- Uniswap does not hold user funds, which removes the usual exchange custody risk.

- Traders can access millions of assets across 17+ supported chains.

- Uniswap combines UniswapX, limit orders, crosschain swaps, and liquidity tools in one product ecosystem.

Start swapping across chains

Uniswap Labs Overview

Additional details

Uniswap Labs Screenshots

Uniswap Labs Pros and Cons

Pros

- Non-custodial design means Uniswap Labs does not hold user wallet balances.

- Broad coverage across 17+ supported networks gives users deep onchain market access.

- 0% interface fee at capture time makes costs easier to understand than many retail buy flows.

- Product depth goes beyond basic swaps, with limit orders, crosschain routing, LP tools, wallet access, and API support.

- Strong fit for users who want direct DeFi exposure without opening a centralized exchange account.

Cons

- Not ideal for beginners who want simple fiat in and fiat out with predictable support.

- No exchange-style custody protections or recovery path if you lose wallet access or sign a bad transaction.

- Total trading cost still depends on pool fees, gas, route selection, and third-party provider fees.

- Some buy, sell, and compliance steps depend on outside payment partners rather than a fully native Uniswap flow.

Is Uniswap Worth It?

Yes, if you want a wallet-based exchange experience rather than a centralized account with onchain features added on top. Uniswap is worth considering if you want broad network coverage and deep onchain liquidity. It also offers useful trading tools such as limit orders, crosschain swaps, and liquidity provision without requiring a custodial handoff of assets.

The trade-offs are clear. You should skip Uniswap if you want simple bank-style onboarding, predictable human support, easy fiat withdrawals, or a platform that can recover access when you make a wallet mistake. Costs can also vary more than they first appear. Pool fees, gas, routing, and third-party payment partners all affect the final result.

Who Is Uniswap Best For

Uniswap is best for intermediate and advanced traders who are comfortable managing their own wallet, handling gas fees, and moving assets across chains. It suits active onchain traders, DeFi users, and liquidity providers who want direct access to markets across supported networks. It is especially appealing to people who already keep funds onchain and care more about route quality than about traditional exchange features.

It also suits builders and wallet-native users who may want the API, portfolio tools, and broader Uniswap product ecosystem. It is a weak fit for beginners, very low-risk traders, and people who mainly need fiat deposits, fiat withdrawals, or step-by-step support. Those needs are usually better served by a beginner-friendly crypto exchange. It is also less suitable for people who want fixed centralized pricing models, custody protections, or an exchange that handles the operational side for them.

Uniswap Fees and Pricing

| Cost area | How pricing works | What changes it |

|---|---|---|

| Swap fee | Set by the pool or route, not by a platform-wide maker/taker schedule | Protocol version, pair, pool depth, and route |

| Network cost | Paid onchain, or reduced on some UniswapX routes | Chain congestion, approvals, wrapping, and route type |

| Fiat buy or sell | Quoted by the payment partner at checkout | Region, provider, payment method, and KYC |

As of March 18, 2026, Uniswap Labs charges 0% interface fees on its web app and wallet. That does not make trading free. Users can still pay liquidity pool fees, network gas, bridge or relayer costs on some routes, and provider fees when entering or exiting through fiat.

Uniswap does not use a centralized maker-taker schedule. For normal swaps, pricing depends on the pool and route selected. On Uniswap v3, standard fee tiers are 0.01%, 0.05%, 0.30%, and 1.00%. On Uniswap v2, pools use a 0.30% total fee tier. On Uniswap v4, fee tiers are flexible rather than fixed. In practice, the cheapest routes are usually deep stablecoin or blue-chip pools. Thinner or more volatile pairs can cost materially more.

There is also no volume-based base tier or top tier in the way a centralized exchange would structure pricing. Costs do not improve because you traded more last month. They change based on the pool fee tier, the route selected, network gas, and whether the trade uses UniswapX. On supported UniswapX routes, fillers cover most network costs for the swap itself. That reduces direct gas friction, although approvals and wrapping can still cost gas. Failed swaps also do not charge the swapper for the swap itself.

Fiat pricing is less standardized. Uniswap does not publish a flat spread schedule, and any effective Uniswap spread in a buy or sell flow depends on the payment partner, region, and payment method. When people buy or sell through the Uniswap web app, they are routed to payment partners such as Robinhood, Coinbase, MoonPay, Transak, Banxa, Stripe, and others depending on region. Those partners set the quote, payment method availability, spread, fees, and settlement timing.

For self-custody transfers, there is no classic exchange withdrawal fee table because Uniswap is not holding user balances in a custodial account. There is no standard Uniswap withdrawal fee in the way a centralized exchange would publish one. The cost of moving funds is mainly the network fee on the chain used. Bridge or relayer costs can be layered in on some routes. People should also watch for fee-on-transfer tokens, because those token-level charges are separate from any Uniswap Labs fee.

There is no staking commission that materially changes the cost picture here. Uniswap’s pricing profile is driven by swaps, routing, and liquidity provision rather than by a centralized Earn product.

The best ways to lower costs on Uniswap are practical. Use cheaper supported networks when liquidity is still strong enough for the pair you want. Prefer lower-fee pools when execution quality remains solid. Use UniswapX where available, since it can reduce direct gas costs and failed-swap friction compared with a standard onchain swap.

Uniswap does not have a public VIP ladder, a maker-taker discount schedule, or a native-token fee discount. Costs change by pool fee tier, route, network choice, and provider pricing, not by account status or trading volume.

Deposits, Withdrawals, KYC and U.S. Availability

Uniswap does not publish one clean global schedule for deposits, withdrawals, and limits in the way a centralized exchange does. The core product is non-custodial. Funding usually happens through your own wallet, while fiat buy and sell flows run through payment partners that set their own supported countries, payment methods, limits, fees, and review times.

| Flow | How it works | Main caveat |

|---|---|---|

| Wallet funding | Connect a self-custody wallet and trade directly from it | There is no native fiat balance inside Uniswap |

| Fiat buy | Use a payment partner inside the web app | Fees, methods, limits, and KYC vary by partner |

| Fiat sell | Use a third-party off-ramp inside the web app | Timing and bank settlement depend on the off-ramp partner |

| Crosschain movement | Use supported routes to bridge and swap in one flow | Route cost and timing vary by chain and relayer |

Geo Access and Entity Mapping

Uniswap works in two layers. The first is the wallet-based web app itself. The second is the partner layer for fiat buy and sell, which varies more by country, payment partner, and compliance rules.

| Region | Access level | Main caveat |

|---|---|---|

| U.S. | Core web app available | Some token access and fiat flows depend on the payment partner and compliance rules |

| EU / EEA | Core web app plus selected buy and sell flows | Fiat rails vary by country and payment partner |

| UK | Core web app plus selected buy flows | Payment methods and support vary by partner |

| Selected international markets | Core web app plus some local payment options | Coverage is partner-driven rather than platform-wide |

| Restricted or sanctioned jurisdictions | Not lawfully available under the Terms | Sanctions and jurisdiction limits apply |

Uniswap does not present the kind of state-by-state entity map that many U.S. centralized exchanges use. The core web app is broadly available. Fiat rails, some token availability, and compliance outcomes can still change by payment partner, location, and asset.

