Overview

Introduction

Stablecoins are crypto tokens designed to hold a steady price against a reference asset, almost always the US dollar.

That one sentence is the short answer, but the fuller picture matters before you use one. A stablecoin is not a bank account, not a government-backed currency, and not risk-free money. It is a token issued by a company or protocol with its own rules around reserves, minting, redemptions, and controls. Whether a stablecoin actually stays close to $1 depends on how well those rules hold under pressure.

This guide covers what stablecoins are, how the main types keep their price, which tokens matter and why, and where things go wrong.

Key Takeaways

- What it is. A stablecoin is a crypto token designed to track the value of another asset, usually one dollar.

- What it changes. Stablecoins let users move dollar-like value across exchanges, wallets, apps, and blockchains without using bank rails every time.

- Main risk or limitation. A peg can fail if reserves, redemption access, issuer controls, smart contracts, chains, or platforms break under stress.

What Are Stablecoins?

Stablecoins are cryptocurrencies designed to hold a steadier value than coins like Bitcoin or Ethereum by tracking an outside asset. Most target $1, so one token is meant to stay close to one dollar in normal market conditions.

But that design is not the same thing as cash. A dollar bill is a direct form of money. A dollar stablecoin is a token issued by a company or a smart contract system, with specific rules that govern how new tokens are created, what backs them, and how holders can get their money back. Those rules vary by issuer and design, and they matter a lot when markets get stressed.

Two distinctions are worth keeping in mind from the start:

- A stablecoin is a crypto asset, so it moves through wallets, exchanges, smart contracts, and blockchain networks.

- A stablecoin is only as dependable as its backing, redemption route, issuer controls, and market liquidity.

CryptoSlate's stablecoin market coverage tracks the sector in real time, including market cap, dominance, and price data across the major tokens. The core idea stays the same across all of them: stability is the goal, not a guarantee.

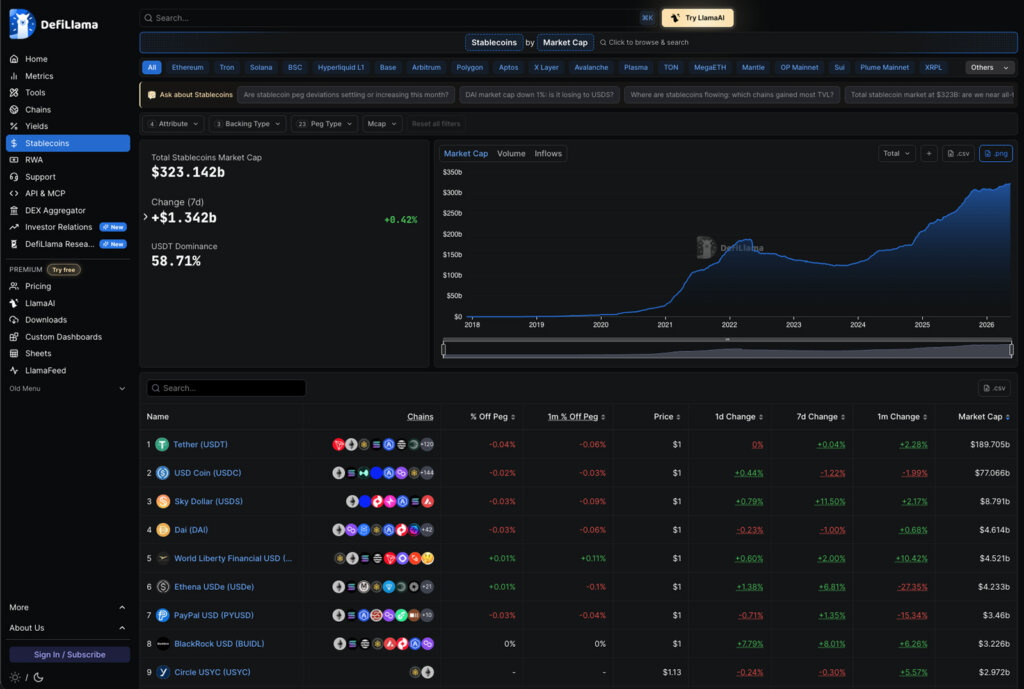

Top Stablecoin Crypto Assets by Market Cap

How Stablecoins Keep Their Peg

A stablecoin keeps its price stable through some combination of backing assets, redemption rights, and market incentives. The basic logic is that if a token can reliably be created and redeemed near its target value, traders have a reason to push its price back toward the peg when it drifts.

