The halving is a pivotal moment in Bitcoin’s lifecycle, primarily because it slashes the reward for mining new blocks in half, reducing the rate at which new coins are generated and released into circulation. This mechanism is a fundamental part of Bitcoin’s design, intended to control inflation and extend the distribution of new coins over a longer period, ultimately capping the supply at 21 million coins.

The halving affects miners’ rewards and has profound implications for the Bitcoin economy through its influence on supply and price. Historically, each halving has led to a flurry of activity and speculation about potential impacts on Bitcoin’s value and the mining ecosystem. This cyclical event is viewed by many as a catalyst for significant price movements and market behavior, making it a critical point of analysis for investors and analysts alike.

With Bitcoin’s fourth halving set to take place on April 20, it’s interesting to examine how the current state of the market compares to that during the previous three halvings — in 2012, 2016, and 2020. Each four-year cycle was characterized by unique economic environments, user engagement levels, mining technologies, and institutional involvement, all of which influenced Bitcoin’s behavior in distinct ways. Analyzing these historical contexts allows us valuable insights into potential trends and outcomes from the upcoming halving.

2012

In 2012, the Bitcoin network was still in its infancy. Despite being four years old, it still had a tiny user base and much less mainstream recognition. It lacked significant coverage in mainstream financial media and was often associated with the underground economy, particularly its use on platforms like the Silk Road.

The concept of a digital currency was still a novel idea, and Bitcoin had yet to experience the kind of speculative interest that would come in later years as its price increased.

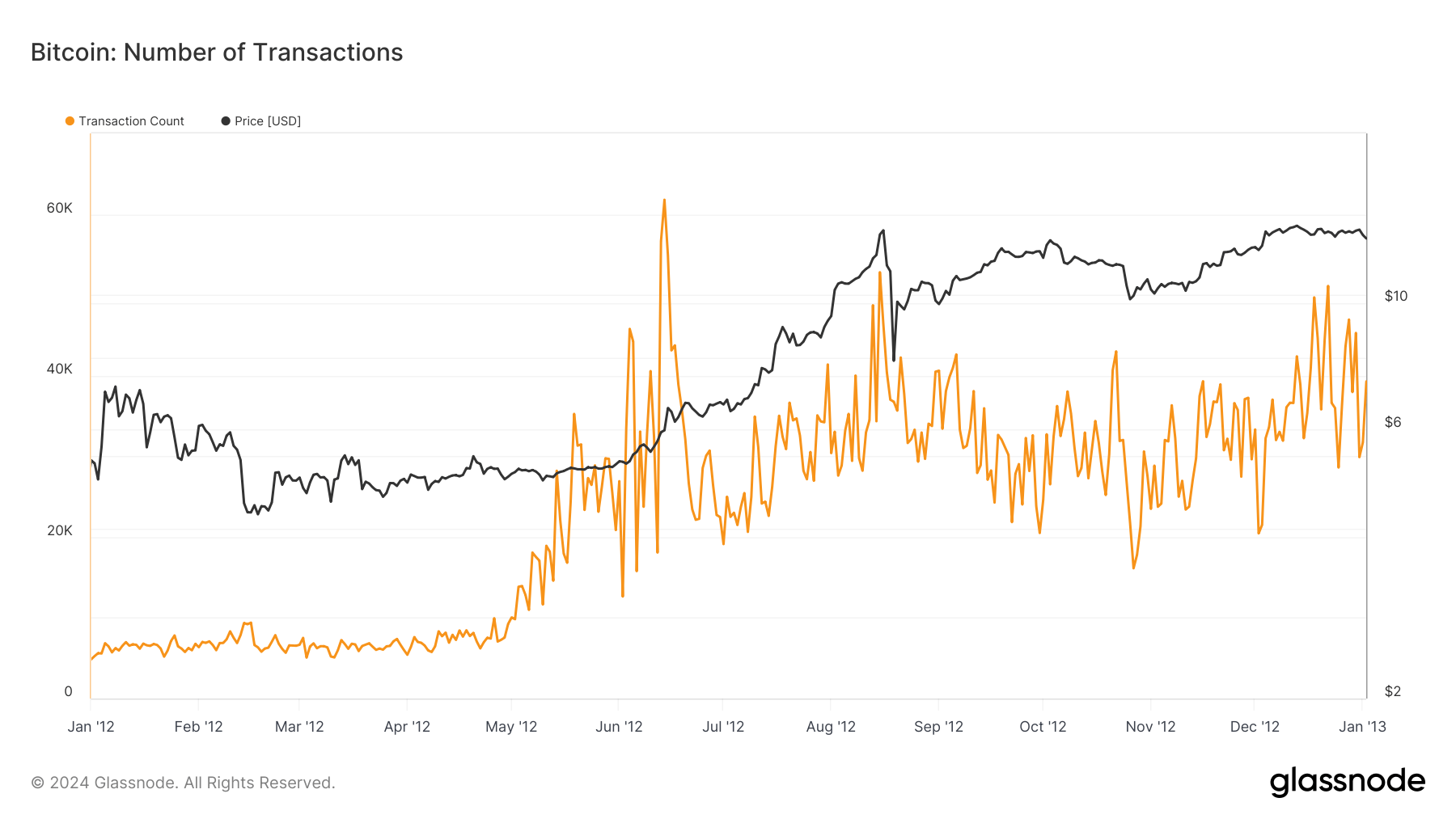

In the months preceding the first halving on Nov. 28, 2012, Bitcoin was primarily held by tech enthusiasts, libertarians, and a niche group of individuals interested in the potential of decentralized digital money. The average daily transaction number hovered between 20,000 and 40,000 — minimal compared to present-day figures.

Graph showing the number of transactions on the Bitcoin network from Jan. 1, 2012, to Jan. 1, 2013 (Source: Glassnode)