Registration and Onboarding

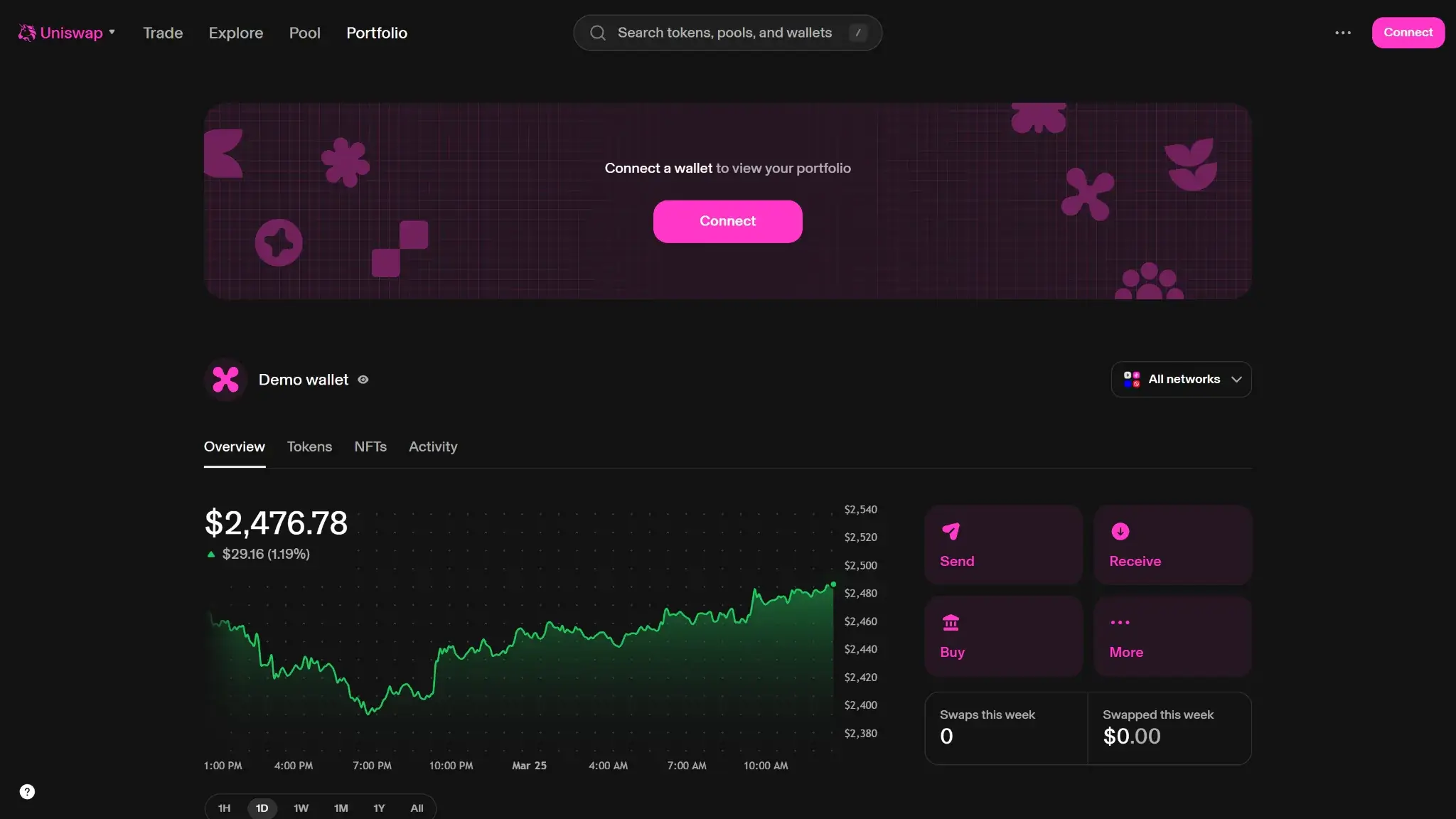

For normal wallet-based use, onboarding is much lighter than it is on a centralized exchange. Users connect a compatible wallet and sign from that wallet. There is no standard exchange account with a native cash balance that needs to be opened first.

KYC usually appears when a user buys or sells crypto for fiat through a third-party provider, not when making a normal onchain swap from a self-custody wallet. Depending on the payment partner and transaction size, the process can require an email address and phone number. It may also require government-issued ID, a selfie or liveness check, and sometimes proof of address. Review timing depends on the provider rather than on a native Uniswap account system.

Security is also user-controlled rather than exchange-controlled. In the Uniswap Wallet, biometric protection and device-level security settings matter. In a third-party wallet, the security defaults depend on that wallet provider.

Fiat Rails by Region

Uniswap does not run a native ACH, wire, or PayPal network of its own. Fiat rails are partner-based. In the U.S., cards, Apple Pay, and Venmo are the most visible consumer methods in supported flows. In parts of Europe, SEPA and SEPA Instant are the most practical options where supported. In selected international markets, local rails such as PIX may appear. Availability still depends on the payment partner, country, asset, and compliance result.

For a typical U.S. user, the lowest-friction funding method is often not buying inside the web app. It is usually cheaper to fund a self-custody wallet elsewhere and then swap onchain through Uniswap. Readers who mainly want direct bank rails may be better served by a U.S.-focused crypto exchange.

