support (region dependent).

- No annual fee and high daily purchase limits up to $25,000.

- No-KYC virtual tier available

- Apple Pay and Google Pay on verified tier

- Crypto top-ups across multiple networks

- Up to 8% Cryptoback rewards (tier-based, paid in WXT)

- $0 annual fee + 0% marketed FX fees on card spending

- Multicurrency spending from fiat, stablecoins, and crypto in one app

- $0 monthly fee and free crypto-to-USD loads.

- High limits — up to $10,000 per day in purchases and $6,000 per day at ATMs.

- Up to 15% cash-back offers at participating merchants.

- High stated spending limits on the physical card

- Virtual and physical cards with Apple Pay, Google Pay, and Samsung Wallet support

- Freeze and unfreeze controls with multiple virtual cards

These eight cards cover most of what the market offers right now, but they do not serve the same user. Some prioritize frictionless everyday spending. Others are built around tiered rewards, platform loyalty, or crypto-backed borrowing. The comparison table below lays out the key differences before the detailed reviews get into the specifics.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability |

|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. |

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. |

| | Visa | Debit | Apple Pay, Google Pay | United States and the United Kingdom. In the U.S., the card is not available in New York, Louisiana, or U.S. territories. In the U.K., Crown Dependencies and British Overseas Territories are excluded. |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) |

| | Visa, Mastercard | Prepaid | — | Varies by jurisdiction. |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay | 100+ countries, varies by jurisdiction. |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay, Samsung Pay | Available in many regions (e.g., US, EEA/UK, SG, CA, AU, BR) with residency-based eligibility and restricted markets per Crypto.com lists. |

| | Mastercard | Prepaid | — | Most countries, excluding restricted markets including the United States, Hong Kong, Cuba, North Korea, Egypt, Iran, Myanmar, Nigeria, Russia, South Africa, Syria, Ukraine, Venezuela, Belarus. |

| | Visa, Mastercard | Debit | Apple Pay, Google Pay | Available in UK and many countries (incl. parts of EEA, AU, NZ, HK, TW), while not available in USA, Canada, China, Japan, South Korea, Philippines, Russia (among others); EEA Mastercard eligibility requires EEA residency excluding Cyprus & Liechtenstein. |

| | Mastercard | Prepaid | Apple Pay, Google Pay | United States only; new applications paused with waitlist available. |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay, Samsung Pay | Varies By Jurisdiction |

The table gives a quick snapshot, but the real differences show up once you look past headline rewards and regional availability. The detailed reviews below cover how each card performs in practice, where trade-offs start to matter, and which type of user each option suits best.

Crypto Cards Reviews

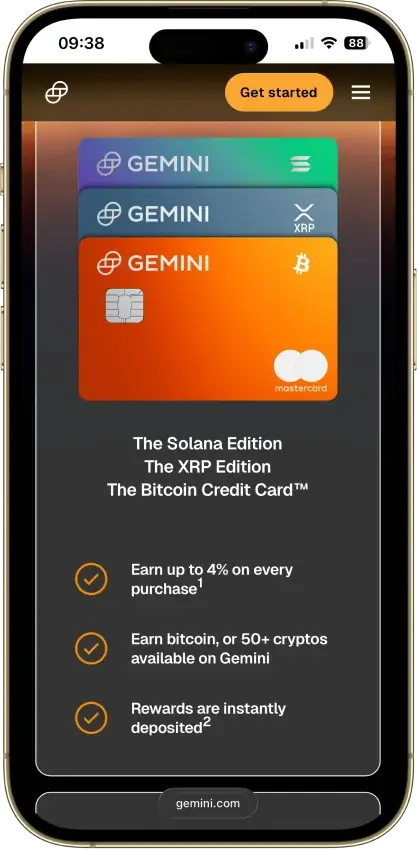

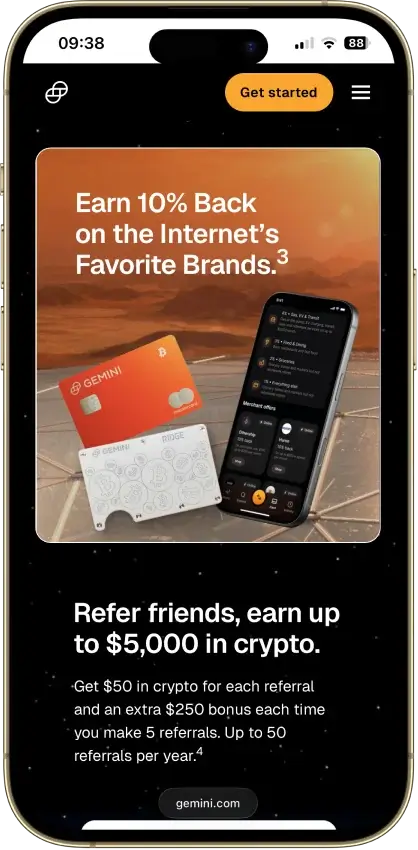

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

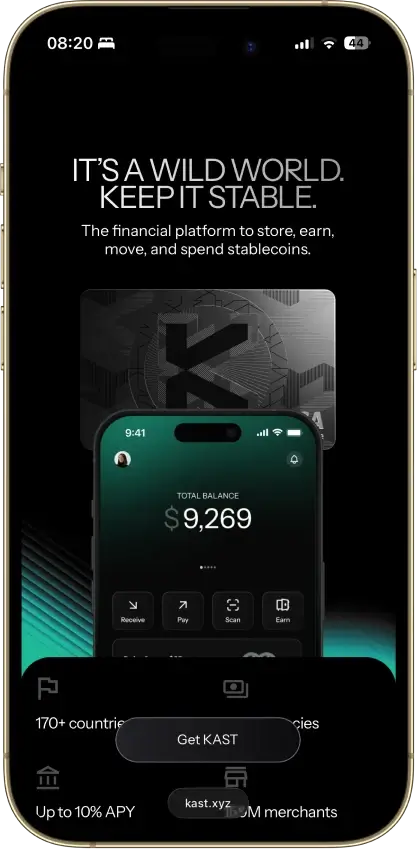

Kast Card

Pros

- Virtual card is ready within minutes of approval, with no shipping wait required

