The big nickel short

CryptoSlate's latest market report dives deep into the nickel crisis that began in March 2022, to analyze the overlooked crisis' effect on the crypto market.

Introduction

In March 2022, the global market was hit by an unprecedented event that shook the commodities trading world and sent ripples across the financial market.

This event, known as the Nickel Crisis, was a complex and multifaceted issue that began with a sudden and dramatic surge in nickel prices and culminated in a series of controversial decisions by the London Metal Exchange (LME). The crisis was not only a significant event in the world of commodities trading but also had far-reaching implications for various sectors of the global economy, including the burgeoning cryptocurrency market.

The nickel crisis unfolded in a matter of days but has had consequences that are still being felt months later. It began with a sudden surge in the price of nickel, a key industrial metal used in a wide range of applications from stainless steel production to electric vehicle batteries. The price of nickel skyrocketed from $20,000 per ton to around $100,000 per ton, driven by a combination of factors that include geopolitical tensions, supply chain disruptions, and market speculation.

As of the time of writing, the nickel market has yet to return to normal, and the consequences of the crisis continue to be felt across the global financial landscape. The crisis has raised serious questions about the governance and risk management practices of major financial institutions and has highlighted the potential vulnerabilities of traditional financial markets.

CryptoSlate dives deep into the nickel crisis to analyze its origins, its immediate consequences, and its potential long-term implications for the broader market.

The genesis of the crisis

While the nickel crisis manifested as a sudden and unexpected event, it was actually a culmination of a series of complex geopolitical events and financial maneuvers that converged to create the perfect storm.

At the heart of this storm were two major players: Tsingshan Holding Group, a Chinese stainless steel and nickel manufacturer, and Elliott Management, a prominent U.S. hedge fund. These two entities found themselves on opposite sides of the nickel market, with Tsingshan building a significant short position and Elliott Management taking a long position.

Tsingshan, led by Xiang Guangda, had a unique perspective on the market. With plans to boost production significantly in 2022, their substantial short position was based on the belief that the price of nickel would only fall. This strategy, known as hedging, is a common practice among companies that rely on commodities for their operations. It allows them to lock in prices and protect themselves against future price fluctuations. In Tsingshan’s case, their position would allow them to buy back the metal at a lower price and profit from the difference.

On the other hand, Elliott’s long position in nickel was based on the expectation that the metal price would rise. Several factors could have influenced this belief. First, traders at Elliott might have anticipated growing demand for electric vehicles, which rely on nickel-based batteries. Additionally, the geopolitical tensions regarding the conflict in Ukraine had the potential to disrupt the global nickel supply chain. Russia and Ukraine are both major producers of nickel and the ongoing conflict and sanctions threatened to cut off the supply coming to Europe.

The opposing positions of Tsingshan and Elliott Management set the stage for a classic short squeeze. A short squeeze occurs when a rapid increase in the price of an asset forces those who have bet against that price (short sellers) to buy the asset to prevent further losses. This buying pressure can drive the price up even further, creating a feedback loop that can lead to dramatic price increases.

The short squeeze was further exacerbated by the escalation of the war in Ukraine, which disrupted the global nickel supply chain and created upward pressure on prices. The consequences of a short squeeze can be severe, particularly in a market as volatile and tightly supplied as nickel.

Despite these clear warning signs, the opposing positions of Tsingshan and Elliott Management went largely unnoticed by the LME and the broader market. This lack of oversight allowed the situation to escalate unchecked, leading to the dramatic price surge that marked the beginning of the Nickel Crisis.

The fallout

The senior management of the London Metal Exchange first became aware of a significant short position held by Tsingshan on February 14 through a Bloomberg report. Despite the size of the position, the LME didn’t perceive it as a cause for concern and didn’t seek additional information. However, the LME only knew of Tsingshan’s on-exchange position, unaware that the total off-exchange position was five times larger.

