US labor federation warns CLARITY Act could push crypto closer to workers’ retirement money

The AFL-CIO says clearer crypto market rules could make digital assets easier to package into 401(k) and retirement investment products before stronger safeguards are in place.

The AFL-CIO is trying to recast the Senate CLARITY Act from a fight over banks, stablecoin rewards, and crypto market structure into a fight over workers' retirement money.

The AFL-CIO is the American Federation of Labor and Congress of Industrial Organizations, the largest federation of labor unions in the United States, representing millions of workers across dozens of unions.

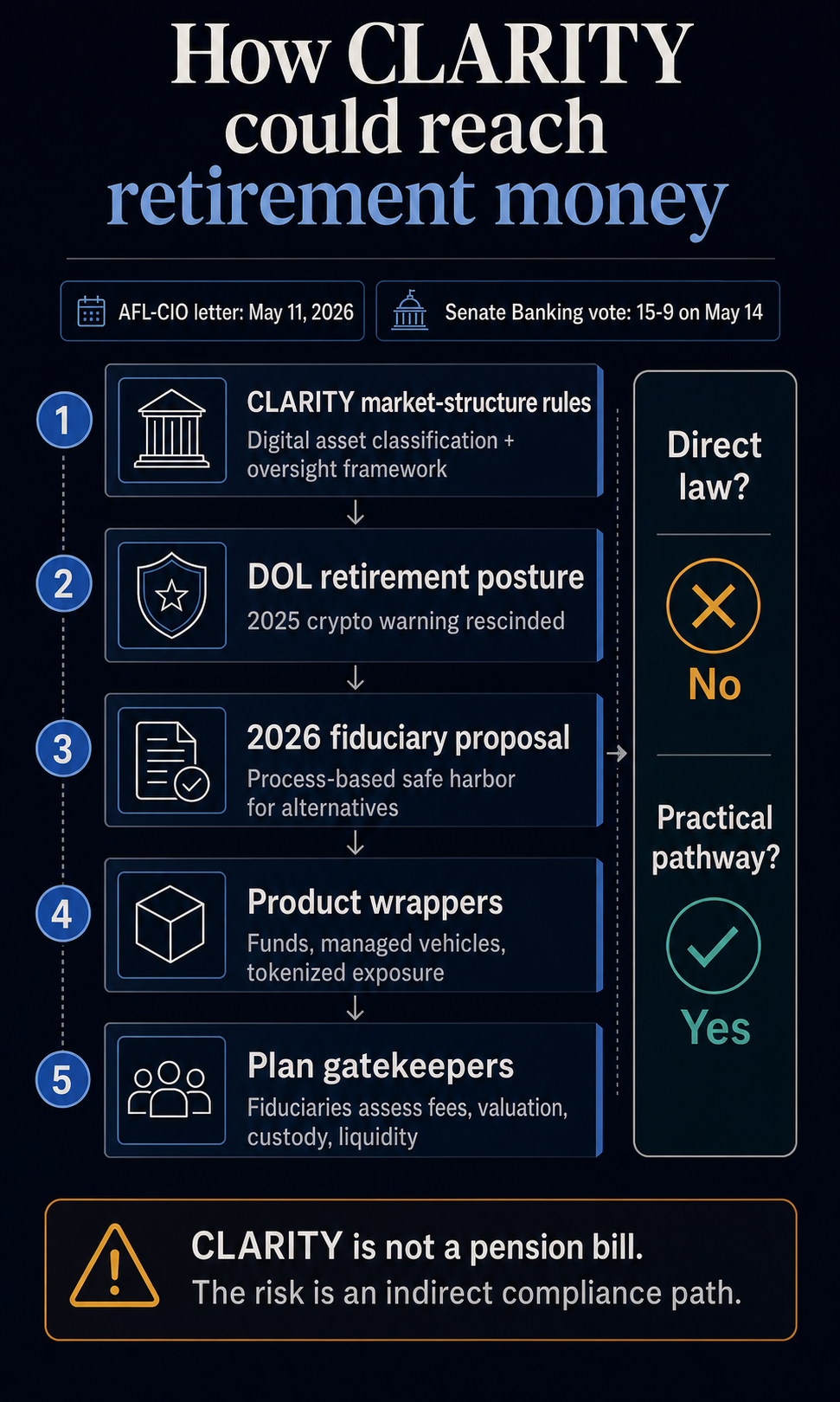

In a May 11 letter to senators, the labor federation urged lawmakers to oppose the Senate version of the House's Digital Asset Market Clarity Act.

The group warned that the bill could push digital assets into pension plans, retirement accounts, and the broader financial system under weak oversight.

The warning landed just days before the Senate Banking Committee advanced H.R. 3633 in a 15-9 vote, sending the crypto market-structure bill toward a harder floor fight.

That vote gave the industry a major procedural win, but it did not settle the political problem underneath the bill.

For months, CLARITY has been framed as a fight between banks and crypto firms over stablecoin rewards, Democrats and Republicans over ethics, and law-enforcement voices over DeFi carve-outs.

The AFL-CIO's intervention adds a different constituency and a more human risk: whether regulatory certainty for digital assets becomes a bridge into retirement savings before safeguards are strong enough.

The caveat is crucial. CLARITY is market-structure legislation rather than retirement law, and it does not order pensions to buy crypto.

The labor argument is about what the bill could unlock once digital assets receive clearer federal labels and market rules.

