Most crypto cards look cheap until you actually use them. The annual fee is the easiest part to advertise and the least useful number to compare. What matters more is what happens when you fund the card, spend outside your home currency, withdraw cash, or try to earn rewards without paying a premium to access them.

This guide ranks five cards by total cost of ownership. That means conversion spread, FX pricing, ATM charges, stablecoin funding paths, and any tier or staking requirement that sits between you and the card's best terms. A card earns a higher score when one practical spending path is cheap, clear, and does not depend on selling crypto at checkout.

Top Low-Fee Crypto Cards

- Instant crypto rewards on every purchase — no waiting for statement close

- Up to 4% back with no annual fee or foreign transaction fees

- Choose from 50+ cryptocurrencies and switch reward asset anytime

- Fast virtual card access

- Broad stablecoin and crypto funding support

- Strong travel and cross-border utility

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 4% rotating crypto rewards (US) with no staking required.

- $0 annual fee and no added foreign transaction fee.

- Instant virtual card with Apple Pay and Google Pay integration.

- Up to 10% Tiered Cashback – Competitive top-end rewards for high spenders and VIP users.

- Fiat-First Spend Logic – Uses fiat balance first, auto-converts selected crypto only if needed.

- Transparent Fee Structure (EEA program) – FX (0.5%) and crypto conversion (0.9%) fees are clearly disclosed rather than hidden in spreads.

Gemini leads because its cost structure is easy to follow and does not depend on selling crypto at checkout. Nexo and KAST stay competitive when you use the lower-cost route they are built around. Coinbase and Bybit can still work well on price, but they get more expensive once you move away from USD, USDC, or the lower-cost route available in your region.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability | Rating |

|---|---|---|---|---|---|

| | Mastercard | — | Apple Pay, Google Pay, Samsung Pay | Available to residents of all 50 U.S. states and Puerto Rico; not available outside the U.S. | 8.5Excellent |

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. | 7.5Very Good |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. | 7.1Good |

| | Visa | Debit | Apple Pay, Google Pay, Samsung Pay | US only (all states except Hawaii) | 7.0Good |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card | 6.5Good |

Gemini is the easiest low-fee option for U.S. users because purchases do not trigger a crypto sale. KAST works well for stablecoin spending in USD. Nexo stays attractive for European users during weekday spending, but costs rise once weekend FX or post-limit ATM fees apply.