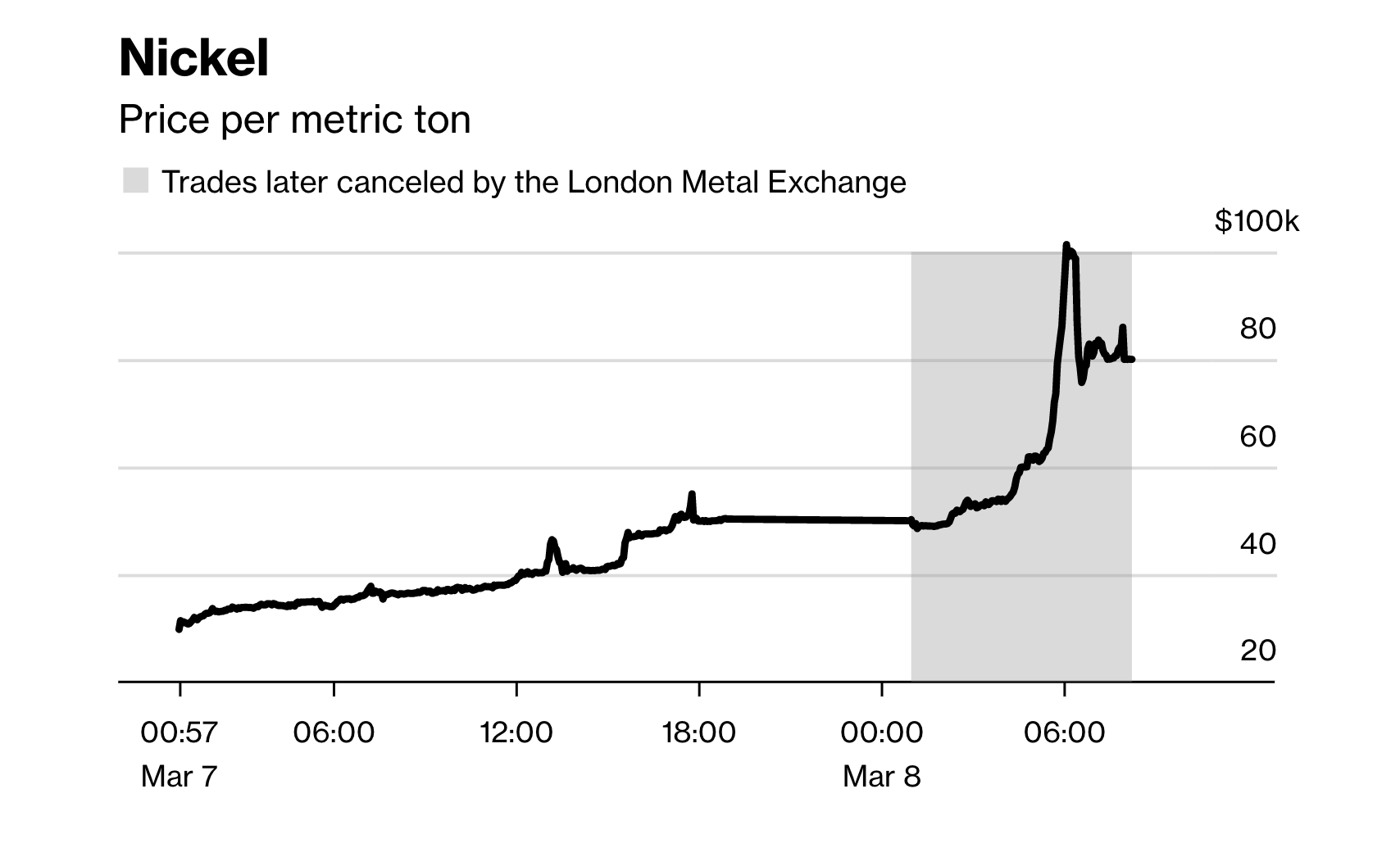

On March 7, nickel prices soared to $36,000 a ton, revealing market strains. Four LME brokers were late meeting their margin calls that morning, including a China Construction Bank Corp. (CCBI) unit that could not pay a margin call in the hundreds of millions of dollars for the entire day. Tsingshan was CCBI’s biggest client at the time, and the company failed to meet its margin calls due to rapidly rising prices.

Such defaults are rare on the LME, and this was the first time since 2014 that a member had defaulted.

As prices continued to surge, the LME began discussing potential responses. The question of whether the market had become “disorderly” was raised. Despite a 60% price increase by 1:30 p.m., the market continued to trade. To alleviate market stress, the LME’s clearinghouse decided to halt margin calls until the following day, potentially increasing risk if prices continued to rise.

