The information provided in this article is for educational and informational purposes only and should not be construed as financial advice.

Overview

Introduction

In our first guide, we explained why a long-term crypto holder may borrow instead of sell. That is the core logic behind the Buy, Borrow, Die strategy: preserve the long-term position, access liquidity through borrowing, and avoid forcing a sale simply because capital is needed elsewhere.

This guide will focus on the part of that strategy many readers overlook. Once collateral leaves a personal wallet, the central question is no longer just how much can be borrowed or how quickly the funds arrive. The question is what the platform is allowed to do with the collateral while the loan is open.

That question matters because rehypothecation, or collateral reuse, has been a standard financing tool in traditional markets and has also appeared across crypto lending models. The Financial Stability Board defines re-hypothecation narrowly as “any use of client assets by a financial intermediary” and describes broader collateral re-use as any use of assets delivered as collateral by an intermediary or collateral taker. The same report notes that these practices can improve collateral availability and reduce liquidity costs, while also creating leverage, interconnectedness, and potential delays when clients try to access assets during an insolvency.

In plain English, the risk begins when collateral posted for one purpose becomes useful to someone else’s balance sheet. A borrower may believe they have pledged BTC, ETH, or XRP against their own loan. In a rehypothecated model, that same asset may be lent onward, pledged elsewhere, or used to support the crypto lender’s financing. At that point, the user is no longer exposed only to crypto volatility and loan terms. They are also exposed to a chain of counterparties they did not choose.

The failures of Celsius, BlockFi, and FTX were not identical, and FTX was not a classic crypto lender. Still, each case pushed the same lesson into the open: when customer assets are pooled, reused, commingled, or otherwise absorbed into a wider corporate risk structure, platform failure can become customer loss with extraordinary speed.

Reuters reported that Celsius used customer deposits in ways customers did not fully understand, BlockFi’s bankruptcy was tied to exposure to FTX and Alameda, and FTX customer funds were used to cover losses at Alameda Research.

First principle

Buy, Borrow, Die depends on what happens to collateral

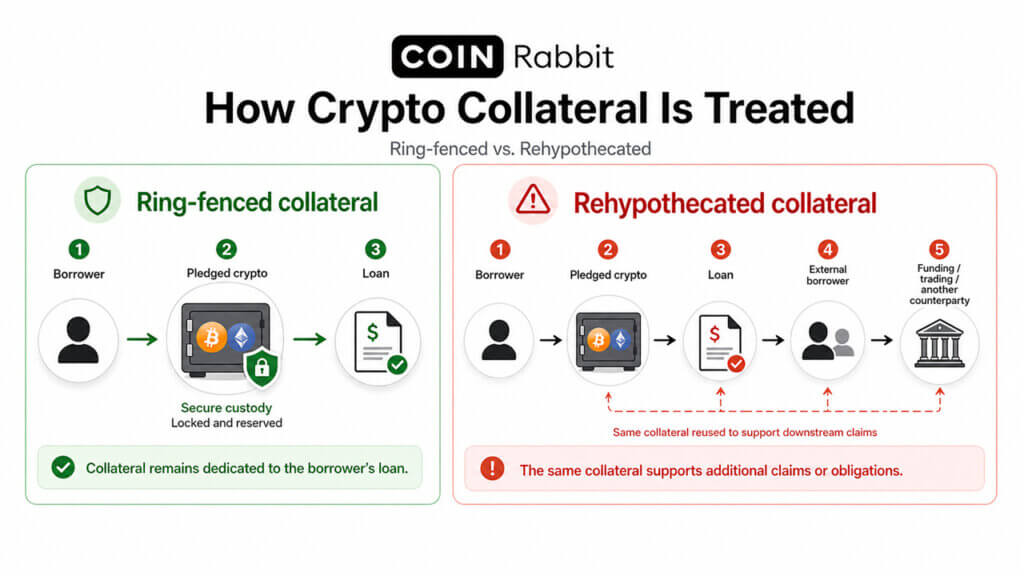

Most people start with the wrong question. They compare interest rates, loan terms, onboarding speed, and liquidation thresholds. Those matter, but they come second. The first question is simpler: after I deposit my collateral, does it stay dedicated to my position, or does it start moving through the lender’s balance sheet?

That distinction is what separates visible risk from hidden risk. If collateral stays ring-fenced, the borrower still faces market volatility, financing cost, and liquidation rules. If collateral is reused, the borrower now also depends on the lender’s counterparties, treasury decisions, and crisis management. The asset may look like “my collateral” on the dashboard, but economically it is no longer only yours to worry about.

