JPMorgan’s $30 billion Strategy call exposes Bitcoin’s new market fault line

Strategy’s capital markets machine may give Bitcoin a huge recurring buyer, but the same flywheel also means BTC could become increasingly dependent on one company’s ability to keep issuing stock and preferred shares.

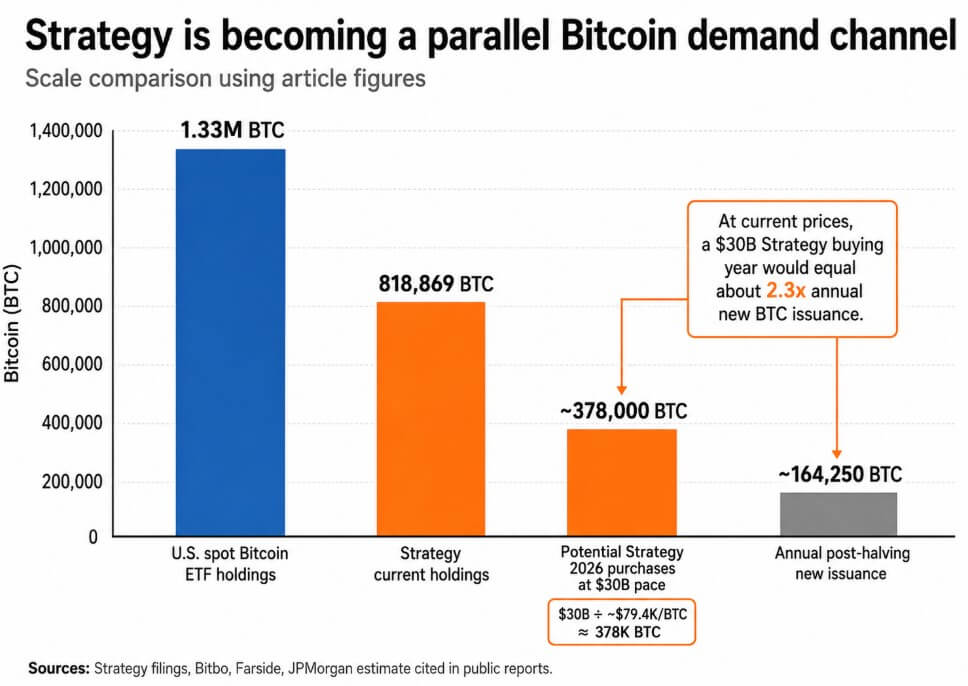

A May 7 JPMorgan client note estimated that Strategy could buy roughly $30 billion in Bitcoin in 2026 if Michael Saylor's company maintains its current purchasing pace.

That figure positions Strategy alongside spot ETF flows and miner supply as a structural force in Bitcoin's demand architecture.

Strategy holds 818,869 BTC acquired for $61.86 billion at an average cost of $75,540, and with $26.35 billion of MSTR stock issuance capacity and $19.46 billion of STRC preferred-stock capacity still available, the capital markets runway exists to approach that number.

JPMorgan's estimate puts Strategy's capital structure at the center of Bitcoin's bull and bear case simultaneously, as the same machine that could create a price floor concentrates Bitcoin's marginal bid within one company's access to equity and preferred stock markets.

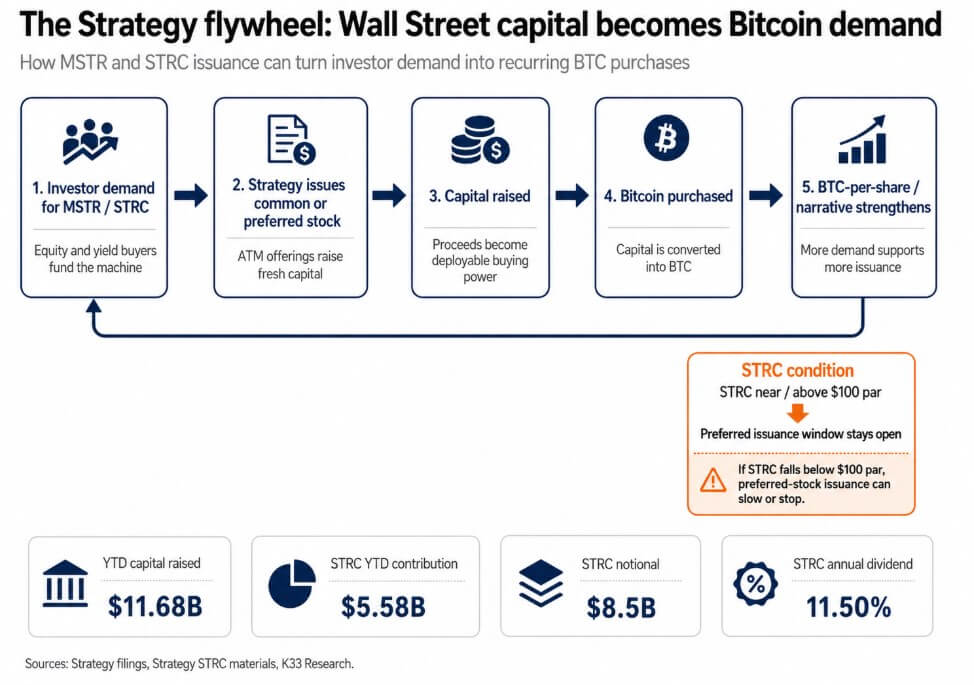

The flywheel

Strategy's buying mechanism consists of raising capital in public markets, converting it into Bitcoin, and using BTC-per-share growth to attract more investor demand, enabling more issuance and more purchases.