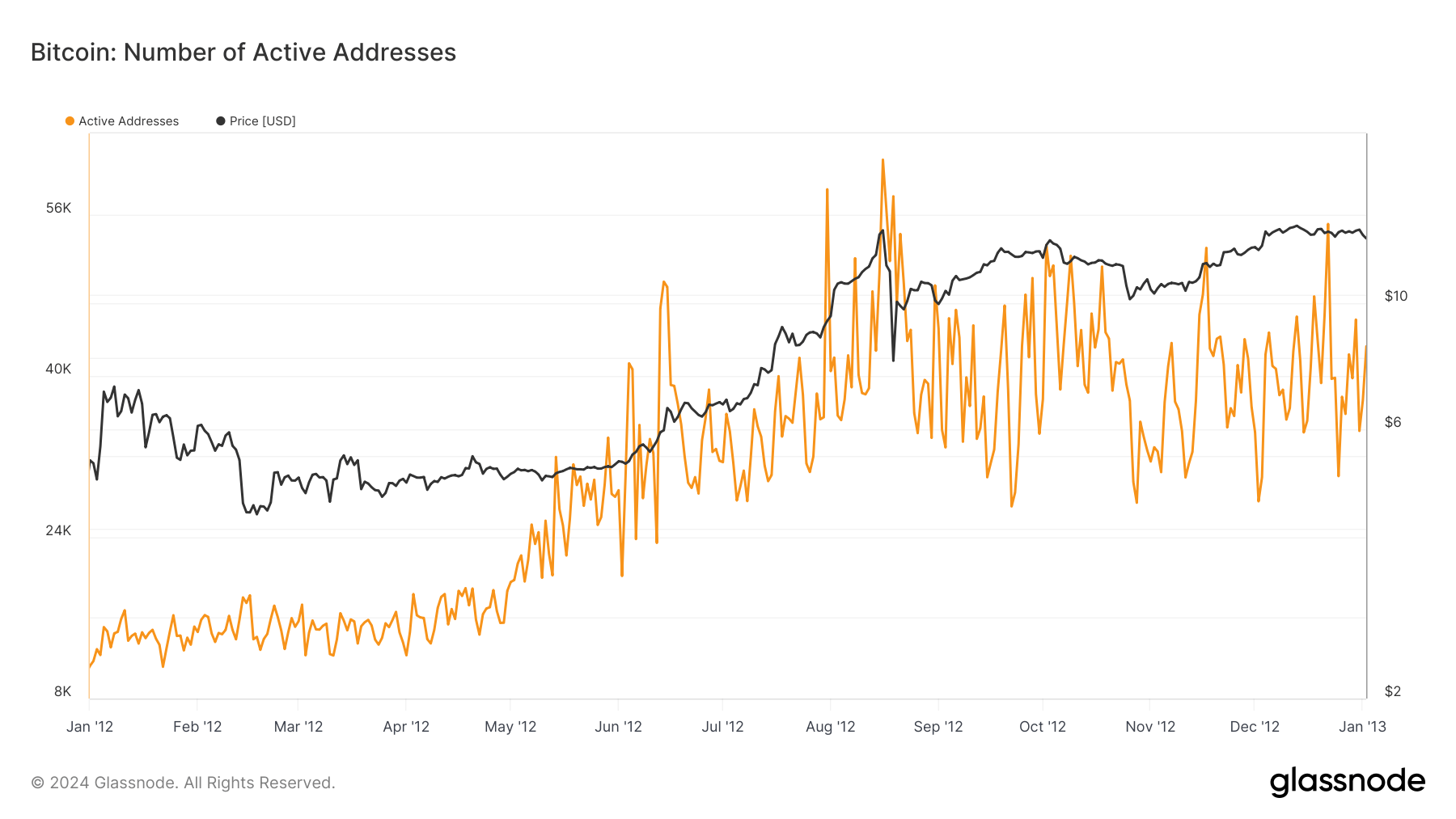

The value of Bitcoin transactions and the total number of active users were also relatively low. The small scale meant that the overall network demand was minimal, directly resulting in lower transaction fees.

Graph showing the number of active addresses on the Bitcoin network from Jan. 1, 2012, to Jan. 1, 2013 (Source: Glassnode)

The mining landscape before the 2012 halving was very different as well. It was not commercialized, with early miners using relatively basic equipment (i.e., personal computers, laptops, etc.) compared to the sophisticated ASIC hardware that became prevalent as Bitcoin’s hash rate increased.

Initially, miners used CPUs and soon moved to GPUs as they provided more hashing power. Some miners also used FPGA (Field-Programmable Gate Array) systems during the halving. These setups were significantly less powerful than later ASICs, which would start to dominate the mining landscape post-2012.

Given this context, the first halving had little immediate impact on the network for several reasons. Firstly, the demand for Bitcoin transactions during the first halving was not high enough to put upward pressure on fees despite the block reward getting slashed in half.

Although people knew the halving was a major deflationary event, the market had yet to grasp its implications fully and learn how to respond to them. It would take more time and more halvings for the pattern of post-halving price increases to become evident.

The relatively low cost and overhead of mining operations at the time meant that the reduction in block rewards did not dramatically alter the profitability of mining for the average participant, allowing them to continue despite reduced rewards.

2016

By 2016, the crypto landscape had evolved significantly from the relatively obscure and technically niche environment of 2012. The second halving, which occurred on July 9, 2016, was set against a backdrop of more sophisticated mining technology, a growing ecosystem of business and services (i.e., exchanges) built around cryptocurrencies, and a generally higher interest in Bitcoin.

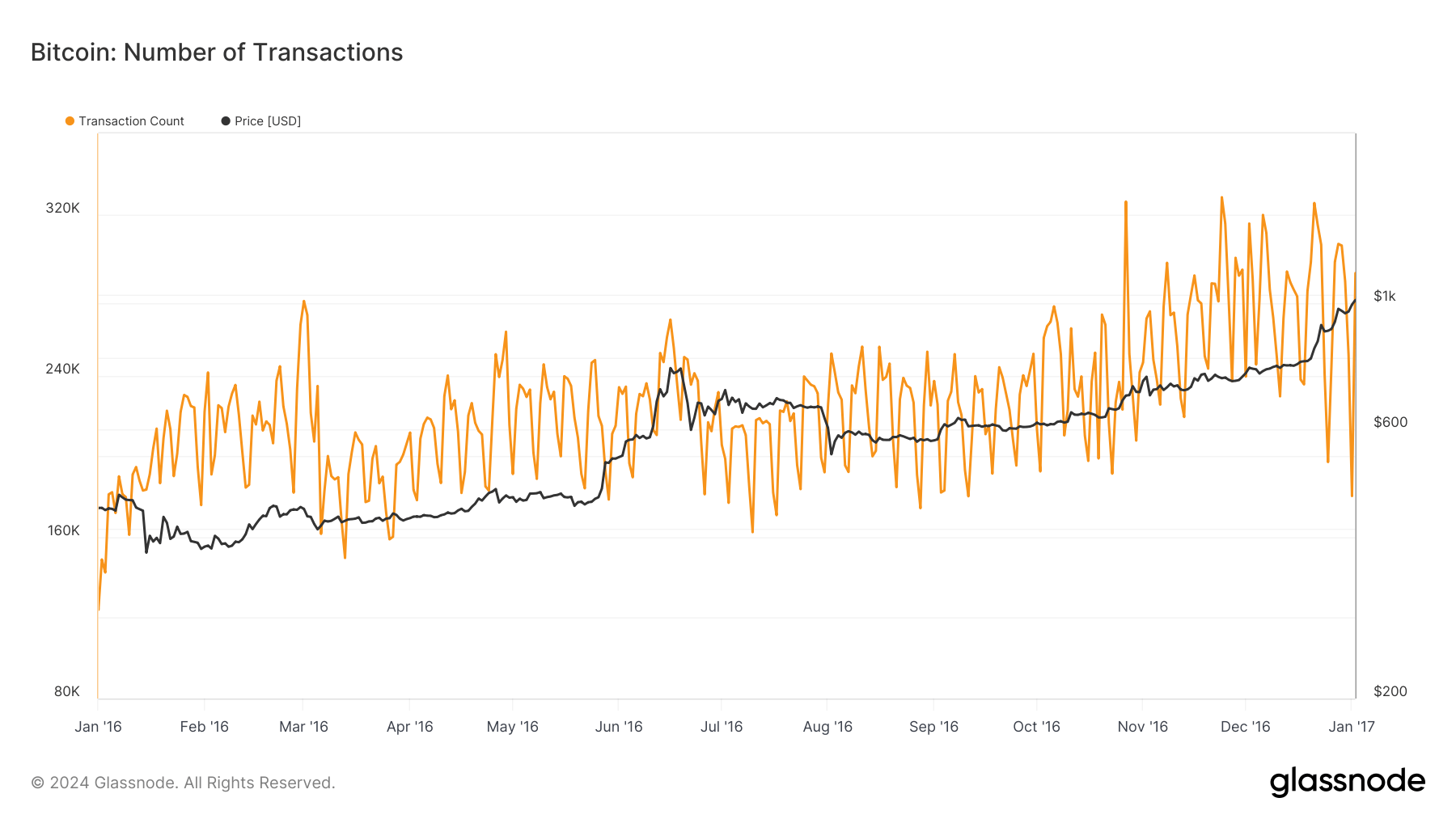

By 2016, the number of daily transactions on the Bitcoin network increased significantly, frequently exceeding 200,000 daily. This growth indicated Bitcoin’s growing acceptance as a medium of exchange and speculative investment.

