Debt nation: The unsustainable rise of debt in the U.S.

Understanding the U.S. debt landscape to provide an overview of the nation's economic health, consumer behavior, and potential future trends.

Introduction

The United States is currently navigating a labyrinth of financial obligations that have profound implications for its economic future. The U.S. debt landscape encompasses a myriad of components, from national to household debts, each with its unique characteristics and challenges. As of 2023, the nation finds itself grappling with soaring debt figures that have been exacerbated by factors such as the global pandemic, policy decisions, and changing consumer behaviors.

Understanding the different types of debt and their respective magnitudes is not just a matter of economic curiosity; it’s a necessity. Each debt type, be it mortgage, student loan, or credit card, reflects specific societal and economic trends. By dissecting these debts, policymakers, investors, and analysts can gain insights into the nation’s economic health, consumer behavior, and potential future trends.

Moreover, in an interconnected global economy, the state of U.S. debt can influence international trade, investment decisions, and even the stability of global financial systems. In essence, U.S. debt resonates far beyond its borders, making its comprehension crucial for anyone vested in the global financial and crypto markets.

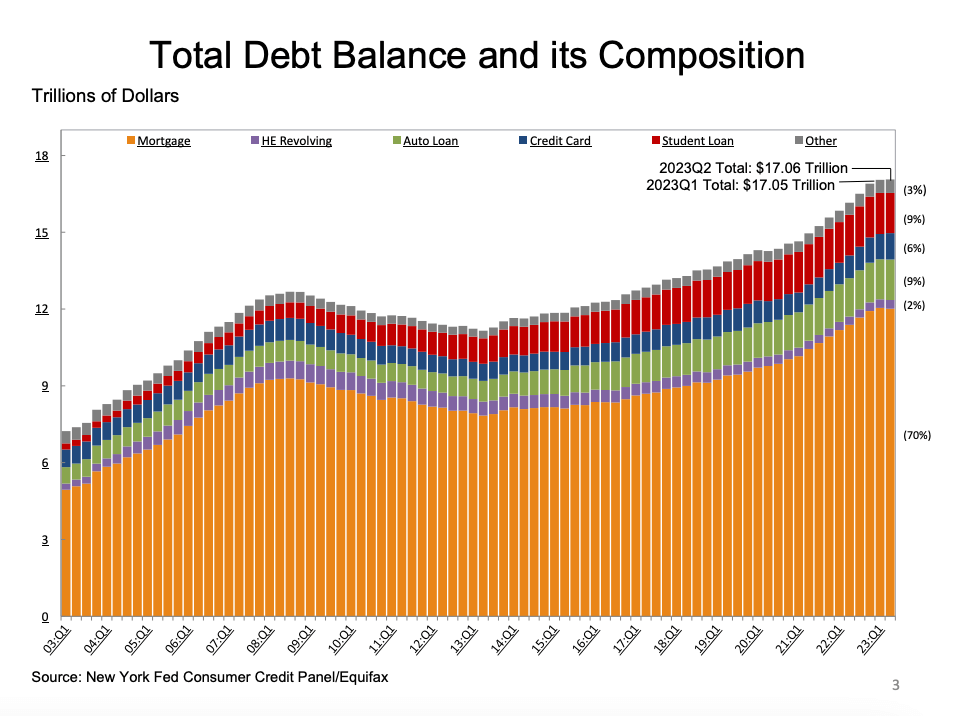

National Debt

The national debt is a term that encapsulates the total amount of money the federal government owes to its creditors. These creditors can range from domestic entities, like individual investors and banks, to foreign governments and international organizations. Essentially, it represents the cumulative amount of deficits the government has run over the years, borrowing to cover its expenses when tax revenues fall short.

As of September 2023, the U.S. finds itself under the weight of a staggering $33 trillion in national debt. To put this into perspective, this amount has seen an increase of $2 trillion just from the previous year, signaling an accelerated rate of borrowing. Such a rapid ascent in the debt level is not a result of spontaneous financial decisions but is deeply rooted in a combination of factors.

{kind=link}

One of the primary contributors to this rise has been the increased government spending during the global pandemic. As the U.S. grappled with the COVID-19 pandemic, there was a pressing need for financial interventions to support businesses, healthcare, and individuals facing economic hardships due to government-mandated lockdowns. Additionally, policy decisions, including tax cuts, have reduced the government’s revenue stream, necessitating further borrowing. Ongoing military expenditures and infrastructural projects have also played their part in driving up the debt.

