A few years ago, “adding crypto” often meant bolting a volatile asset class onto a consumer app and hoping demand carried the product. That era is fading. Today, institutions revisiting crypto are doing it with more pragmatic goals and tighter controls.

Demand is real, but needs governance

Customer demand exists across multiple use cases, and it is rarely “just trading.” Common asks include trading and conversion, transfers, spending, and treasury utility. The challenge is not demand, it is delivering a controlled experience with clear disclosures, predictable operations, and compliant workflows.

Competitive pressure is structural

Neobanks and super-app style fintechs increasingly bundle more financial services under one roof. Crypto is often on the shortlist because it can lift engagement and retention, but only if the product is reliable and supportable at scale.

Monetization is measurable

Crypto products can be evaluated like any other financial product line. Common levers include conversion take rate, spreads (with transparent disclosure), transaction fees, premium tiers, and retention-driven revenue per user expansion. The key is to model unit economics alongside risk and operational cost from day one.

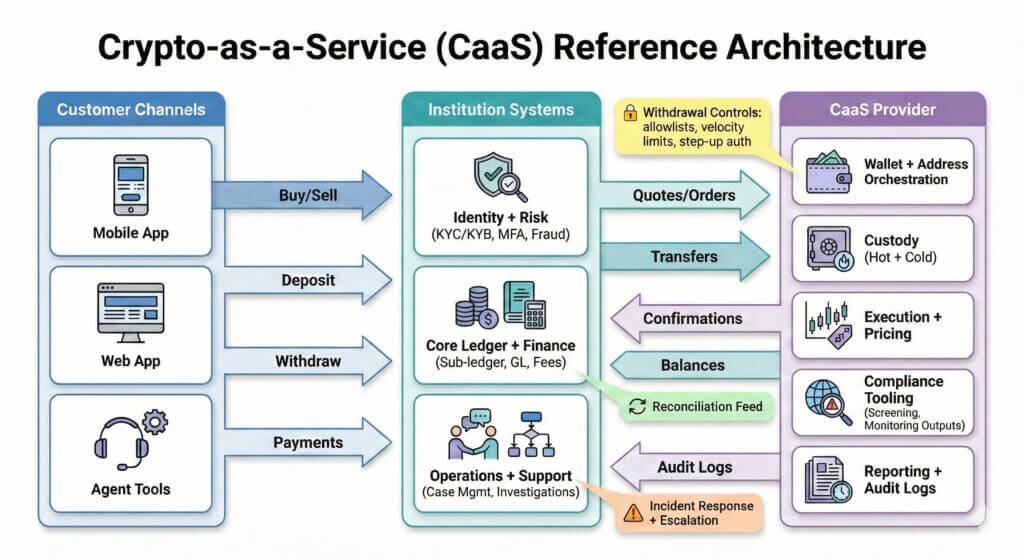

Partnerships shorten the path

For many newly launching banks and fintech programs, the most realistic path is integration: white-label partners and core-banking providers can connect to a CaaS provider so a new institution can receive crypto functionality without standing up every component internally.

WhiteBIT tie-in: CaaS is positioned as a faster, lower-risk route than building a full stack, especially when you want to keep governance inside the institution while outsourcing specialized infrastructure.