Graph showing the number of daily transactions on the Bitcoin network from Jan. 1, 2016, to Jan. 1, 2017 (Source: Glassnode)

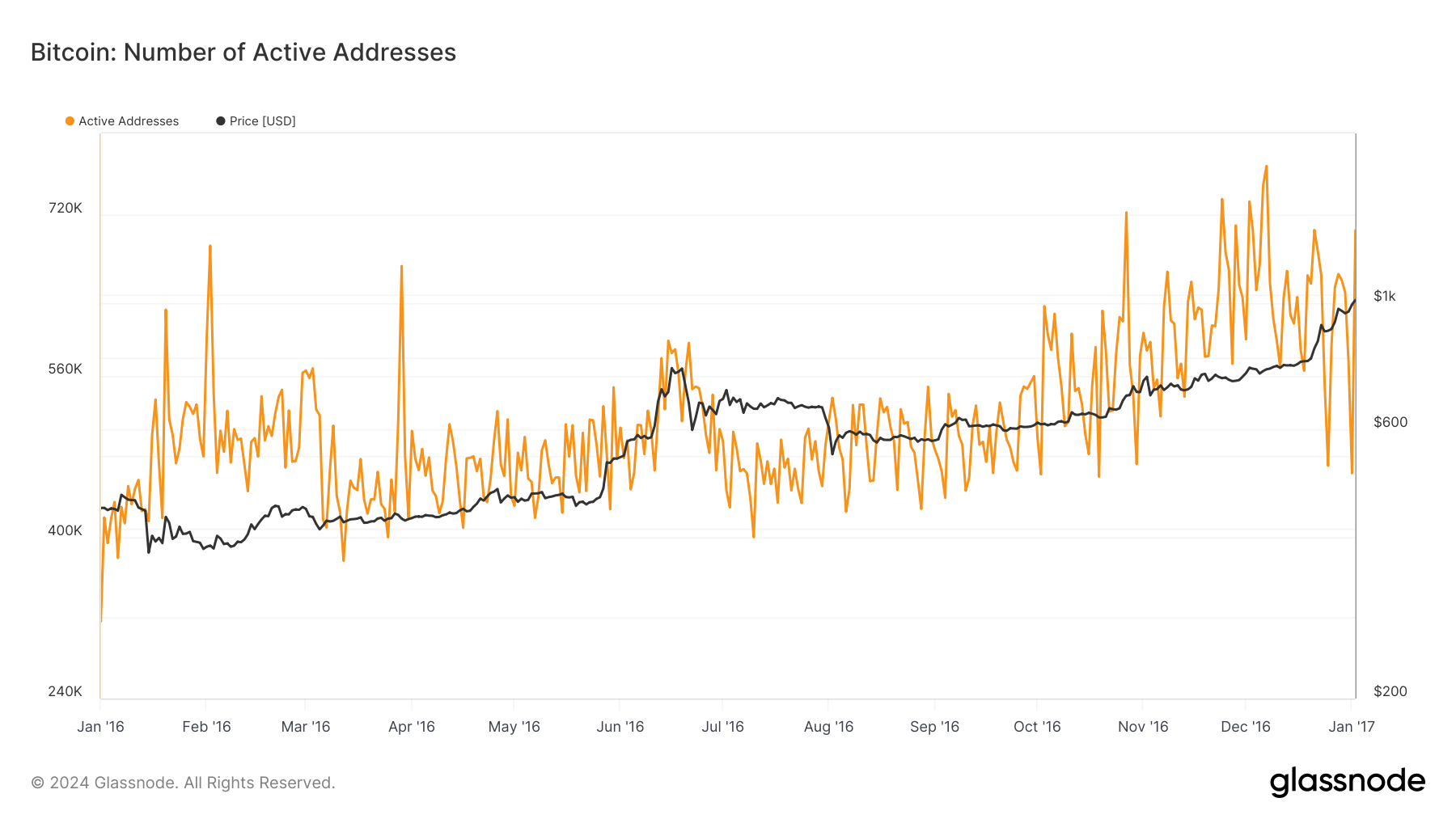

The user base expanded beyond tech enthusiasts to include more mainstream users, including investors and people from countries with unstable currencies, who saw Bitcoin as a store of value or an alternative to traditional banking.

Graph showing the number of active addresses on the Bitcoin network from Jan. 1, 2016, to Jan. 1, 2017 (Source: Glassnode)

