Overview

Introduction

USD Coin (USDC) is a stablecoin pegged to the U.S. dollar, issued by Circle. Unlike Bitcoin or Ethereum, it is not designed to go up in value. One USDC is meant to equal one dollar, and Circle maintains that peg by holding dollar-denominated reserves and letting eligible institutions redeem tokens directly for cash.

That design makes USDC useful for traders who want to stay in crypto markets without price exposure, for DeFi users who need a stable settlement asset, and for businesses that want programmable dollar payments on a blockchain.

But USDC is not a bank account. It does not pay interest, it is not government-insured, and the peg can slip during stress events. This guide covers how it works, what backs it, where it runs, and the risks that matter most for beginners.

Key Takeaways

- USDC is Circle's dollar-pegged stablecoin, built to represent U.S. dollar value on public blockchains.

- It is widely used as a trading quote asset, DeFi settlement token, payment rail, and dollar access tool in 170+ countries.

- USDC depends on Circle, reserve banks, legal access, compatible blockchain networks, and functioning secondary markets.

How USDC Keeps Its Dollar Peg

Most crypto assets fluctuate based on market demand. USDC works differently. Circle issues and redeems USDC against dollar-denominated reserves, backed by highly liquid cash and cash-equivalent assets, redeemable 1:1 for U.S. dollars through Circle's redemption framework. That backing is what makes USDC a fiat-backed stablecoin.

This puts USDC in a different category from two common alternatives. Crypto-backed stablecoins like DAI hold overcollateralized crypto positions as backing. Algorithmic stablecoins try to maintain a peg through incentive mechanisms rather than reserves. USDC's approach is simpler: one token should correspond to one dollar held in reserve for holders' benefit.

The peg holds as long as three conditions are met: holders trust they can redeem at par, reserves stay liquid, and exchanges maintain deep enough markets for everyday users. Circle redeems 1 USDC for 1 USD for eligible Circle Mint users, subject to applicable law and fees. Holders who are not eligible for Circle Mint, which includes most retail users, need to exit through exchanges or wallet apps instead. Circle also publishes reserve information and monthly attestations on its transparency page.

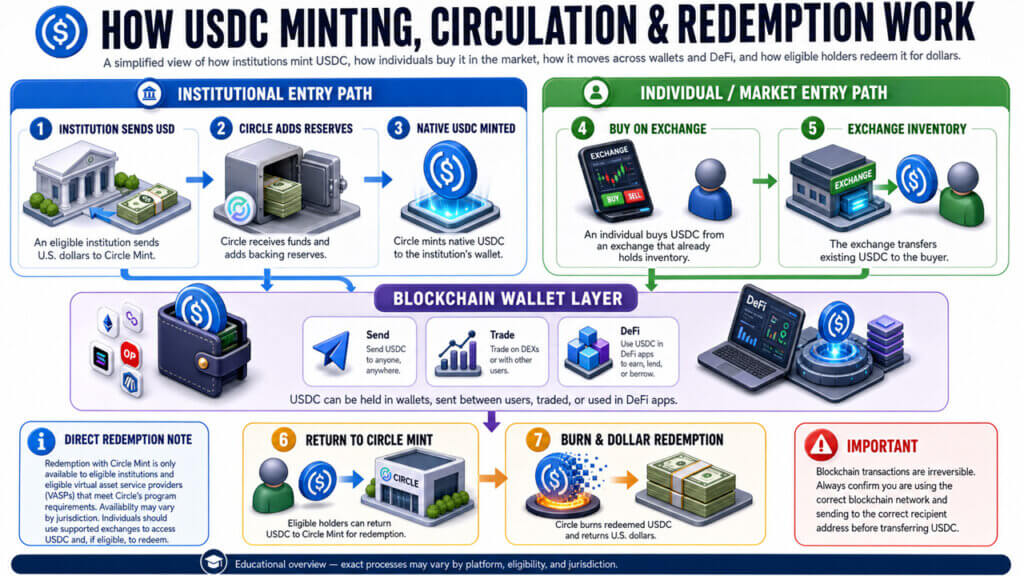

What Happens When USDC Is Minted, Moved, and Redeemed

Circle mints USDC when an eligible business or institution deposits dollars through Circle Mint. When a business deposits USD into its Circle account, Circle issues an equivalent amount of USDC. When that business redeems USDC for dollars, Circle burns the tokens and sends dollars back. Circle Mint is available to institutions, exchanges, wallet providers, banks, and consumer app companies, not to individual retail users.

