Choosing the best crypto card comes down to how you actually spend, not which issuer advertises the highest headline reward. A card that looks great for cashback may be a poor fit for travel, stablecoin spending, or day-to-day use if the fees, limits, or availability do not line up with your needs.

A better starting point is to work backward from your use case. The right crypto card is usually the one that fits your region, funding style, and spending habits with the least friction, not the one with the loudest marketing.

Best for Everyday Spending

If you want a crypto card to replace part of your normal card usage, focus on reliability first. Everyday spending works best with a card that has clear limits, simple funding, stable rewards, and an app that makes it easy to manage transactions without surprises.

Cards like the Coinbase debit card or the Crypto.com Visa Card can make sense here because they are built around frequent usage. What matters most is not just the reward rate, but how easy it is to top up, track spending, and avoid hidden costs over time.

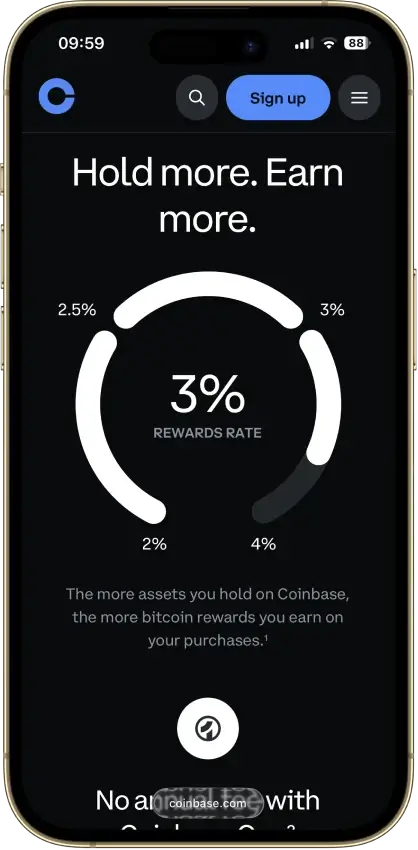

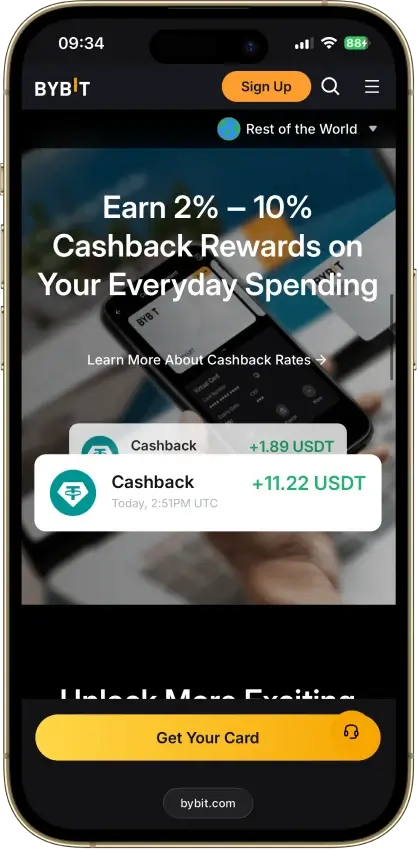

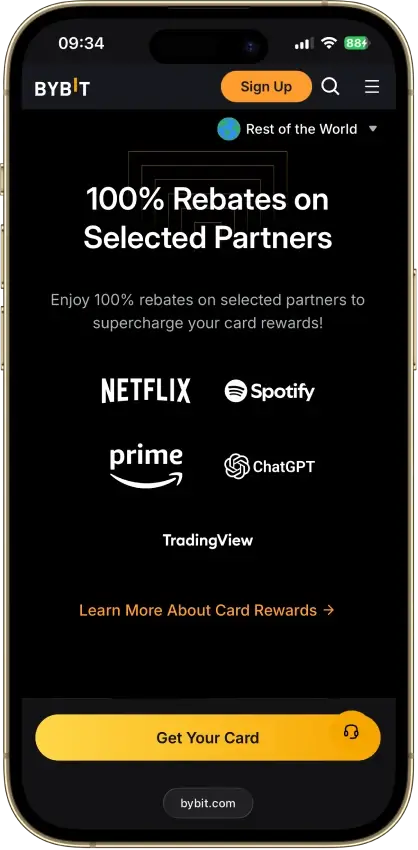

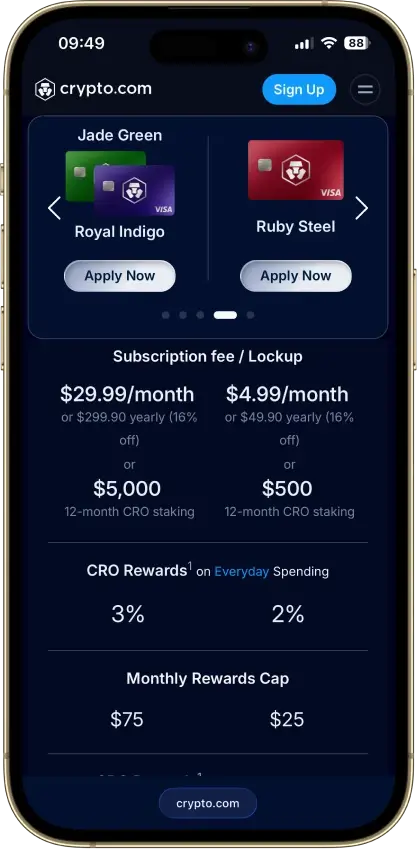

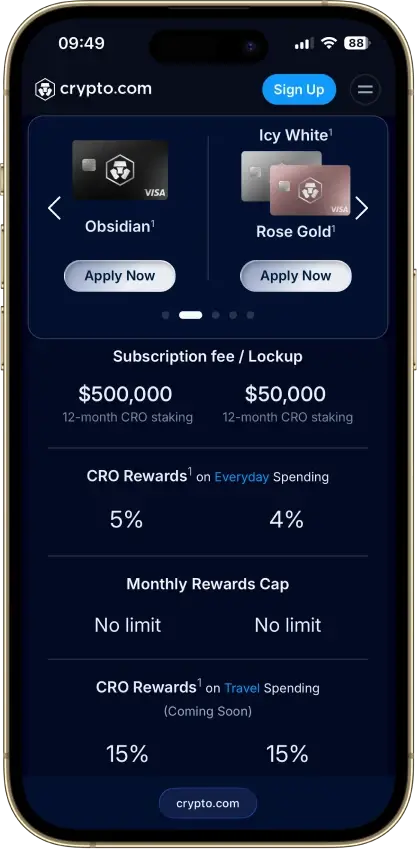

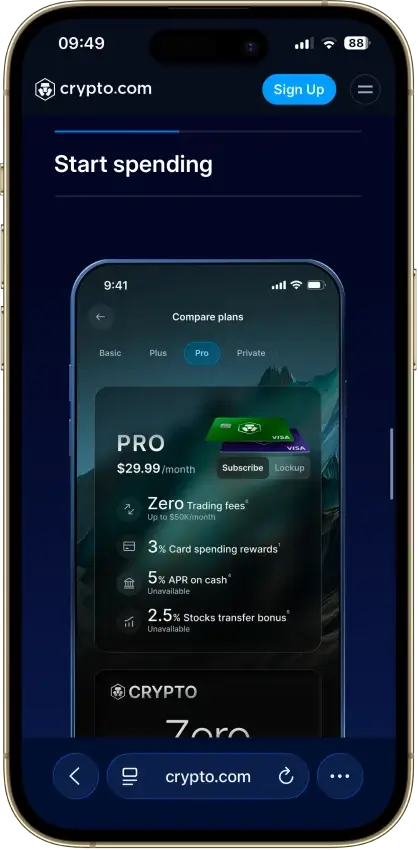

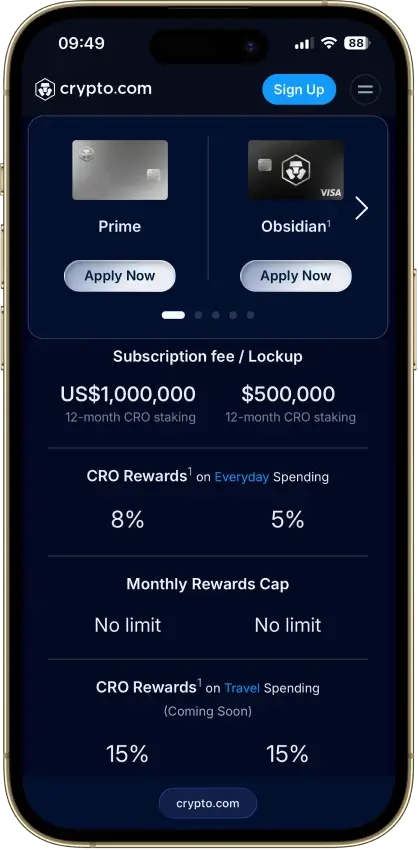

Best for Rewards-Focused Users

If your priority is earning the most value back, look closely at how the reward structure actually works. Some cards advertise high headline percentages, but the real value may depend on spending caps, loyalty tiers, subscriptions, staking, or promotional windows.

