Part 1 Advanced The Market Maker’s Exchange Checklist (Liquidity, Latency, and Risk Controls) Market makers and HFT desks: evaluate exchanges on execution quality, liquidity, latency, fees, margin, and security — with a WhiteBIT walkthrough. Open guide

Part 1 Advanced The Market Maker’s Exchange Checklist (Liquidity, Latency, and Risk Controls) Market makers and HFT desks: evaluate exchanges on execution quality, liquidity, latency, fees, margin, and security — with a WhiteBIT walkthrough. Open guide

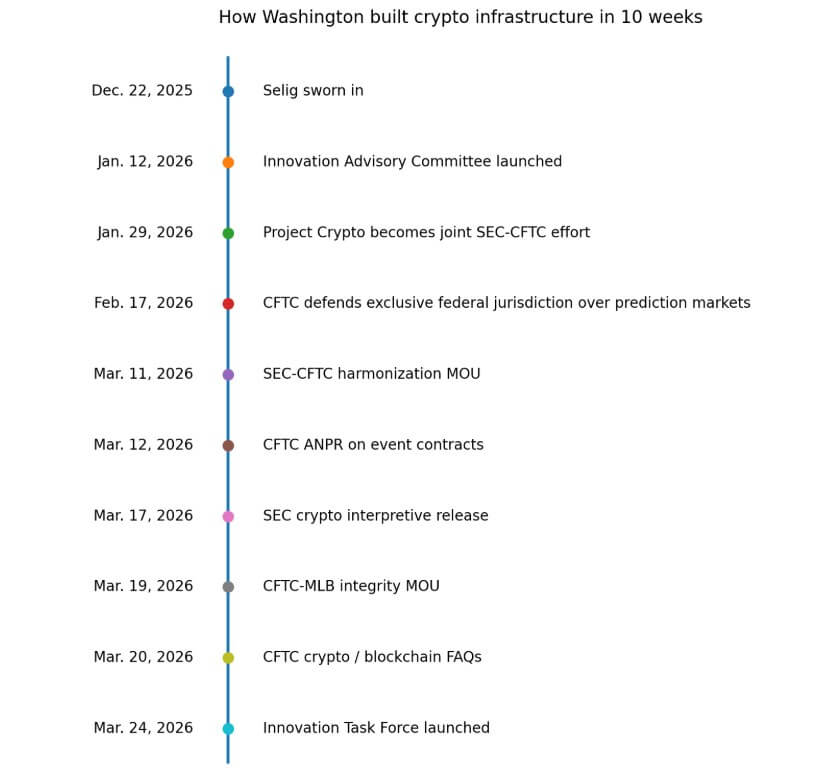

On Mar. 24, the Commodity Futures Trading Commission (CFTC) launched its Innovation Task Force, tasked with developing frameworks for crypto assets, blockchain technologies, AI systems, and prediction markets.

Alongside everything else Washington has done in the past three months, it reads as the moment when a provisional, enforcement-heavy posture toward crypto began to harden into something more permanent.

The asset class became too financially embedded, too politically contentious, and too jurisdictionally tangled for the federal government to keep handling on a case-by-case basis.

A timeline that argues for itself

The pace since Chairman Michael Selig's swearing-in in December 2025 is the clearest evidence available.

On Jan. 12, the CFTC launched an Innovation Advisory Committee with 35 members, including Coinbase, Uniswap, Ripple, Kraken, Gemini, Chainlink, Nasdaq, CME, Kalshi, and Polymarket.

That roster captures where crypto now sits: interwoven with the largest incumbent exchanges and clearinghouses in the US market structure.

By Jan. 29, Project Crypto had become a joint SEC-CFTC undertaking. On Feb. 17, the CFTC filed to defend its exclusive federal jurisdiction over prediction markets against state challenges.

On Mar. 11, the two agencies signed a harmonization MOU, establishing a public initiative in which staff coordinate to eliminate duplicative requirements, clarify jurisdictional boundaries, and open streamlined pathways for new products.

On Mar. 12, the CFTC opened an advance notice of proposed rulemaking on event contracts.