At 4 p.m., the LME’s “Special Committee” decided to keep the market open, attributing the price move to geopolitical and macroeconomic factors. However, by the end of the day, CCBI’s margin call remained unpaid, and the exchange’s executives were growing increasingly concerned.

The market opened as usual at 1 a.m. on March 8. After a few calm hours, prices rose again as banks sought to reduce their exposure to Tsingshan by covering part of the short position. The LME’s operations team, in charge of limiting extreme price moves, suspended price bands at 4:49 a.m. following complaints from market participants. This led to a rapid increase in nickel prices. By 5:30 a.m., the price had reached $60,000 a ton and rose another $40,000 in just 38 minutes.

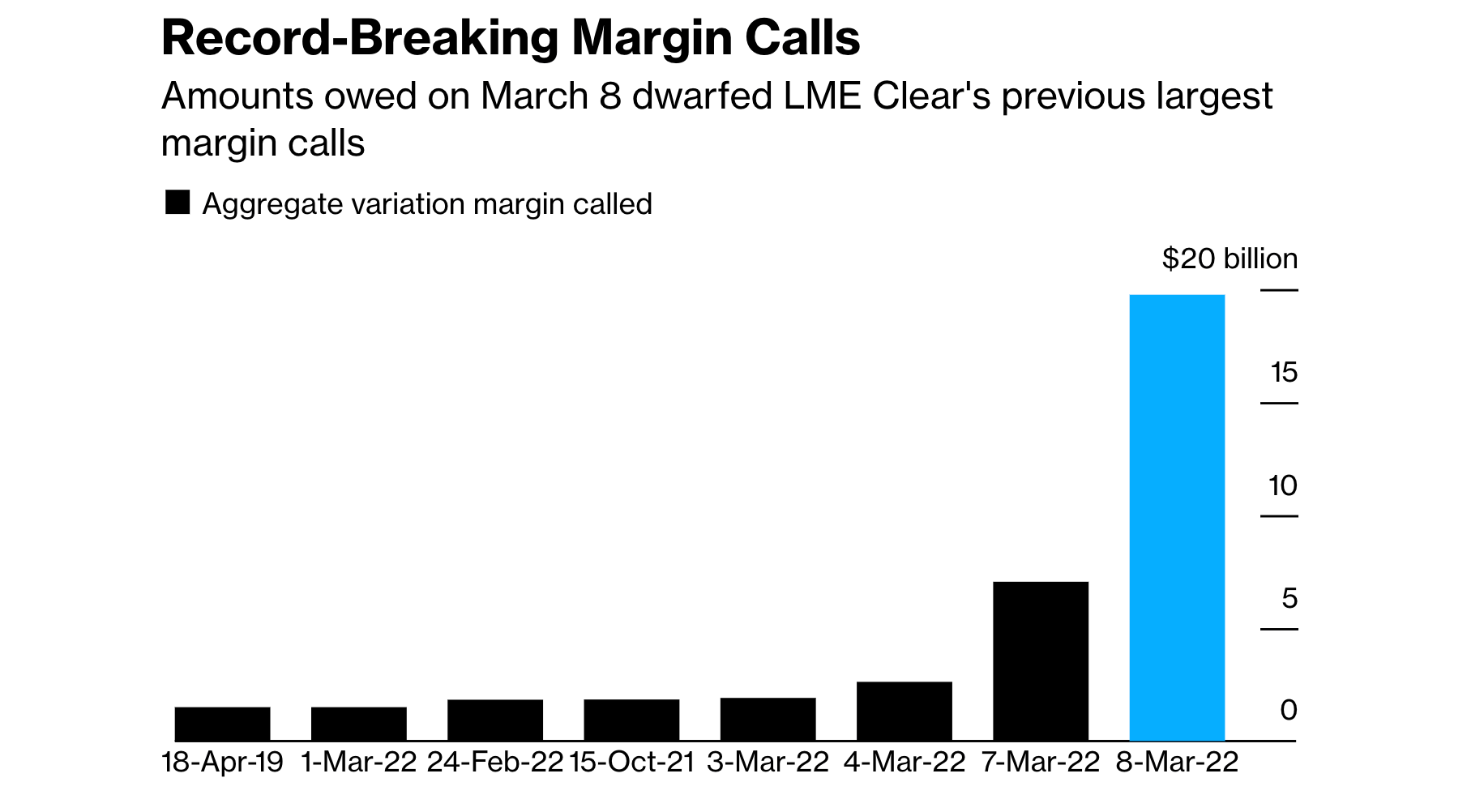

The LME was still unaware of the scale or importance of Tsingshan’s position, the real driver behind the price rally. It wasn’t until later that day that the LME became aware of Tsingshan’s difficulties. Meanwhile, brokers were panicking as they faced an unprecedented margin call of $19.75 billion from 28 banks and brokers. In response to the crisis, the LME decided to suspend the market.