- Apple Pay and Google Pay are supported from the start, so you can spend before the physical card arrives

- Stablecoin deposits (USDT, USDC, USDe, PYUSD, RLUSD) convert to USD at 1:1 with no spread

- The Standard tier costs nothing to open, which keeps the entry bar low for first-time users

- Visa acceptance and physical card delivery cover 170+ countries, which is a wider reach than most crypto cards offer

Cons

- Deposited crypto is treated as sold to KAST on entry, with no self-custody option inside the card flow

- Full KYC and partner approval can block or delay access, even for users in supported countries

- Non-USD spend adds a 0.5% to 1.75% FX fee on top of every transaction

- ATM withdrawals require the physical card, cost $3 plus 2% per transaction, and are capped at $750 per day

- Premium tiers start at $1,000 per year, which is hard to justify unless you spend a very high volume and want KAST Points and token rewards rather than cash

Uphold Card

Pros

- Up to 4% XRP rewards on Elite, with a promotional window for new U.S. applicants

- Spend from 200+ assets including fiat, stablecoins, and crypto from one wallet

- Instant virtual card with Apple Pay and Google Pay on both U.S. and U.K. accounts

- No annual fee on Essential

Cons

- Crypto-funded purchases carry a variable conversion spread that reduces net value

- U.S. rewards are XRP-only with no option to switch reward asset

- Essential tier has a $2,500 daily spend cap and $500 ATM limit

- Available only in the U.S. and U.K., with additional state and territory exclusions