For a fiat-backed stablecoin, the process is relatively straightforward. A user or institution sends dollars or approved cash-equivalent assets to the issuer. The issuer mints new tokens and sends them to the user. Those tokens circulate on blockchains, exchanges, payment apps, and DeFi protocols. When a holder wants to exit, they redeem the token with the issuer, and the issuer removes the redeemed tokens from circulation.

In practice, the peg can still drift. A token meant to trade at $1 might sit at $0.998 or $1.002 due to exchange liquidity, chain congestion, fees, redemption limits, or stress in the issuer's reserves. That gap is usually small, but it widens fast when confidence drops.

Three pressure points drive most failures:

- Redemption needs a clear path back to the reference asset.

- Collateral needs enough value and liquidity to survive stress.

- Algorithmic supply changes need sustained market confidence to keep working.

The market is large enough that these mechanics affect everyday users, not just traders. DeFiLlama's stablecoin dashboard showed about $323 billion in total stablecoin market cap at the time of writing, with USDT holding close to 59% dominance.

At that scale, redemption quality, liquidity depth, and chain support are practical concerns whether you're moving $500 or $500,000.

Think of the mechanism as a loop. A user deposits dollars or collateral, an issuer or protocol mints the token, the token circulates on-chain, and the holder either trades it or redeems it through the available path. Reserve risk sits near the deposit stage, market price risk sits in circulation, and redemption path risk shows up at the exit. Network transfer risk runs underneath the whole loop, on every chain the token touches.

Types of Stablecoins and What Backs Them

Stablecoin types differ mainly by what supports the peg. The backing can be bank deposits, Treasury bills, crypto collateral, commodities, supply incentives, hedged positions, or a mix of assets and rules.

| Type | How it works |

|---|---|

| Fiat-backed stablecoin | The issuer holds cash, bank deposits, Treasury bills, or similar reserve assets and issues tokens meant to redeem near 1:1. |

| Crypto-backed stablecoin | Users lock crypto collateral in a protocol, often above the value of the stablecoins they mint. |

| Commodity-backed token | The token tracks a commodity such as gold and depends on custody, redemption, and audits of the underlying asset. |

| Algorithmic stablecoin | Software incentives try to expand or contract supply to defend the peg, often without full high-quality reserves. |

| Hybrid or synthetic dollar | The product combines collateral, hedging, protocol incentives, or yield strategies to create dollar exposure. |

| Yield-bearing or rewards-linked token | The token or wrapper passes through some form of yield, reward, or protocol return while trying to stay close to a target value. |

The table is a starting point, not a safety ranking. Fiat-backed tokens still carry issuer and banking risk. Crypto-backed tokens still face smart-contract, oracle, and liquidation risk. The type tells you what to check, not whether the token is safe.

Stablecoin Examples: USDT, USDC, DAI, PYUSD, and More

No major stablecoin is a universal recommendation. Each one teaches a different trust model, and the right choice depends on what you need: liquidity, issuer access, network support, or regulatory fit.

| Example | What it shows |

|---|---|

| USDT | The largest liquidity network for dollar stablecoins, widely used across centralized exchanges and several blockchains. |

| USDC | A major regulated-dollar stablecoin often used in wallets, exchanges, apps, and institutional payment flows. |

| DAI and USDS | DeFi-native stablecoin lineage with crypto collateral, governance, and newer real-world-asset exposure. |

| PYUSD | A payment-company stablecoin that shows how consumer brands can issue dollar tokens through regulated partners. |

| PAXG and XAUT | Gold-linked tokens that track a commodity rather than a fiat currency. |

| USDe | A synthetic dollar design that depends on hedging and protocol mechanics rather than simple dollar deposits. |

| Frax USD | A hybrid stablecoin lineage shaped by collateral changes and lessons from earlier algorithmic designs. |

The list is not limited to dollar tokens. CryptoSlate's euro stablecoin category covers fiat-backed tokens that track euro exposure instead, which changes the issuer, reserve structure, and regional rules a user needs to check.

USDT and USDC are the two dollar stablecoins most users compare first. The trade-off usually starts with liquidity and network reach on one side, and reserve transparency, regulatory posture, and direct redemption access on the other.

Before choosing between tokens, it helps to check four things:

- What backs the token.

- Who controls redemption and under what conditions.

- Where liquidity is deepest.

- Which networks the sender and receiver both support.

What Stablecoins Are Used For

The most common use is also the simplest: holding a dollar-like balance inside crypto markets without converting back to a bank account after every trade. But stablecoins support a wider range of practical flows beyond that.