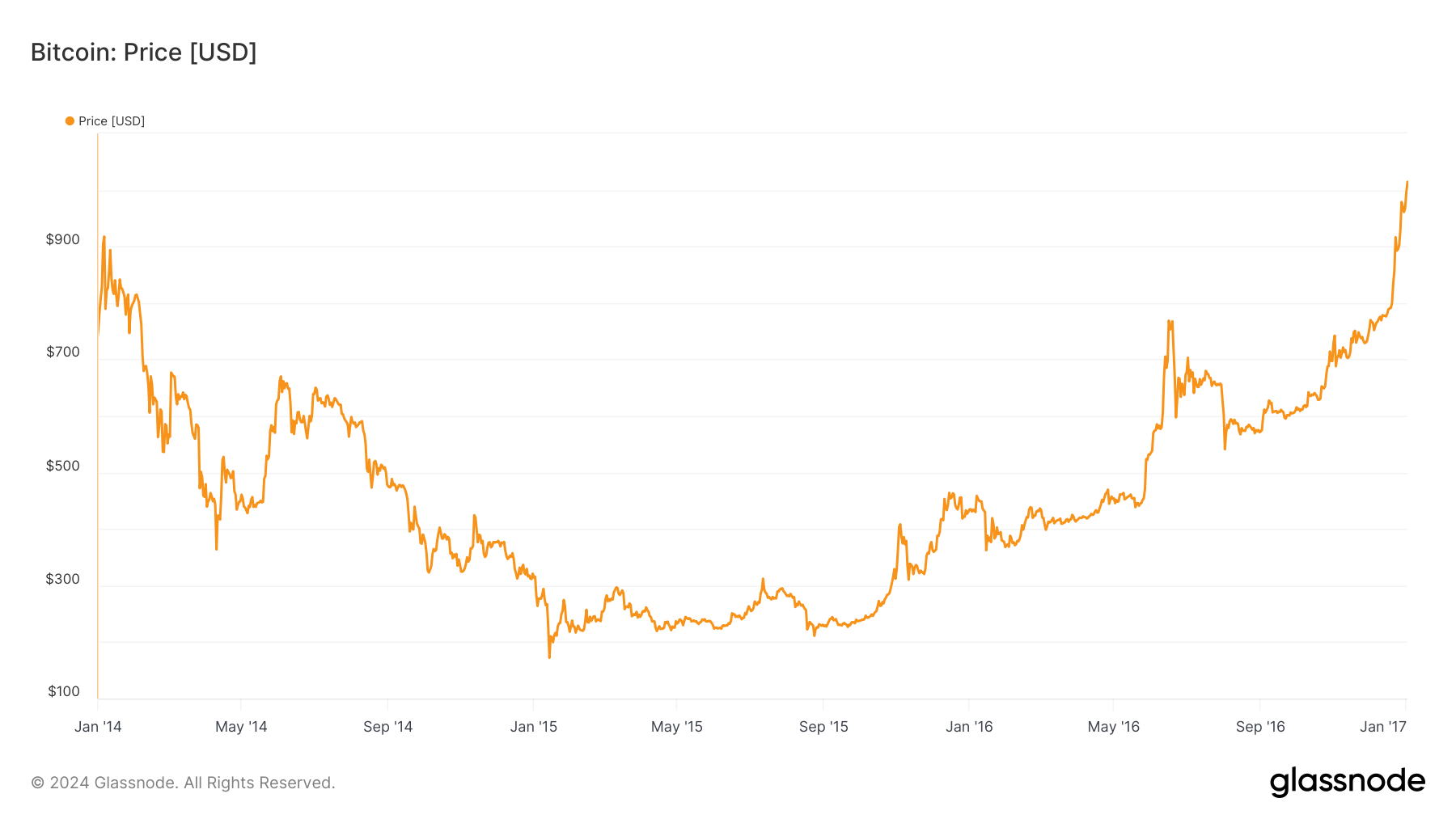

Bitcoin’s price had seen significant spikes and falls by this point, going through two distinct bull cycles. This period included the recovery after the collapse of Mt. Gox, which significantly damaged Bitcoin’s reputation and price in 2014.

Graph showing Bitcoin’s price from Jan. 1, 2014, to Jan. 1, 2017 (Source: Glassnode)

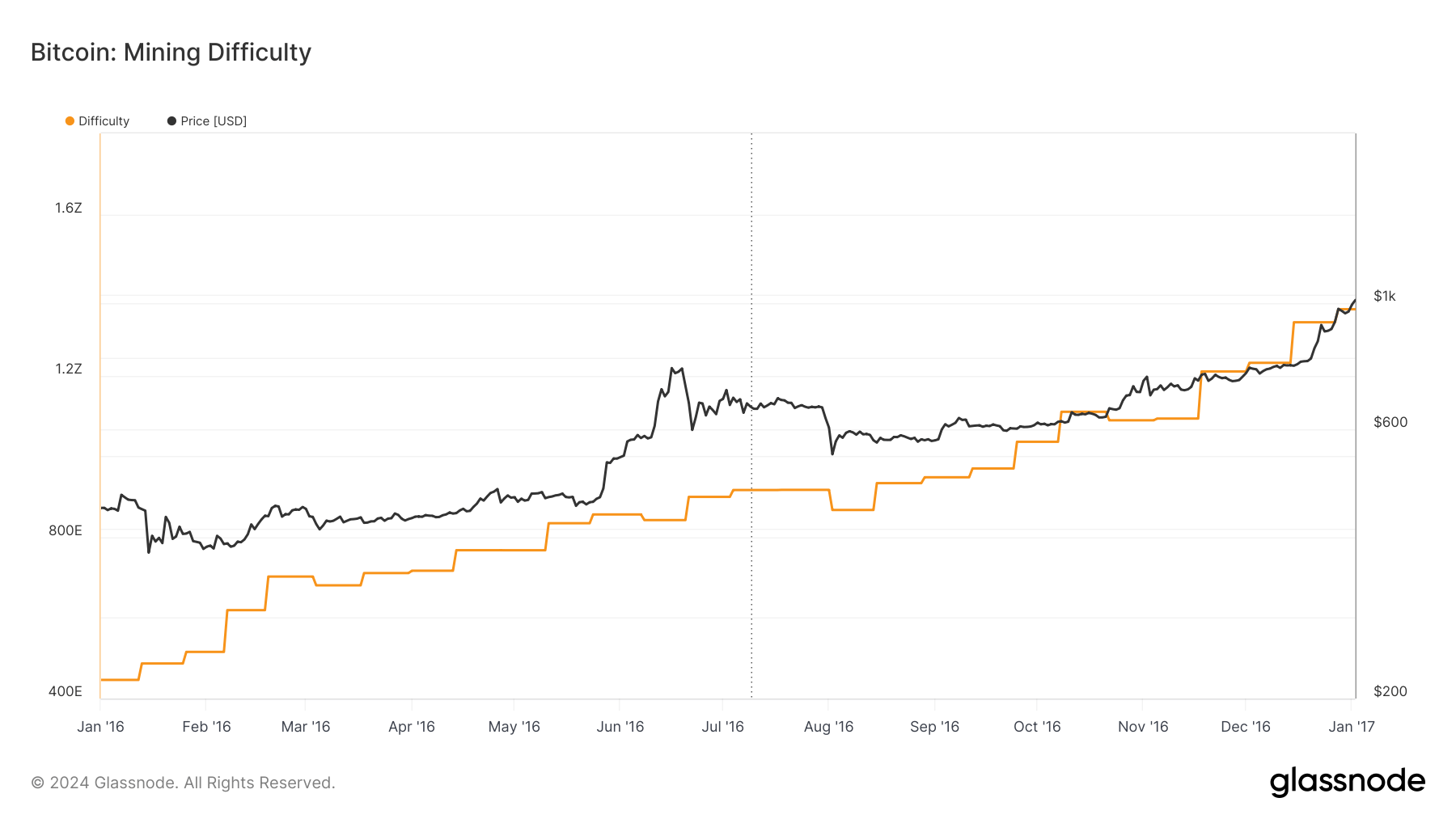

When it comes to mining, the industry has already seen a shift from GPUs and FPGAs to more powerful and efficient ASIC miners. These devices were designed specifically for mining Bitcoin and represented significant capital investment, much higher than the hardware used in the early days. By this time, the increased difficulty level of the Bitcoin network meant that mining had become less profitable for individual miners, and the rise in ASIC hardware and its high price pushed mining towards industrial-scale operations.

Graph showing the Bitcoin mining difficulty from Jan. 1, 2016, to Jan. 1, 2017 (Source: Glassnode)

The second halving in 2016 occurred during these very different market circumstances and had a significantly higher impact than the previous one. With the block reward halving from 25 BTC to 12.5 BTC, the market was ripe with speculation, leading to significant volatility in Bitcoin’s price before the halving. This speculative run-up was supported by the broader understanding of Bitcoin’s supply constraints and its potential impact on prices.

As the block reward halved and the network continued seeing increased traffic, transaction fees began to represent a more significant portion of miner revenue. This was a natural shift intended by Bitcoin’s design to compensate for the decreasing block rewards. However, despite the increase in transaction fees, the immediate aftermath of the halving saw concerns about the profitability of mining operations. However, the rising Bitcoin price and increasing efficiency of ASIC mining hardware helped offset the reduced block reward.