Most everyday users never interact with Circle directly. They buy USDC through a crypto exchange, a wallet app, an on-ramp service, or a DeFi protocol. The mechanics behind those purchases still trace back to the institutional mint-and-redeem system, but the user experience depends entirely on the intermediary.

Once a user holds USDC, it behaves like any other token on a supported blockchain. It can be held in a self-custody wallet, kept on an exchange, used as collateral in a lending protocol, sent to a merchant, or swapped for another asset.

The clearest way to think about the lifecycle: dollars enter through Circle or a distribution partner, USDC is created onchain, users move it across compatible networks, and USDC is burned when eligible holders redeem it back to dollars.

The diagram below maps one USDC from dollar deposit to blockchain transfer to redemption, with separate institutional and retail access paths.

Where USDC Runs: Native Tokens, Networks, and CCTP

USDC started as an Ethereum token, but it is now a multichain stablecoin available on 32 blockchain networks, including Ethereum, Solana, Base, Arbitrum, Avalanche, Polygon PoS, Stellar, Sui, XRPL, ZKsync Era, and others.

The word “native” carries real weight here. Native USDC is issued directly by Circle on that blockchain. Bridged USDC is a wrapped version created by a third-party bridge, and it carries extra risk. Sending unsupported tokens, including USDT or bridged USDC, to a Circle Mint address can result in permanent loss of funds.

Circle's Cross-Chain Transfer Protocol (CCTP) is built to move native USDC between supported chains without relying on a wrapped-token bridge pool. CCTP burns USDC on the source blockchain and mints USDC on the destination blockchain, creating 1:1 native transfers. This is more reliable than traditional bridging for chains that support it.

The table below shows the practical differences between common USDC transfer methods:

For any USDC transfer, check four things before sending: the ticker (USDC, not USDT), the blockchain network, the receiving address, and the withdrawal fee. A small test transfer to a new wallet or new network is worth the cost.

What USDC Is Used For

USDC is most visible on exchanges, where it gives traders a dollar-like quote asset without leaving crypto markets. A trader can sell ETH into USDC, wait, and later buy another asset without wiring money back to a bank. That does not remove trading risk, but it removes the need to cycle through fiat rails for every trade. Beginners comparing venues can start with CryptoSlate's compiled list of crypto exchanges, or narrow it down to the best exchanges for beginners.

In DeFi, USDC is used as collateral, liquidity, and a settlement asset. Lending protocols, automated market makers, payment apps, and onchain treasuries often prefer stablecoins because stable-denominated accounting is simpler than working with a volatile asset. A loan denominated in USDC is easier to price and manage than one denominated in ETH.

Businesses use USDC when they want programmable dollar settlement. A company can receive USDC from a customer, hold it on a balance sheet, convert it through a payment provider, or route it through a blockchain-based workflow. The exact cost and compliance burden depend on jurisdiction, provider, and transaction size.

How To Earn USDC

USDC is a stablecoin, so it does not generate native protocol staking rewards. It is not designed to increase in value or pay interest, and holders are not entitled to returns earned on Circle's reserve assets.

Any yield from USDC comes from third-party products. The most common routes are lending, liquidity provision, and exchange reward programs:

| Method | How It Works | Native Or Third-Party? | Main Risk |

|---|---|---|---|

| Exchange rewards or earn products | A platform credits rewards for eligible USDC balances. Coinbase runs USDC Rewards as a loyalty program funded by Coinbase itself. Binance Earn lists USDC products with availability that varies by product and region. | Third-party | Custody risk, changing eligibility, variable rates, regional limits, and program discontinuation |

| Lending products | Centralized platforms take custody of USDC and pay interest under their own terms. Nexo offers flexible and fixed-term USDC savings, with rates that depend on the product, loyalty tier, region, and account settings. | Third-party | Counterparty failure, lockups, withdrawal limits, and jurisdiction restrictions |

| DeFi money markets | A wallet supplies USDC to a protocol that lends it to borrowers. Aave and Compound III both pay interest on supplied assets. Compound’s first deployment used USDC as its base asset.> | Third-party protocol | Smart contract bugs, oracle issues, liquidity limits, and collateral settings |