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

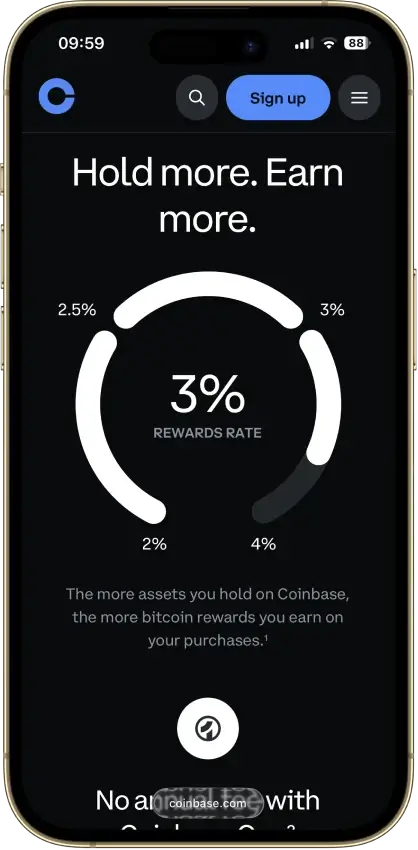

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

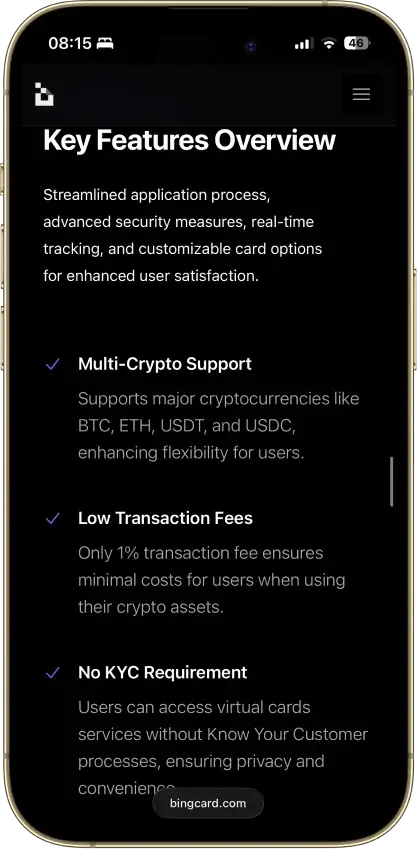

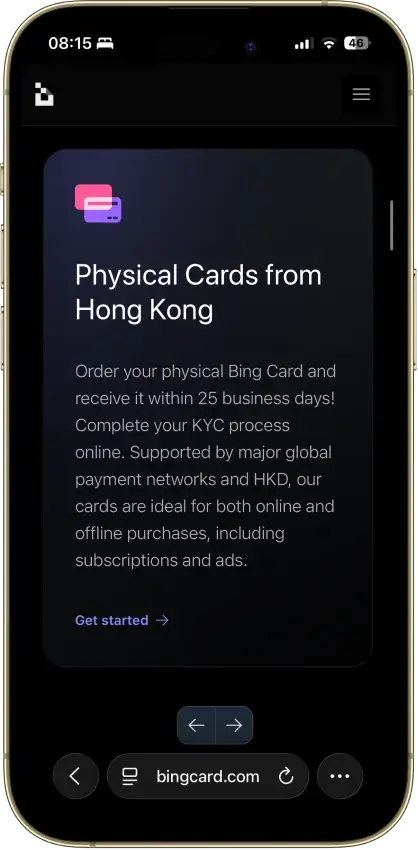

Bing Card

Pros

- Virtual cards can be issued in about five minutes

- Virtual card access does not require standard KYC

- Supports BTC, ETH, USDT, and USDC top-ups

- Works for subscriptions, online checkout, and ad spend

- Transaction history and downloadable reports are available

Cons

- No cashback, points, or travel perks

- All tiers charge an upfront issuance fee

- Top-up, withdrawal, and cross-border fees still apply

- Availability and eligibility need closer jurisdiction checks

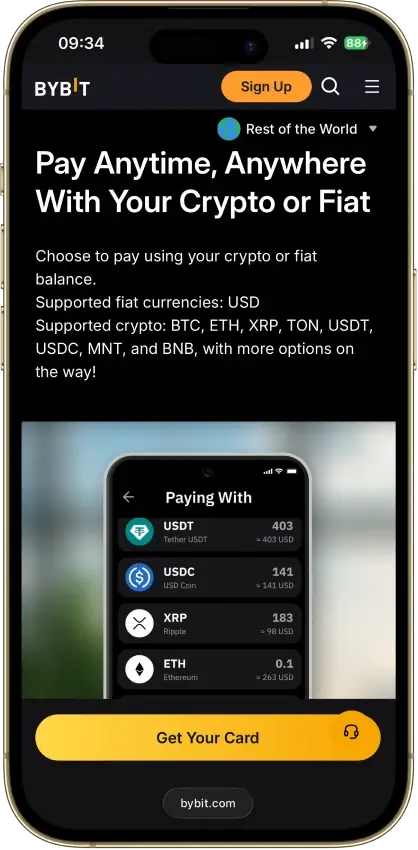

Bybit Card

Pros

- Up to 10% tiered cashback in Rewards Points.

- No annual, inactivity, or card cancellation fee

- Fiat-first spending can avoid crypto conversion fees.

- Strong card controls (freeze, limits, toggles).

Cons

- Limited country availability (no U.S.).

- 0.9% crypto conversion fee (EEA program).

- 0.5% FX on cross-currency spend (EEA program).

- Rewards are tier-based and capped monthly.

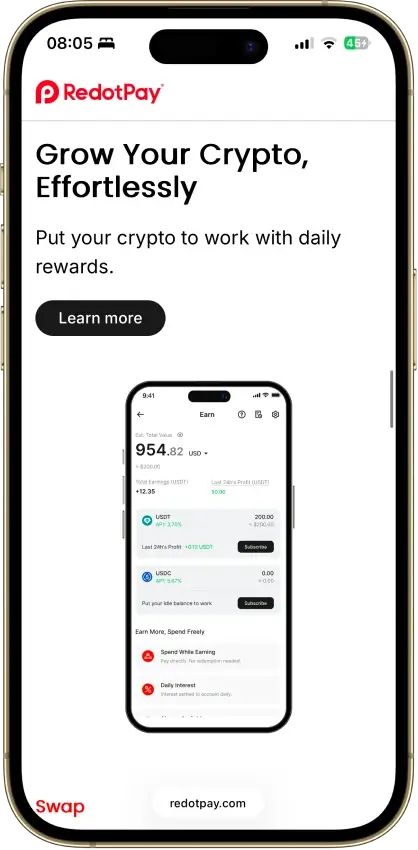

RedotPay

Pros

- Virtual card activates fast after KYC and funding, so online spend starts within minutes of approval.

- Physical card unlocks ATM access and in-store use, not just checkout payments.

- Apple Pay support means you can tap to pay in supported regions without carrying the physical card.

- No monthly or annual fee keeps the holding cost flat once you've paid the issuance fee.

- One app covers cards, wallet balances, transfers, swaps, P2P, and crypto-backed credit.

Cons

- Full KYC including ID upload and face scan is required before any core feature is accessible.

- Physical card issuance costs $100 and that fee is non-refundable.

- A 1.2% FX fee applies on every cross-currency transaction, including ATM withdrawals in a foreign currency.

- Custody sits with RedotPay and its partners, so balances can be frozen if compliance checks flag the account.

- The $50 chargeback fee and 3-to-6-month resolution timeline make disputes expensive and slow.