Low-Fee Crypto Cards Reviews

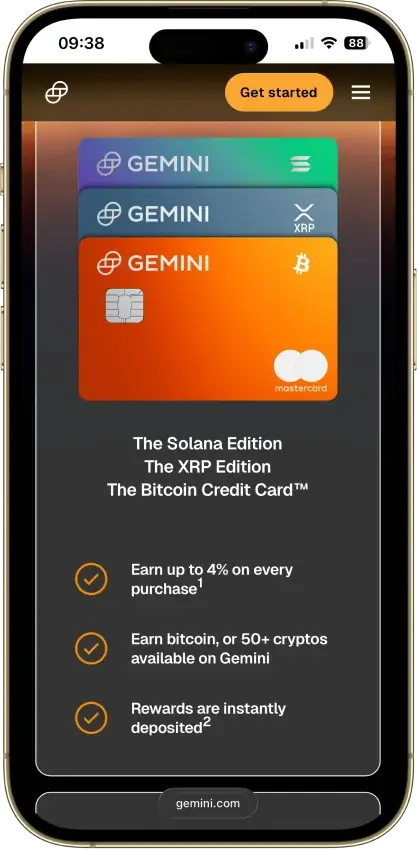

Gemini Credit Card

Pros

- Up to 4% crypto rewards

- No annual or FX fees

- Instant reward deposits

Cons

- U.S.-only

- 1% base rate

- Cannot pay with crypto

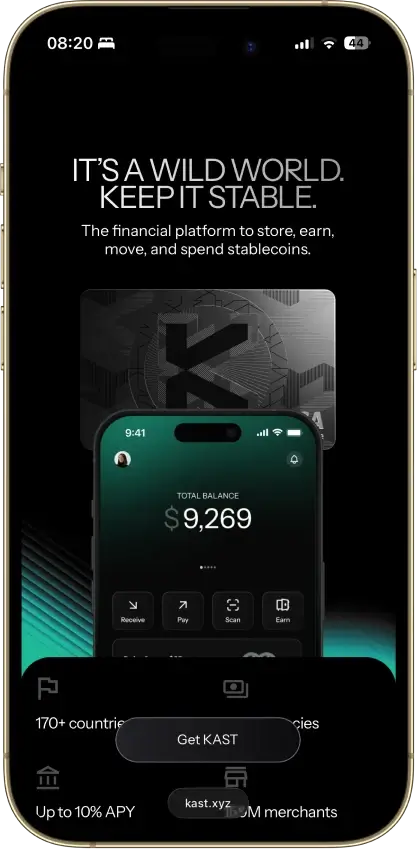

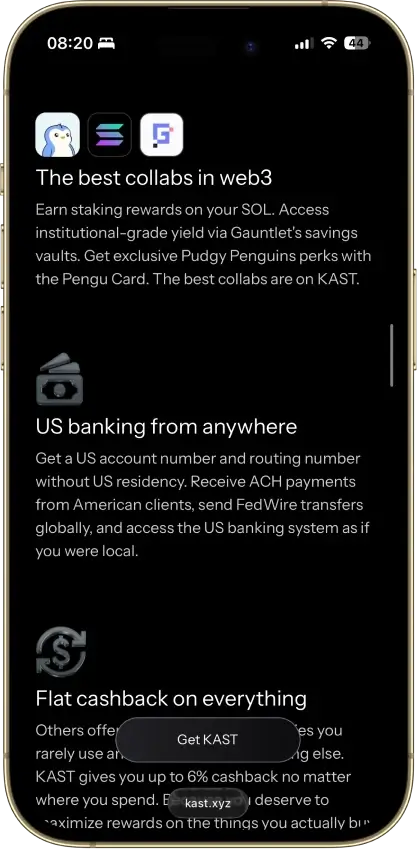

Kast Card

Pros

- Virtual card is ready within minutes of approval, with no shipping wait required

- Apple Pay and Google Pay are supported from the start, so you can spend before the physical card arrives

- Stablecoin deposits (USDT, USDC, USDe, PYUSD, RLUSD) convert to USD at 1:1 with no spread

- The Standard tier costs nothing to open, which keeps the entry bar low for first-time users

- Visa acceptance and physical card delivery cover 170+ countries, which is a wider reach than most crypto cards offer

Cons

- Deposited crypto is treated as sold to KAST on entry, with no self-custody option inside the card flow

- Full KYC and partner approval can block or delay access, even for users in supported countries

- Non-USD spend adds a 0.5% to 1.75% FX fee on top of every transaction

- ATM withdrawals require the physical card, cost $3 plus 2% per transaction, and are capped at $750 per day

- Premium tiers start at $1,000 per year, which is hard to justify unless you spend a very high volume and want KAST Points and token rewards rather than cash

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

Coinbase Card

Pros

- Up to 4% crypto rewards (US, rotating)

- No annual or foreign transaction fee

- Instant virtual card + mobile wallet support

- No credit check or staking requirement

Cons

- Conversion spread on crypto purchases

- Rewards limited to US users

- Daily spending and ATM caps

- Apple Pay and Google Pay are US-only

Bybit Card

Pros

- Up to 10% tiered cashback in Rewards Points.

- No annual, inactivity, or card cancellation fee

- Fiat-first spending can avoid crypto conversion fees.

- Strong card controls (freeze, limits, toggles).

Cons

- Limited country availability (no U.S.).

- 0.9% crypto conversion fee (EEA program).

- 0.5% FX on cross-currency spend (EEA program).

- Rewards are tier-based and capped monthly.