| Liquidity pools | A wallet adds USDC to an automated market maker pool and receives a share of trading fees. Each liquidity provider receives a share of fees earned by the pool. | Third-party protocol | Impermanent loss, pool imbalance, smart contract risk, and paired-asset depeg risk |

| Payment or card rewards | Some card programs let users select USDC or another crypto asset as a purchase reward. The Gemini Credit Card includes USD Coin among selectable crypto reward assets.> | Third-party program | Eligibility changes, card terms, custody, and reward-asset availability |

| Promotional campaigns | Short-lived exchange campaigns may add bonus rewards or vouchers. Product availability often varies by region and rewards rates can change. | Third-party | Expiry, caps, rate changes, and regional restrictions |

| Faucets | Circle’s testnet faucet issues testnet USDC for developers, not real mainnet USDC income. | Not an earning route | Scam risk if a site asks for deposits, private keys, seed phrases, or token approvals |

None of these products pay yield from Circle. The source is always a platform program, a borrower payment, a pool fee, a card reward, or a short promotion. Rates are variable, eligibility can change, and a product denominated in USDC can still lose money through custody failure, protocol failure, depeg stress, or withdrawal limits.

Can You Stake USDC?

No. USDC cannot be staked natively. It is a stablecoin issued by Circle, not a proof-of-stake network asset, and the token itself does not generate interest or returns for holders.

Products labeled “USDC staking” usually mean something else. They may involve lending USDC to a centralized platform, depositing USDC into an exchange earn product, supplying USDC to a DeFi protocol, or providing USDC as liquidity in a pool. None of those are validator staking in the way that Ethereum staking works, where tokens secure a blockchain network.

Before using any USDC yield product, check for the following:

- Counterparty risk (who controls the funds)

- Custody risk (can you withdraw at any time)

- Smart contract risk (has the protocol been audited)

- Depeg risk (what happens if USDC briefly moves off $1)

- Variable rates (what triggers a rate change)

- Lockups and redemption limits

- Regulatory or jurisdiction restrictions

- Network mismatch risk when moving USDC between chains

A product can fail even when USDC holds its peg. A mistaken network transfer can still cause a permanent loss even when the product is fine.

USDC vs USDT, DAI, and Bank Dollars

USDC, Tether (USDT), DAI, and bank dollars all try to solve different versions of the same problem: how to hold or move dollar value. The right comparison depends on what you need.

| Asset or balance | Issuer or backing model | Typical use | Main limitation |

|---|---|---|---|

| USDC | Circle-issued, fiat-backed stablecoin | Exchange settlement, payments, DeFi, treasury flows | Depends on Circle, reserve access, and compliance controls |

| USDT | Tether-issued, fiat-backed stablecoin | High-liquidity trading and global stablecoin transfers | Different issuer, disclosure model, and regulatory profile |

| DAI | Crypto-backed stablecoin from Maker ecosystem, with changing collateral mix | DeFi-native borrowing, lending, and liquidity | Depends on protocol governance and collateral composition |

| Bank dollars | Deposit balance at a bank | Payroll, cards, bank transfers, savings, invoices | Bank hours, jurisdiction, account access, and settlement limits |

USDC is not a central bank digital currency. USDC is issued through regulated Circle affiliates, while a CBDC would be issued by a government or central bank. USDC also does not pay holders the interest Circle may earn on reserves.

USDC also differs from a bank deposit. A bank balance may carry deposit insurance in some jurisdictions and can sometimes be reversed under bank rules. USDC transactions are not reversible once confirmed onchain, which makes it useful for final settlement but risky when funds go to the wrong address.

What Can Go Wrong With USDC?

USDC has three real risk categories, and a beginner should understand all of them before holding or transferring it.

Peg risk is the most obvious. USDC is designed to trade near $1, but exchange prices can slip during stress. Circle's own terms include a “no guarantee of price stability on third-party platforms” clause. That distinction matters during volatile markets, where exchange prices and Circle's 1:1 redemption rate can briefly diverge.

Reserve and banking risk is less visible but equally real. USDC's March 2023 depeg showed what happens when a reserve bank fails. A $3.3 billion USDC reserve deposit held at Silicon Valley Bank, about 8% of the total reserve at the time, became temporarily inaccessible. The situation resolved quickly after U.S. regulators acted, but USDC briefly traded below $0.90 on some exchanges. This is a useful reminder that a fiat-backed stablecoin still depends on the banking system. Details are in Circle's March 2023 statement.