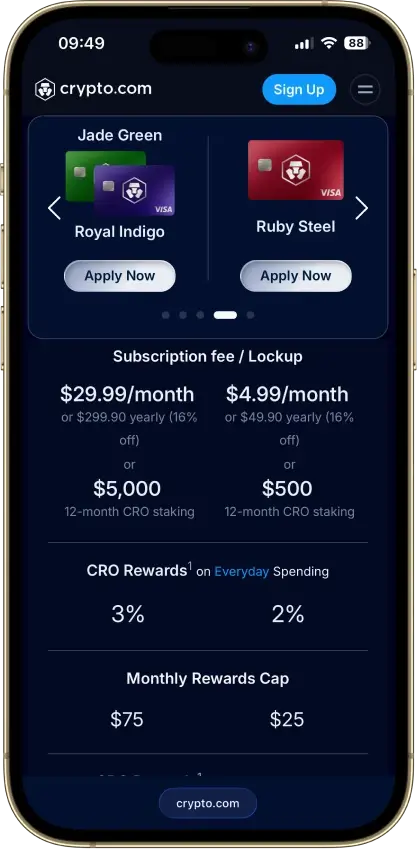

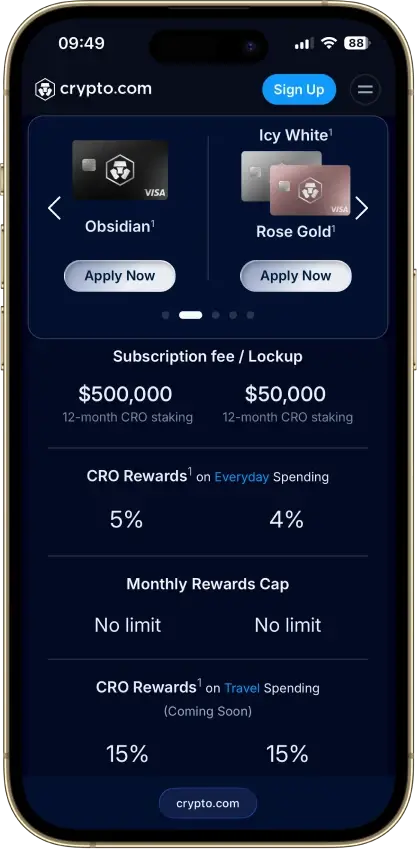

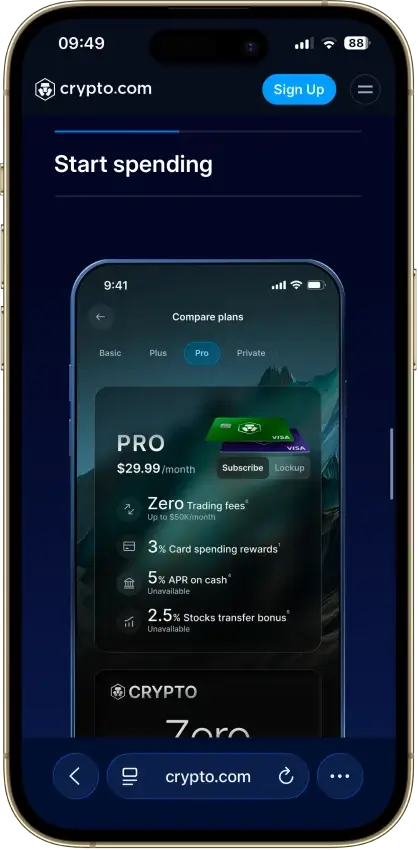

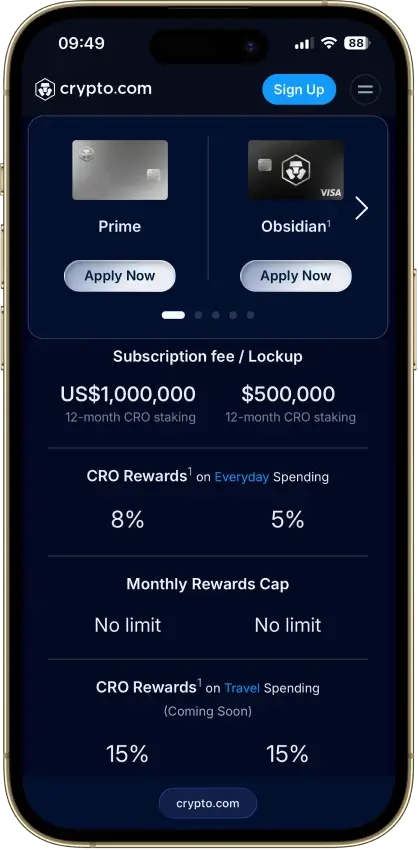

Crypto.com Card

Pros

- Up to 5% CRO back with instant rewards.

- No annual fee and high spending limits.

- Instant virtual card and strong mobile wallet support.

Cons

- 3% foreign fee on lower tiers (US market).

- Monthly cashback caps on mid tiers.

- Requires a monthly fiat subscription or a 12-month CRO lockup to earn rewards.

- Crypto funding includes a conversion spread.

