There has been an increase in bank accounts belonging to crypto professionals being frozen or restricted across the UK, US, and EU over the past few months. They say you often don't care about something until it happens to you; well, this week, it did. To my genuine surprise, it came from the one place I least expected it.

Revolut has long been regarded as the most crypto-friendly bank in the United Kingdom, offering in-app crypto purchases and, in 2023, finally adding the ability to send and receive crypto, albeit with certain limitations. However, recent events have called into question the bank's commitment to providing a seamless experience for its cryptocurrency-using customers.

Despite the UK no longer being part of the European Union, under which MiCA EU regulations apply, the newly implemented Travel Rule requires similar disclosures. This means that users are now required to reveal and identify the owners of any unhosted wallets that are the recipients of withdrawals from Revolut.

However, UK crypto firms are allowed to apply a risk-based approach to determine when they should gather information on unhosted wallets. They simply need to have the capability to identify where their customers are transacting with unhosted wallets and assess the riskiness of those transactions.

How the UK's most crypto-friendly bank froze my account of 0.23ETH

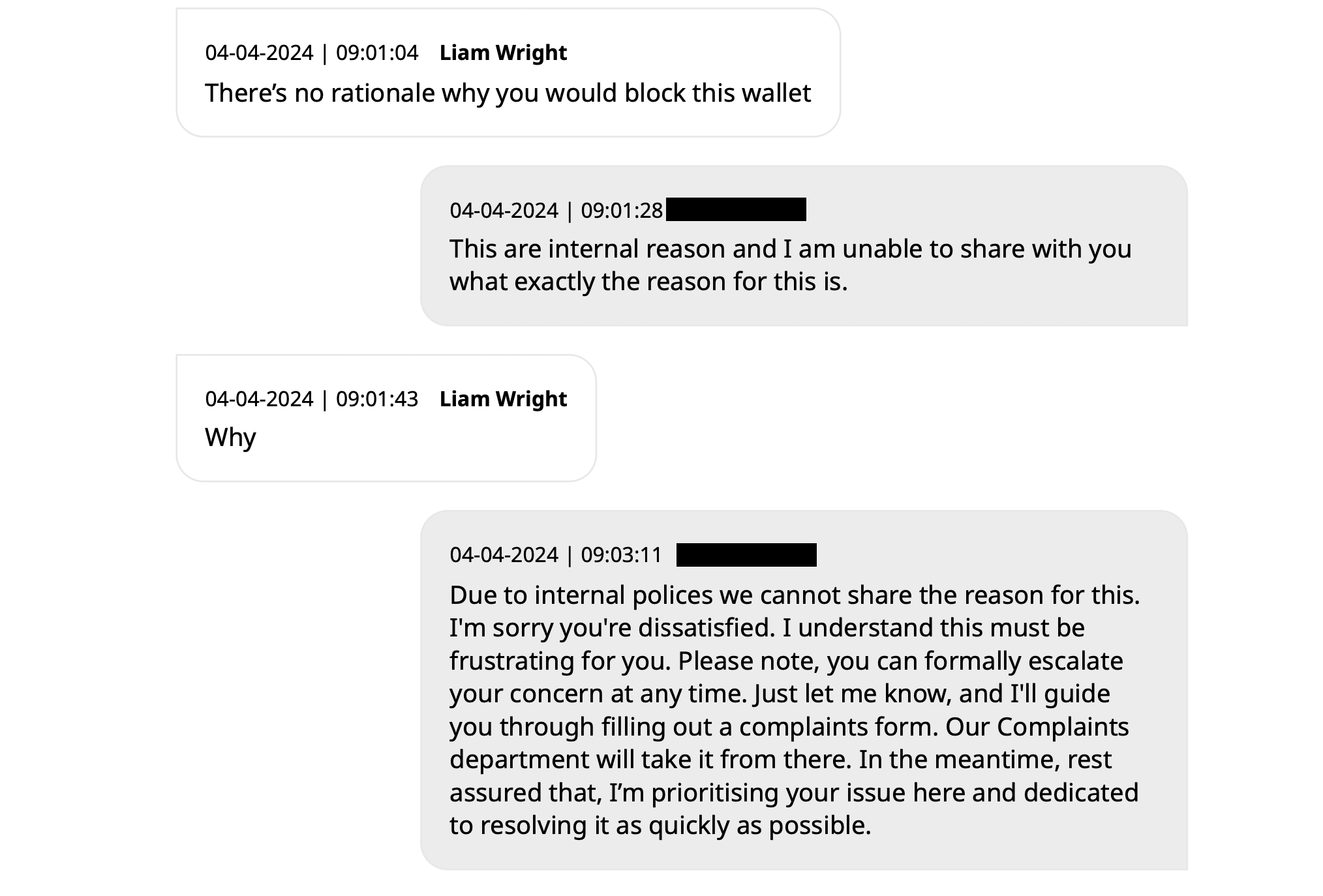

Two days ago, I purchased a modest 0.23 ETH (£550) through the Revolut app and attempted to transfer the funds to my personal Ethereum wallet, which is linked to a well-known ENS domain. To my surprise, Revolut blocked the transaction and took fees from the account. Moreover, my entire bank account, including a joint account with my wife, was frozen.

