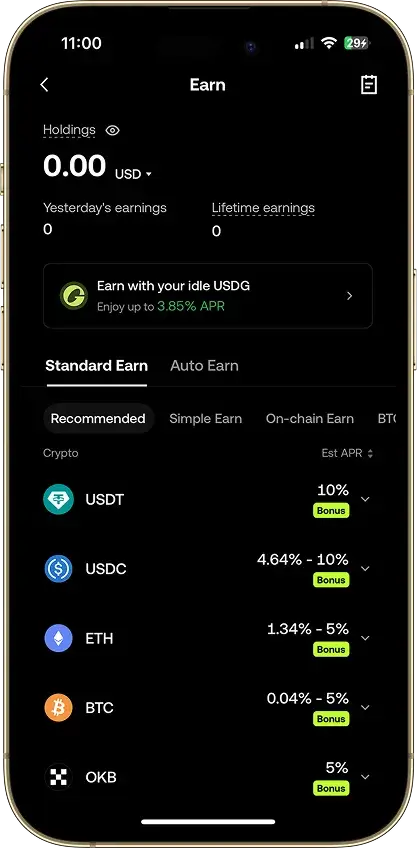

The advertised staking rate only shows one side of the position. The more useful question is what gets taken out before rewards arrive, what it costs to move the asset in and out, and how quickly the funds can actually be used again.

That is where a lot of staking comparisons fall apart. Two platforms can support the same asset and post similar rates, then land in very different places once commissions, spreads, gas, withdrawal fees, and unstaking rules are counted together.

| Friction Point | What It Usually Looks Like | Why It Matters |

|---|

| Validator commission or platform cut | A share of staking rewards kept by the exchange, validator, or protocol layer | Lowers net yield even when the displayed rate looks competitive |

| Buy and sell spreads | Paying above market to enter the asset and below market to exit it | Can wipe out weeks of staking rewards on short holding periods |

| Gas or network fees | Wallet transaction costs, bridging costs, or claim costs onchain | Hits smaller balances hardest and matters more in DeFi flows |

| Withdrawal fees | Exchange fee, network fee, or both when moving assets off-platform | Reduces net return, especially for frequent withdrawals or smaller positions |

| Unbonding periods | Waiting days or weeks after unstaking before funds are released | Reduces liquidity when the user wants to sell, rotate, or move funds |

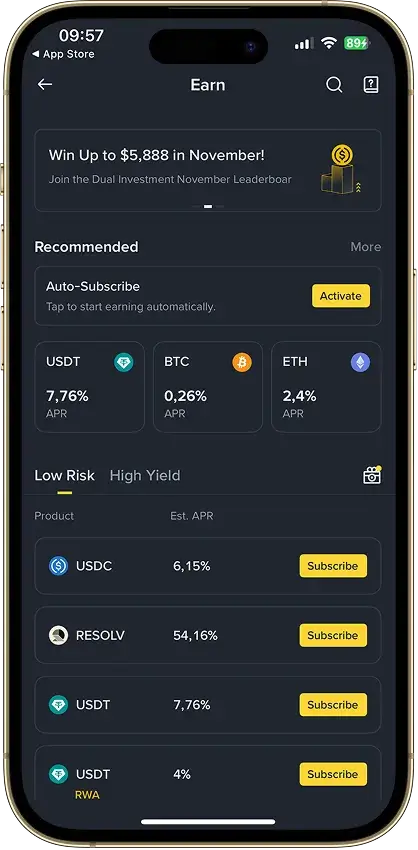

| Early exit limitations | Locked products may cut rewards or delay redemptions | Higher yield often comes with stricter terms |

| Reward payout timing | Daily, weekly, epoch-based, or delayed reward crediting | Affects compounding, tracking, and how quickly rewards become usable |

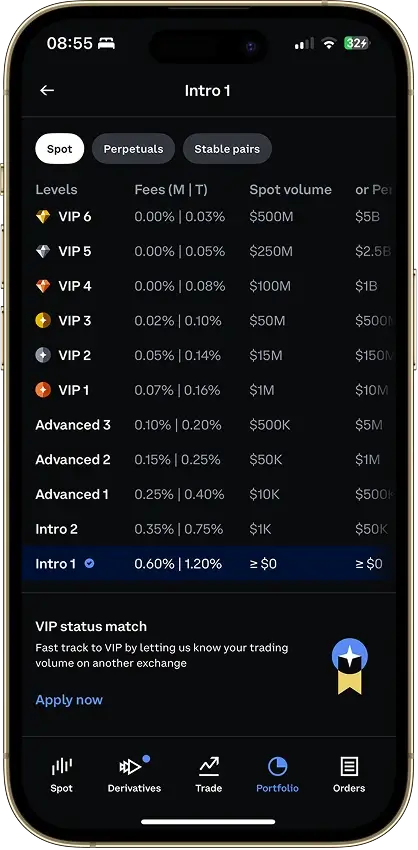

Validator commission or platform cut is often the easiest cost to miss. Some exchanges show a net rate and keep their share in the background. Some DeFi routes make the validator cut more visible. Either way, the number that matters is the net reward after that share is taken, not the gross figure that appears in marketing copy.

Spreads can be just as important as staking yield. A user who buys an asset through a simple conversion flow, stakes it for a short period, then exits through another spread-heavy route may lose more on entry and exit than the staking rewards can make back. That matters most when the position is small or the hold period is short.

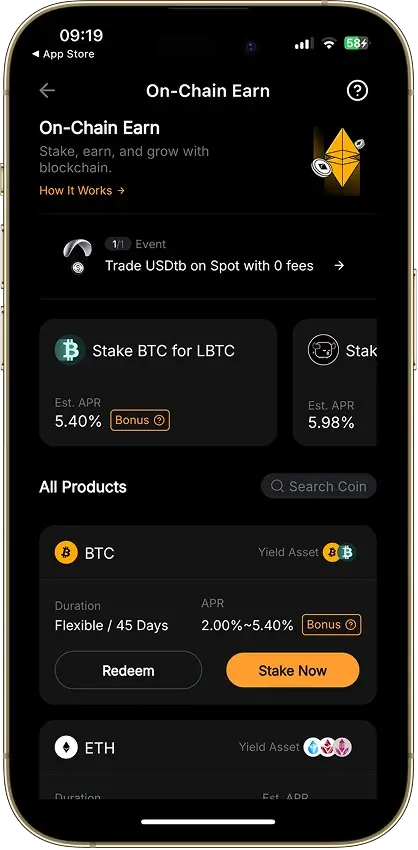

Onchain costs also change the picture. DeFi staking can look cleaner because there is no exchange layer in the middle, but wallet transactions, bridging steps, swaps, and claim flows can all add cost. On smaller balances, those costs can weigh more heavily than the difference between one staking rate and another.

Unbonding periods are another blind spot. Some assets can be unstaked quickly. Others need days or weeks before they become transferable again. That delay matters during sharp price moves, portfolio rotations, or any moment when liquidity suddenly matters more than yield.

Locked products make the same point from a different angle. A higher rate often comes with tighter conditions. Some products reduce or remove rewards on early redemption. Others make users wait until the lock period ends. The rate looks stronger because flexibility has been traded away.

Reward timing should also be read more carefully. Daily crediting feels different from weekly or epoch-based rewards, especially for users who want to compound, move rewards quickly, or keep closer track of what the position is actually generating. A platform that pays slightly less but credits rewards more clearly can still be easier to manage.

That is why the best staking platform is not always the one with the highest posted number. It is often the one where the costs are easier to understand, the exit rules are easier to live with, and the net result still makes sense after every layer of friction is counted.