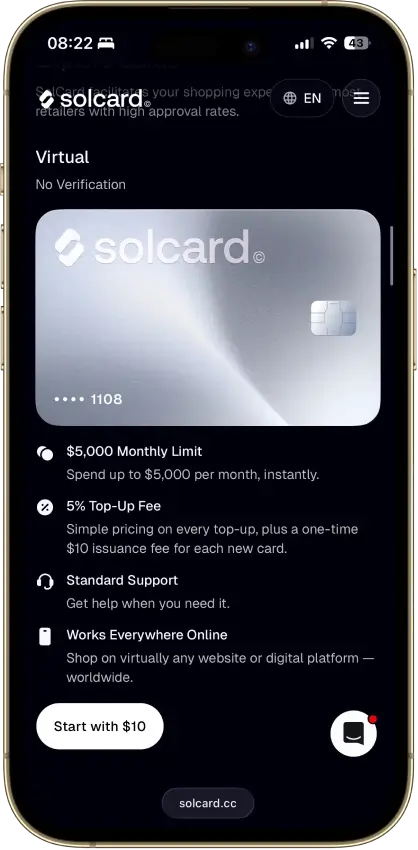

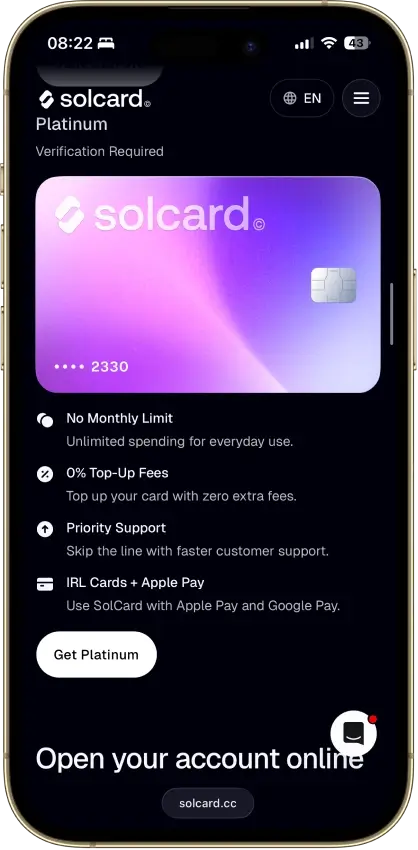

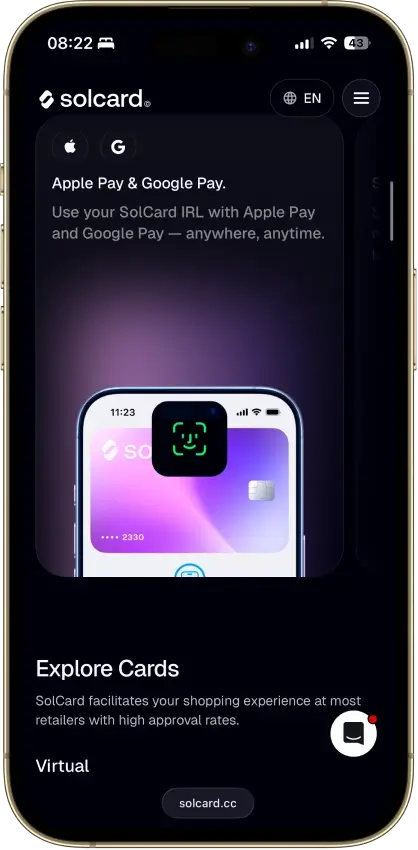

Solcard

Pros

- No-KYC virtual card for online spending

- Verified tier adds Apple Pay and Google Pay

- Supports USDT and USDC on several networks

- Unused balance can be withdrawn back to wallet

Cons

- Standard tier charges 5% on each top-up

- $0.30 purchase fee applies on successful transactions

- No physical card and no ATM access

- Blocked merchants and repeated declines can freeze the account permanently

Wirex Card

Pros

- Up to 8% rewards at higher X-tras tiers

- No annual fee

- Strong in-app controls

Cons

- Not available in US

- Rewards paid in WXT

- ATM fees after free limit

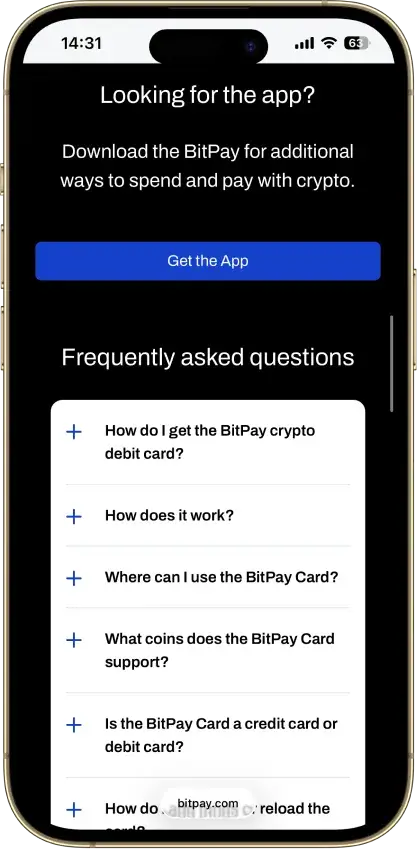

BitPay Card

Pros

- No monthly fee and free loads.

- High daily spending and ATM limits.

- Instant virtual card with Apple Pay and Google Pay support.

- Up to 15% merchant offers.

Cons

- 3% FX fee.

- No base cashback on everyday purchases.

- $5 dormancy fee after 90 days of inactivity.

- U.S.-only and new applications currently paused.

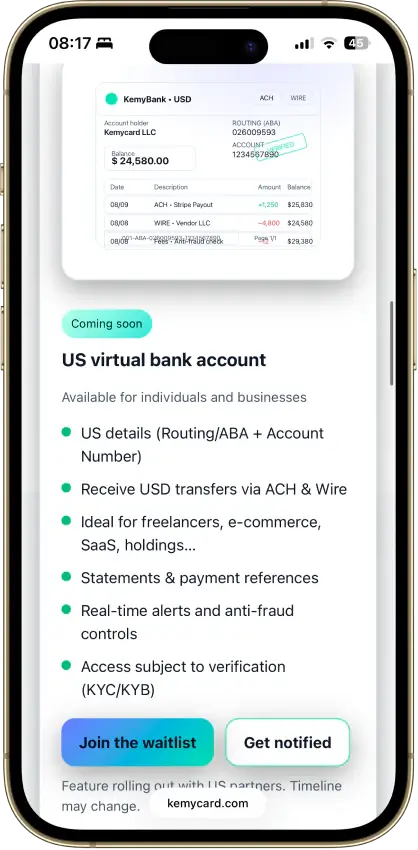

KemyCard

Pros

- Virtual card can be created quickly for online spend

- Physical card supports Apple Pay, Google Pay, Samsung Pay, and NFC

- Physical card has unusually high stated spend limits

- Multiple virtual cards help separate subscriptions or budgets

- Freeze and unfreeze controls are built into the dashboard

Cons

- Main account deposits carry a very high stated fee

- Virtual card charges both top-up fees and per-transaction fees

- Physical card has a high upfront cost and monthly fee

- Supported crypto assets are not clearly broken out

- US account and crypto-to-fiat payout features are not live yet

Ranking Methodology

We rank crypto cards by practical value, not by the biggest advertised reward rate. A card only ranks well when an eligible user can apply, fund the account, spend reliably, understand the costs, and keep enough value after fees, caps, spreads, restrictions, and tax-record friction.

This methodology is built for mixed card models. It covers exchange-linked debit cards, prepaid crypto cards, stablecoin cards, virtual-first cards, crypto rewards credit cards, and hybrid debit/credit products. Each card is judged within the model it actually uses, but friction that affects normal use still lowers the score.