In trading, stablecoins act as quote currencies. A user sells BTC into USDT or USDC, waits in a dollar-denominated balance, then buys another asset when ready, without triggering a bank withdrawal each time. That same logic applies to anyone who wants to pause exposure during volatility without fully exiting the market.

Beyond trading, stablecoins show up across a range of use cases. Some are operational, others are more experimental:

- Moving value between exchanges when both venues support the same token and network.

- Supplying collateral, liquidity, or swap routes in DeFi protocols and decentralized exchanges.

- Paying contractors, merchants, or apps where crypto payments are accepted.

- Spending through crypto card programs when a provider supports the user's token and jurisdiction.

- Depositing and settling on prediction market platforms, where dollar-pegged tokens are often the only accepted currency. CryptoSlate's prediction markets section covers platforms that rely on stablecoins to price outcomes and pay out winnings in a currency that does not swing 10% between a bet and its resolution.

The benefit is speed and composability. A stablecoin payment can settle quickly on-chain, but the user still has to manage chain fees, address accuracy, issuer risk, platform custody, and local tax or reporting obligations.

For businesses and treasury teams, stablecoins can reduce settlement friction when counterparties operate across borders or crypto venues. They can also add new operational complexity, since wallets, signing policies, exchange limits, and redemption routes all become part of cash management in ways that bank accounts do not require.

Stablecoins vs Cash, Bank Deposits, CBDCs, and Volatile Crypto

Stablecoins look like dollars on a screen, but they are not the same instrument as cash, a bank balance, a central bank digital currency, or a volatile crypto asset. The difference lies in the legal claim and the system that records ownership.

| Comparison | Main difference |

|---|---|

| Stablecoin vs cash | Cash is money itself, while a stablecoin is a tokenized claim or mechanism designed to track money. |

| Stablecoin vs bank deposit | A bank deposit is a liability of a regulated bank, while a stablecoin is issued by a company or protocol. |

| Stablecoin vs CBDC | A CBDC would be issued by a central bank, while stablecoins are private or protocol-issued assets. |

| Stablecoin vs BTC or ETH | BTC and ETH float freely, while stablecoins target a reference price. |

| Stablecoin vs exchange balance | An exchange balance is an account entry on a platform, while a stablecoin can usually be withdrawn to a supported wallet. |

The insurance difference is especially important in the United States. The FDIC explains that deposit insurance covers deposits at insured banks and does not apply to crypto assets issued by non-bank entities.

Two practical points follow from that distinction:

- A stablecoin holder typically relies on issuer reserves, redemption rules, platform custody, and market liquidity rather than deposit insurance.

- A CBDC would be government-issued central bank money, while stablecoins are privately issued or protocol-managed tokens that run on crypto networks.

Stablecoin Risks: Depegs, Reserves, Freezes, Chains, and Platforms

Stablecoin risk depends on where in the system the failure happens. A token can hold its peg on one exchange while withdrawals are paused elsewhere. An issuer can remain solvent while a user loses funds through a wrong-network transfer. Understanding these failure points by category is more useful than treating all stablecoins as one risk level.

| Risk | What to check |

|---|---|

| Reserve risk | Whether the backing assets are high quality, liquid, segregated, and regularly reported. |

| Redemption risk | Whether ordinary holders can redeem directly or must sell through exchanges. |

| Depeg risk | How far the token has traded from its target during stress and how quickly liquidity returned. |

| Issuer control | Whether the issuer can freeze or blacklist tokens under legal or policy rules. |

| Smart-contract risk | Whether protocol contracts, oracles, and liquidation systems can fail or be exploited. |

| Chain risk | Whether the network has congestion, outages, high fees, or confusing token standards. |

| Platform custody | Whether a wallet, exchange, lender, or app controls withdrawals or private keys. |

| Yield risk | Whether a yield offer adds lending, smart-contract, leverage, liquidity, or counterparty exposure. |

Reserve and redemption risk sit at the center. If reserves are hard to value or hard to liquidate, the token may trade below its target when holders rush to exit at the same time. If direct redemption is limited to large institutions, smaller users depend on exchange liquidity instead of going to the issuer, which adds a layer of exposure that is easy to miss.

Freeze powers are another risk that beginners often overlook. Some fiat-backed issuers can block addresses or freeze tokens to comply with legal orders, sanctions, or platform policies. That may be necessary for regulated payment use, but it means holding a stablecoin in a self-custody wallet does not remove the issuer's ability to freeze your specific balance.