On Mar. 17, the SEC issued a crypto interpretive release that formalizes a taxonomy covering digital commodities, digital collectibles, digital tools, stablecoins, and digital securities, explicitly framing it as a bridge while Congress continues working on market-structure legislation.

On Mar. 19, the CFTC signed a first-of-its-kind MOU with Major League Baseball to coordinate on the integrity of prediction markets. On Mar. 20, the staff published FAQs on crypto and blockchain. On Mar. 24, the task force launched.

Regulation by institution

Advisory committees, formal MOUs, harmonization portals soliciting written industry input, joint interpretive releases, rulemaking dockets, and dedicated task forces leave a lasting infrastructure.

The CFTC now has all of them, and the SEC is operating in parallel. The harmonization initiative is an operational channel where firms can request joint meetings and submit written input for staff review.

The SEC's Mar. 17 interpretation draws explicit taxonomic lines, determining which products fall under securities law, which fall under commodities law, and which occupy a newly defined middle ground.

The CFTC's no-action position on Phantom, a self-custodial wallet provider, signals that regulators are now considering how on-chain software interacts with registered derivatives markets.

Congress has not delivered comprehensive market structure legislation.

Senate talks hit an impasse in early March, and the Banking Committee has not cleared a bill. Meanwhile, agencies are assembling a de facto operating system from the tools at their disposal: interpretations, staff guidance, MOUs, rulemaking notices, and standing interagency processes.

These are the base of a scaffolding that is harder to dismantle than a single guidance document.

| Tool | Recent example | Why it matters |

|---|---|---|

| Advisory committee | Innovation Advisory Committee launched on Jan. 12 with 35 members from crypto firms, exchanges, and market infrastructure groups | Creates a standing channel for industry input and signals that crypto is being treated as a permanent policy area rather than a one-off enforcement problem |

| Interagency agreement | SEC-CFTC harmonization MOU signed on Mar. 11 | Builds a formal process for reducing duplicative requirements, coordinating staff, and clarifying jurisdictional boundaries |

| Harmonization portal | Public SEC-CFTC initiative allowing firms to request joint meetings and submit written input | Turns coordination into an operational process firms can actually use, not just a press-release commitment |

| Interpretive guidance | SEC crypto interpretive release on Mar. 17 | Draws taxonomic lines across digital commodities, digital securities, stablecoins, collectibles, and other crypto assets, shaping how products are classified under federal law |

| Staff guidance | CFTC crypto and blockchain FAQs published on Mar. 20 | Provides practical direction that helps firms navigate live compliance questions even without a full statute |

| Staff relief / no-action | CFTC no-action position involving Phantom | Shows regulators are now addressing how self-custodial wallets and on-chain software connect to registered derivatives markets |

| Rulemaking docket | CFTC ANPR on event contracts opened on Mar. 12 | Moves prediction markets from ad hoc treatment into formal notice-and-comment rulemaking |

| Jurisdictional assertion | CFTC filing defending exclusive federal jurisdiction over prediction markets on Feb. 17 | Signals that the agency is actively trying to define and defend the perimeter of federal authority in a fast-growing market |

| Integrity partnership | CFTC-MLB MOU signed on Mar. 19 | Shows prediction markets have become mainstream enough to implicate sports-league integrity monitoring and broader public scrutiny |

| Dedicated task force | Innovation Task Force launched on Mar. 24 | Assigns ongoing staff capacity to crypto, blockchain, AI, and prediction markets, making the regulatory buildout harder to unwind |

Where crypto stops looking abstract

Prediction markets are where the regulatory reckoning becomes impossible to treat as a niche technical debate.

Since the 2024 US election, the sector has expanded rapidly, drawing in contracts tied to sports outcomes, political events, and economic data.

The CFTC's exclusive-jurisdiction filing, its ANPR, and its MLB integrity MOU show one agency trying to hold the perimeter of a fast-growing market.

On Mar. 24, Senators Adam Schiff and John Curtis introduced the bipartisan Prediction Markets are Gambling Act, targeting sports-style contracts on prediction market platforms.

The bill's existence confirms the political pressure: Washington is debating what kind of federal attention prediction markets deserve.