Withdrawal Networks and Fees

| Route type | Cost pattern | Main caveat |

|---|---|---|

| Ethereum mainnet transfers | Network fee only | Gas can become expensive during congestion |

| Cheaper supported L2s | Lower network fee | Liquidity can be thinner on some pairs |

| Wrapped BTC or other non-native exposures | Route-dependent | This is not a direct BTC mainnet withdrawal model |

| Crosschain swaps | Bridge or relayer cost plus network cost | Timing and fees vary by route |

Because Uniswap is non-custodial, there is no classic exchange withdrawal queue or withdrawal fee table. Users lower transfer costs by choosing cheaper supported networks when liquidity is good enough, avoiding unnecessary bridge hops, and using the most efficient stablecoin route available on the destination chain.

Verification Levels and Withdrawal Limits

Uniswap does not publish a unified in-house verification ladder or fixed platform-wide deposit and withdrawal limits. For normal wallet-based swaps, there is no platform-level KYC. For partner fiat buys and sells, identity checks, limits, and review times are set by the provider and can change by country, payment method, asset, and transaction size.

The more practical operational risk is that a provider review, bank check, or identity check can delay a fiat buy or sell even when the core Uniswap swap interface itself remains available. There is also no standard whitelist or travel-rule table presented as a native exchange setting for all users in the way many custodial exchanges do.

Is Uniswap Safe? Security, Custody and Proof of Reserves

As of March 18, 2026, Uniswap’s safety profile is strongest in custody design rather than in the balance-sheet transparency model used by centralized exchanges. The platform is non-custodial, so users keep control of their own assets instead of leaving balances with an exchange operator. That meaningfully reduces exchange insolvency risk. It does not remove wallet compromise, malicious approvals, bridge risk, or bad-token risk if someone trades carelessly.

Controls

Uniswap does not use a standard centralized account-security stack on its web app because there is no native custodial exchange account at the center of the product. There is no platform-wide 2FA login, passkey system, withdrawal allowlist, or vault-style delayed withdrawal flow in the usual CEX sense. Users connect a wallet and approve transactions from that wallet.

The protections that do exist are wallet- and device-focused. In the Uniswap Wallet, users can enable Face ID, Touch ID, or Android biometrics for app access and transaction approval. Those controls are useful, but they are optional and they protect the device rather than the recovery phrase itself.

Uniswap’s anti-scam protections are stronger than many users expect from a DEX. The web app uses token warnings and labels to flag malicious tokens, impersonator tokens, and tokens with extreme buy or sell fee behavior. Uniswap Labs also maintains an unsupported-token list. It can restrict certain tokens or addresses in its own interface for legal, fraud, sanctions, intellectual property, or user-safety reasons. On the support side, Uniswap only recognizes official support channels and warns people away from Telegram and WhatsApp impersonators.

Custody and Insurance

Uniswap’s custody model is one of its biggest strengths and one of its clearest trade-offs. Uniswap Labs describes its products as non-custodial, which means it does not have custody, possession, or control of user digital assets. Users hold their own keys, control their own wallets, and remain responsible for protecting recovery phrases and transaction approvals.

That structure removes the usual exchange-balance custody risk, but it also means there is no operator recovery path if a user loses access, signs a malicious approval, or sends funds to the wrong destination. Transactions are generally irreversible once confirmed onchain, and Uniswap cannot reverse or recover funds on a user’s behalf.

Uniswap does not present a crypto-balance insurance program, crime insurance policy, or specie-style custody coverage for self-custodied user assets. If a bank partner or fiat provider is involved in a buy or sell flow, any protection that exists there applies to that partner relationship. It does not apply to crypto held in a wallet through Uniswap. Bank-partner insurance does not mean crypto balances are insured.

Proof of Reserves or Audits

There is no exchange-wide proof of reserves in the usual centralized-exchange sense because Uniswap Labs is not holding pooled customer balances that need to be attested. There is no reserve dashboard, reserve ratio, or recurring solvency attestation for users to verify.

The stronger trust signals are code-review and audit based. Uniswap Wallet and the Uniswap Extension have been independently reviewed by Trail of Bits. At the protocol level, Uniswap v4 launched after nine independent audits, a $2.35 million security competition, and a $15.5 million bug bounty. Uniswap has also highlighted that v2 and v3 processed very large cumulative volume without a protocol hack.

This is useful, but it is not the same thing as proof of reserves. Audits can reduce contract risk. They do not remove user error, malicious tokens, compromised wallets, bridge failures, or future smart-contract vulnerabilities.

Incidents and Remediation

Uniswap’s published security history is more about prevention and risk reduction than about recovering from a classic exchange custody event. Because the product is non-custodial, the more relevant risks are malicious tokens, compromised wallets, unsafe approvals, and smart-contract exposure rather than reserve shortfalls or frozen withdrawals.

One of the more important remediation steps was the expansion of token warnings and labels across the Uniswap web app and wallet. Those warnings make it easier to spot impersonator tokens, malicious tokens, and tokens with extreme sell-fee behavior before a swap is submitted. Uniswap’s unsupported-token and address-blocking policy also gives the company a way to restrict access through its own interface where legal, fraud, sanctions, or user-safety concerns apply.

At the protocol layer, the biggest recent safety signal was the launch of Uniswap v4 after unusually heavy review rather than after a public exploit. That does not make the product risk-free, but it does show a strong emphasis on pre-launch security work.

How to Verify PoR Yourself

There is no proof-of-reserves report to verify because Uniswap is non-custodial. The more useful safety checks are practical: confirm that you are on an official Uniswap domain, verify the token contract before swapping, pay attention to token warnings, and remember that a security audit is not the same as asset insurance.