Where you hold a stablecoin matters as much as which one you hold. The custody layer creates meaningfully different tradeoffs. A standard crypto wallets setup gives users a place to hold and send stablecoins outside of exchange accounts. A centralized custodial wallet may add recovery options and compliance controls. A decentralized self-custodial wallet shifts key management and signing risk to the user entirely.

Stablecoin yield is a separate exposure layer that often gets treated as a bonus rather than a risk. Holding USDC or USDT in a wallet is one risk profile. Lending it through a protocol, depositing it into a liquidity pool, bridging it across chains, or using it in a leveraged strategy adds new ways to lose money even if the stablecoin itself stays close to $1.

Wrong-chain transfers are one of the most common operational mistakes new users make. Legitimate USDT sent over a network the receiving exchange does not support may not appear in the receiving account even if the blockchain shows the transaction as successful. Recovery depends on whether the recipient controls that address on that network, and many exchanges do not recover wrong-chain deposits.

USDT vs USDC and Other Trade-Offs

USDT vs USDC is not a universal safety ranking. It is a set of trade-offs between liquidity, chain support, reserve disclosure, regulatory posture, redemption access, freeze powers, and the specific exchange or app a user needs.

Tether USDT tends to have the deepest trading-pair liquidity across global exchanges and the widest spread across transfer networks. USD Coin USDC is more common in US-regulated, payment, and app-oriented contexts. That difference can affect fees, withdrawal routes, supported chains, and how quickly a user can move between crypto and bank-linked venues.

Regulation shapes this comparison because rules affect which issuers can serve a market, what reserves must support a token, what disclosures are required, and how exchanges or apps can offer the asset. Regulatory clarity reduces some risks but does not eliminate user-level ones.

The current US regulatory track has two relevant layers:

- The GENIUS Act became Public Law 119-27 on July 18, 2025, and requires permitted payment stablecoin issuers to maintain at least 1:1 identifiable reserves.

- The OCC's 2026 proposal covers implementation rules for payment stablecoin issuers under its jurisdiction.

For users, these trade-offs show up in practical details rather than abstract compliance frameworks. The relevant questions are:

- Which issuer can serve your jurisdiction.

- Which token the exchange, wallet, or app you are using actually supports.

- How often reserve reports are published and what asset categories they cover.

- Whether redemption, freeze powers, and compliance controls are documented publicly.

- Whether local rules classify the token as a payment stablecoin, e-money token, asset-referenced token, or something else.

In the EU, MiCA creates uniform rules for crypto assets and separates asset-referenced tokens from e-money tokens. ESMA's interim MiCA register was last updated on May 4, 2026. Regulation can improve reserve standards, licensing, and supervision, but a user still needs to verify the exact issuer, token, chain, wallet, exchange, and redemption path for their own situation.

FAQs

Are stablecoins safe?

Stablecoins are safer than volatile crypto only in the narrow sense that they aim to hold a steadier price. They can still lose value through depegs, weak reserves, issuer failure, platform freezes, smart-contract bugs, bridge exploits, wrong-network transfers, or unsafe yield products. Safety depends on the specific token, issuer, platform, and how you use it.

Can a stablecoin lose its peg?

Yes. A stablecoin can trade below or above its target when confidence drops, liquidity thins, reserves come into question, redemptions slow, or the mechanism that supports the peg breaks. The risk is higher when the backing is complex, opaque, or dependent on market incentives rather than direct collateral.

Are stablecoins FDIC insured?

Stablecoins are generally not FDIC-insured. FDIC coverage applies to deposits at insured banks, not to crypto assets issued by non-bank entities or held through crypto wallets, exchanges, and protocols.

What are stablecoins backed by?

Stablecoins can be backed by cash, bank deposits, Treasury bills, crypto collateral, commodities, protocol incentives, hedged positions, or a mix of these. The backing model determines which risks are most relevant. The label “stablecoin” alone is not enough to tell you what you actually hold.

What is the difference between USDT and USDC?

USDT typically has broader liquidity and exchange support, especially across global markets and multiple transfer networks. USDC is more common in regulated-dollar, app, and payment contexts. The better fit depends on the venue, chain, jurisdiction, and what you plan to do with the token.

What happens if I send a stablecoin on the wrong network?

The token may not appear in the receiving account even if the blockchain shows the transaction as confirmed. Recovery depends on whether the recipient or exchange controls the receiving address on that specific network and is willing to retrieve the funds. Many exchanges do not offer wrong-chain recovery, or charge a fee that may exceed the transfer amount.