This is why no-rehypothecation resonates so strongly with serious holders. This is a more direct promise about where the risk stops. When people know their assets are sitting intact instead of being passed to a trading desk, affiliate, or external borrower, trust becomes easier to justify because the structure is easier to understand.

Market context

Rehypothecation is common enough to require attention

The Buy, Borrow, Die framework only works if the “borrow” step is built on trust. The holder wants liquidity without selling a long-term asset, but that preference does not justify handing collateral to any platform that offers a loan. A strategy designed to preserve capital can be undermined if the collateral becomes part of another firm’s risk engine.

This is why collateral treatment belongs near the beginning of the due-diligence process. Interest rate, loan-to-value ratio, funding speed, and supported assets all matter, but they sit downstream from a more fundamental issue: whether the asset remains dedicated to the borrower’s position or becomes available for reuse by the lender.

A ring-fenced model does not remove market risk. The borrower still has to monitor collateral value, interest cost, and liquidation thresholds. It does, however, make the structure easier to understand. If the asset is not being passed to a trading desk, affiliate, external borrower, or funding partner, the user has a clearer view of where the collateral is and what has to happen for it to be returned.

| Model | What happens to the asset | Main user risk |

|---|---|---|

| Ring-fenced / fully reserved | Asset is held for the loan or custody relationship | Market risk, operational risk, liquidation rules |

| Rehypothecated / reused | Asset is re-lent, re-pledged, or deployed elsewhere | Counterparty chain risk, withdrawal dependency, solvency stress |

| Commingled / misused | Asset is mixed with firm or affiliate risk | Asset shortfall, legal ambiguity, insolvency disputes |

Plain English

What rehypothecation is, and how it works

Rehypothecation should not be treated as an obscure or outdated corner of finance. It is part of the broader crypto lending landscape. In traditional markets, collateral reuse has long supported securities financing, repo markets, prime brokerage, and other balance-sheet activities. The FSB’s framing is deliberately balanced: collateral reuse can make markets more liquid and reduce transaction costs, but it can also increase leverage and connect firms in ways that are difficult to see during calm periods.

Crypto lending has inherited the same tradeoff. Some platforms explicitly use collateral reuse as part of their economics, often to reduce borrowing costs or support yield generation. Ledn, for example, describes standard Bitcoin or ETH-backed loans as a structure in which collateral is rehypothecated to lower client interest rates, while its custodied loan option is designed so collateral cannot be rehypothecated. That distinction shows the modern landscape clearly: rehypothecation is not always hidden, but users need to know which model they are entering.

The practical implication is not that every platform reuses collateral, or that all reuse is automatically fraudulent. The point is more disciplined: borrowers should assume nothing. A platform’s category label, brand size, or advertised rate does not answer the asset-treatment question. Only the product terms, custody model, disclosures, and operating controls can do that.

Structural risk

Why collateral reuse can turn liquidity into dependency

Collateral reuse can look efficient in stable conditions. A crypto lender can use pledged assets to source liquidity, support additional lending, or lower costs for borrowers. In a rising market, those benefits are easy to market because asset values are increasing and counterparties are usually willing to extend credit.

The weakness appears when market direction changes. Falling collateral values, rising withdrawal demand, counterparty stress, and reduced market liquidity can arrive together. A platform that has reused customer assets may then need multiple external relationships to perform at the same time. If one counterparty fails, the user’s supposedly simple loan can become entangled in a wider liquidity problem.

This is why collateral reuse has played such a damaging role in past crypto failures. It does not need to be the sole cause of a collapse to make the outcome worse. By creating hidden leverage and dependency chains, rehypothecation can turn a liquidity product into a solvency exposure.

Failure pattern

What Celsius, BlockFi, and FTX taught the market

The purpose of bringing up Celsius, BlockFi, and FTX is not to turn this guide into a platform-by-platform postmortem. The more useful lesson is structural. Each case showed what can happen when customer assets are not protected by a simple, transparent, limited-use model.

Celsius made asset-use opacity impossible to ignore. Reuters reported that the court-ordered examiner found Celsius gathered retail crypto deposits and invested them in the wholesale crypto market, used new customer deposits to fund customer withdrawal requests in June 2022, and concluded that the business sold to customers differed from the business the company actually operated. For borrowers and depositors, the lesson is direct: if users cannot understand how assets are being used, they cannot evaluate the real risk.