Our Ranking Methodology

This low-fee ranking is based on total cost of ownership, not only the annual fee. A card can have a $0 yearly fee and still rank lower if it adds cost through spread, crypto conversion, FX, ATM use, shipping, paid tiers, or unclear exchange rates.

Final score = sum of (criterion score 0 / 0.5 / 1.0) × weight.

| Criterion | Weight | What We Check |

|---|---|---|

| Availability + Setup Friction | 0.75 | Eligible countries or states, KYC, credit check, plan gate, waitlist, virtual and physical access |

| Low-Cost Funding Route + Conversion Clarity | 1.25 | USD, fiat, stablecoin, crypto, top-up route, conversion trigger, conversion timing, refund destination |

| Stated Card Fees + Hidden Cost Drag | 1.50 | Annual fee, monthly fee, issuance, replacement, shipping, top-up, spread, small-transaction fees, declined fees, inactivity fees |

| FX + International Spend Cost | 1.25 | Foreign transaction fee, network FX, weekend FX, regional FX differences, cross-border card rules |

| ATM + Cash Access Cost | 0.75 | ATM allowance, flat ATM fee, percentage ATM fee, operator surcharge, cash-advance treatment, ATM limits |

| Real-World Spend Reliability | 1.00 | Network acceptance, online spend, in-store spend, subscriptions, pre-authorizations, travel use, prepaid quirks |

| Limits + Operational Convenience | 0.75 | Issuance timing, funding-to-spend timing, daily limits, monthly limits, cash limits, refund timing |

| Rewards Value After Conditions | 0.50 | Reward rate, caps, excluded categories, token or point risk, paid tiers, volatility, redemption limits |

| App + Controls + Virtual Card Tooling | 0.50 | Freeze/unfreeze, alerts, card controls, virtual cards, Apple Pay, Google Pay, statements, export basics |

| Security + Custody + Freeze Risk | 0.75 | Issuer, custody model, account freeze risk, stablecoin or crypto custody, insurance disclosures, escalation path |

| Support + Refunds + Chargebacks | 0.50 | Human support, dispute path, unauthorized transaction process, refund handling, support channels |

| Tax + Reporting Readiness | 0.50 | Whether spending causes crypto disposals, statement quality, CSV/export tools, reward reporting, manual tracking burden |

Crypto Card Fees Explained

Crypto card fees are described in inconsistent ways across issuers. One card labels the cost as a conversion fee. Another folds the same charge into spread or foreign-currency pricing. Breaking the fees apart by type makes it easier to identify which cards are genuinely cheaper before you commit to one.

Annual Or Monthly Fee A fixed charge to keep the card open. All five cards on this list waive the annual fee. The key question is whether the card still delivers value at the base tier, or whether the good terms sit behind a paid plan.

- Gemini: $0 annual fee, no monthly fee

- Coinbase: $0 annual fee, no monthly fee

- Nexo: $0 annual fee, no monthly fee

- KAST: $0 annual fee at base; Luxe tier required for 8% cashback — tier pricing should be confirmed directly

- Bybit: $0 annual fee at all tiers; cashback rate varies by account level

Crypto Conversion Fee A stated percentage added when the card sells crypto to complete a payment. This is one of the most common hidden costs on crypto debit cards. Spending from fiat or stablecoin balances usually avoids it entirely.

- Gemini: No conversion fee at checkout — rewards are paid from Gemini's balance, purchases do not trigger a sale

- Coinbase: 2.49% liquidation fee when spending from BTC, ETH, or non-stable assets; 0% from USD or USDC

- Nexo: No stated conversion fee for card spend from credit line; check for spread on crypto-to-fiat conversion on funding

- KAST: No conversion fee when spending from USDC or USDT balance; token conversion applies if topping up from other assets

- Bybit: No stated conversion fee for direct crypto spend; confirm current spread on asset liquidation

Spread The gap between the live market price and the rate the card uses when converting crypto for a purchase. Spread is rarely disclosed as a named fee. It shows up in the actual sell rate at checkout, and it is one of the harder costs to compare across cards.