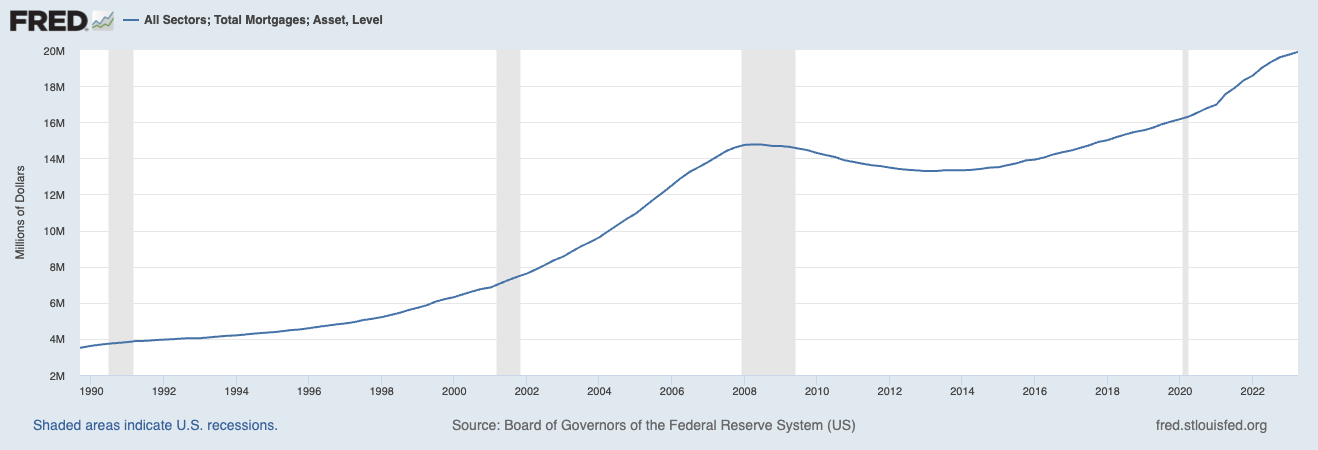

Mortgage debt

Mortgage debt arises when individuals or families borrow money to purchase residential properties. This form of debt is secured by the value of the property, meaning if the borrower defaults on the loan, the lending institution can take possession of the property through a legal process known as foreclosure.

In the U.S., the magnitude of mortgage debt has been steadily rising, reflecting the broader trends in the housing market and the financial behaviors of consumers. According to the Federal Reserve Bank of New York, residential mortgage debt in the U.S. totaled $19.92 trillion as of the second quarter of 2023. This figure underscores the pivotal role of homeownership in the American dream and the financial landscape.

Mortgage lenders issued 1.52 million residential loans in the fourth quarter of 2022, marking the most significant decline since 2014. Furthermore, the average balance for a first mortgage reached a record high in 2022, standing at $323,780, according to the Mortgage Bankers Association.

The global pandemic had a profound impact on mortgage rates. Initially, the economic fallout from the pandemic led to borrowing becoming cheaper, enticing many with record-low mortgage rates.

However, these low rates were juxtaposed with record-high home prices, creating a challenging environment for potential homebuyers. As 2022 rolled in, the Federal Reserve began raising interest rates in response to inflation and other economic factors, slightly slowing down the home-selling frenzy.