BlockFi showed how deployed assets and counterparty concentration can transmit losses. In its 2022 settlement materials, the SEC said BlockFi generated interest for its interest accounts by deploying assets through institutional and corporate lending, among other activities. The SEC also stated that BlockFi’s terms allowed it to pledge, repledge, hypothecate, rehypothecate, sell, lend, or otherwise transfer investor crypto, and that BlockFi pooled, commingled, and rehypothecated BIA assets with other assets.

Later, Reuters reported that BlockFi’s bankruptcy filing cited substantial exposure to FTX, including loans to Alameda and assets trapped on FTX.

FTX was not a rehypothecation case in the narrow crypto lending sense, but it remains relevant because it changed how the market thinks about custody and segregation.

Reuters reported that Sam Bankman-Fried was sentenced to 25 years after a judge found FTX customers lost $8 billion, and that former associates testified he directed them to use FTX customer funds to cover losses at Alameda Research. The lending lesson is adjacent but essential: when customer assets become available to a corporate risk pool, users are exposed before liquidation thresholds ever come into view.

These failures differed in mechanics, but they point to the same diligence question. Are customer assets held for the customer’s purpose, or can they be absorbed into someone else’s strategy?

Simpler trust

Why intact, ring-fenced collateral changes the trust equation

The trust value of ring-fenced collateral is straightforward. The user wants confidence that assets dedicated to a loan remain intact for that loan, rather than being passed along, pledged elsewhere, or used to support the lender’s own obligations. When that condition is clear, the borrower can focus on visible risks: market movement, loan-to-value ratio, interest cost, and repayment timing.

This matters emotionally as well as financially. Long-term holders often borrow because they do not want to break the core position. They feel safer when the path back to the asset is simple: manage the loan, repay it, and retrieve the collateral according to the platform’s terms. Hidden reuse complicates that path because the return of the asset may depend on entities outside the borrower’s control.

Regulatory guidance after the 2022 failures moved in the same direction. Updated 2025 guidance from the New York State Department of Financial Services emphasizes segregation, separate accounting, limited use of customer virtual currency, and clear disclosure. It states that custodians should treat customer virtual currency as belonging solely to customers and should not employ it for the custodian’s own use.

Due diligence

How to evaluate a crypto lender before you deposit

A polished homepage can explain the desired user experience. The legal terms and custody disclosures explain what happens when markets move, withdrawals rise, or the platform faces stress. Serious borrowers should therefore begin with asset treatment before comparing rates.

The core diligence question is whether the platform can use, lend, pledge, re-pledge, or otherwise deploy customer assets. If it can, the borrower needs to understand the full counterparty chain, the purpose of reuse, whether assets are segregated by product, and what happens if a downstream borrower or affiliate fails. If it cannot, the structure is easier to analyze, though market and liquidation risk remain.

The minimum checklist

Before posting collateral, a serious borrower should be able to answer the following questions:

- Can the platform reuse, lend, pledge, or otherwise deploy collateral?

- Are customer assets segregated from corporate and affiliate assets?

- Does the platform disclose how assets are treated in insolvency?

- Are liquidation thresholds, alerts, and collateral top-up tools clear?

- Who controls storage, and does the platform use cold storage or multisig controls?

- Are withdrawal and collateral-return mechanics clear for both open loans and repaid loans?

- Is support available when market conditions change quickly?

Separate platform risk from market risk

Platform risk concerns what the company can do with customer assets, how it manages custody, and whether hidden counterparties sit behind the user’s position. Market risk concerns price movement, loan-to-value ratio, interest, margin calls, and liquidation.

Borrowers often combine these two risks because both can lead to losses. Separating them leads to better decisions. A no-rehypothecation model may reduce hidden asset-use risk, but it does not remove the need to monitor collateral value.

Brand bridge

Where CoinRabbit fits

CoinRabbit is as an example of the more conservative side of the lending landscape. The relevant question is not only whether a platform is fast, flexible, or broad in asset coverage. It is whether the collateral model avoids the hidden reuse dynamics that made past failures more destructive.

CoinRabbit’s loans page states that collateral is fully secured and never reused under a strict no-rehypothecation rule. The same page presents the platform as fully reserved, says collateral is stored in cold wallets with multisig access, and notes that the platform’s comparison table lists rehypothecation as “No” for CoinRabbit. Its homepage also describes user capital as “fully reserved, never reused” and frames the company as a crypto asset management platform focused on security, speed, and confidence.