- Gemini: Spread applies on rewards redemption; not at the point of purchase

- Coinbase: Spread applies when liquidating crypto assets to fund a payment

- Nexo: Spread may apply on weekend FX conversion; weekday purchases use the Mastercard interbank rate

- KAST: Near-zero spread on USDC/USDT spend; spread applies if topping up with volatile assets

- Bybit: Spread applies on crypto liquidation; exact rate depends on asset and market conditions at time of transaction

FX Fee An extra charge when a purchase settles in a currency other than your card's base currency. FX pricing is one of the fastest ways for a card to become expensive, particularly for international travel or cross-border online spend.

- Gemini: 0% FX fee; Mastercard network rate applies

- Coinbase: 0% stated FX fee on USD spend; check Visa rate on non-USD purchases

- Nexo: 0% on weekdays using Mastercard interbank rate; weekend FX markup applies — rate not always published in advance

- KAST: 0% FX fee on USDC/USDT purchases; check rate on non-stablecoin spend

- Bybit: 0% for in-network spend; FX markup applies on cross-currency transactions

ATM Fee The flat or percentage fee charged by the card issuer for cash withdrawals. Most cards offer a free monthly allowance. After that allowance runs out, the per-transaction cost can make small cash withdrawals expensive quickly.

- Gemini: $0 fee up to $1,000/month; $2.50 flat fee per withdrawal after

- Coinbase: $1,000/day ATM limit; operator fees apply; issuer fee structure should be confirmed

- Nexo: $10,000/month free ATM allowance; $2 flat fee per withdrawal after the limit; physical card currently paused

- KAST: ATM allowance varies by tier; confirm current limits before relying on cash access

- Bybit: Up to €10,000/month free ATM withdrawals (tiered); fee applies after limit

Top-Up Fee A charge to add funds to the card or linked balance. Bank transfer top-ups are usually free. Card top-ups and crypto deposits sometimes carry a fee or spread. This is worth checking for any card that requires a separate funding step before you can spend.

- Gemini: Funded through Gemini account balance; no separate top-up fee stated

- Coinbase: Funded directly from Coinbase balance; no separate top-up fee for USD or USDC

- Nexo: Funded through Nexo credit line or balance; check for fees on specific deposit methods

- KAST: Stablecoin top-up (USDC/USDT) is the primary low-cost route; top-up fees for other assets should be confirmed

- Bybit: Funded from Bybit exchange balance; confirm any fee on specific asset deposits

Physical Card Or Shipping Fee A one-off cost to order or replace the physical card. Free virtual crypto cards are standard across all five cards here. Physical card access and shipping terms vary by issuer and region.

- Gemini: Physical card included; shipping fee should be confirmed against current terms

- Coinbase: Physical card available; check current shipping and replacement fee

- Nexo: Physical card issuance currently paused; virtual card only for new users

- KAST: Physical card available on eligible tiers; confirm issuance and shipping fee

- Bybit: Virtual card available immediately; physical card availability and shipping fee should be confirmed by region

Small Transaction Or Declined Transaction Fee An extra charge on low-value purchases or failed payments. Less common on stronger cards, but still present on some prepaid and balance-based products. Worth checking before using a card for frequent small purchases.

- Gemini: No stated small transaction or declined transaction fee

- Coinbase: No stated small transaction or declined transaction fee

- Nexo: No stated small transaction or declined transaction fee

- KAST: No stated small transaction or declined transaction fee; check for any sub-threshold rules at current tier

- Bybit: No stated small transaction or declined transaction fee

Inactivity Fee A fee charged after a period without card use. Most cards on this list do not charge inactivity fees, but the absence of a fee at launch does not guarantee the same terms going forward.

