On Jan. 10, 2024, the U.S. Securities and Exchange Commission (SEC) approved the trading of 11 spot Bitcoin ETFs, an event many saw as the opening of floodgates for institutional and retail capital into the Bitcoin market. This approval came after years of anticipation and multiple rejections, highlighting the regulatory hurdles that Bitcoin and the broader crypto market have faced in their journey toward mainstream acceptance.

In their first week of trading, these ETFs saw a surge in investor interest, as evidenced by the substantial trading volumes and inflows. CryptoSlate reported that on the first day of trading alone, spot Bitcoin ETFs saw trading volumes exceeding $4 billion, indicating a strong market appetite for these new financial products. This debut was significant in terms of the sheer volume of trade and in setting a precedent for the type of regulated Bitcoin exposure that investors can now access.

Introducing these ETFs is not merely a new investment vehicle; it marks a paradigm shift in how Bitcoin is perceived in the financial world. For the first time, investors have the opportunity to gain exposure to Bitcoin through a regulated framework, providing a more accessible means to invest in this digital asset. The implications of this shift are far-reaching, extending beyond the crypto market to impact traditional financial markets as well.

In this report, CryptoSlate will dive deep into the first five days of the ETFs’ trading, analyzing their impact on the market. The report will cover the trading performance of individual ETFs, focusing on significant players like BlackRock and Grayscale and the broader market implications of these new investment tools.

This report aims to provide a comprehensive understanding of how the launch of spot Bitcoin ETFs is reshaping the investment landscape for Bitcoin and what it means for the future of digital asset trading.

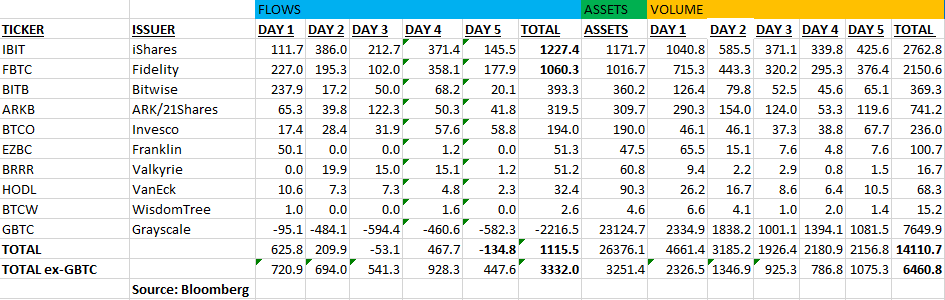

The first week of ETF trading

The launch of spot Bitcoin ETFs heralded a new era of investment opportunities in the U.S., and their initial trading week was a display of significant market movement and investor interest. Analyzing the data from Bloomberg, it’s clear that the performance of individual ETFs varied, with certain funds attracting more inflows and others facing outflows, indicative of investor sentiment and strategic positioning within the market.

iShares’ Bitcoin Trust (IBIT) ETF, representing BlackRock’s foray into the spot Bitcoin ETF arena, showed a promising start with a cumulative inflow of $1.22 billion by the end of the first five trading days. IBIT’s performance is significant not only because of the volume but also due to BlackRock’s heavyweight status in the investment world, suggesting a credible institutional endorsement of Bitcoin as an investable asset. The ETF’s assets under management swelled rapidly, signaling strong market confidence.

Fidelity’s Bitcoin ETF (FBTC) also experienced substantial inflows, totaling $1.06 billion. Bitwise (BITB) trailed with an inflow of $393.3 million, while other ETFs like ARK/21Shares (ARKB) and Invesco (BTCO) attracted $319.5 million and $194.0 million, respectively.

On the other side of the spectrum, Grayscale’s Bitcoin Trust (GBTC) faced significant outflows totaling $2215.6 million. This shift could be attributed to GBTC’s transition from a trust to an ETF, coupled with the market’s reaction to fee structures and the appeal of newly available ETFs.

During the first week of trading, ETFs excluding GBTC saw their largest inflow on Day 1, with $720.9 million entering these funds. This contrasts with the total for all ETFs, where Day 1 also led with $625.8 million in inflows, a lower figure due to GBTC’s substantial outflows.

The highest trading volume for ETFs, not including GBTC, was on Day 4, reaching $1078.6 million. When we include GBTC, the peak trading volume hit $2165.8 million on Day 5. This suggests that despite GBTC’s outflows, investors were actively trading it, possibly to take advantage of price differences or to adjust their holdings in response to market moves.

The significant inflows into new ETFs reflect a strong investor demand for regulated Bitcoin products. The data shows that investors are choosing new ETFs over GBTC, likely due to the potential advantages of the new offerings, like lower fees and better liquidity.

The cumulative volume traded across all ETFs in the first five days of trading, excluding GBTC, was $6.46 billion. This trading volume shows the market’s readiness to embrace regulated Bitcoin products and may foreshadow the trajectory of its adoption in traditional investment portfolios.

BlackRock’s entry, in particular, is poised to be a bellwether for institutional engagement with cryptocurrency, as it brings financial clout and a level of mainstream legitimacy to the Bitcoin investment thesis. The success of these ETFs in their initial week, as shown by the strong inflows and trading volumes, signals a potential shift in the broader financial ecosystem’s approach to digital assets.

Table showing the flows and trading volume for spot Bitcoin ETFs by days of trading, in millions (Source: Eric Balchunas)

The problem with redemptions and contract creation

Contract creation and redemptions are central to how ETFs interface with the underlying asset markets and are crucial in creating liquidity and price stability.