That message supports the Buy, Borrow, Die narrative because the strategy depends on confidence in the asset’s return path. A holder borrowing against BTC, XRP, ETH, or another supported asset is not simply buying temporary liquidity. The holder is trying to preserve long-term exposure while using capital more flexibly. That goal is easier to justify when collateral is not passed onward to generate yield for the platform.

CoinRabbit also emphasizes practical controls for the risks that remain: real-time email or SMS alerts when a loan enters a risk zone, Auto Increase for collateral top-ups, and 24/7 human support. These controls do not eliminate volatility, but they support active management, which is the appropriate posture for any crypto-backed loan.

The right message is not perfect safety. It is a narrower and more credible claim: fewer hidden asset-use risks, a clearer collateral model, and tools for managing the market risks that still exist. That distinction matters for institutional readers, large holders, and anyone using borrowing as part of a long-term capital-preservation strategy.

No-rehypothecation matters because it keeps the risk map simple. Borrowers still need to manage price volatility and liquidation risk, but their collateral should not also depend on a hidden chain of counterparties, affiliates, or balance-sheet decisions they never agreed to underwrite.

On the day-to-day user side, the platform also highlights practical controls that matter once volatility shows up: real-time email or SMS alerts when a loan enters a risk zone, an Auto Increase option for collateral top-ups, and 24/7 human support. The overall pitch is coherent: minimize hidden asset-use risk first, then help users manage visible market risk second.

That does not make the product risk-free. CoinRabbit’s say collateral becomes a Deposit when transferred in, that equivalent digital assets are returned after repayment, and that liquidation can happen without borrower approval once thresholds are reached. The right message is not “perfect safety.” It is “fewer hidden asset-use risks, plus tools to manage the risks that remain.”

Fast answers

FAQ

What is rehypothecation in crypto lending?

Rehypothecation occurs when a platform uses collateral or customer assets after receiving them, rather than holding them solely for the original customer relationship. In a loan context, that can mean lending collateral onward, pledging it elsewhere, or using it to support the platform’s own financing. The Financial Stability Board defines re-hypothecation as a financial intermediary’s use of client assets.

Is rehypothecation widely used?

Yes, rehypothecation and collateral reuse are established practices in traditional finance, and crypto lending has adopted versions of the same model. Some modern crypto lending platforms explicitly offer rehypothecated and non-rehypothecated structures as separate product choices. Borrowers should verify the model rather than assume all platforms handle collateral the same way.

Why can rehypothecation become dangerous?

Rehypothecation can add leverage and dependency chains to a loan that appears simple from the user’s perspective. If the lender’s counterparty fails, or if several counterparties need liquidity at the same time, customer access to assets can be delayed or impaired. The FSB has warned that collateral reuse may increase interconnectedness and create operational impediments during insolvency.

Is FTX an example of rehypothecation?

Not in the narrow lending sense. FTX is better understood as a customer-asset misuse and commingling case. It still belongs in this discussion because it showed why segregation, limited use, and clear asset treatment are essential whenever a platform controls user assets.

Why does no-rehypothecation matter if collateral can still be liquidated?

Liquidation and rehypothecation are different risks. Liquidation comes from market movement against a loan. Rehypothecation comes from the platform’s use of assets behind the scenes. A no-rehypothecation structure may reduce hidden counterparty exposure, but the borrower still needs to manage loan-to-value ratio, interest, and collateral buffers.

Can I withdraw loan collateral whenever I want?

Loan collateral is not the same as an unencumbered wallet balance. Collateral secures the loan until repayment or release conditions are met. CoinRabbit’s loans page says collateral is returned after repayment and immediately available to withdraw, while its Terms state that equivalent digital assets are transferred back after full repayment.

What should I check before depositing collateral?

Start with whether the platform can reuse, lend, pledge, or otherwise deploy customer assets. Then review segregation, custody, sub-custody, liquidation thresholds, collateral-return mechanics, and support availability. Updated NYDFS custody guidance emphasizes similar concepts: segregation, limited use, and clear customer disclosure.

How does this connect to Buy, Borrow, Die?

Buy, Borrow, Die depends on preserving the long-term asset while accessing liquidity. Rehypothecation matters because it can weaken the borrower’s confidence that the asset remains dedicated to their position. A no-rehypothecation model makes the “borrow” step cleaner by reducing hidden asset-use risk.

Unlock and manage liquidity without selling

Don’t sell. Preserve your capital through a more strategic, portfolio-focused approach.