- Gemini: No stated inactivity fee

- Coinbase: No stated inactivity fee

- Nexo: No stated inactivity fee

- KAST: No stated inactivity fee; confirm this is not a waived launch-period term

- Bybit: No stated inactivity fee

Worked Examples

These examples show how fees and rewards interact in real spending scenarios. All figures use stated card terms. Where a rate range applies, the conservative end is used.

Example 1: $500 in everyday US spending — Gemini vs Coinbase

You spend $500 on groceries and dining in the US using each card, funded from a crypto or stable balance.

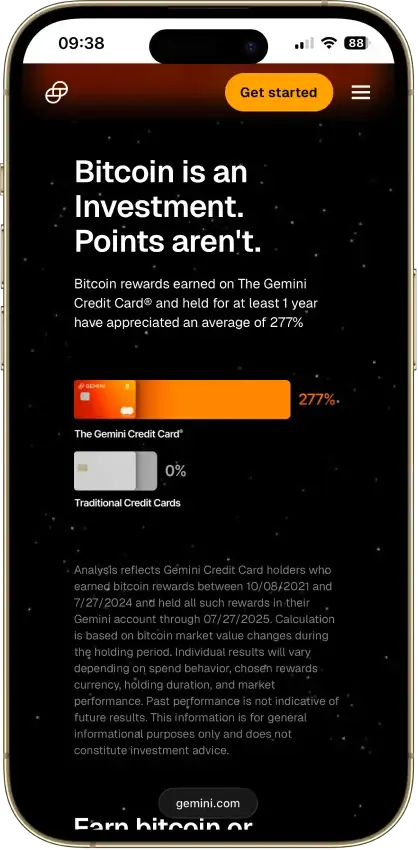

With the Gemini Card, the $500 purchase does not trigger a crypto sale. The card charges 0% FX fee and no conversion fee. At a 3% average reward rate on eligible categories, you earn $15 back in crypto. Net cost of spending: $0 in fees, $15 reward received.

With the Coinbase Visa Debit Card, spending from a USDC balance also avoids the 2.49% liquidation fee. At a 4% reward rate on the active rotating category, you earn $20 back. If you fund the same $500 spend from ETH instead, the 2.49% fee adds $12.45 in cost, reducing net reward value to $7.55.

Both cards are cheap when you stay in USD or USDC. The Coinbase card can reward more in the right category, but the penalty for spending from volatile assets is steep.

Example 2: €400 weekend travel spend in Europe — Nexo vs Bybit

You spend €400 across a weekend in a non-home currency, using each card for restaurant meals and transport.

With the Nexo Card on a weekday, 0% FX applies and you spend at the Mastercard interbank rate. At 2% NEXO cashback, you earn the equivalent of €8 back. On a weekend, a markup applies to the exchange rate. A conservative 1% estimate adds €4 in hidden cost, reducing net reward value to roughly €4.

With the Bybit Card at a base cashback tier, assume 2% back. On in-network spend, 0% FX applies and you earn €8. On cross-currency spend, the FX markup reduces that. At a conservative 1% markup, the net reward is again around €4.

Nexo is the stronger option when you can confine foreign spend to weekdays. On weekends, the two cards are roughly comparable at base tier rates.

Example 3: $200 ATM cash withdrawal — Nexo vs Gemini

You withdraw $200 cash while traveling. Nexo's free ATM allowance is $10,000/month, so this withdrawal falls within the free tier — issuer fee: $0. Gemini's free allowance is $1,000/month. If you have not yet reached the limit, the withdrawal is also free. If you have already used the allowance, the Gemini fee is $2.50 flat. In both cases, the ATM operator may add its own surcharge regardless of issuer fee.

For occasional cash access, both cards are effectively free within their monthly allowance. Nexo's higher free-withdrawal ceiling gives it an edge for frequent or higher-value cash use.

Stablecoin Spending Vs Selling Crypto At Checkout

Stablecoin spending is often the cleaner low-fee route because the checkout value is easier to predict. If a card lets you fund with USDC and converts near 1:1 into a spending balance, your budget is easier to manage and the cost is easier to understand before you tap the card. Conversion spread is lower, there is no volatile asset being liquidated mid-transaction, and in most jurisdictions the tax position is simpler. USDT spending works on the same logic — predictable value at checkout, lower spread, less reporting friction.