Status Page and Incident History

Uniswap does not present a proof-of-reserves page or exchange-solvency monitor because those are not relevant to its non-custodial model. The more useful security record is the product’s audit history, token-risk controls, and the absence of a disclosed exchange-wide custodial shortfall in the official materials reviewed for this update.

| Month Year | Event | Impact | Resolution |

|---|---|---|---|

| December 2024 | Expanded token warnings and labels rolled out across the Uniswap web app and wallet | Users gained better visibility into impersonator tokens, malicious tokens, and extreme sell-fee risks | Additional warnings and labels were added to help users screen token risk before swapping |

| January 2025 | Uniswap v4 launched after nine audits, a security competition, and an active $15.5M bug bounty | No critical issue from those pre-launch review programs was presented as a blocker to launch | v4 launched with unusually heavy review and the bug bounty remained active for ongoing research |

| March 2026 | No disclosed exchange-wide custodial breach or reserve shortfall appears in the official materials reviewed for this update | Users still face wallet, token, bridge, and contract risk, but not the usual custodial-balance solvency risk | The main protections remain self-custody, audits, warnings, and user verification rather than reserve attestations |

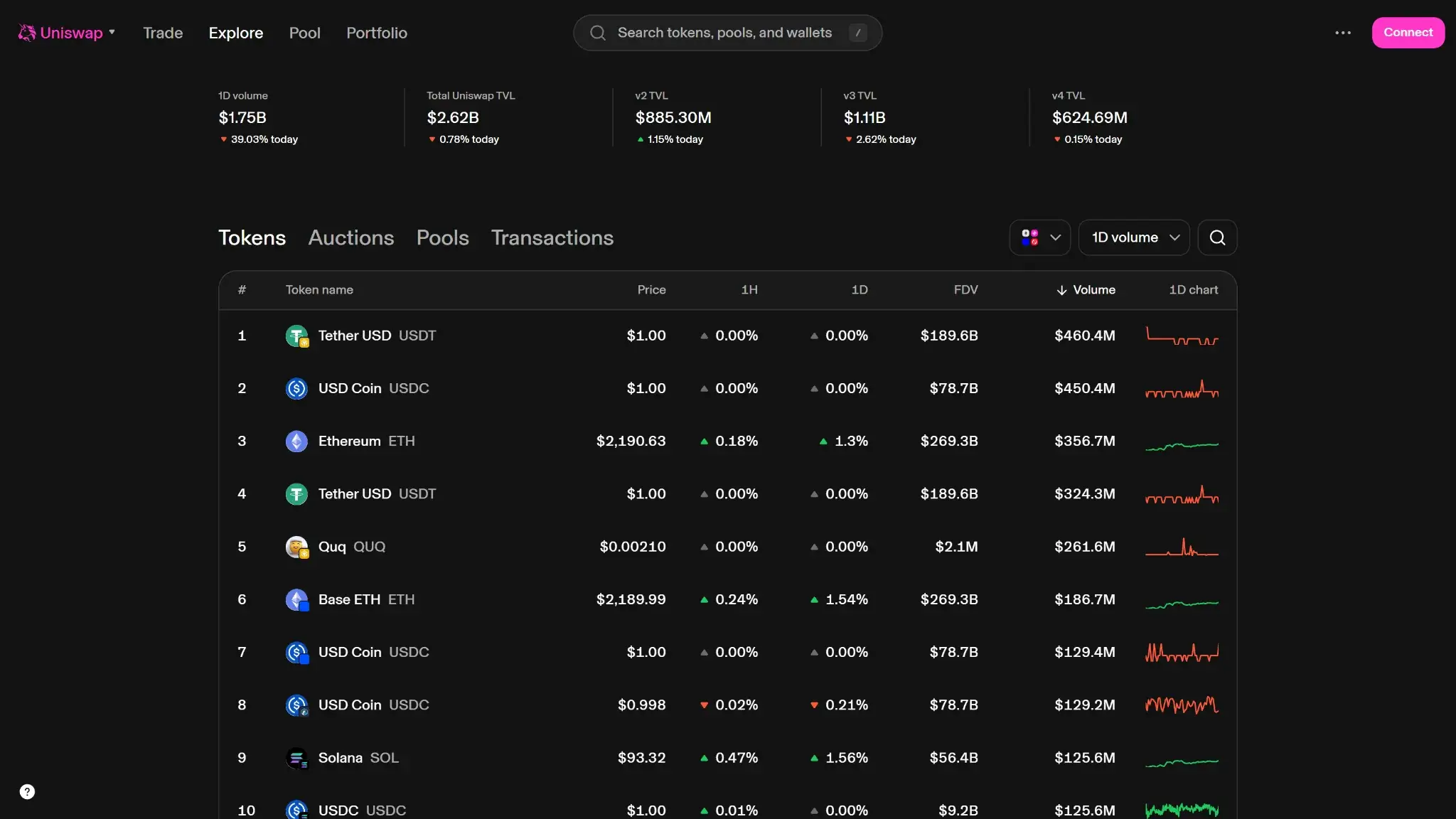

Supported Assets and Markets

Uniswap’s market access is a major strength. The web app now supports more than 17 chains. Because trading is routed through permissionless onchain liquidity, the practical asset universe is far larger than the fixed coin menus used by most centralized exchanges.

That breadth still needs context. Uniswap is strongest as an onchain spot venue, not as a full-service exchange with every market type under one roof. The core stack includes swaps, liquidity provision, crosschain transfers, limit orders, and token-auction tools. It does not include native margin, perpetuals, or options, so traders who want leverage are better served by crypto exchanges with futures.

There is no fixed Uniswap coin list in the way a centralized exchange publishes one. Market access depends on supported chains, token contracts, and what Uniswap Labs chooses to surface or restrict in its own products.

Stablecoin coverage is strongest where most traders would expect it to be. USDC is the most consistent anchor asset across supported buy, sell, swap, and bridging routes. USDT and DAI also matter, especially on Ethereum and supported bridging paths. The direct fiat buy flow is much narrower than the full swap universe. On Ethereum, supported buy tokens include ETH, USDC, DAI, USDT, WBTC, and WETH. On several other supported networks, the list narrows to ETH, USDC, or the chain’s main asset.

This is not a fiat-pair exchange in the usual sense. There is no deep centralized USD, EUR, or GBP order book to compare against a rival venue. Fiat access is handled through outside services, and local currency support changes by region. Once funds arrive in a wallet, the market is primarily token-to-token trading across supported chains.

For U.S. users, the onchain catalog is broadly similar to what international traders see. The bigger differences show up in payment partners, off-ramp availability, and compliance-driven restrictions around certain tokens or services. The base web app itself is far less geographically split than a typical centralized exchange.

The UNI token does not function like a classic exchange token that unlocks fee discounts or VIP tiers. Its role is governance rather than retail pricing. Holding UNI does not lower swap costs in the way BNB or similar tokens can on centralized platforms.

There are still clear gaps. Direct fiat-supported token coverage is much narrower than the full swap catalog. Some networks have more limited product support than others. Solana currently appears in the Uniswap Web App rather than as a fully uniform experience across every Uniswap product. Traders who want direct BTC mainnet trading, TRON-based stablecoin rails, or leveraged markets will notice those gaps quickly.