How The Score Is Calculated

Each card receives a weighted score out of 10. Every metric gets a score of 0, 0.5, or 1.0, then that score is multiplied by the metric weight.

Final score = sum of each metric score × metric weight

A score of 1.0 means the card performs well on that metric for the version being reviewed. A score of 0.5 means the card is usable, but there is meaningful friction, missing detail, or a condition that reduces practical value. A score of 0 means the feature is weak, unavailable, paused, unclear, or not verified from reliable sources.

What We Score

The table below shows every metric, the weight assigned to it, what gets checked, and why it changes the final rank. The highest weights go to spend reliability, funding path, fees, and security because those areas shape whether a crypto card works as a real payment product.

| Metric | Weight | What We Check |

|---|---|---|

| Availability And Setup Friction | 1.0 | Current application status, eligible countries or states, waitlists, paused programs, invite-only access, KYC, credit checks, source-of-funds checks, plan gates, and issuer restrictions. |

| Funding Rails And Conversion Path | 1.25 | Fiat funding, crypto funding, stablecoin support, linked account model, top-up flow, supported spend assets, conversion timing, chain support, and refund destination. |

| Real-World Spend Reliability | 1.5 | In-store payments, online payments, subscriptions, travel use, merchant acceptance, pre-authorizations, mobile-wallet spend, card declines, prepaid quirks, and stated limits. |

| Rewards Value After Conditions | 1.0 | Reward rate, reward asset, category caps, monthly caps, exclusions, staking requirements, token-hold rules, plan fees, loyalty tiers, redemption limits, and reward volatility. |

| Fees And Hidden Cost Drag | 1.25 | Annual fees, monthly fees, issuance fees, replacement fees, spreads, FX fees, ATM fees, top-up fees, inactivity fees, gas costs, partner fees, and unclear charges. |

| Operational Convenience And Limits | 0.75 | Virtual and physical issuance timing, funding-to-spend speed, purchase limits, ATM limits, cash access, refund timing, reversal handling, and upgrade friction. |

| App Controls And Virtual Card Tooling | 0.75 | Freeze and unfreeze tools, alerts, PIN controls, virtual cards, Apple Pay, Google Pay, card replacement tools, statements, CSV exports, and app reliability. |

| Security, Custody, And Freeze Risk | 1.25 | Custody model, issuer or banking partner clarity, account security, two-factor authentication, fraud controls, compliance reviews, freeze risk, and escalation path. |

| Support, Refunds, And Chargebacks | 0.75 | Support channels, human escalation, refund process, dispute process, unauthorized-transaction handling, chargeback rights, and cardholder agreement clarity. |

| Tax And Reporting Readiness | 0.5 | Monthly statements, transaction history, CSV exports, reward records, crypto disposal records, stablecoin-spend records, and clarity around tax-relevant activity. |

| Total | 10.0 | Weighted score out of 10 |

How We Keep The Scoring Fair Across Card Types

Crypto cards do not all work the same way. Some spend from a prepaid balance, some liquidate crypto at the point of sale, some use stablecoins, some pay crypto rewards on normal credit-card spend, and some let users borrow against crypto collateral.

The score reflects the intended model. A crypto rewards credit card is not marked down because it does not support onchain spending. A stablecoin prepaid card is not marked down because it lacks traditional credit-card rewards. A crypto-backed credit card is not marked down simply because it uses collateral.

However, the user still has to live with the product. If a card has confusing fees, weak support, unclear custody, poor refund handling, limited availability, or a funding path that creates avoidable cost, that friction reduces the score.

Why Net Value Beats Headline Rewards

The reward rate is only one part of the ranking. A card advertising 5%, 8%, or 10% back can still rank below a lower-reward card if the top rate depends on a paid plan, staking, a native-token balance, a capped category, promotional timing, or a loyalty tier most users will not reach.

We also account for cost drag. FX fees, ATM fees, crypto conversion spreads, top-up charges, issuance fees, and partner costs can reduce or erase the value of a reward. A 2% reward can be stronger than a higher advertised rate when the lower-rate card is cheaper, easier to fund, and easier to use consistently.

This is why the ranking focuses on retained value. The best card is not always the card with the biggest number. It is the card that leaves the user with the best combination of access, cost, reliability, rewards, and control.

How Availability Changes The Ranking

Availability is not treated as a footnote. It can change the rank materially.

A card ranks lower if it is not open to new applicants, has a waitlist, excludes major regions, lacks clear country or state coverage, hides eligibility rules, or only works after a user joins a specific plan. A card can also fall if the virtual card, physical card, rewards program, or mobile-wallet support is available in one market but missing in another.

For the main hub, live cards open to new applicants get priority. Legacy cards, paused cards, waitlisted cards, and region-paused cards should be separated or clearly downgraded so they do not outrank cards a user can apply for now.

How We Handle Regional Versions, Tiers, And Modes

Some crypto cards change heavily by region, issuer, plan, or mode. A card may have one fee schedule in the U.K., another in the EEA, and a different setup elsewhere. Some cards also split value by tier, loyalty level, virtual-card status, physical-card status, Debit Mode, Credit Mode, or verified account level.

When that happens, the review should state the version being scored. If no specific region or tier is being reviewed, the score should reflect the version a new user is most likely to get by default.

The ranking should not assume the highest tier unless that tier is clearly the normal path for the target user. Paid plans, staking levels, premium metal cards, VIP cashback boosts, or promotional tiers only improve the score when the cost and conditions still leave clear value.

How Rankings Are Updated

Crypto card terms can change quickly. Rewards, availability, fees, supported regions, issuer partners, physical-card status, and mobile-wallet support should be checked during major page updates.