2020

Bitcoin’s third halving took place during exciting and volatile times. This period differed greatly from the previous halvings due to Bitcoin’s maturity as a financial asset and the global economic landscape.

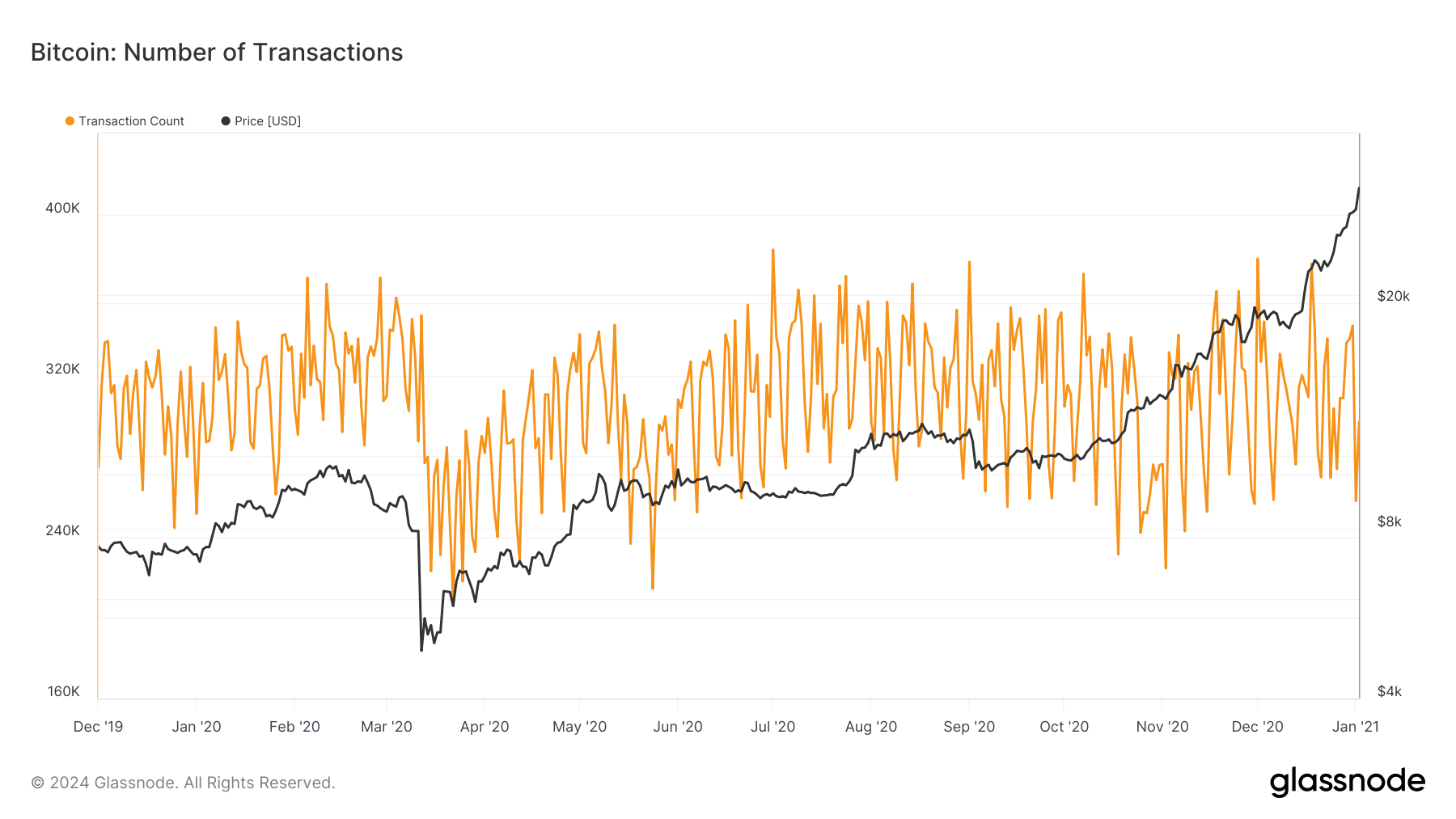

By May 2020, Bitcoin transactions grew steadily, often exceeding 300,000 per day. The growth reflected broader adoption among general users and increased Bitcoin transfers — both as a means of payment and for trading.

Graph showing the number of transactions on the Bitcoin network from Dec. 1, 2019, to Jan. 1, 2021 (Source: Glassnode)