Listings and Delistings Policy

Uniswap does not use a classic centralized listings committee for protocol-level token access. The underlying protocol is permissionless, so the more relevant policy question is what Uniswap Labs chooses to support, surface, or restrict inside its own products.

New network and product support is typically rolled out through official product announcements and help-center updates. A good recent example is Solana support, which was added to the Uniswap Web App in October 2025 to expand market access beyond EVM chains inside the web interface.

Delistings and restrictions are handled differently from a centralized exchange. Uniswap Labs maintains an Unsupported Token List for tokens it removes from its own products due to legal and regulatory requirements, fraud allegations, intellectual-property claims, or risks to user safety. That means a token can remain tradeable through the permissionless protocol while still being hidden or restricted in Uniswap Labs’ official interfaces.

App, UX and Customer Support

As of March 18, 2026, Uniswap’s product experience is well organized for people who already understand wallet-based trading. The current interface separates Trade, Explore, Pool, and Portfolio clearly. The mobile wallet extends that experience with push notifications, biometric protection, and onchain search. Localization is better than many DeFi products, with language support across the web app, wallet, and extension. The support model is still closer to a documentation-first crypto product than to a bank-style customer service desk.

UI and Navigation

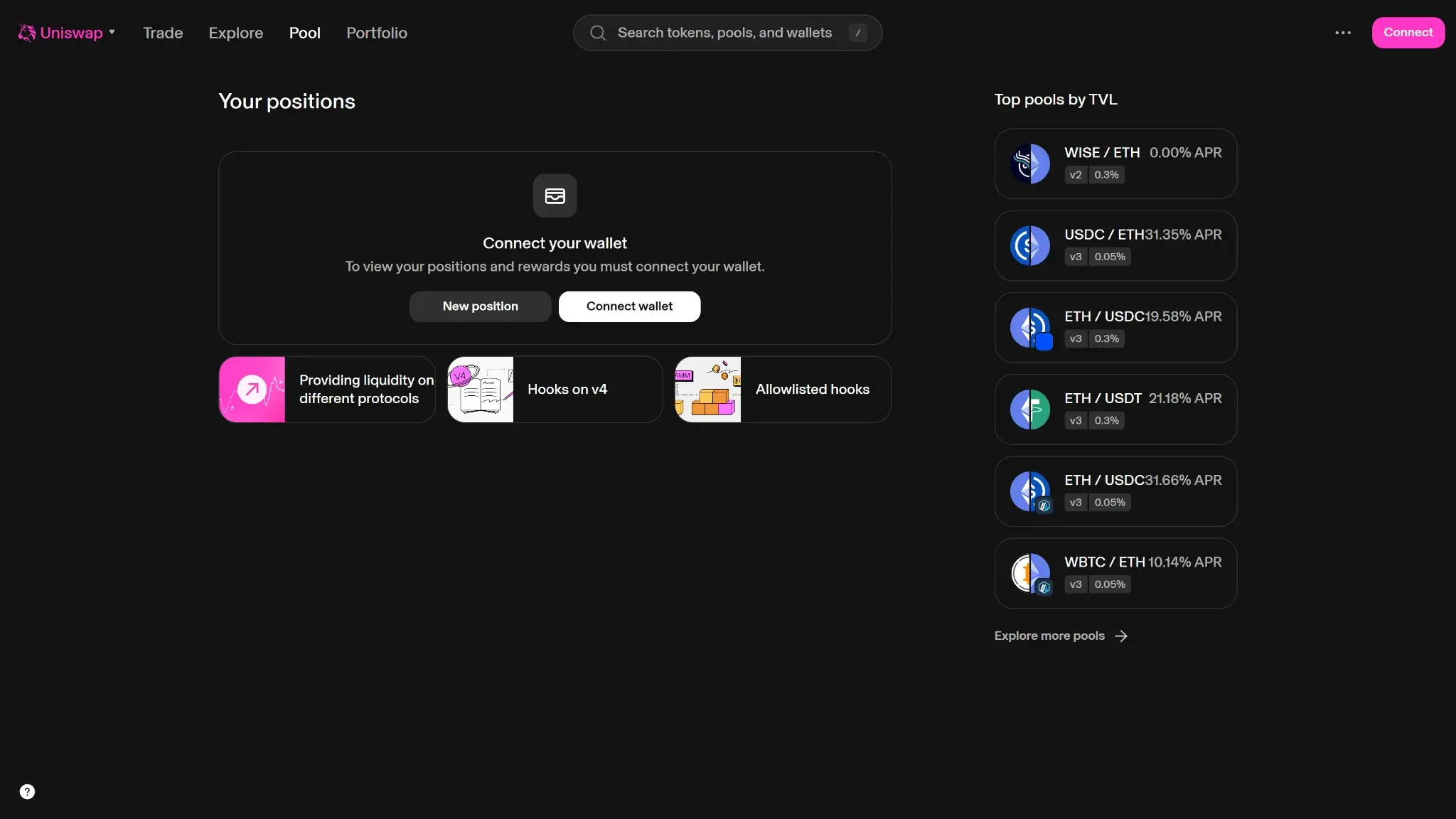

Uniswap’s information architecture is one of the stronger parts of the product. On desktop, the top-level navigation makes the platform easier to understand than many DEX interfaces that bury everything inside a single swap card. Trade handles swaps, limit orders, buy, and sell. Explore is the discovery layer for tokens, pools, and transaction data. Pool is reserved for liquidity actions across protocol versions. Portfolio gives users one place to review balances, positions, and activity.

That structure works well because it separates intent cleanly. Someone who wants to swap can do that immediately without digging through analytics. A liquidity provider can go straight to pool actions without wading through retail buy flows. Advanced features are present, but they are not especially hard to find once the basic navigation is understood.

The trade-off is that Uniswap still assumes a working level of crypto literacy. The interface is smooth when someone already understands wallets, approvals, slippage, bridging, token contracts, and gas. It becomes less intuitive when someone expects the platform to abstract those decisions away. In practice, the friction points are usually not visual design problems. They come from network context, provider handoffs, and the fact that token and chain risk still sit with the user.

Localization is a meaningful plus. Uniswap’s web app, wallet, and extension all support language translation. The wallet and extension currently support English, Chinese, French, Japanese, Portuguese, Spanish, and Vietnamese. The web app language can also be changed from the settings menu. That said, the product still reads like an English-first DeFi platform, especially once users move into more technical flows.