The legal repercussions

The fallout and legal repercussions of the nickel crisis have been significant and far-reaching.

According to Jonathan Crow, the LME’s lawyer, the exchange dealt with a “once-in-a-generation experience,” highlighting the abnormality of the situation.

The LME argues that it was justified in closing the market and canceling trades because $19.7 billion of margin calls would have otherwise led to the defaults of multiple clearing members, creating systemic risk. Failing to suspend trading and cancel deals would have led to a “death spiral” on the LME that would have spread to other financial markets. With multiple defaults of members, the exchange’s clearing house, LME Clear, would have had to take over positions and liquidate them, causing further price spikes and more defaults. Brokers and banks would also have had to drain liquidity from other markets to pay escalating margin calls, hitting other financial markets.

However, trading firm Jane Street argued that the LME had no senior management monitoring the market as nickel prices surged in Asian trading last year. They claim that the LME had only low-level staff on duty in Asia from 1 a.m. London time when the market opened, leading to a breach of its obligations to the market.

Several companies, including Jane Street and Elliott Management, are suing the LME. They argue that the LME had no power to unwind transactions to prevent defaults or tackle systemic risks. They also claim that the LME failed to consult with financial firms that could lose millions of dollars before the decision to cancel trades.

The LME’s lawyers have argued that Elliott and Jane Street have failed to identify any sufficient basis for the court to set aside the LME’s decision-making. They also noted that exchanges are legally required to maintain market order and have the power to cancel trading activity in response to exceptional market events. The LME also defended its decision to suspend its “price bands” for nickel on the morning of March 8, 2022, arguing that the rapid price rises on that day made the bands ineffective.

Implications for the crypto market

The interconnectedness of global financial markets means that disruptions in one sector can have ripple effects across others, including the crypto market.

The immediate impact of the nickel crisis on the crypto market was a heightened sense of volatility. And while it’s hard to determine how much the nickel crisis attributed to the Bitcoin volatility that started with the conflict in Ukraine, its effects were clearly felt.

The uncertainty surrounding the LME’s decision to cancel trades and the subsequent legal actions further exacerbated this volatility. Investors, unsure of the potential fallout from the lawsuits, may have chosen to move their assets into or out of cryptocurrencies, contributing to price swings.

Moreover, the nickel crisis has underscored the importance of regulatory clarity and transparency for all financial markets, including cryptocurrencies. The LME’s decision to cancel trades, while legal, was controversial and has led to significant backlash from market participants. This has highlighted the need for clear, predictable rules and procedures in all financial markets, including the relatively unregulated crypto market. The ongoing lawsuits against the LME could potentially lead to increased calls for more robust regulation and oversight of the crypto market.

Furthermore, the lawsuits against the LME could have implications for how market disruptions are handled in the future. If the courts rule against the LME, it could set a precedent that exchanges cannot unilaterally cancel trades, even in extraordinary circumstances. This could have implications for crypto exchanges, which may face similar situations of extreme market volatility. Crypto exchanges may need to reconsider their policies and procedures for handling such situations to avoid potential legal challenges.

If the lawsuits result in significant changes to how traditional exchanges operate, some investors may view cryptocurrencies as a more attractive investment due to their decentralized nature, which could potentially insulate them from similar controversies. On the other hand, if the lawsuits lead to increased regulatory scrutiny of financial markets, this could deter some investors from cryptocurrencies, often viewed as high-risk, unregulated investments.

Conclusion

While the nickel crisis and the LME lawsuits are primary concerns of the commodities market, their implications for the crypto market could be significant.

The outcomes of these events could shape the future of the crypto market, influencing its regulatory landscape, investor sentiment, and market volatility.

More Market Reports