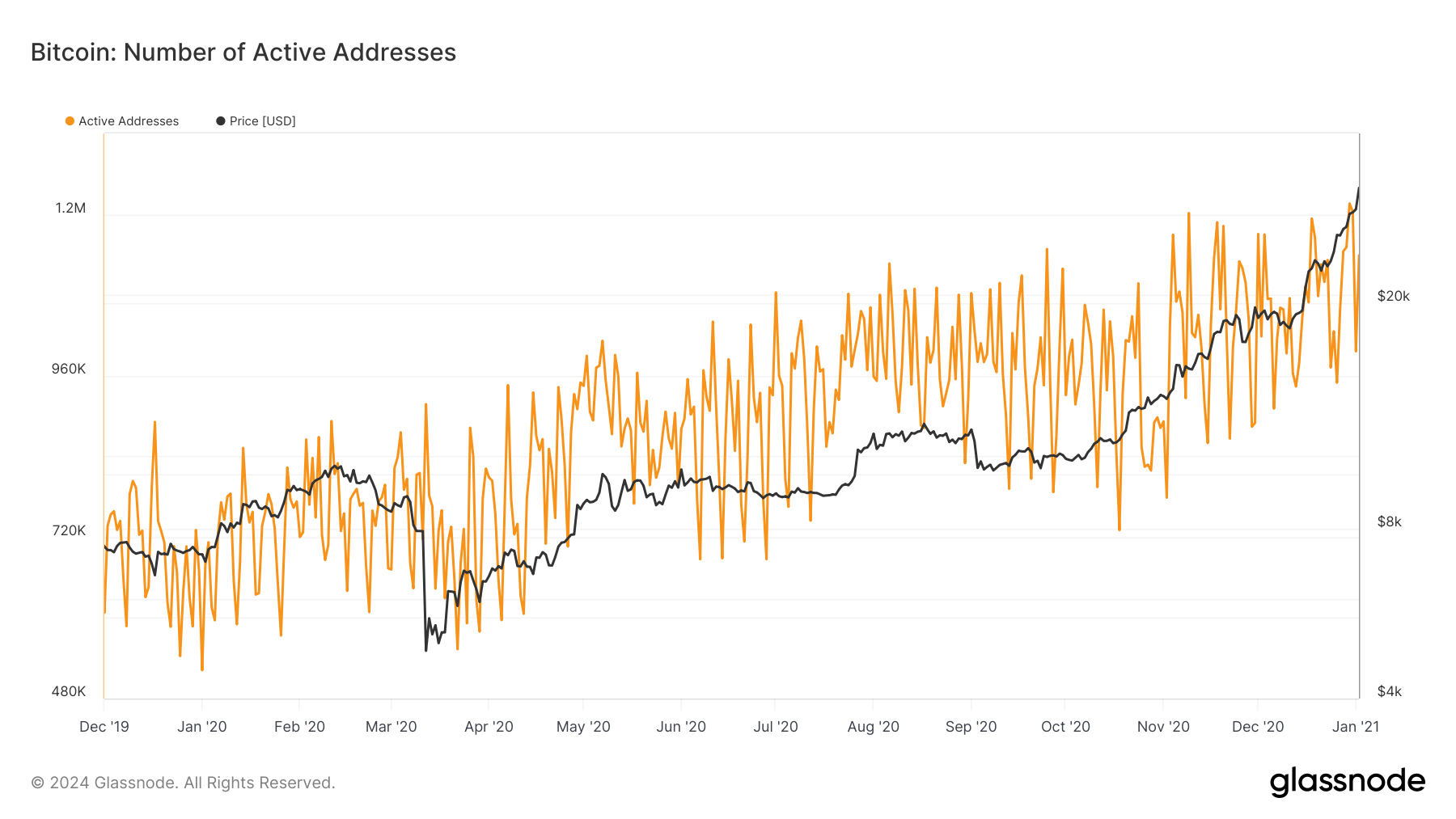

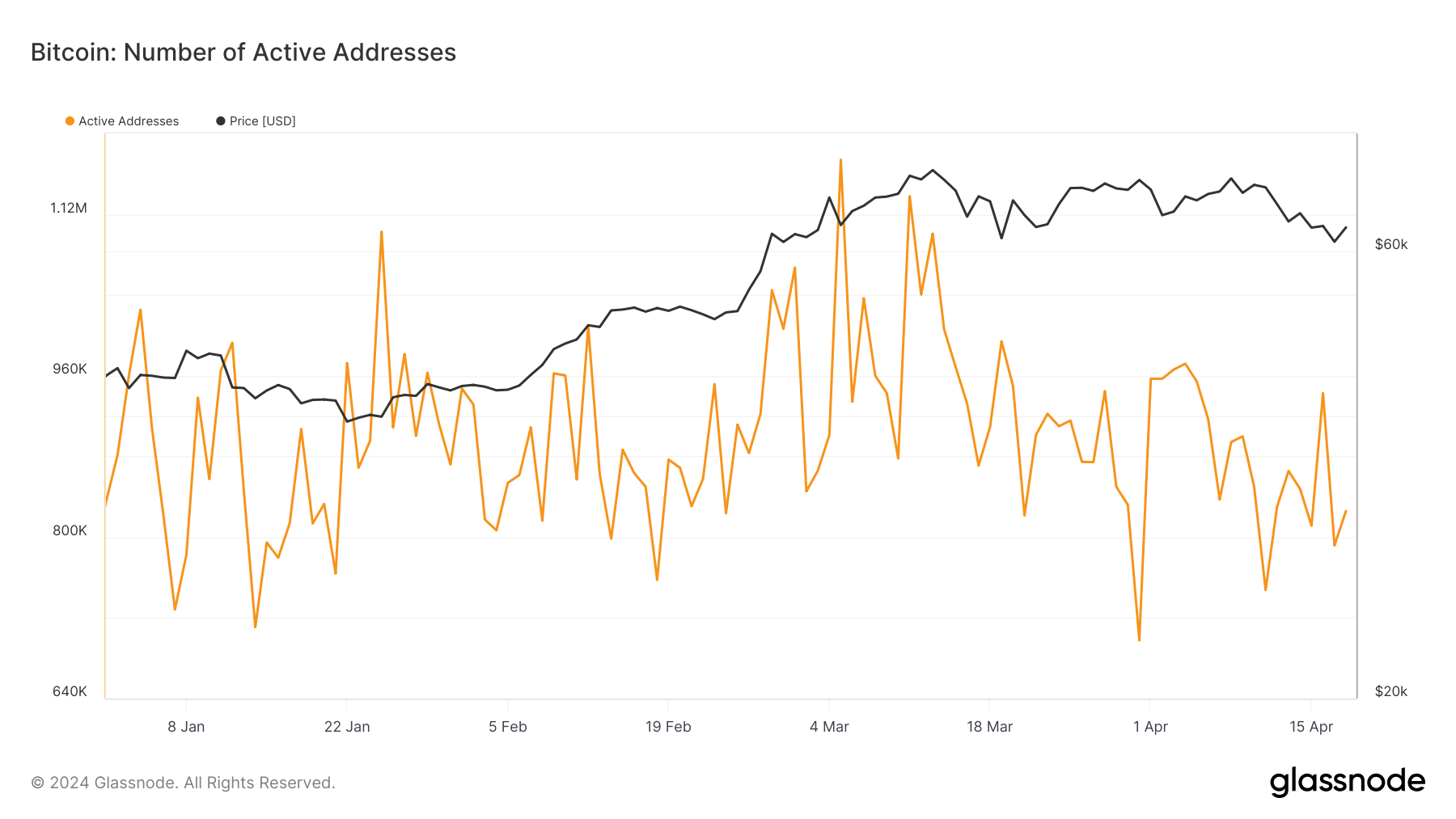

The user base expanded significantly to include the retail market and institutional investors. This was seen in the growth in popularity of institutional investment instruments like GBTC at the time, as well as a broader industry push for ETFs and more regulation.

Graph showing the number of active addresses on the Bitcoin network from Dec. 1, 2019, to Jan. 1, 2021 (Source: Glassnode)

Due to the increasing hash rate, Bitcoin mining has become highly institutionalized with advanced ASIC miners and significant capital requirements. Some large mining operations are now listed on NASDAQ and other large exchanges, adding another level of complexity to the industry.

By this period, mining operations were predominantly large-scale facilities, often located in regions with low electricity costs, such as China. Large players dominated the industry, and the competition had pushed the efficiency of mining operations to new heights. Mining pools were common, allowing smaller players to participate profitably by combining their computational resources.