That same pressure applies to crypto more broadly, as the industry now touches derivatives plumbing, tokenized collateral, wallet access to regulated venues, sports integrity monitoring, election forecasting, and federal-state jurisdictional lines.

At that scale, ad hoc regulation becomes untenable because the complexity of the asset class outgrew the tools designed to police it from a distance.

The infrastructure outlasts the moment

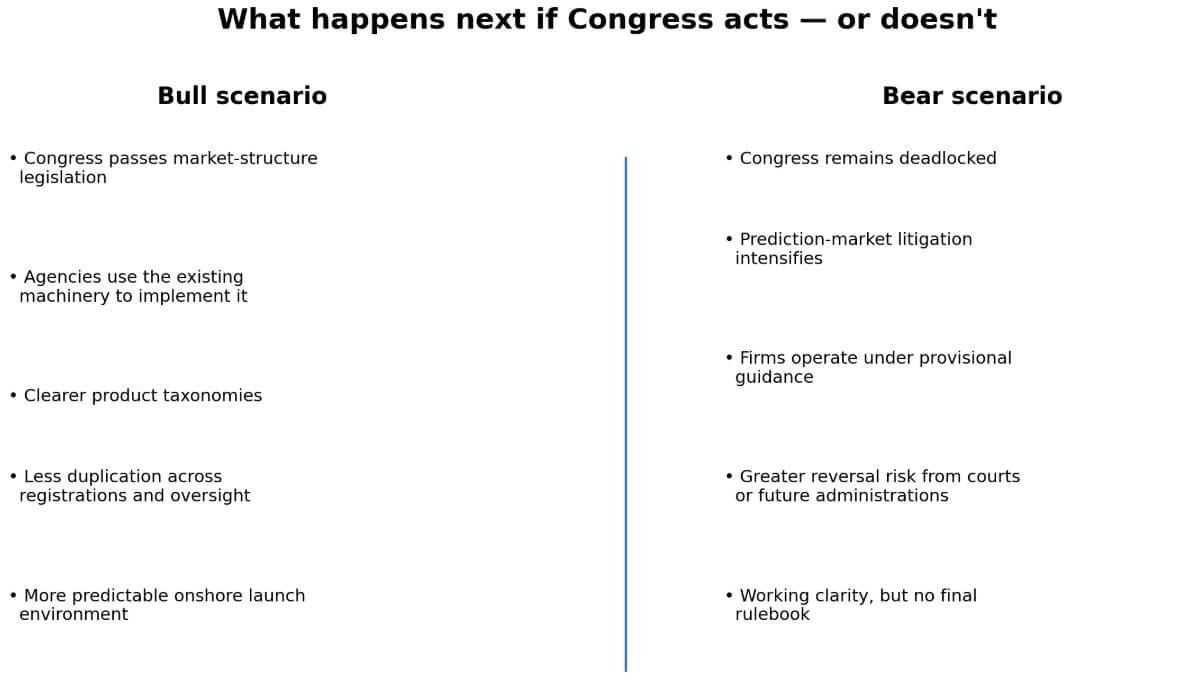

In the bull scenario, Congress eventually passes market structure legislation, and agencies use the existing harmonization machinery to implement it efficiently.

The task force, the MOU, the interpretive releases, and the advisory committee become the scaffolding for a cleaner, more durable US crypto framework. The new structure reduces duplication in registrations, provides clearer product taxonomies, and creates a more predictable onshore launch environment for new financial products.

In the bear case, Congress stays deadlocked, litigation over prediction markets intensifies, and guidance from the SEC and CFTC is still partly provisional.

Firms operate under a working clarity that is not sufficient to serve as a final rulebook. The machinery Washington built runs on interpretive authority, making it more vulnerable to reversal by future administrations or unfavorable court decisions.

Neither scenario changes the observation that federal agencies are reorganizing around crypto regardless of what Congress does next. The structures built in the past weeks do not disappear when a rulemaking stalls or a bill fails a committee vote.

Crypto's growing presence in Washington is measured in the formation of committees, the signing of interagency agreements, the opening of rulemaking dockets, and the deployment of staff to work on nothing else.

That is what it looks like when a financial market crosses from a recurring compliance problem into a permanent feature of the regulatory landscape.