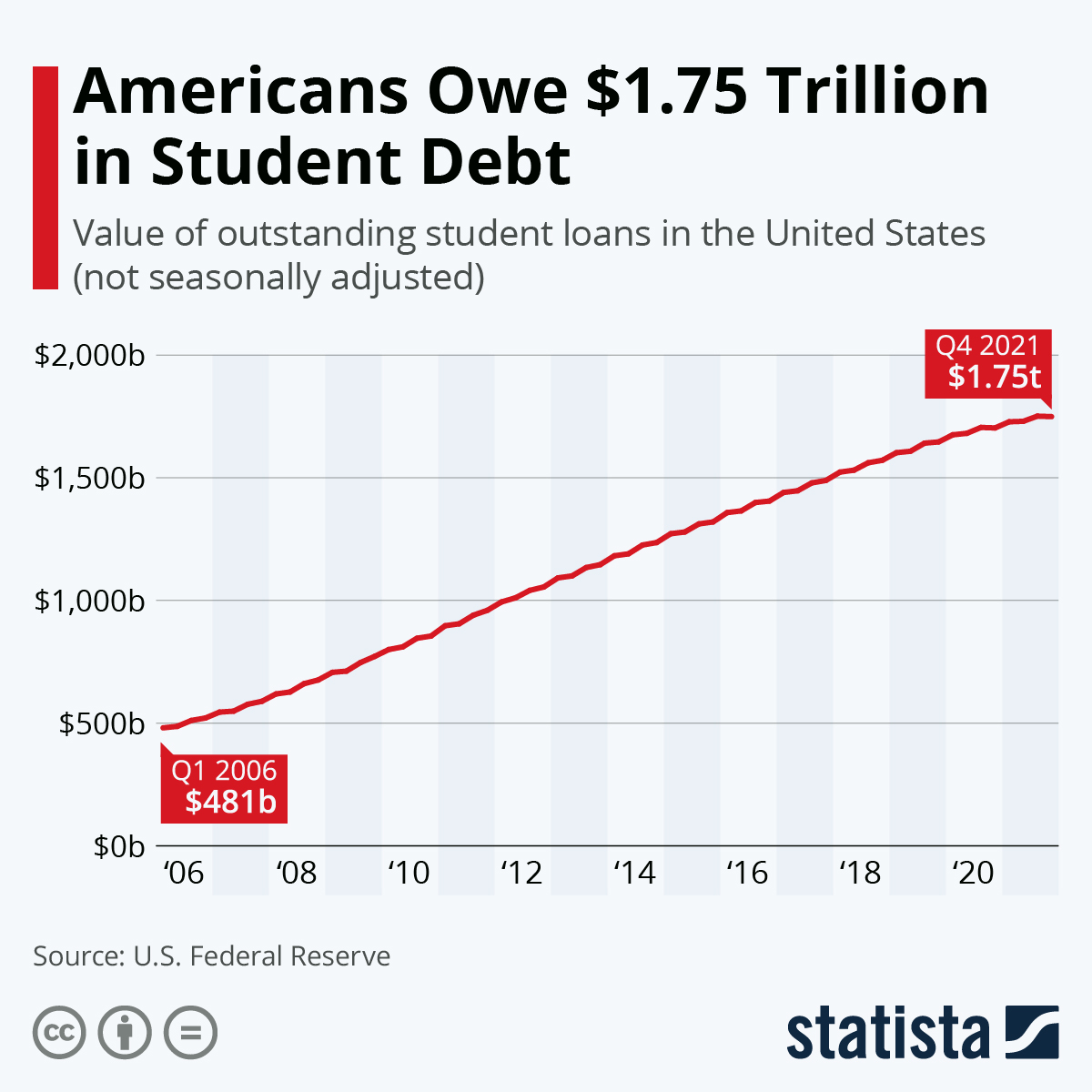

Student loan debt

Student loan debt is a financial obligation incurred by individuals to cover the costs of their education, typically at the post-secondary level. There are two primary types of student loans: federal and private. Federal student loans are funded by the U.S. government and often come with benefits such as income-driven repayment plans and potential loan forgiveness options. Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders, and they often have higher interest rates and fewer repayment options compared to their federal counterparts.

As of 2023, the total student loan debt in the United States has reached a staggering $1.75 trillion. This includes both federal and private loans. To further break it down, about 92% of this debt is from federal student loans, while the remaining portion is from private student loans.

The average amount owed per borrower stands at $28,950. This figure is a testament to the rising costs of higher education in the U.S. and the increasing reliance on loans to finance it. The cost of college has seen a significant increase over the last 30 years, with tuition costs at public four-year colleges growing from $4,160 to $10,740 and from $19,360 to $38,070 at private nonprofit institutions, after adjusting for inflation.

The weight of student loan debt is distributed evenly across institutions. For instance, 55% of students from public four-year institutions had student loans, while 57% of students from private nonprofit four-year institutions took on education debt. The national average balance of federal student loan borrowers is $35,210.