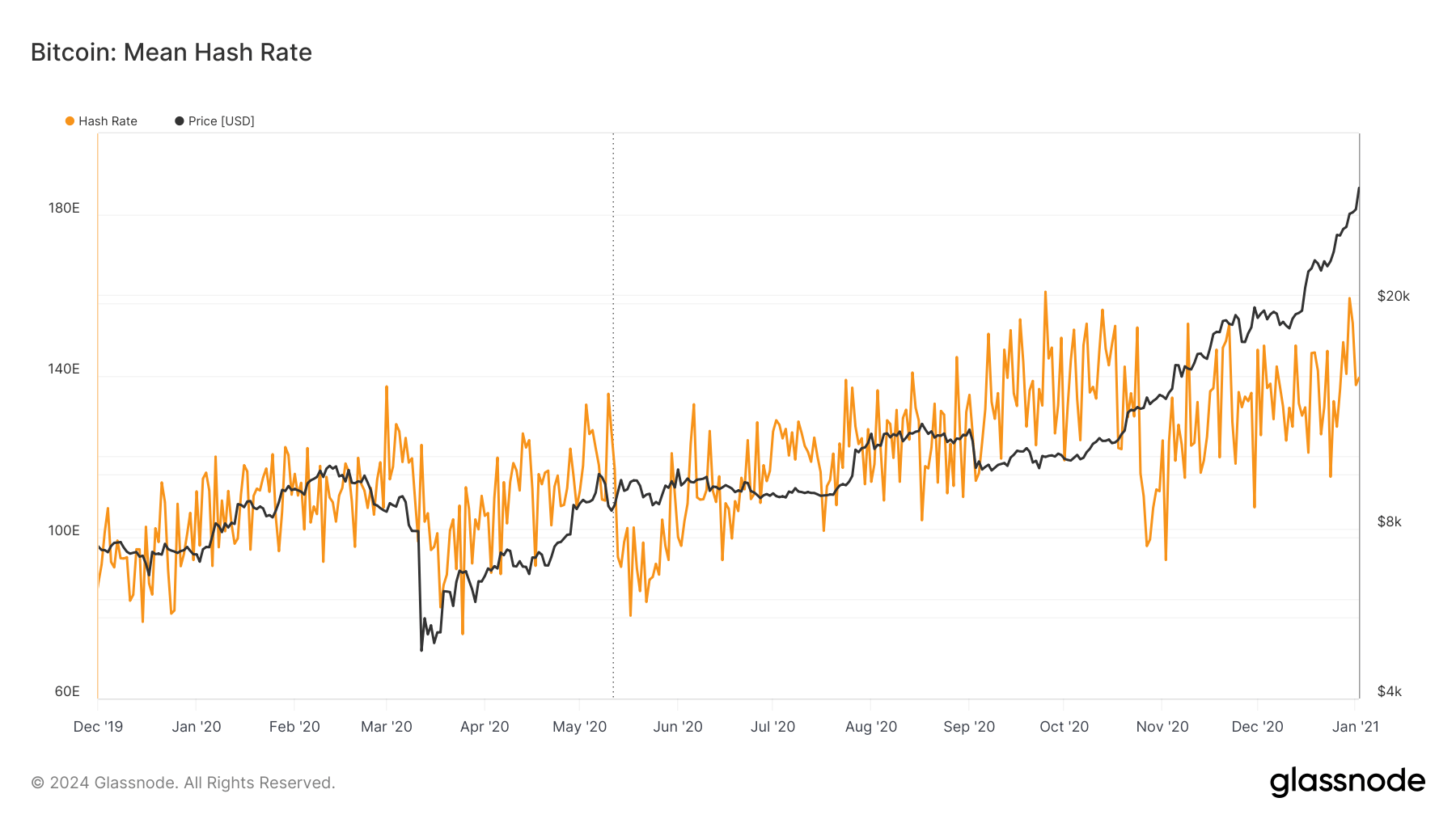

Graph showing Bitcoin’s hash rate from Dec. 1, 2019, to Jan. 1, 2021 (Source: Glassnode)

Despite the stark difference in the observed on-chain metrics, it’s hard to understand the difference between the crypto market in 2016 and 2020. The last halving occurred in a unique economic and social environment, just two months after the beginning of the COVID-19 pandemic.

Markets across the board experienced a significant tumble as the pandemic spread worldwide, with some posting the biggest losses in over 30 years. Bitcoin dropped from $10,500 in mid-February to as low as $5,000 on March 9, 2020 — wiping out billions from the crypto market.

However, by July, BTC had regained all of its losses and began a rapid rise that many predicted would happen in the year following the halving. The global economic uncertainty during the pandemic certainly played a part in this, as Bitcoin quickly became a safe-haven asset, attracting many new and institutional investments.

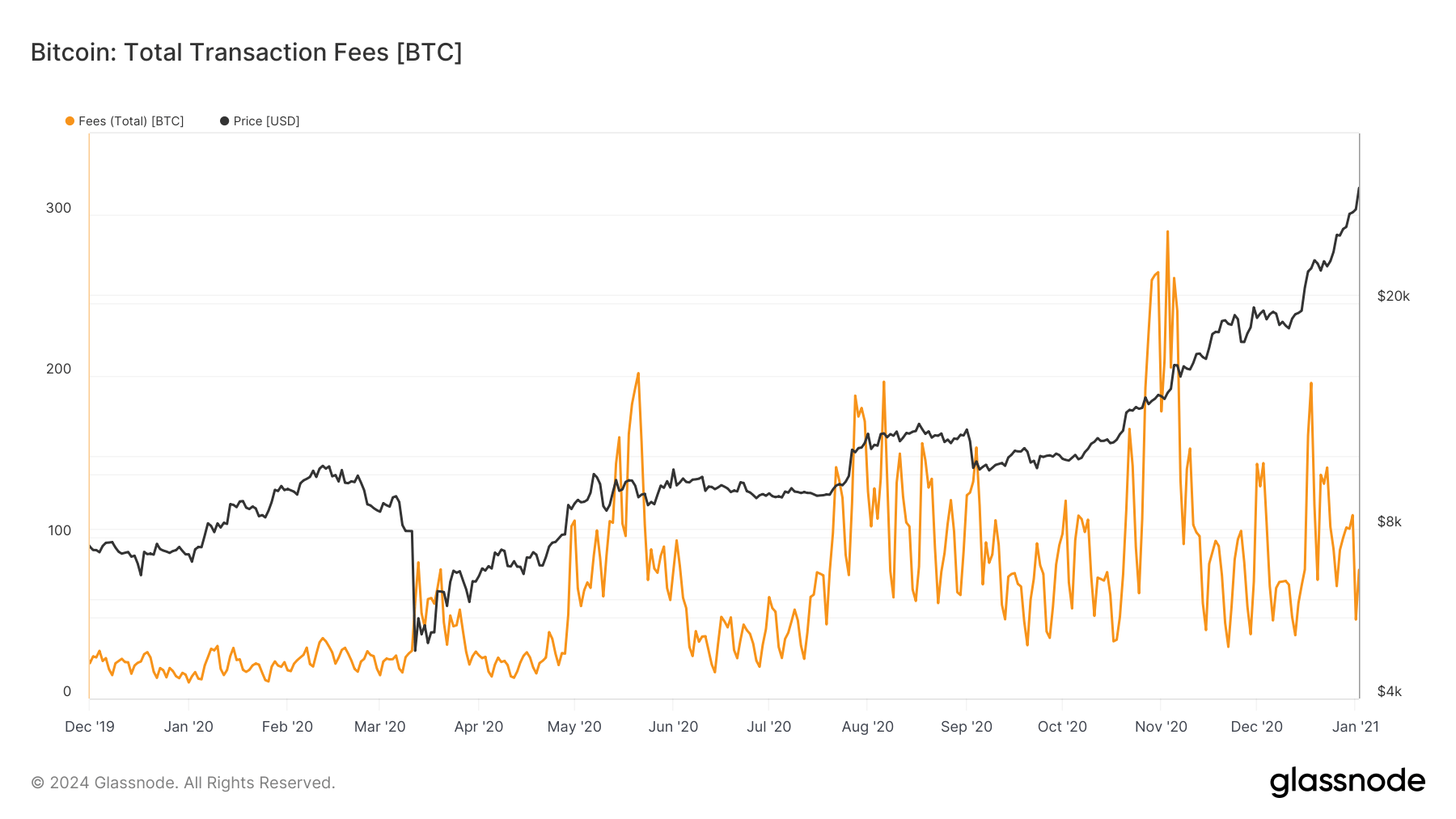

Despite concerns over miner profitability due to the halved rewards, the rising Bitcoin price post-halving helped sustain the mining industry. Transaction fees also increased, partially compensating for the reduced block reward.