When a card pauses new applications, changes issuer, removes a reward tier, adds a required plan, changes a fee schedule, or restricts a major region, its ranking should be reviewed. If a key claim cannot be verified from official or high-reputation sources, the review should use conservative wording or mark the point as not verified.

Best Crypto Cards by Category

The table below works as a shortcut. Each row names the category and the cards that currently fit it best.

| Category | Top Cards |

|---|---|

| Best Crypto Debit Cards | Coinbase Card, Crypto.com Card, Wirex Card |

| Best Crypto Cards In The USA | Gemini Credit Card, Coinbase Card, KAST Card |

| Best Crypto Cards In The UK | Uphold Card, Nexo Card, Wirex Card |

| Best Crypto Cards In Europe | Nexo Card, Wirex Card, KAST Card |

| Best Crypto Cards For International Travel | KAST Card, Wirex Card, Nexo Card |

| Best Free Crypto Cards | Coinbase Card, Gemini Credit Card, Nexo Card |

| Best Low-Fee Crypto Cards | Coinbase Card, Gemini Credit Card, KAST Card |

| Best USDT Crypto Cards | KAST Card, RedotPay, Bybit Card |

| Best USDC Crypto Cards | KAST Card, Coinbase Card, RedotPay |

| Best Bitcoin Cards | Gemini Credit Card, Coinbase Card, Crypto.com Card |

| Best Solana Cards | SolCard, KAST Card, Coinbase Card |

| Best XRP Cards | Uphold Card, Gemini Credit Card, Bybit Card |

What Is a Crypto Card?

A crypto card is a payment card that lets users spend through traditional card networks while drawing value from a crypto-linked balance or from a program that pays rewards in crypto. In practice, a cryptocurrency card or crypto payment card does the same basic job: it turns digital balances or crypto rewards into something usable through ordinary card rails.

Some crypto cards work like debit cards and pull from a funded account, exchange balance, or topped-up wallet. Others work more like credit cards and reward purchases in Bitcoin or other digital assets instead of standard cashback or points.

That setup means users can pay at regular online stores, apps, and physical merchants without the merchant needing to accept crypto directly. The main differences come down to how the card is funded, how rewards are paid, and what fees or restrictions apply in the background.

How Do Crypto Cards Work?

Most crypto cards follow a simple setup. The user opens an account, completes identity checks if required, and orders either a physical card, a virtual card, or both. The card is then linked to the provider's app or exchange account.

From there, the user either funds the account with crypto or fiat, tops up a spending balance, or uses a card that rewards normal spending in crypto. When a purchase is made, the payment moves through standard card rails — Visa or Mastercard — while the provider handles conversion, settlement, or rewards logic in the background.

The checkout experience feels familiar, but the economics behind it can vary widely. Some cards focus on direct spending from a crypto balance. Others are mainly built around earning crypto on everyday purchases.

Crypto Card Benefits

The biggest benefit of a crypto card is convenience. It gives users a cleaner way to spend from a crypto-linked balance or earn digital assets back without manually moving money for every transaction.

Many of the best crypto rewards cards also add value through cashback, token rewards, instant virtual cards, and support for Apple Pay or Google Pay. For users who already hold crypto, a good card can also tie rewards, spending, and account management into one place instead of keeping crypto separate from everyday purchases.

Crypto Card Drawbacks

Crypto cards are not always as simple as the headline reward rate suggests. Several costs can reduce the real value of a card over time. Here are the main ones to watch:

- Conversion spreads baked into the exchange rate at point of sale

- Funding fees when topping up with certain assets

- ATM charges once a free monthly allowance runs out

- Subscription or staking requirements to unlock better tiers

- Tax obligations when a purchase triggers a disposal of an appreciated asset

- Regional restrictions, with some cards limited to specific countries or U.S. states

- KYC requirements that lock features until full verification is complete

- Reward structures that shift depending on region, plan, or promotional window

None of these make crypto cards a bad choice. They do mean the best option is usually the one that balances convenience, rewards, and total cost rather than the one with the loudest marketing.

Why Conversion Spreads Matter

Conversion spreads are one of the easiest ways for a crypto card to look better on paper than it performs in practice. Even when a card advertises no annual fee and a decent reward rate, that value can shrink quickly if the provider bakes a margin into the exchange rate or charges a separate conversion fee when non-fiat assets are used to settle a purchase.

This is especially relevant for low-fee crypto cards that convert crypto at the point of sale. A 1% or 2% reward rate loses much of its appeal if the card also charges a spread or adds a fee when assets are sold behind the scenes. Comparing only the reward percentage is rarely enough.

Taxes When Spending Crypto

Using a crypto card can trigger a taxable event in some jurisdictions because the provider may sell or convert crypto to settle the purchase. In those cases, the transaction can be treated more like selling crypto than making a standard card payment.

Spending stablecoins or fiat balances can simplify record-keeping because fewer conversions occur. However, rules vary by country, and tax treatment depends on local regulations.

Because card conversions create transaction records, many users export card statements and exchange logs regularly to track the fiat value at the time of each purchase.

How to Get a Crypto Card

Getting a crypto card is usually straightforward, but the exact path depends on the type of card you want and where you live. Some providers only operate in selected countries or U.S. states, some require full identity verification before you can apply, and some only unlock their best features if you use the provider's exchange, hold a certain token, or pay for a higher-tier plan.

The process is different for a no-KYC crypto card versus a full credit or debit product from a regulated issuer, but for most users the steps look like this:

- Choose the type of crypto card you want. Decide whether you want a crypto debit card, a crypto credit card, a virtual crypto card, or a prepaid option. The right choice depends on whether you want to spend from an existing balance, earn crypto rewards on credit purchases, or get quick virtual access for online use.