The retirement path is indirect

CLARITY is designed to draw lines between digital commodities, digital asset securities, intermediaries, custody, trading activity, DeFi services, and stablecoin-related conduct.

Its supporters argue that this brings crypto into a more transparent rulebook after years of regulatory uncertainty. That framing is exactly why the AFL-CIO sees a retirement problem.

Pension trustees, 401(k) plan fiduciaries, asset managers, custodians, and compliance teams generally do not need Congress to tell them to buy crypto. They need enough legal certainty to decide whether a product can be offered, diligenced, benchmarked, valued, custodied, and defended under fiduciary standards.

The Department of Labor has already moved in that direction outside CLARITY.

In 2025, DOL rescinded its 2022 crypto-specific warning to 401(k) fiduciaries, returning to a more neutral ERISA process standard.

In March 2026, the agency proposed a rule to create process-based safe harbors for selecting alternative assets in 401(k) plan menus, including investment vehicles with digital-asset exposure, according to the agency's release and the Federal Register notice.

That makes the retirement pathway a stack, not a switch.

CLARITY would not force plan sponsors to add crypto funds. But it could make digital assets easier to classify and wrap inside products that retirement-plan gatekeepers can evaluate under a more permissive DOL posture.

| Layer | What it does | Retirement-money effect |

|---|---|---|

| CLARITY | Creates federal market-structure rules for digital assets | May reduce classification uncertainty for products and compliance reviews |

| DOL posture | Moves from a crypto-specific warning toward process-based fiduciary standards | May give plan fiduciaries more room to consider alternative-asset exposure |

| Product design | Places crypto exposure inside funds, managed vehicles, or tokenized products | Could make crypto less visible to workers than a direct coin allocation |

| Plan oversight | Requires fiduciaries to assess fees, valuation, liquidity, custody, and risk | Determines whether access becomes isolated, broad, or blocked |

That distinction also limits the strongest version of the AFL-CIO's claim.

The bill remains a market-structure measure. The risk is that it becomes one part of a larger policy environment that makes retirement exposure more likely.

Labor adds a retirement front to the floor fight

The AFL-CIO letter is blunt because retirement money is politically different from stablecoin rewards.

A bank-deposit fight presents like a turf battle between regulated lenders and crypto exchanges. A DeFi liability fight is more technical. A pension fight aims to put workers, retirees, and plan sponsors at the center of the news cycle.

CLARITY's committee vote was only the first Senate test.

CryptoSlate's markup coverage showed how the bill survived objections over national security, stablecoin yields, ethics, and President Donald Trump's crypto interests.

A follow-up analysis noted that Galaxy Research raised its 2026 passage odds to 75% after the vote but still pointed to ethics demands, DeFi language, and the compressed calendar as live constraints before a possible summer signing window.

Labor's critique adds another reason Democrats may demand changes before floor support.

It sits alongside concerns over illicit finance and conflicts of interest, while giving those disputes a more tangible endpoint: if the rules are too loose, the next pool of capital may not be traders chasing yield. It may be workers whose retirement menus are selected by fiduciaries and product providers.

The Government Accountability Office has already warned that crypto in 401(k)s raises hard oversight questions.

A 2024 GAO report highlighted volatility, valuation, and projection uncertainty, limited data, and oversight gaps around crypto assets in defined-contribution plans.

GAO also found current use was low, which makes the AFL-CIO's argument a warning about access expanding rather than a claim that retirement portfolios are already stuffed with crypto.

Market scale makes the warning more consequential. CryptoSlate's market pages showed a total crypto market cap of around $2.58 trillion, Bitcoin around $1.55 trillion, Tether around $189 billion, and USDC around $76 billion.

Even small retirement allocations could change flows in a market where liquidity, product design, and regulatory labeling shape investor behavior.

The labor critique is also more difficult for CLARITY supporters to dismiss than a broad anti-crypto argument.

Supporters can say the bill brings digital assets into the sunlight, creates disclosure obligations, and gives regulators a framework. The AFL-CIO's counter is that weak rules can still be useful to industry if they provide enough legitimacy to move risk into mainstream portfolios.

The next test is the Senate text

The bill's supporters still have a straightforward answer: regulatory certainty is safer than the current patchwork.

They can argue that without a federal framework, digital assets remain in a harder-to-police market, while retirement-plan fiduciaries remain bound by ERISA duties regardless of what CLARITY says.

That answer is only partly responsive to the labor warning. ERISA duties do not eliminate product pressure, political pressure, or the practical effect of legal labels.

If CLARITY makes digital assets easier to classify and DOL makes alternative-asset access easier to defend, retirement-plan exposure can grow without Congress ever writing a line that says pensions should buy crypto.

That is why the floor debate now has a clearer test.

If senators add stronger safeguards around tokenization, enforcement, conflicts of interest, or retirement-plan exposure, the AFL-CIO can claim the bill had a real vulnerability.

If the bill moves quickly without those changes, labor's argument becomes a pressure point aimed at Democrats whose committee votes did not guarantee floor support.

AFL-CIO has identified a credible political and regulatory pathway, rather than a direct pension mandate in CLARITY.

The fight is no longer only about who pays rewards on stablecoins or which agency gets jurisdiction over digital assets. It is about whether a bill sold as crypto clarity also creates the legal comfort needed to put volatile assets closer to workers' retirement savings.

That makes the next Senate text more important than the committee vote.

The retirement-access test is whether lawmakers close the gaps before CLARITY gives crypto a clearer route to that door.