Issuer control risk is the third category. USDC is not a permissionless asset in the way Bitcoin is. Circle can block certain addresses and freeze associated USDC under some circumstances, including suspected illegal activity or valid government orders. That compliance layer makes USDC more acceptable to regulated institutions, but it also means USDC holders can have their funds frozen.

Operational risk sits underneath all three. Sending USDC to the wrong address, routing it over the wrong network, losing a private key, or trusting an insecure exchange can cause loss even if USDC itself stays at $1. A stable price target does not reduce operational risk.

Regulation, Reserves, and Circle’s Role in 2026

USDC's issuer became a public company in 2025. Circle Internet Group's Class A common stock began trading on the New York Stock Exchange under the ticker CRCL on June 5, 2025. Public-company reporting does not eliminate stablecoin risk, but it creates more company-level disclosure than a private issuer would provide.

Stablecoin regulation also moved forward in the United States. The GENIUS Act, framed by the U.S. Treasury in April 2026 as a federal framework for payment stablecoins, would direct Treasury to impose Bank Secrecy Act, anti-money laundering, and sanctions compliance obligations on permitted payment stablecoin issuers. That context matters because USDC is competing to become the compliant dollar token of choice for exchanges, fintechs, and institutions. The same controls that make it acceptable to banks and regulators can become a limitation for users who want a neutral bearer asset.

This regulatory shift also affects other products built on blockchain infrastructure. Prediction markets like those reviewed in CryptoSlate's Polymarket review use stablecoins like USDC for settlement, and any change to stablecoin compliance rules filters through to those platforms too.

USDC reserve holdings are disclosed weekly, and a Big Four accounting firm provides monthly third-party assurance confirming that reserve value exceeds USDC in circulation. Those attestations verify reserve balances at reporting dates. They confirm what is held, not every possible legal, technical, or counterparty outcome. A full financial audit and an attestation are different instruments.

How To Start With USDC SafelyHow To Start With USDC Safely

Start by deciding whether you need USDC at all. For trading, it functions as a dollar-like balance on an exchange. For payments, it can move quickly across supported networks with final settlement. For savings, it is not a bank deposit and it does not generate native yield through Circle.

Next, choose your custody model. An exchange is simpler for beginners, but the exchange controls the account and the withdrawal process. A self-custody wallet gives more control, but you manage private keys, network selection, and transaction finality yourself. Beginners comparing options can start with CryptoSlate's full list of crypto wallets or narrow it down to wallets for beginners.

Before buying or transferring USDC, check four things: the ticker (confirm it is USDC, not USDT or a bridged version), the blockchain network, the receiving address, and the withdrawal fee. Send a small test transfer first when using a new wallet or new network for the first time. More advanced users moving USDC into onchain trading can compare CryptoSlate's list of decentralized exchanges before choosing a venue.

FAQs about USDC

Can you stake USDC?

No. USDC cannot be staked natively because it is a stablecoin issued by Circle, not a proof-of-stake network asset. When a platform advertises “USDC staking,” it usually means lending USDC, depositing it into an earn product, supplying it to a DeFi money market, or providing liquidity in a pool.

How can you earn USDC?

USDC yield normally comes from third-party routes, not from USDC itself. Common options include exchange rewards, centralized lending or savings products, DeFi money markets, liquidity pools, card rewards that let users select USDC, and occasional promotions. Each route depends on a provider, protocol, eligibility rules, variable rates, and withdrawal terms.

Is USDC staking the same as lending?

No. Native staking secures a proof-of-stake network and pays protocol rewards. USDC does not do that. Most products labeled as USDC staking are lending or earn products where a platform or protocol uses deposited USDC to support loans, liquidity, or rewards. The risk profile is closer to credit, custody, or smart contract risk.

What are the risks of earning yield on USDC?

The main risks are counterparty failure, custody loss, smart contract bugs, USDC depegging, changing reward rates, lockups, redemption limits, and jurisdiction restrictions. Network mismatch is also a practical risk because USDC exists on multiple chains. A stable price target does not remove operational or platform risk.

Is earning USDC safer than earning volatile crypto?

It can reduce price-volatility risk because USDC targets $1, but it does not make the yield product safe. A USDC earn product can still fail through the provider, loan book, smart contract, liquidity pool, redemption process, or network transfer route. The risk shifts from market price swings to counterparty, custody, protocol, and peg exposure.