- Check country or state availability. Before going further, confirm the card is offered where you live. Availability is one of the biggest differences between issuers, and some cards that look attractive on paper are limited to certain markets.

- Create an account and complete verification. Most providers ask you to open an account and complete KYC before the card is issued. In practice, that means confirming your identity, age, address, and sometimes your residency status.

- Order the physical or virtual card. Once your account is approved, you can usually request a physical card, a virtual card, or both. Some providers make virtual access available first, while physical delivery can take longer depending on region.

- Fund the eligible balance or connect the right product. With a debit-style crypto card, this usually means adding crypto or fiat and topping up a spending balance. With a crypto credit card, it may mean activating the card and linking it to the provider's rewards or borrowing setup.

- Set up security and spending preferences. Before using the card, turn on two-factor authentication, review card controls in the app, and check whether you can freeze or unfreeze the card, change your PIN, or manage spending settings in real time.

- Add it to your wallet and start using it. If the card supports Apple Pay and Google Pay, you can often start using it before the physical card arrives. That can be one of the biggest practical advantages of a strong virtual setup.

It is also worth checking the small-print requirements before applying. Some issuers require users to be at least 18, some reserve better rewards for premium tiers, and some tie the card tightly to their exchange ecosystem or loyalty program. Getting a crypto card is usually simple. Getting good value from it depends on choosing a card that actually fits your region, funding style, and spending habits.

How to Choose the Best Crypto Card for You

Choosing the best crypto card comes down to how you actually spend — not which issuer advertises the highest reward. A card that looks strong for cashback may be a poor fit for travel, stablecoin spending, or daily use if the fees, limits, or availability do not match your needs.

A better starting point is to work backward from your use case. The right crypto card fits your region, funding style, and spending habits with the least friction.

Best for Everyday Spending

If you want a crypto card to replace part of your normal card use, start with reliability. Everyday spending works best with a card that has clear limits, simple funding, stable rewards, and an app that makes it easy to track transactions without surprises. Cards like the Coinbase debit card and the Crypto.com Visa Card are built around frequent use. What matters most is not just the reward rate — it is how easy the card is to top up, how clearly spending is tracked, and how much friction builds up over time from hidden costs.

Best for Rewards-Focused Users

If earning back the most value is the priority, look closely at how the reward structure actually works. Some cards advertise high headline percentages, but real returns may depend on spending caps, loyalty tiers, subscriptions, staking, or promotional windows. A rewards-focused user should compare the asset paid out, the cap on the highest reward category, and whether the better tier requires a meaningful extra commitment. The best crypto card rewards are the ones you can access consistently — not just during a promotional period.

Best for Stablecoin Users

If you mainly hold stablecoins, the best option is usually the one with the cleanest path from balance to payment. USDT crypto cards and USDC crypto cards appeal to users who care less about speculation and more about simple settlement, predictable value, and fewer surprises at checkout. In this case, easy funding, clear conversion rules, and low friction often matter more than a marginally better reward rate tied to a volatile native token.

Best for Travelers

Travelers should focus more on foreign transaction costs, ATM rules, regional acceptance, and wallet compatibility than on the headline cashback figure. A crypto card that works well domestically can become expensive fast once ATM allowances are used up or FX costs begin to stack. For this type of user, the best crypto card for international travel is one that works across merchants and regions, offers solid virtual access, and does not punish normal international usage with tight limits or layered fees.

Best for Beginners

Beginners should usually prioritize simplicity over optimization. The best crypto card for beginners is one with a straightforward setup, clear in-app controls, easy-to-understand funding, and a reward model that does not depend on too many moving parts. A card that is slightly less aggressive on rewards can still be the better pick if it removes confusion around tiers, conversion, and eligibility. Usability usually determines whether a new user keeps using the card at all.

Best for Instant Virtual Access

If you want to start spending quickly, virtual access matters. The best virtual crypto card is usually one that can be issued fast, added to Apple Pay or Google Pay without friction, and managed entirely through the app. This is especially practical for users who make frequent online purchases, want immediate access before a physical card arrives, or prefer a fully digital spending setup.

Security and App Controls to Look For

A good crypto card makes day-to-day security feel easy. Freeze and unfreeze controls, real-time spending alerts, PIN management, and visible transaction tracking are baseline features that make a card both safer and more usable. Account-level protection matters just as much. Strong two-factor authentication, responsive support, and reliable app controls often make the difference between a card a user keeps and one they abandon after the first few weeks.

The Best Crypto Card Depends on How You Spend

Once you look at funding model, fees, and usable rewards together, it becomes easier to see which card fits your needs. Coinbase is a strong pick for users who want straightforward debit-style spending. Gemini is the cleaner option for users who want traditional credit card rewards paid in crypto. Crypto.com, Wirex, Bybit, and Nexo make more sense for users willing to trade simplicity for bigger perks, broader flexibility, or higher upside.

The right choice comes down to what you value most: easy everyday use, stronger rewards, low-fee virtual access, predictable costs, or a more flexible spending model. The best crypto card is the one that fits your region, funding style, and real spending habits — without asking you to pay too much for the privilege.

FAQ

What is the best crypto card in 2026?

How do crypto debit cards work?

What is the difference between a crypto debit card and a crypto prepaid card?

Are there crypto cards with no KYC?

What is the best crypto card for international travel?

Do crypto cards work with Apple Pay and Google Pay?

Can I use a crypto card to spend stablecoins like USDT or USDC?

What are the tax implications of using a crypto card?

Why do crypto card payments get declined?