The increasing student loan debt has broader implications for the economy, affecting borrowers’ ability to buy homes, start businesses, and make other significant financial decisions.

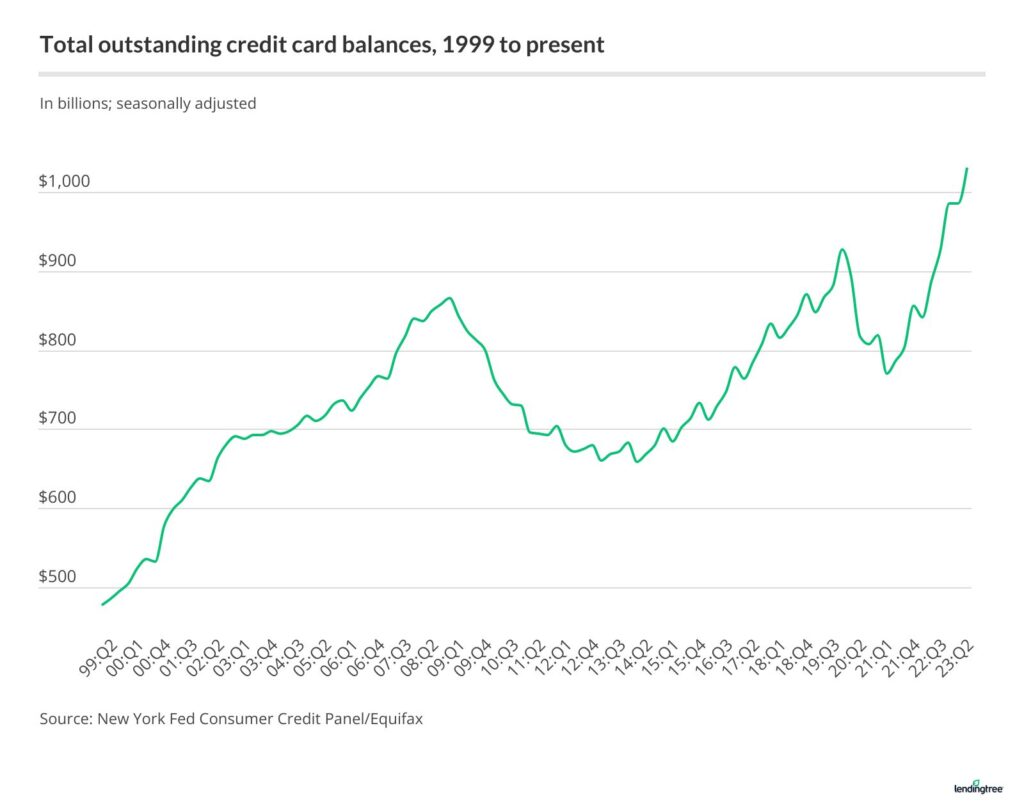

Credit card debt

Credit card debt is the outstanding amount consumers owe to credit card companies. It arises when cardholders make purchases using their credit cards but do not pay off the full balance by the due date. Instead, they carry over a portion of the balance, which then accrues interest. This type of debt is revolving, meaning it can vary from month to month based on new purchases, payments, and accrued interest.

As of the second quarter of 2023, the credit card debt in the U.S. stands at a $1.031 trillion. This figure is particularly noteworthy as it marks the first time credit card debt in the U.S. has surpassed the $1 trillion threshold. The increase of $45 billion in the second quarter comes after a period in the first quarter where the debt level remained unchanged, a deviation from historical trends. In fact, credit card balances have surged by $175 billion since the fourth quarter of 2021, and the current debt is $104 billion higher than the record set in the fourth quarter of 2019.

On a household level, the national average card debt among cardholders with unpaid balances as of December 2022 was $7,279. This encompasses both bank cards and retail credit cards.

Several factors have contributed to the rise in credit card debt. Persistent inflation, rising interest rates, and other economic challenges have made it harder for many consumers to pay off their balances in full each month. Additionally, the aftermath of the pandemic saw a sharp decline in credit card balances — from $927 billion in the fourth quarter of 2019 to $770 billion in the first quarter of 2021. However, a significant spike in the fourth quarter of 2021 reversed this trend, pushing balances to their current levels.

High balances and interest rates can lead to financial strain for many households, affecting their overall economic well-being and future financial decisions.