After several hours of frustration and confusion, the account was eventually unfrozen, and fees were refunded after a further request. However, the specific wallet address remains blocked, preventing me from sending funds to that account. This experience has left me questioning the true nature of Revolut's supposed crypto-friendliness. Given the alternatives in the UK, Revolut remains the best option for those unsatisfied with traditional banks, but it is a low bar. I believe that incidents such as these have less to do with Revolut being ‘anti-crypto' and more to do with a fear of regulatory retribution.

Still, the chat transcript between Revolut's support team and me reveals a lack of transparency regarding the reasons behind the account freeze and the wallet address block. The support representatives could not provide a clear explanation, citing internal policies that prevent them from sharing the specific reasons for these actions.

This incident raises concerns about the autonomy and control that Revolut users have over their own funds, particularly when it comes to digital assets transactions. Blocking a personal wallet address without a satisfactory explanation undermines trust in the bank's ability to facilitate smooth crypto transactions.

As the UK navigates the post-Brexit financial landscape, banks like Revolut must strike a balance between compliance with regulations and providing a user-friendly experience for their customers. The strict application of laws and the lack of transparency in addressing account and wallet issues risk alienating crypto users who rely on these services. This is especially true given that the company is looking to open a dedicated crypto exchange offering.

Debanking crypto users in the United States

In the United States, even crypto users who have been long-time customers of traditional banks face account closures due to their involvement with digital assets. John Paller, co-founder of ETH Denver, recently shared his experience on Twitter, revealing that Wells Fargo had debanked him after 26 years of patronage and millions paid in fees. Paller's checking, savings, credit card, personal line, non-profit, and business accounts were all shut down without explanation, despite him not using his personal accounts for crypto purchases in recent times.

Caitlin Long, Founder and CEO of Custodia Bank, responded to Paller's tweet, noting a significant increase in inquiries from crypto companies urgently seeking to replace bank accounts closed by their banks. She referred to this trend as another wave of “Operation Choke Point 2.0,” suggesting a full-on witch hunt against crypto-related businesses.

Bob Summerwill, Director of the Ethereum Classic Cooperative, echoed the sentiment, emphasizing the need for banks like Custodia. He shared his own experience with PayPal, which closed the Ethereum Classic Cooperative's account without providing specific reasons, only stating that the decision was permanent and could not be overturned.

These incidents highlight a growing concern within the crypto community: even those who have established relationships with traditional banks and have a compliance history are at risk of losing access to banking services. The lack of transparency and the abrupt nature of these account closures raise questions about the underlying motivations behind these actions and the potential impact on the growth and adoption of cryptocurrencies in the United States.

Positive friction really just means a terrible user experience

Anecdotally, I have also heard from at least five other individuals who work in crypto and regularly move substantial sums of FIAT currency through traditional banks that have had accounts frozen. I am not advocating for a Wild West; common sense regulation is all I ask.

CryptoSlate Daily BriefDaily signals, zero noise.

Market-moving headlines and context delivered every morning in one tight read.

5-minute digest 100k+ readers

The UK's approach to regulation also includes what it considers ‘positive friction.' The concept refers to a set of regulatory measures designed to introduce certain barriers or checks that slow down the process of investing in digital assets. These measures are intended to counteract the social and emotional pressures that might lead individuals to make hasty or ill-informed investment decisions. The Financial Conduct Authority (FCA) has introduced these ‘positive frictions' as part of its financial promotions legislation, aiming to enhance consumer protection in the crypto market.

Specific examples of “positive friction” include personalized risk warnings and a 24-hour cooling-off period for first-time investors with a firm. These measures are designed to ensure that individuals are adequately informed about the risks associated with crypto investments and have sufficient time to reconsider their investment decisions without the influence of immediate emotional or social pressures.

The reality is a series of questions designed to scare off new investors, followed by an unsightly banner warning across the top of every crypto app that seemingly never goes away even after you have passed all requirements.

I would like to know when the government will be implementing a test on fractional reserve banking for all traditional finance customers? We have to know about the nuances of government regulation on crypto, such as who the FCA oversees and whether a whitepaper is required. Suppose we were to ask ten people on the street what happens when you deposit funds into their checking accounts. I wonder how many would pass the test?

How many know US and UK banks' reserve requirements are 0%? Previous limits of 5 – 10% were dropped in 2020, and now it is at a bank's own discretion how much of its customers' funds are actually held in cash. Therefore, it is entirely legal for a bank to take a £1,000 deposit and loan the total amount out to another party.

Of course, traditional finance is regulated, and money is ‘guaranteed' by government insurance, so we don't need to worry. Let's just not look back to 2008 when we had to rely on such tools, shall we? It took less than 10% of customers to withdraw funds from Northern Rock for it to collapse.

Banks don't have all of your money; well-run crypto exchanges and self-custody wallets do, but regulations suggest we should be terrified of crypto?

I think it's the banks that are terrified.

I asked Revolut's support and X teams if the PR department would like to comment on my situation ahead of this op-ed, but the question was repeatedly ignored.

Mentioned in this article