Sell-to-spend cards work differently. They can still be useful, especially for users who want to spend directly from BTC or ETH holdings without maintaining a separate fiat balance. The price can drift once spread is included, and each sale may add tax reporting work depending on your jurisdiction. For users already tracking crypto disposals, the added reporting burden may be manageable. For users who want to keep spending simple, it usually is not.

The choice comes down to how much you value predictability at checkout versus flexibility in what you hold. These two paths serve different needs:

Stablecoin-first spending usually fits users who want:

- More predictable checkout value

- Lower volatility at spend time

- Cleaner budgeting

- Less surprise from conversion timing

Selling crypto at checkout is a better fit for users who want:

- Direct use of BTC or ETH balances without converting to fiat first

- Fewer idle fiat balances sitting in a card account

- One app for holding and spending without managing multiple balance types

- Spending flexibility over cost certainty

Foreign Transaction Fees And ATM Fees On Crypto Cards

Foreign spending and ATM withdrawals can change the effective cost of a card quickly. Some cards advertise competitive local spend pricing and then add a weaker FX rate, a weekend markup, or a flat ATM fee that makes travel significantly more expensive than expected. For European users in particular, the weekday-versus-weekend FX split on cards like Nexo is one of the more consequential terms to check before spending abroad.

The following areas account for most of the gap between how cheap a card looks and what it actually costs in international use:

- Foreign Purchase Fee: Whether the card charges a stated cross-border or foreign transaction fee. A 0% annual fee does not help if every non-local purchase adds a separate card charge.

- FX Spread Or Markup: The exchange rate used for non-home-currency purchases. A weak FX rate can cost more than a visible foreign transaction fee over repeated transactions.

- Weekend FX Rule: Whether the FX rate changes on weekends or outside market hours. Weekend pricing can make the same card materially more expensive for travel or leisure spend.

- ATM Fee: The flat fee or percentage charged by the issuer for cash withdrawals. Small cash withdrawals can become expensive quickly once a fixed fee is applied.

- Free ATM Allowance: How much cash can be withdrawn before the issuer fee starts. A useful free allowance can still make a card work well for occasional travel cash access.

- Operator Fee: The extra fee charged by the ATM owner, separate from the card issuer's charge. Even when the issuer fee is low, the machine itself can raise the final cost.

Are Crypto Cashback Cards Worth It After Fees?

Crypto rewards cards are only worth chasing when the reward survives the full cost structure. A 1% to 3% reward rate looks attractive until spread, plan fees, foreign transaction charges, or cash-withdrawal costs absorb most of it. The real question is not the headline reward rate. It is what remains after the full spending route is accounted for.

Rewards become weaker in specific situations. If the reward asset is volatile, the value you see at earning time may not match the value at redemption. If the rewards are tied to a paid tier or require staking a platform token, the cost of maintaining that position eats into the return. For fee-conscious users, lower cost at checkout often delivers more consistent value than a higher but conditional headline rate.

The question of whether cashback offsets fees depends on how you actually use the card. Two contrasting paths illustrate where the math works and where it does not:

When cashback tends to offset fees:

- Reward is paid in a stable or widely redeemable asset

- Spending stays within the card's low-cost route (USD, USDC, weekday FX)

- No paid tier is required to access the stated rate

- Monthly spend volume is high enough for the reward to outweigh any fixed costs

When fees tend to outweigh cashback:

- Reward asset is volatile or difficult to redeem

- Spend includes FX conversion, weekend markups, or liquidation fees

- The headline rate requires staking, a paid plan, or a minimum balance

- ATM withdrawals or physical card fees add recurring cost outside the reward path

Free Crypto Virtual Cards Vs Physical Crypto Cards

Free virtual cards are often the right choice for users who spend online, add the card to a mobile wallet, and want instant access without paying shipping or replacement fees. A virtual card can be issued in minutes and works immediately through Apple Pay or Google Pay at contactless terminals. Physical cards become more practical once you need ATM access, travel to merchants that do not accept wallet payments, or want a backup for situations where your phone or app is unavailable.