Accessibility signals are mixed. The mobile wallet supports standard device-level controls such as Face ID, Touch ID, and Android biometrics, but the App Store listing does not currently disclose specific accessibility features. That does not make the app inaccessible, but it does mean Uniswap is not presenting accessibility as a major trust or product pillar.

Mobile App

Uniswap offers a live mobile app on both iOS and Android under the name Uniswap: Crypto & NFT Wallet, putting it firmly in the same day-to-day use category as other hot crypto wallets. On iOS, the app currently holds a 4.8 rating from about 19,000 ratings. On Google Play, it shows a 4.6 rating, roughly 23,000 reviews, and more than 1 million downloads. These are strong adoption signals for a wallet-based product.

The update cadence looks active. The iOS version history shows multiple releases between January and March 2026, including versions 1.64.2, 1.65.1, 1.67, 1.67.1, and 1.68.0. Most of those releases are framed as bug fixes and performance improvements rather than big front-end redesigns. That usually points to steady maintenance rather than neglected mobile support.

Feature parity with the web app is good, but it is not complete. The wallet handles the core mobile use case well: portfolio tracking, swaps, token discovery, buy flows, NFT viewing, and wallet-based security. The broader Uniswap product family still stretches across web, wallet, and extension. Some people will see the experience as ecosystem-wide rather than fully unified inside one app.

Push notifications are a practical strength. The wallet can notify users when transactions complete, even if those transactions were initiated on another app or device. That is genuinely useful in a multi-device crypto workflow.

Security controls are also solid by mobile-wallet standards. Users can require Face ID, Touch ID, or Android biometrics for opening the app and for submitting transactions. Recovery phrase backup options are also built into the wallet. The main limitation is that these controls secure the device and session, not the recovery phrase itself.

Mobile reliability still depends heavily on the surrounding chain and provider environment. If a swap route is congested, if a provider rejects a payment, or if pricing data is delayed, the mobile experience can still degrade even when the app itself is functioning normally.

Reliability and Status Page

Uniswap does not present a prominent public status page in the way many centralized exchanges do. Instead, operational issues are mostly surfaced through help-center documentation and troubleshooting guides. That is workable for experienced users, but it is less transparent than a dedicated live status dashboard with incident timestamps.

Not every display issue stops trading. When Uniswap’s third-party subgraphs are down, price charts, liquidity charts, and some token-page data can disappear, but swapping and liquidity management can still continue. This separates cosmetic or analytics issues from execution issues.

Routine reliability issues usually fall into three buckets. First, there are data and chart problems, especially when subgraphs go down. Second, there are stuck or pending transaction states, which can require people to clear app data, refresh the app, or cancel a pending transaction from the wallet. Third, there are provider-side fiat delays, where a crypto purchase or sale can take longer than expected because of bank checks, provider review, or payment verification.

| Month Year | Event | Impact | Resolution |

|---|---|---|---|

| December 2025 | Subgraph downtime guidance published for web, wallet, and extension | Token prices, charts, and liquidity visuals can disappear even while swaps still work | Users can still swap, manage liquidity, and rely on quoted swap output while data services recover |

| January 2026 | App-data clearing tools documented for stuck transactions and display issues | Pending transactions, token balance display issues, and cached pricing problems can make the interface feel broken | Users can clear account history, cache, or all saved app data from settings and retry the action |

| February 2026 | Provider-side purchase and payment troubleshooting updated | Fiat buy flows can take from minutes to days, or fail if the bank or provider declines the payment | Users are routed to the relevant provider support path and may need to change payment method or wait for review |

Uniswap’s core execution layer is often more resilient than its surface data layer. Still, the lack of a traditional status page means users need to rely more on troubleshooting docs than they would on a centralized platform with a formal incident dashboard.

Customer Support

Uniswap’s support model is functional, but it is lean. The main official human support route is support@uniswap.org, backed by the Uniswap Help Center. The official links page also points people to Uniswap’s website, Discord, X, YouTube, GitHub, and Reddit. Those channels are useful for updates and documentation, but they are not presented as full account-support desks.

There is no clear public phone line or standard live-chat queue in the official support materials reviewed for this update. Uniswap’s Terms also say the company may offer an AI-powered support chatbot for general questions and navigation support. It is not positioned as legal, financial, tax, or investment advice.

Support is strongest when the issue can be solved through documentation. The Help Center covers wallet setup, swaps, network costs, stuck transactions, scam prevention, unsupported tokens, and buy or sell flows handled by outside services. It also covers extension setup. That works well for people who are comfortable troubleshooting on their own. It works less well for anyone who expects live hand-holding after a failed bank transfer or a complex wallet mistake.

Lockouts and recovery highlight the limits of the model. Because Uniswap is non-custodial, support cannot restore a lost recovery phrase or reverse an onchain mistake. In many cases, the best recovery path is documentation rather than intervention. That is a consequence of the custody model, not just a service decision.

There is a more formal dispute route if needed. Uniswap’s Terms direct people with legal disputes to contact legal@uniswap.org before formal resolution procedures begin. That is useful for serious complaints, but it is not a substitute for routine product support.

For day-to-day help, the most useful resources are the official Help Center, the official links page, and the guidance built into the wallet, extension, and swap flows. Never use Telegram, WhatsApp, unsolicited DMs, or “wallet recovery” agents for Uniswap support. Uniswap says support runs through official channels and warns that Telegram and WhatsApp support accounts are scams.