As of May 3, the company had raised $11.68 billion year to date, with STRC contributing $5.58 billion, up 189% year to date, scaling to $8.5 billion in nine months and pushing preferred equity outstanding above $13.5 billion.

Strategy designed STRC to trade near its $100 par value by adjusting the monthly dividend rate, keeping investor demand calibrated around par, and maintaining a consistent ATM issuance window.

When STRC trades at or above par, Strategy sells additional shares and uses the proceeds to buy Bitcoin, converting yield demand into BTC demand.

K33 documents that STRC-linked purchases grew from 4,467 BTC in January to 22,131 in March and 46,872 in April.

At $30 billion annualized, that buying absorbs approximately 378,000 BTC, roughly 2.3 times Bitcoin's post-halving daily issuance of 450 BTC, sustained over a full year.

US-traded spot Bitcoin ETFs hold approximately 1.33 million BTC in total since launch, and a $30 billion Strategy purchase year would equal roughly 51% of all cumulative spot ETF net inflows of $59.18 billion.

Strategy's 818,869 BTC already equals about 62% of US spot ETF holdings, placing it alongside the ETF complex as a parallel demand channel.

Recurring bid becomes absorbed supply

Strategy buys dips systematically, as its $75,540 average cost is roughly 5.1% below the current BTC price near $79,373, demonstrating accumulation through market volatility.

Its remaining $45.81 billion in combined MSTR and STRC issuance capacity provides runway for sustained purchases. At 1,036 BTC per day, Strategy would consistently absorb more than twice Bitcoin's daily new supply, drawing down available float throughout the year.

In April, when STRC traded at or above $100, Strategy executed 46,872 BTC of STRC-linked purchases amid mixed ETF flows, providing demand precisely when the diversified institutional channel was running lean.

Citi's bullish 12-month BTC scenario targets $165,000, contingent on easing liquidity and sustained institutional demand. A Strategy flywheel running at JPMorgan's reported $30 billion pace supplies exactly the sustained corporate-finance demand that scenario requires.

When the flywheel stalls

When STRC trades below $100 par, the preferred-stock ATM program closes because selling below par destroys value.

K33 noted that STRC-linked purchases went from 46,872 BTC in April to 1 BTC in the single week STRC slipped below par, a complete shutdown of the preferred-stock funding channel from one instrument's dislocation.

Strategy's STRC prospectus sets dividend payments as contingent on board declaration, reserves management's right to skip payments even when funds are available, and grants sole discretion over rate adjustments designed to maintain the $100 par target.

The company also states it expects to fund cash dividends primarily through additional capital raising, meaning the dividend depends on the same issuance machine it is meant to support.

At $8.54 billion in STRC notional and an 11.50% annual dividend, the cash obligation is approximately $982 million per year, equivalent to around 12,370 BTC at current prices, a carrying cost that persists regardless of whether new issuance is underway.

| Scenario | Capital-market condition | Strategy buying pace | BTC implication |

|---|---|---|---|

| Floor case | STRC trades at/above $100; MSTR premium holds | Purchases remain large; $30B annualized pace possible | Strategy absorbs supply and supports BTC upside |

| Base case | STRC near par; MSTR issuance still open but less aggressive | Buying continues below $30B pace | BTC gets support, but less of a durable floor |

| Stall case | STRC below par; preferred ATM shuts | Purchases shrink sharply, like April’s 46,872 BTC falling to 535 BTC in the latest week | BTC loses a major marginal buyer |

| Fault-line case | BTC falls below $75,540 average cost; MSTR premium compresses | Issuance becomes more expensive or dilutive | Strategy shifts from price-floor narrative to downside amplifier |

The bearish sequence runs directly from Bitcoin falling toward Strategy's $75,540 average cost, MSTR's premium to net asset value compressing, STRC slipping below par and shutting preferred-stock issuance, Strategy's weekly purchases collapsing from thousands of BTC to a trickle, and Bitcoin loses a buyer that had been absorbing more than twice its daily new supply.

Citi's adverse macro scenario places Bitcoin at $58,000, 23% below Strategy's average cost, at which point the floor narrative inverts entirely.

Between May 4 and May 10, Strategy bought 535 BTC for $43 million, with the company's April flywheel at 46,872 BTC collapsing to a 535 BTC purchase, showing how directly BTC accumulation tracks which capital markets channel is open at a given moment.

The concentration issue

US-traded spot Bitcoin ETFs distribute demand across dozens of issuers, market makers, and investor bases, each holding BTC independently with costs and obligations spread across the entire complex.

Strategy consolidates all of that into one capital structure, one management team's discretion, and one set of securities whose market performance determines Bitcoin's corporate bid.

JPMorgan's reported $30 billion estimate extrapolates the current pace and depends on capital markets, BTC price, STRC demand, and MSTR premiums staying favorable simultaneously.

Citi's base case of $112,000 over 12 months is the scenario in which Strategy's flywheel runs at a pace close to that. At $58,000, the same flywheel becomes the mechanism through which a single company's funding stress amplifies Bitcoin's downside, inverting its role from floor to amplifier.

Strategy's buying may be a price floor as long as capital markets stay open, but when yield buyers demand more to stay in STRC, and equity buyers require a lower MSTR premium, the floor starts to look like a fault line.

Bitcoin is -3.17% over the past 24 hours and currently sits at rank #1 by market cap.

More Bitcoin market context Supply, launch date, volume flow, and price-cycle context.

Where the broader market sits right now

Right now, the total crypto market is valued at $2.14T with $68.68B in 24-hour volume. Bitcoin dominance sits at 58.15%. Explore the market