A rewards-focused user should compare the asset paid out, the cap on the highest reward category, and whether the better tier requires a meaningful extra commitment. In practice, the best crypto card rewards are the ones you can actually access consistently.

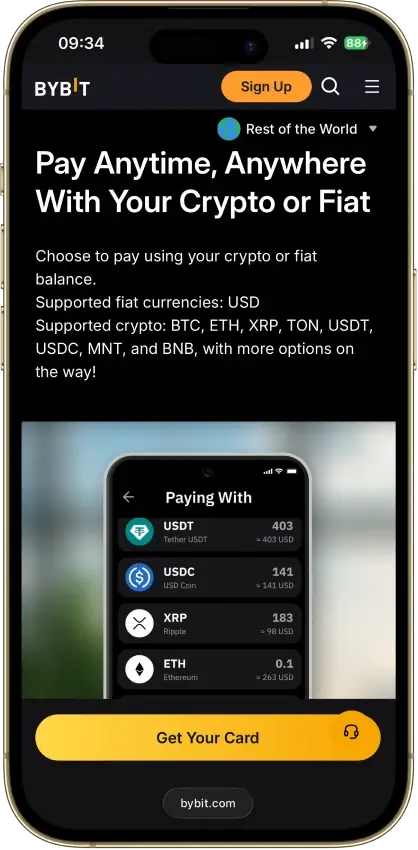

Best for Stablecoin Users

If you mainly hold stablecoins, the best crypto card is often the one that gives you the cleanest path from balance to payment. Stablecoin users usually care less about speculation and more about simple settlement, predictable value, and fewer surprises when funds are used at checkout.

In this case, a card with easy funding, clear conversion rules, and low friction is often more valuable than one built around flashy token perks. A smooth spending experience can matter more than a marginally better reward rate.

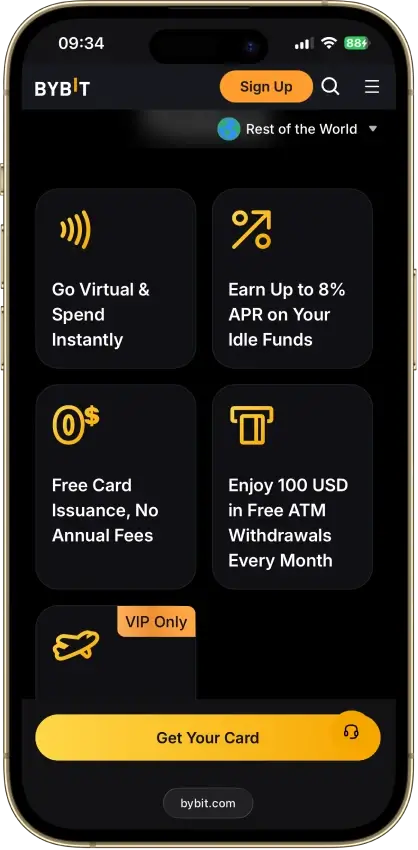

Best for Travelers

Travelers should pay more attention to foreign transaction costs, ATM rules, regional acceptance, and wallet compatibility than to the headline cashback figure. A crypto card that works well domestically can become expensive very quickly once ATM allowances are used up or foreign-exchange costs begin to stack.

For this type of user, a strong card is one that travels well across merchants and regions, offers good virtual access, and does not punish normal international usage with weak limits or layered fees.

Best for Beginners

Beginners should usually prioritize simplicity over optimization. The best crypto card for a new user is one with a straightforward setup, clear in-app controls, easy-to-understand funding, and a reward model that does not depend on too many moving parts.

A card that is slightly less aggressive on rewards can still be the better choice if it removes confusion around tiers, conversion, and eligibility. In most cases, usability is what determines whether a beginner keeps using the card at all.

Best for Instant Virtual Access

If you want to start using a card quickly, virtual access matters. The best virtual crypto card is usually the one that can be issued fast, added to Apple Pay or Google Pay without friction, and managed entirely through the app.

This is especially useful for users who make frequent online purchases, want immediate access before a physical card arrives, or prefer to keep their spending setup fully digital.

Security and App Controls to Look For

A good crypto card should make day-to-day security feel easy, not hidden. Freeze and unfreeze controls, real-time spending alerts, PIN management, and visible transaction tracking are basic features that make a card more usable and safer at the same time.

It is also worth paying attention to account-level protection. Strong two-factor authentication, responsive support, and reliable app controls can matter just as much as rewards when something goes wrong. For many users, the difference between a card they keep and a card they abandon comes down to whether the product feels dependable after the first few weeks of use.