Features That Matter on Uniswap

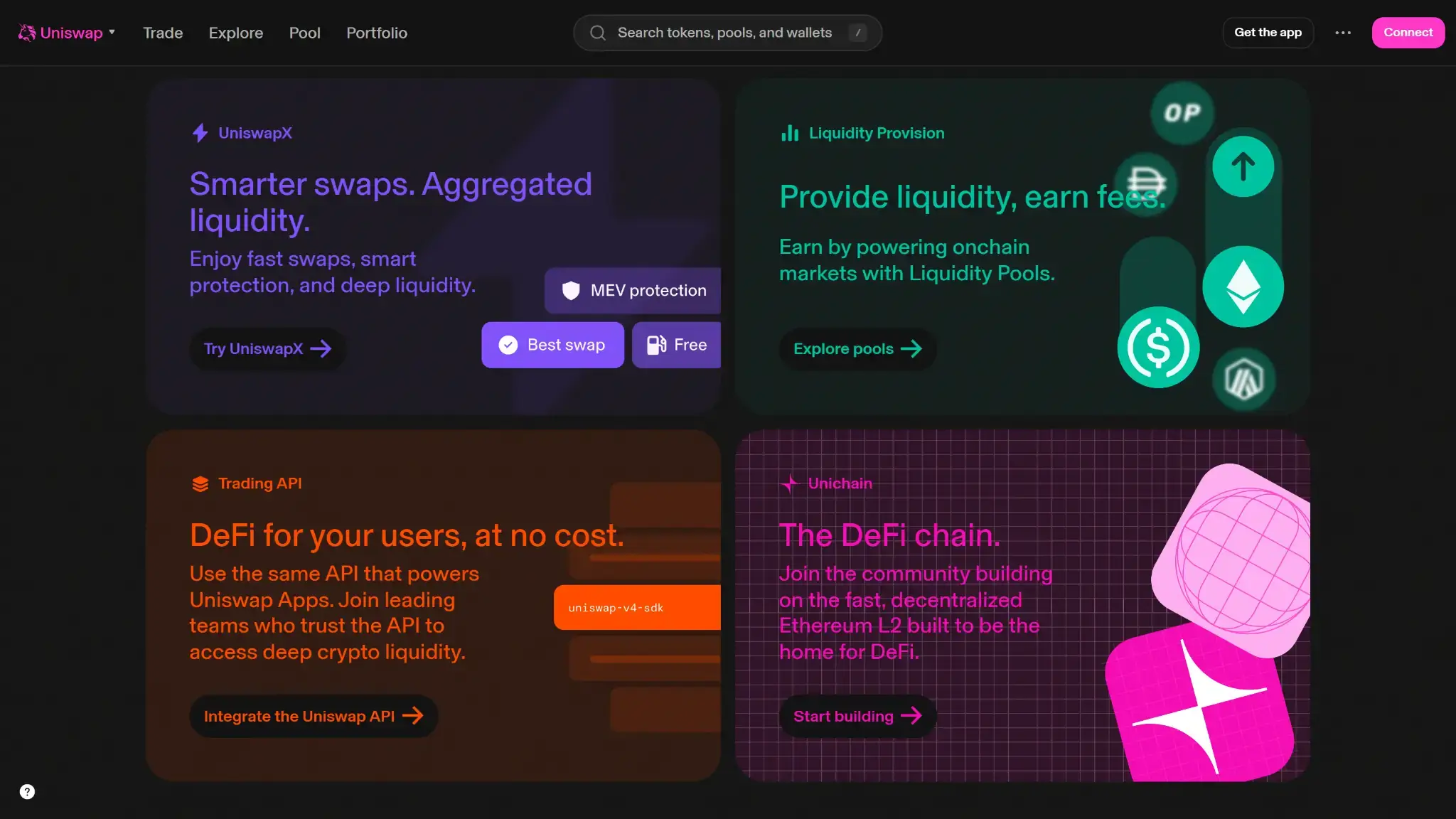

Uniswap is not trying to be a one-stop centralized exchange with cards, leverage, and yield products layered on top. Its real ecosystem is built around onchain trading, liquidity access, routing, and developer infrastructure. The features that matter most are the wallet and extension, UniswapX and limit orders, crosschain execution, liquidity tools, and the API that lets other apps tap into the same routing stack.