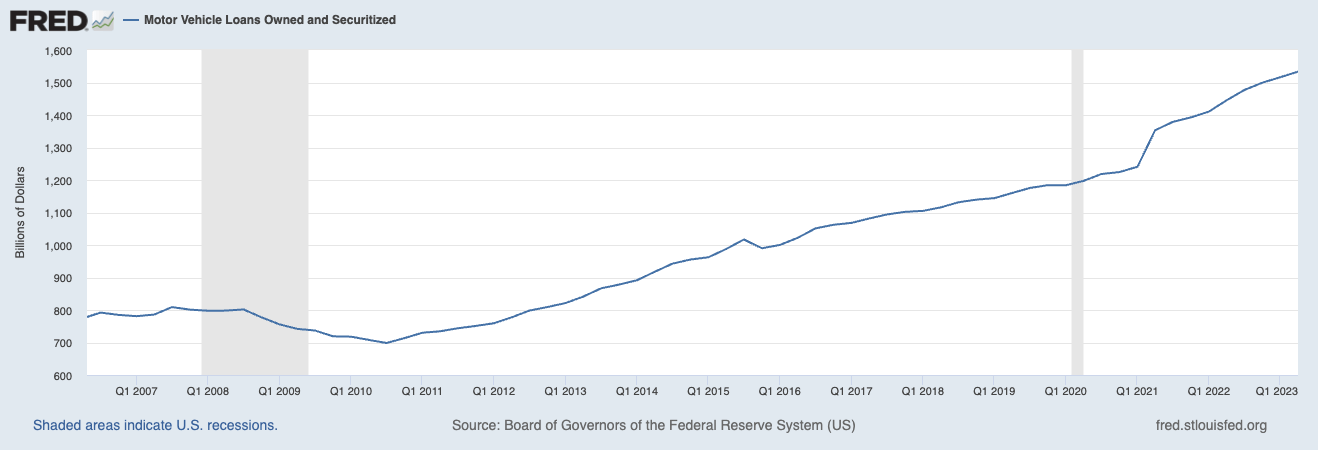

Auto loan debt

In the U.S., auto loan debt has been on an upward trajectory. As of recent data, the auto loan debt in the country stands at a record high of $1.5 trillion. This figure is indicative of the increasing reliance on vehicles for transportation and the rising costs of automobiles, making financing a necessity for many consumers.

Delving into the specifics, the average monthly loan payment for a new vehicle in 2023 is $725, marking an increase from $650 in 2022. For used vehicles, the average monthly payment is $516 in 2023, up by 2% from the previous year. These figures, provided by Experian, highlight the growing financial commitments consumers are undertaking when purchasing vehicles.

Several factors have contributed to the rise in auto loan debt. The aftermath of the Covid-19 pandemic, coupled with supply chain disruptions, has led to increased vehicle prices. Stubborn inflation and the Federal Reserve’s interest rate hikes have further exacerbated the situation, making car ownership more expensive than ever. Joanna Dean, vice president of sales at Toyota Financial Services Group, said that given the current transaction and vehicle prices, financing has become almost indispensable for many consumers.

Conclusion

The mounting debt across various sectors in the U.S. paints a complex picture with far-reaching implications, not just domestically but on a global scale.

For the U.S. economy, high levels of debt can stifle growth. As more funds are allocated to servicing debt, less is available for investment in infrastructure, research, and other growth-promoting activities. This can lead to reduced economic output, potentially resulting in recessions or stagnation.

U.S. citizens bear the brunt of this debt directly. High household and personal debts can lead to financial strain, limiting purchasing power and reducing overall quality of life. The ripple effects can be seen in delayed life milestones, such as home purchases, marriages, and starting families.

On the global front, the U.S. economy plays a pivotal role in driving world economic trends. A debt-laden U.S. can lead to reduced imports, affecting economies dependent on U.S. trade. Furthermore, global investors might become wary of U.S. securities, leading to shifts in global investment patterns.

Lastly, the crypto market, which has been seen as an alternative investment and hedge against traditional financial systems, could experience volatility. As investors seek safe havens or speculate on the U.S. debt situation, crypto prices might witness fluctuations. Moreover, regulatory responses to national debt crises could impact the crypto landscape, either promoting its use as an alternative or imposing restrictions.

More Market Reports