Contract creation in a spot Bitcoin ETF involves the issuer creating new shares in exchange for Bitcoin. This process typically begins with an authorized participant (AP) – often a large financial institution – who buys the underlying asset, Bitcoin, in this case, and delivers it to the fund. In return, the ETF issuer provides the AP with ETF shares equivalent to the value of Bitcoin delivered, which can then be sold on the secondary market.

Conversely, redemptions involve the AP returning ETF shares to the issuer and receiving the underlying Bitcoin in exchange. This mechanism allows the ETF to reflect the net asset value (NAV) of the underlying Bitcoins more accurately, as shares are created and redeemed according to demand, theoretically ensuring that the ETF does not trade at a significant premium or discount to its NAV.

These mechanisms have a significant role in the context of liquidity and price stability. The creation of ETF shares in response to demand helps to maintain liquidity in the market, as it provides a way for the ETF to adjust its supply of shares without directly impacting the Bitcoin market. Redemptions serve a similar function in reverse, providing a method to reduce the number of ETF shares when demand falls.

The impact of these processes on the Bitcoin market is nuanced. On the one hand, they can provide stability by smoothing out market imbalances through the APs’ activities. On the other hand, significant redemptions could exert downward pressure on Bitcoin prices if APs sell large amounts of Bitcoin in the open market. Additionally, the time lag between redemption requests and the actual sale of Bitcoin could contribute to price discrepancies, potentially increasing market volatility.

This delay arises from various operational processes that include order placement, execution, settlement, and the transfer of assets between the AP and the ETF issuer. During periods of high volatility in the Bitcoin market, this time lag can lead to discrepancies between the ETF’s net asset value (NAV) and the prevailing market price of Bitcoin.

For instance, if Bitcoin’s price were to plummet rapidly within a short time frame, the redemption process might result in the sale of Bitcoin at a price lower than what was factored at the time of the redemption request. Conversely, during a sharp increase in Bitcoin’s price, the creation process might see APs acquiring Bitcoin at higher prices than anticipated.

The price inefficiencies created by ETF’s inability to mirror Bitcoin’s price accurately could result in the ETF trading at a premium or discount relative to its NAV. CryptoSlate’s deep dive into the ETF mechanisms provides a deeper understanding of the intricacies involved and how they may influence the ETFs’ alignment with Bitcoin’s price.

The impact on Bitcoin

One of the most evident impacts spot ETFs have had on Bitcoin has been the increase in liquidity. The first week of trading saw spot Bitcoin ETFs generate a trading volume in the billions, with BlackRock’s ETF alone attracting over $1.2 billion in assets. This influx of capital has the potential to reduce volatility by dampening sharp price movements that are often characteristic of less liquid markets.

The ETFs also represent a shift in Bitcoin’ investment landscape, lowering the barrier for entry for a wide range of investors. By providing a regulated investment path, spot Bitcoin ETFs may contribute to a perception of Bitcoin as a mature and established asset class, potentially leading to more significant inflows of capital from tradfi.

However, there are many downsides to consider.

The creation and redemption mechanisms of ETFs, with their inherent time lags, can lead to situations where the ETFs do not perfectly track the price of Bitcoin, potentially leading to inefficiencies in the price discovery process.

ETFs aggregate the holdings of Bitcoin into the hands of a few institutional players, which could be seen as antithetical to the decentralized principles that underpin cryptocurrency. This concentration of ownership may also lead to greater market manipulation risks, where large flows into or out of the ETF could disproportionately influence Bitcoin’s price.

Additionally, the reliance on traditional financial institutions as authorized participants in the ETF mechanism could introduce systemic risks to Bitcoin. These institutions become gatekeepers for the flow of funds into and out of Bitcoin, and their financial stability or operational integrity could have a significant impact on the market.

For instance, if a major AP were to face liquidity issues or regulatory challenges, it could impact the efficiency of the creation and redemption process, potentially destabilizing the ETF’s tracking of Bitcoin’s price.

There’s also a concern that spot Bitcoin ETFs could siphon liquidity away from the actual Bitcoin market. If investors opt for the convenience of ETFs over purchasing Bitcoin directly, the underlying asset’s market could become less liquid, making it more susceptible to volatility from large trades.

Conclusion

The launch of spot Bitcoin ETFs has been marked by a remarkable influx of capital. In the first five days alone, inflows into these ETFs, excluding Grayscale’s GBTC, totaled $3.33 billion, while volumes reached $6.46 billion. The iShares (IBIT) ETF led this surge with $1.22 billion in inflows, followed by Fidelity (FBTC) and Bitwise (BITB), with inflows of $1.06 billion and $393.3 million, respectively.

Despite the size of these inflows, which made spot Bitcoin ETFs the second-largest commodity ETFs in the world, it’s important to understand that they are unlikely to be sustained indefinitely. Flows into these ETFs and their trading volumes are anticipated to fluctuate, oscillating with market momentum and investor sentiment.

The initial enthusiasm may taper as the market normalizes and investors rebalance their portfolios. The demand for Bitcoin ETFs could also grow significantly over time if they follow the trajectories of other commodity-based ETFs.

Moreover, the significant capital commitments made during the first week do not inherently render these ETFs less volatile or more predictable. The nature of Bitcoin means that these ETFs are subject to the same underlying volatility as BTC. The substantial early inflows should not be misconstrued as a signal of long-term stability.

While the initial reception of spot Bitcoin ETFs has been incredibly strong, it is essential to approach these figures with an analytical perspective, recognizing that they only represent a snapshot in time of a very, very volatile market. The true test will be the resilience and consistency of inflows and volumes over an extended period beyond the initial excitement.