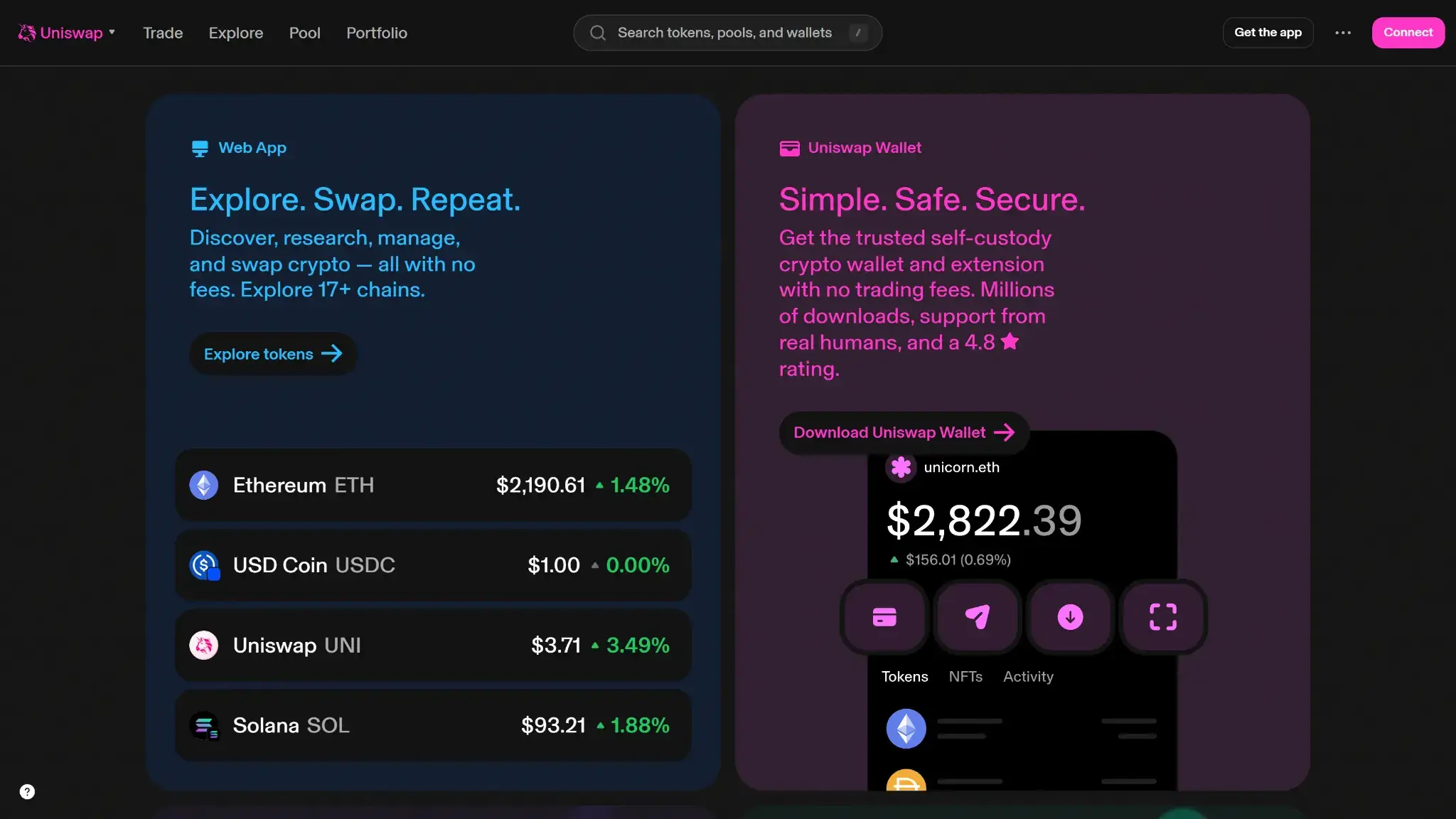

Wallet and Self-Custody Options

Uniswap’s wallet setup is best understood as a self-custody product family rather than a single app. Traders can use the web app with a compatible wallet, use the Uniswap Wallet on mobile, or install the Uniswap Extension in Chrome. That creates a more cohesive wallet-native experience than many DEXs that rely almost entirely on outside wallets.

The trade-off is responsibility. The Uniswap Wallet is self-custody, so people control their own assets and recovery phrase. That reduces exchange custody risk. It also means Uniswap cannot restore access or reverse a bad transaction. For experienced onchain traders, that is part of the appeal. For beginners who want recovery help, it is a real drawback compared with wallets for beginners.

Network support is broad, but not perfectly uniform across products. The web app, mobile wallet, and extension support a wide set of chains, yet feature coverage still varies at the margin. Solana, for example, is currently supported in the web app only rather than across the full product suite.

This setup suits people who already live onchain and want more than a generic browser wallet. It is especially useful for traders who swap regularly, manage multiple assets, want portfolio visibility, and prefer to keep execution inside one recognizable ecosystem.

API and Programmatic Trading

Uniswap’s API is one of the clearest differentiators between the platform and a standard retail DEX front end. The API is free to use, requires an API key, includes OAS documentation, and supports quote, swap, and liquidity workflows. It is built for wallets, fintech apps, embedded trading flows, and teams that want to use Uniswap routing without rebuilding the full stack themselves.

This is more than a hobby developer add-on, but it is not presented like a classic institutional FIX stack either. The public documentation is centered on API-key access, integration guides, quote simulation, routing controls, and production endpoints rather than on prime-broker style connectivity. Uniswap also allows integrators to build white-label swap flows, plug trading into custodial wallets, and set their own integrator fee in supported flows.

The main limitations are practical rather than fatal. Default rate limits are modest, there is no sandbox environment, and testing happens through supported testnets on production endpoints. That makes the API more serious than a marketing feature, but still lighter than the infrastructure stack some institutional trading firms may expect.

UniswapX, Limit Orders, and Crosschain Execution

This is where Uniswap feels more advanced than the old “connect wallet and swap” DEX model. UniswapX improves execution on supported routes by letting third-party fillers compete to fill orders, which can reduce direct gas friction and improve pricing relative to a plain onchain swap. It is one of the most meaningful reasons to use Uniswap instead of a thinner AMM front end.

Limit orders matter too, even though their scope is still narrow. They currently run through UniswapX and are available on Ethereum Mainnet only. That makes them genuinely useful for active Ethereum users, but not yet a universal trading feature across every supported network.

Crosschain swaps make the product easier to use in practice. Instead of forcing users to bridge first and swap second, Uniswap can handle the bridge and swap together in one flow on supported routes. That reduces friction for users moving between Ethereum, Base, Arbitrum, Optimism, Unichain, and several other supported networks. The route still adds bridge fees and can take longer than a same-chain swap.

Together, these features make Uniswap stronger for active spot users than for passive buy-and-hold users. The platform does not need leverage products to feel sophisticated because its routing and execution layer already gives experienced traders enough to care about.

Liquidity Provision and Other Onchain Tools

Liquidity provision is still one of Uniswap’s defining features. Users are not limited to swapping. They can also add liquidity, manage positions, compare pools, and work across multiple versions of the protocol through the same ecosystem. Uniswap is one of the few products in this category where LP access is not an afterthought.

The product ecosystem is also broadening around those core DeFi use cases. The Explore experience now surfaces more token and pool data, and Uniswap has begun pushing into newer product layers such as token auctions inside the web app. Those features are still less central than swapping and LP management, but they reinforce what Uniswap actually is: a serious onchain market interface, not just a swap widget.

There is no meaningful card product shaping the decision here, and there is no native leveraged trading stack to weigh against a derivatives exchange. Readers focused on spending perks may get more value from a crypto card than from a DEX. Uniswap is at its best when the user wants self-custody spot access, better routing, and deeper onchain tooling rather than a long menu of exchange add-ons.

Final Verdict

Uniswap is a strong fit for users who already understand wallets, onchain execution, and the trade-offs that come with self-custody. It gives active DeFi users broad market access, strong routing, useful liquidity tools, and a more complete product ecosystem than most DEX interfaces. The trade-offs are clear. It is less suitable for beginners, fiat-first users, and anyone who wants exchange-style recovery, support, or derivatives. For self-custody spot traders, though, Uniswap still earns its place near the top of the category.

Best For

Self-custody onchain traders

Uniswap does not hold user funds, which removes the usual exchange custody risk., Traders can access millions of assets across 17+ supported chains., Uniswap combines UniswapX, limit orders, crosschain swaps, and liquidity tools in one product ecosystem.

Why it stands out

- Non-custodial design means Uniswap Labs does not hold user wallet balances.

- Broad coverage across 17+ supported networks gives users deep onchain market access.

- 0% interface fee at capture time makes costs easier to understand than many retail buy flows.

- Product depth goes beyond basic swaps, with limit orders, crosschain routing, LP tools, wallet access, and API support.

- Strong fit for users who want direct DeFi exposure without opening a centralized exchange account.

What to consider

- Not ideal for beginners who want simple fiat in and fiat out with predictable support.

- No exchange-style custody protections or recovery path if you lose wallet access or sign a bad transaction.

- Total trading cost still depends on pool fees, gas, route selection, and third-party provider fees.

- Some buy, sell, and compliance steps depend on outside payment partners rather than a fully native Uniswap flow.

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.