The decision between virtual and physical also carries a cost dimension. Shipping fees, physical card issuance charges, and replacement fees can add up, particularly on cards that do not include the physical card at the base tier. Nexo's physical card is currently paused for new users entirely, which makes the virtual-versus-physical question moot for that card until issuance resumes.

Virtual cards are the better option when:

- You mainly shop online or use contactless mobile payments

- You want instant access after approval without waiting for delivery

- You use Apple Pay or Google Pay regularly

- You want to avoid shipping, issuance, or replacement costs

Physical cards become more important when:

- You need ATM access for cash withdrawals

- You travel frequently or visit merchants that reject mobile wallet payments

- You want a fallback option when your phone or app is unavailable

- You need wider acceptance across point-of-sale terminals in different regions

Crypto Debit Cards Vs Crypto Credit Cards On Fees

Fee behavior changes as much by card model as by brand. Some cards spend directly from a balance, some delay repayment like a traditional credit card, and some work like prepaid spending accounts. The cheaper option depends on how the card funds purchases and where the added cost appears in that process. Cards without identity verification — no-KYC cards — tend to sit in the prepaid category and often carry higher top-up or issuance fees to offset the reduced compliance overhead.

| Card Model | Usually Cheaper For |

|---|---|

| Crypto Debit Card | Spending from USD or stablecoin balances |

| Crypto Credit Card | Everyday spending when the balance is repaid on time |

| Prepaid / Balance Card | Stablecoin top-ups, online spend, and controlled travel use |

Credit cards often come out cheaper when they avoid crypto liquidation and the balance is paid in full each month. Debit and prepaid cards can still be efficient, especially when they spend directly from USD or stablecoins, but they become less competitive once conversion spread or cash-access fees start to accumulate.

Which Type Of Low-Fee Crypto Card Fits Your Use Case?

The cheapest card for one person can be the wrong choice for someone else. The right pick depends on what balance you want to spend from, where you live, and whether your primary use is daily purchases, online checkout, travel, or foreign-currency spending. Cost differences between cards are small when you use them inside their optimized path. They grow quickly once you step outside it.

| User Type | Card |

|---|---|

| Daily Stablecoin Spender | KAST Card |

| U.S. Rewards User | Gemini Card |

| EEA User Wanting Cheap FX | Nexo Card |

| Online-Only User Needing A Virtual Card | Bybit Card |

| Travel User Needing ATM Access | Nexo Card |

KAST is the cleaner pick for stablecoin-first spending in a wide range of countries. Gemini works best for U.S. users who want rewards without triggering a crypto sale at checkout. Nexo is the more practical option for European users focused on weekday FX and ATM use. Bybit is the simpler virtual-card choice if you already use the exchange and want fast online spending access without a separate account setup.

Common Crypto Card Fees To Avoid

Some of the most expensive card terms sit outside the headline fee. A card can look cheap at signup and become more expensive through conversion costs, foreign spend charges, or ATM pricing that only becomes visible once you start using the card regularly.

The following patterns appear most often on cards that look cheap and spend expensively. Each one is worth checking before you commit:

- No annual fee paired with expensive conversion spread on every non-stable transaction

- Free virtual card, but a paid physical card with a shipping fee on top

- Strong rewards rate locked behind staking requirements or a paid tier

- Small transaction fees that add up on daily low-value purchases

- Inactivity fees on balances left in a dormant card account

- Declined transaction fees that apply even when your balance was technically sufficient

- Competitive local spend pricing with weak FX rates on any non-home-currency purchase

- A useful free ATM allowance followed by steep per-withdrawal fees

- Rewards paid as platform tokens or points that are difficult to redeem or subject to volatility