Graph showing the total transaction fees on the Bitcoin network from Dec. 1, 2019, to Jan. 1, 2021 (Source: Glassnode)

2024

The maturity and complexity of the crypto market seem to grow exponentially with each halving. Bitcoin’s maturity in 2024 is reflected in the amount, availability, and popularity of sophisticated financial products connected to BTC and a more profound understanding of its long-term value proposition.

Spot Bitcoin ETFs played a pivotal role in Bitcoin’s mainstream adoption, leading to the 2024 halving. They facilitated incredible institutional and retail participation, providing a regulated and familiar avenue for investing in Bitcoin. These instruments have attracted significant capital inflow from traditional investors looking for exposure to crypto as an asset class.

However, their popularity also created a looming danger of a drastically reduced supply available for trading. As the total supply of Bitcoin inches closer to its cap of 21 million, the declining availability of new coins is becoming a critical factor influencing the market. Each halving reduces the supply of new bitcoins, intensifying scarcity and potentially driving up the price if demand remains steady or increases. This scarcity effect is magnified by the substantial holding of bitcoins by long-term investors and institutions, which reduces the active circulation further and could amplify price volatility around the halving.

Transaction fees have been increasing this year and are expected to explode around the time of the halving. Historically, the event has led to increased fees as miners seek to compensate for the loss of block rewards by prioritizing higher-fee transactions. However, the significance of this halving will see traders, institutions, and miners racing to have their transactions or inscriptions included in the coveted block 840,000, at which the mining reward halves.

Bitcoin has over 825,000 active daily addresses as of April 19, with a peak of over 1.1 million active addresses recorded on March 5 this year.

Graph showing the number of active addresses on the Bitcoin network from Jan. 1 to April 18, 2024 (Source: Glassnode)

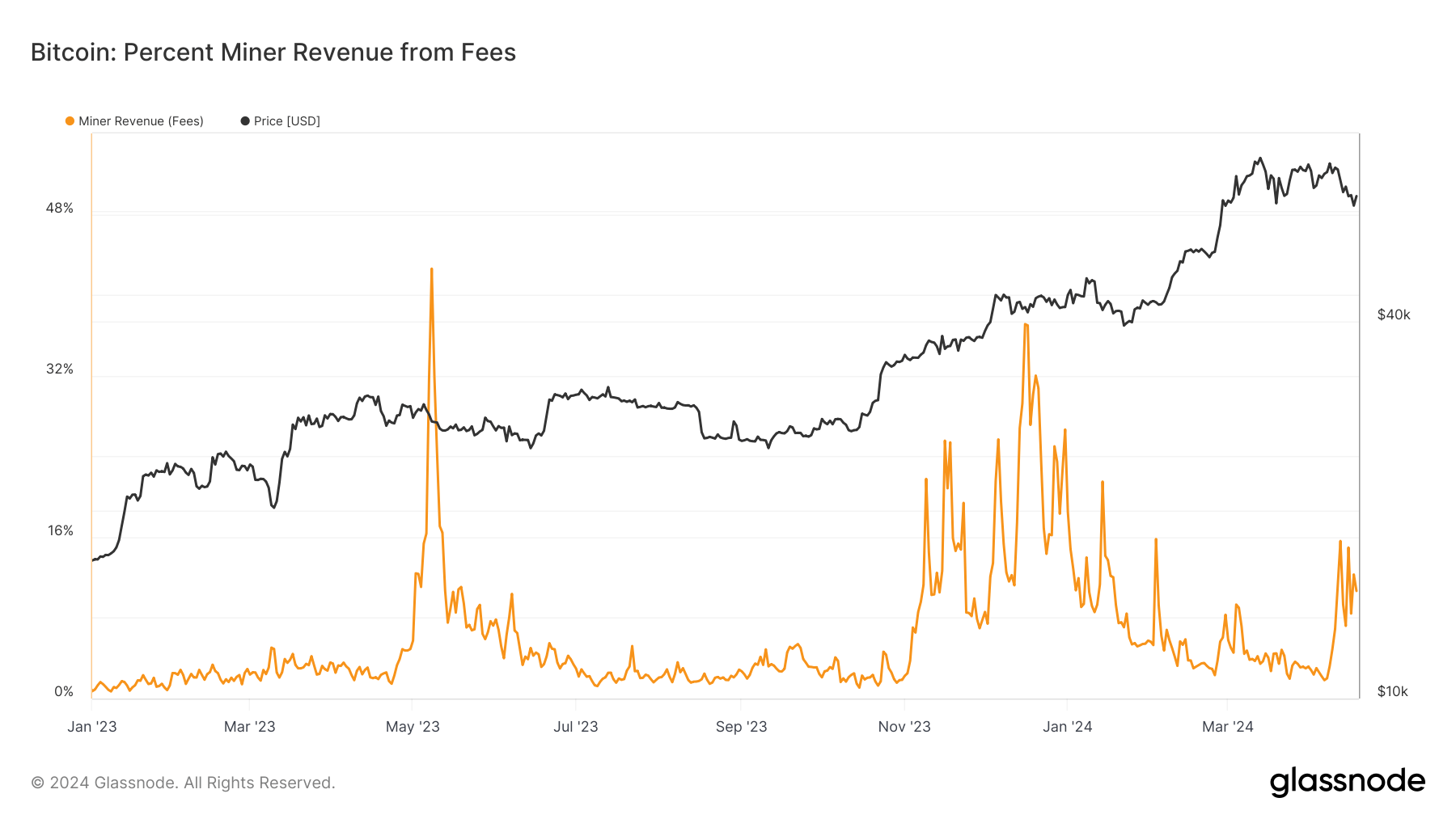

The fees paid to the network are also unprecedented. While the introduction of Ordinals theory and inscriptions pushed these fees to new highs last year, when the hype dried down, the fees remained consistently elevated, accounting for a higher percentage of miner revenue this year.

Graph showing the percent of miner revenue coming from fees from Jan. 1, 2023, to April 19, 2024 (Source: Glassnode)

Conclusion

Given the current conditions surrounding the upcoming halving, we can anticipate several key outcomes. Firstly, the reduced block reward will tighten the supply of new coins, which could exert upward pressure on Bitcoin’s price due to ongoing strong demand. However, this effect may be tempered by market volatility in the short term, mirroring past halving events.

Furthermore, we can expect a significant increase in transaction fees as network activity heightens around and at the time of the halving. Aside from compensating miners to some extent for the reduced block rewards, this will most likely create notable congestion when processing transactions as most of the market won’t be able or willing to pay a high fee to process a low-value transaction.

Higher fees may lead to greater emphasis on scaling solutions like the Lightning Network as users turn to cheaper, more efficient transaction options.

Finally, the involvement of institutional investors, coupled with the broadening appeal of Bitcoin ETFs, could potentially stabilize the market after the halving. Nevertheless, the market should remain prepared for significant price fluctuations, as historical trends have shown pronounced movements following past halvings. As such, the post-halving period will be critical for Bitcoin, reflecting its growing mainstream acceptance and the complex interplay of forces that now dominate the market.