The Federal Reserve, the central banking system of the United States, currently maintains a keen focus on inflation, aiming to stabilize it to ensure the health and vitality of the U.S. economy. For several decades, their primary objective has been to keep inflation rates steady, with a target set at 2%.

This target is not arbitrary; it’s a carefully considered figure that aims to strike a balance between promoting maximum employment and ensuring stable prices for consumers.

Understanding inflation is paramount for understanding the economy, as it directly impacts the purchasing power of consumers and affects the rate of return on investments. Inflation also influences central bank decisions, including interest rate adjustments, which in turn can have broad implications for the economy at large, affecting everything from personal loans to mortgages.

In this report, CryptoSlate dives deep into the topic of inflation, its historical context, and current implications to present an argument for why the Federal Reserve should consider increasing its inflation target.

Historical context

Established in 1913, the Federal Reserve’s primary objectives have evolved over time, but its commitment to price stability and economic growth has remained constant. In the early years of its existence, the Fed grappled with the challenges of the Great Depression and the post-war economic landscape, leading it to continually refine its approach to monetary policy.

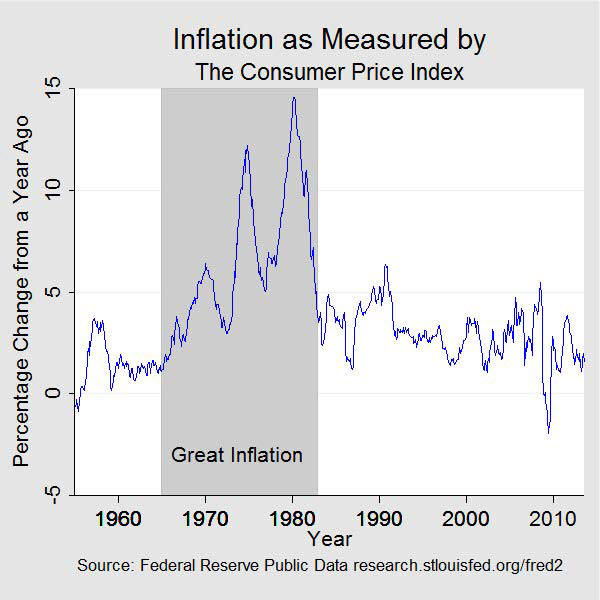

By the mid-20th century, the U.S. economy experienced periods of high inflation, notably during the 1970s.

It was during these tumultuous times that the Federal Reserve recognized the need to stabilize inflation and ensure it didn’t spiral out of control. The decision to stabilize inflation below 3% was influenced by the economic challenges of the era, including oil price shocks and global economic shifts. This move was seen as a way to provide a predictable economic environment for businesses and consumers alike.

However, it wasn’t until the 1990s that the Federal Reserve formally announced its decision to set an explicit inflation target at 2%. Several factors influenced this decision. Research and global economic trends suggested that a 2% target would strike the right balance between preventing deflation and allowing room for economic growth. Moreover, other major central banks, like the European Central Bank and the Bank of England, had adopted similar targets, further validating the 2% figure.

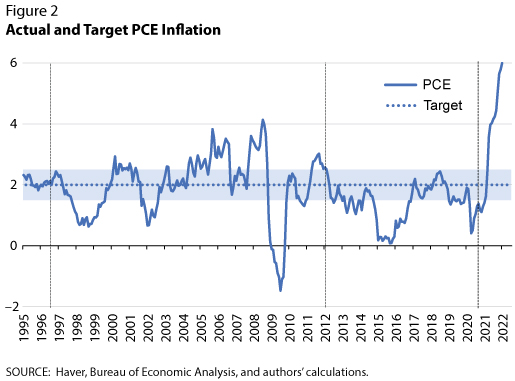

Graph showing the actual and target PCE inflation in the U.S. from 1995 to 2022 (Source: Federal Reserve)

Inflation targets are of paramount importance for several reasons. They provide a clear guideline for monetary policy decisions, ensuring transparency and predictability. For the market, a clear inflation target means businesses can make investment decisions with a degree of certainty about the future economic landscape. It also helps anchor public expectations about future inflation, which can influence wage negotiations, lending rates, and long-term contracts.

The case for a higher inflation target

Inflation targeting has been the subject of renewed debate among economists and policymakers. As the global economic landscape evolves, there’s a growing consensus that a higher inflation target could offer several advantages to the U.S. economy.

One of the primary benefits of a higher inflation target is its potential to provide a buffer against deep economic downturns. With a higher inflation rate, the Federal Reserve would have more room to reduce real interest rates, providing a more potent tool to combat recessions. In essence, a higher target could amplify the effectiveness of monetary policy during economic downturns, allowing for a quicker and more robust recovery.

A slightly higher inflation rate can make it easier for firms to implement nominal price increases. Concurrently, it can also make wage freezes more palatable. In situations where businesses face economic hardships, they could freeze wages instead of resorting to layoffs. Given that the real value of these wages would decrease with higher inflation, businesses could reduce labor costs without resorting to job cuts, thereby preserving employment levels.

A higher inflation target can also act as a catalyst for investment. When businesses anticipate future price increases, they are more likely to invest in capital now rather than later. This forward-looking behavior can lead to increased economic activity, fostering growth and innovation.

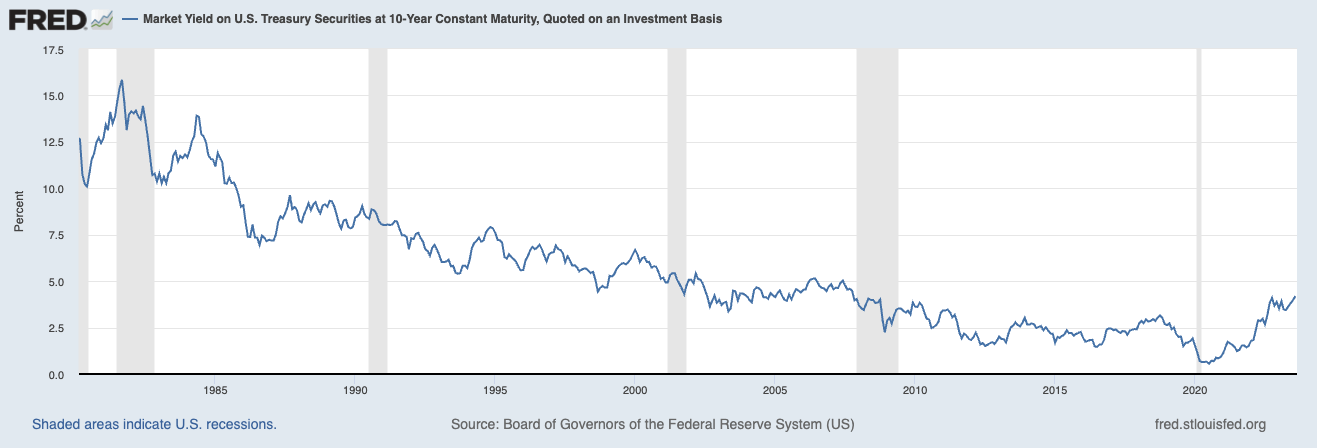

Furthermore, a review of economic indicators since the 1990s provides empirical support for a higher inflation target. Notably, the behavior of the 10-year Treasury yield, a benchmark for long-term interest rates, has shown a declining trend. This decline suggests that investors anticipate lower average inflation and lower real interest rates in the future.

Graph showing the 10-year Treasury yield from 1980 to 2023 (Source: Federal Reserve)

Additionally, the increasing frequency of zero interest rates, or the so-called “zero lower bound,” has constrained the Federal Reserve’s ability to combat recessions using traditional monetary policy tools. A higher inflation target could reduce the frequency with which the zero lower bound binds, thereby enhancing the efficacy of monetary policy.

Graph showing the Fed funds interest rate from 2003 to 2019 (Source: Mother Jones)

In light of these considerations, it becomes evident that while the 2% target served its purpose in a different economic era, the evolving macroeconomic environment necessitates a reevaluation. A higher inflation target, if adopted judiciously, could equip the Federal Reserve with enhanced tools to navigate the complexities of today’s economy.

Challenges of transitioning to a higher target

While the potential benefits of transitioning to a higher inflation target are compelling, the Federal Reserve and the broader U.S. economy would need to navigate a series of complexities and potential pitfalls.

One of the most significant achievements of the 2% target has been its success in anchoring inflation expectations. A sudden shift could unsettle these expectations, leading to uncertainty in financial markets, wage negotiations, and long-term contracts.

The Federal Reserve’s credibility is paramount, and a hasty or poorly communicated transition could erode trust in the institution. If market participants doubt the Fed’s commitment to the new target, it could lead to volatile financial conditions. A credible transition is essential to ensure all stakeholders understand, anticipate, and accept the change.

The economy could face several adverse outcomes without a smooth and credible transition. These might include capital flight, where investors move their assets to countries with more stable monetary policies, or a rapid increase in interest rates, which could stifle borrowing and investment. Additionally, if businesses and consumers believe that the Fed might revert to a lower target, they might delay spending and investment decisions, leading to economic stagnation.

The path forward

The journey towards a higher inflation target will be a hard one, requiring a clear roadmap and unwavering commitment from the Federal Reserve.

In the short term, the Federal Reserve’s primary focus should remain on taming inflation. The challenges posed by rising prices, especially in the wake of economic disruptions, cannot be ignored. Thus, a higher inflation target should be approached as a long-term strategic goal rather than a short-term tactical shift.

The first step in this journey is for the Fed to articulate clear motives for the shift. A well-defined goal will not only bolster the Fed’s credibility but also ensure that the transition is rooted in sound economic reasoning rather than short-term expedients.

With this in mind, a phased approach seems prudent. The Fed could aim to raise the inflation target from 2% to 3% by 2025. This gradual transition would allow markets, businesses, and consumers to adjust their expectations and behaviors accordingly. Post-2025, a period of observation and analysis would be essential. By 2030, the Federal Reserve should undertake a comprehensive review of its policies, assessing the impact of the higher target and determining the next steps. This iterative approach ensures that policy decisions are data-driven, responsive to the evolving economic landscape, and in the best interest of long-term economic stability and growth.

Conclusion

If executed with precision and clear communication, a hawkish pivot to a higher inflation target could offer several benefits. It could provide a more substantial buffer against economic downturns, promote proactive investment behaviors due to anticipated future price increases, and offer more tools to combat severe recessions. Such a shift could also foster a more dynamic economic environment, encouraging innovation and growth.

While the road to a higher inflation target is fraught with challenges, the potential benefits for the U.S. economy’s long-term health are significant. With careful planning, clear communication, and a commitment to data-driven decision-making, the Federal Reserve can chart a course that ensures both immediate stability and long-term prosperity.